Travelzoo (NASDAQ: TZOO) – Q3 2025 Earnings

Travelzoo (NASDAQ: TZOO) – Q3 2025 Earnings

Earnings Release Date: Oct. 28, 2025

Stock Price: $10.04

Market Cap: $116.6 million

Q3 2025 sales of $22.2 million vs $20.1 million in the prior year

Q3 2025 EPS of $0.01 vs $0.26 in the prior year

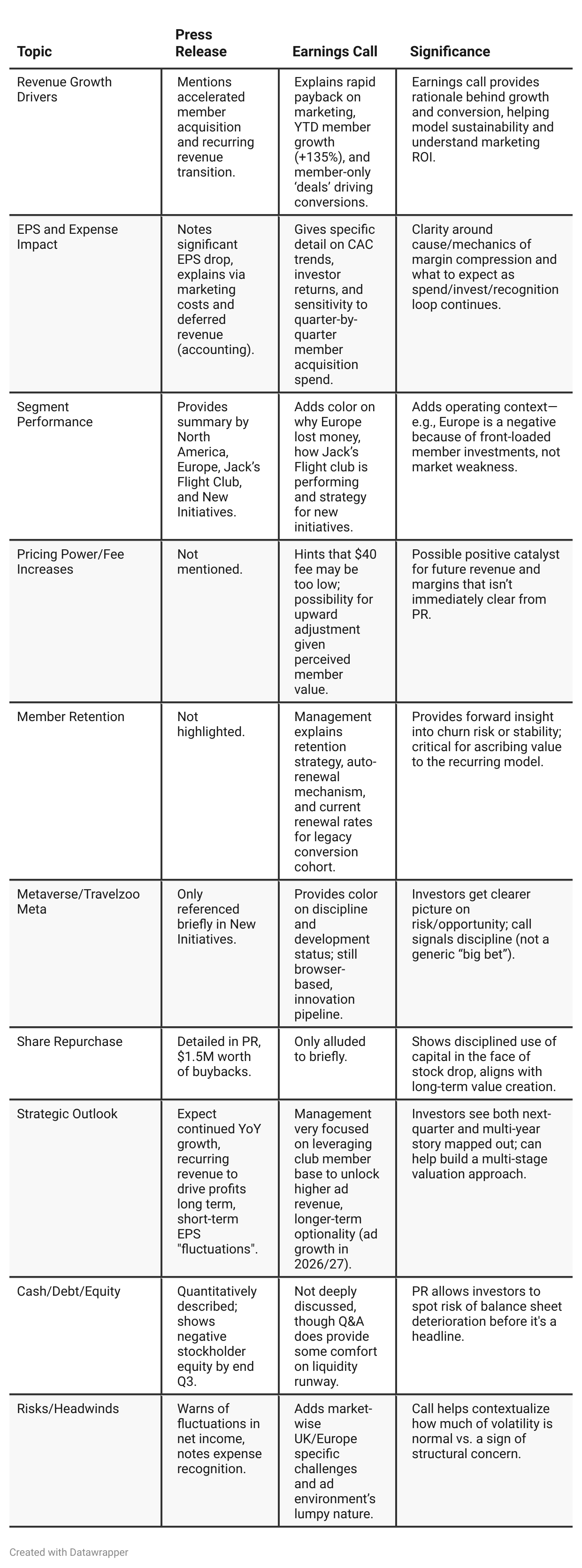

Press Release vs Call Transcript Comparison

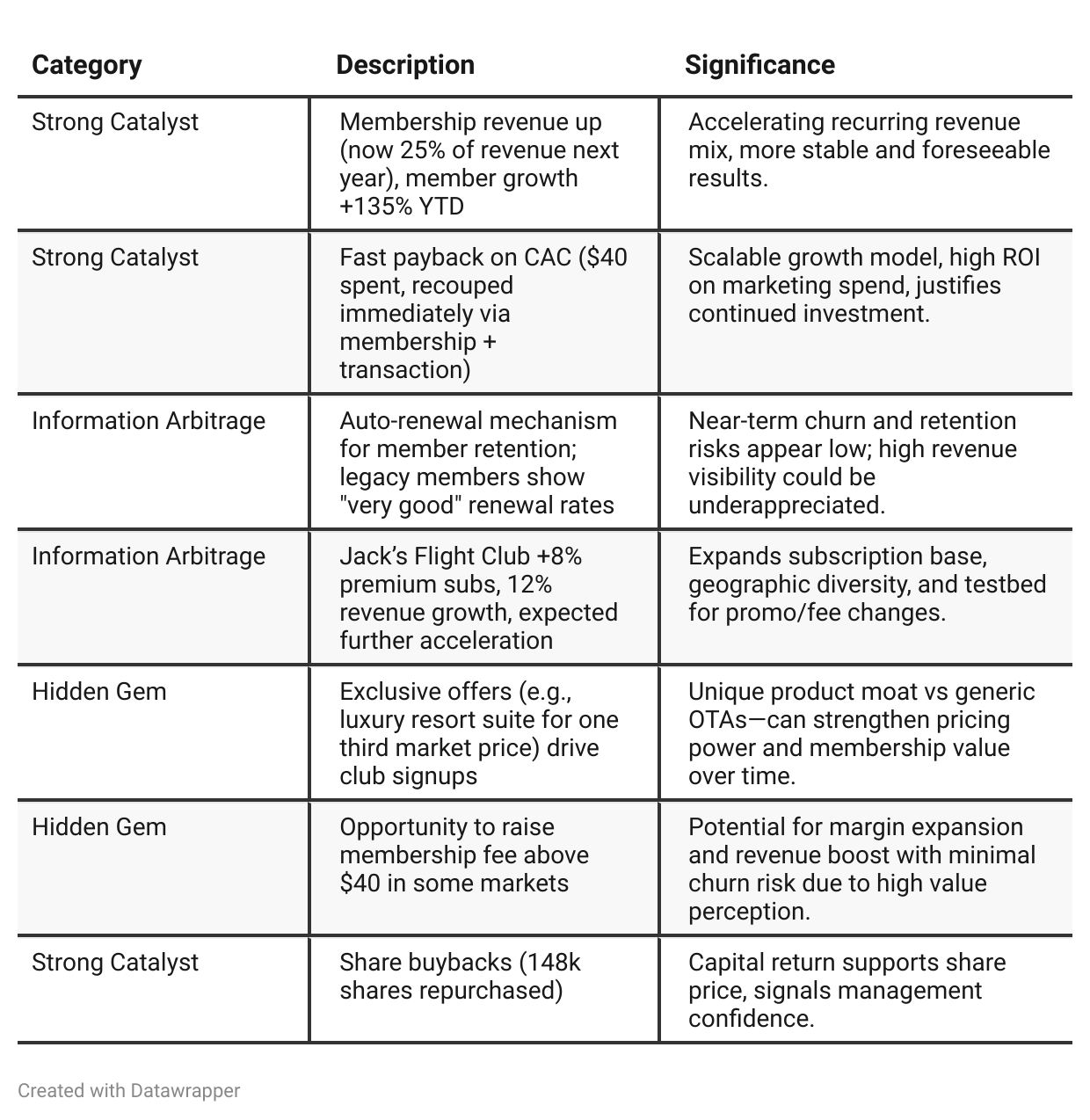

Business Model Transformation: Both documents indicate Travelzoo is successfully shifting from an ad-reliant business to a recurring, subscription-driven one—an arguably higher-quality revenue mix.

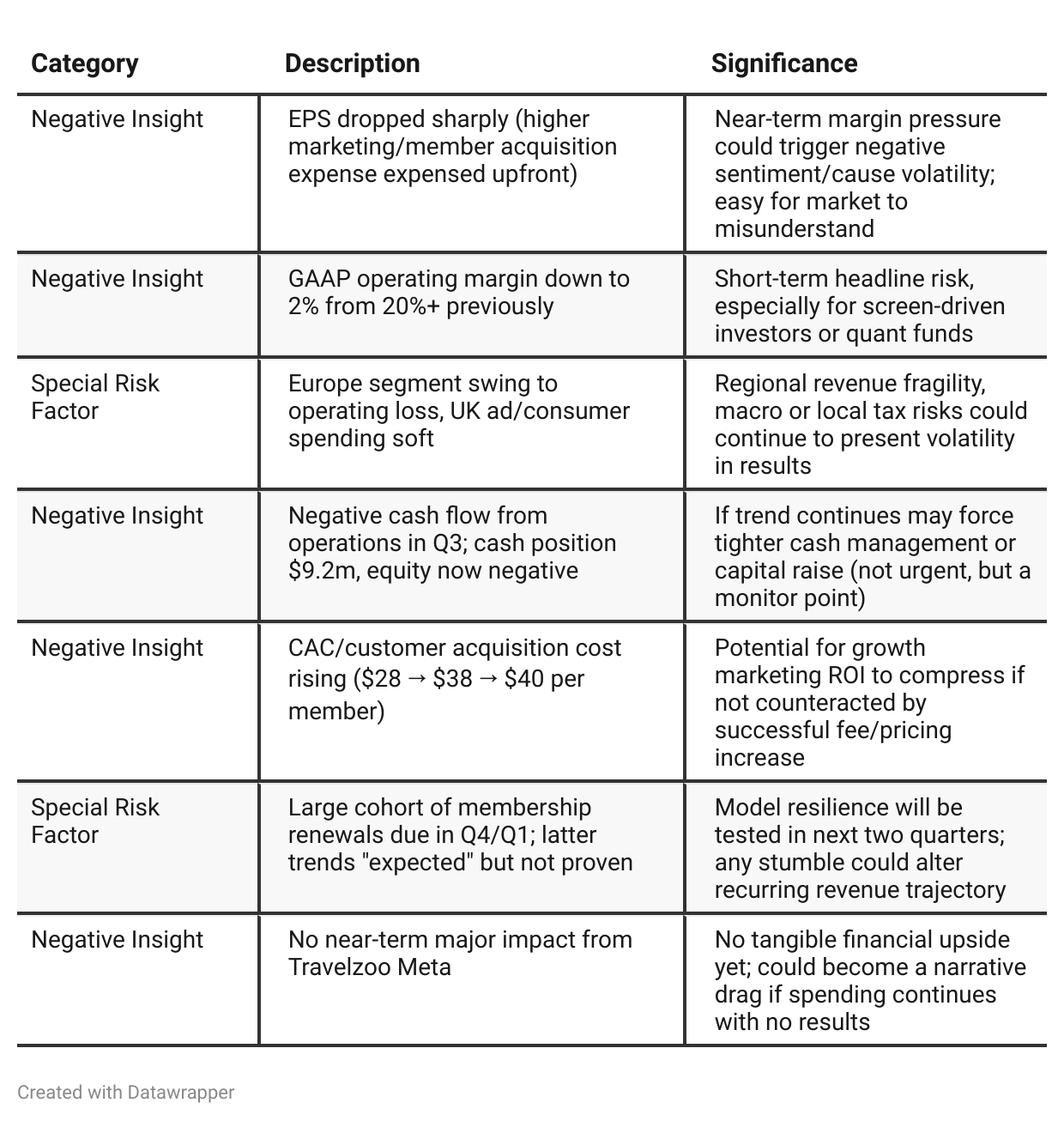

Margin Reset but Poised for Expansion: Short-term compression in operating profit/margins is strategic to build a sticky, high-LTV member base; margins likely to expand as marketing spend moderates and renewal base grows.

Buyback as Signal: Aggressive Q3 buybacks support share price and signal management confidence.

Metaverse/Innovation Option: While not immediate, the “Meta” project is being developed cautiously, offering long-term narrative upside if Metaverse/VR travel trends revive.

Regionally Nuanced Risks: Europe softer due to tax/public spending uncertainty; North America is a bigger bright spot.

Liquidity OK for Now: Despite negative cash from ops in Q3, management is not flagging immediate concern and is reducing merchant payables.

Retention Metrics Key for Q4/Q1: The large member renewal cohort at year-end and start of 2026 is the next major test for the model.

Positive Insights

Negative Insights

Tariff Risk

No mention of U.S. tariffs, trade policies, or related risks in the transcript. No discussion of supply chain, pricing, market share, or innovation impacts from tariffs. No actions described to mitigate tariff risk. Investors concerned with tariff exposure can deprioritize this risk based on this transcript.

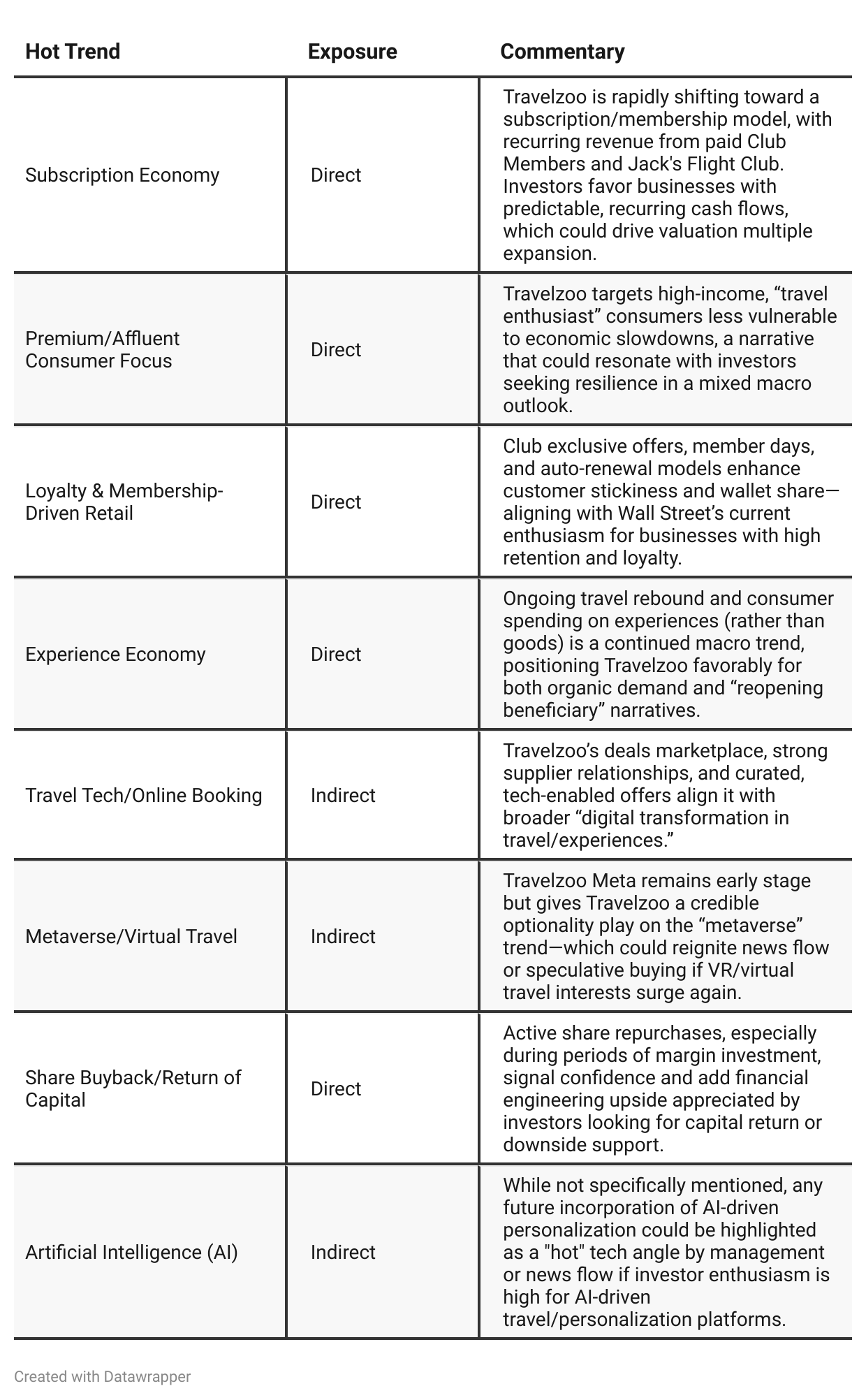

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025: Travelzoo is in full-scale transformation, pivoting from ad-based travel deals to a subscription “club for travel enthusiasts.” The strategy focuses on adding new paying members via aggressive marketing spend backed by immediate and favorable payback economics. The company is taking advantage of excess inventory in a weak travel market to craft compelling offers that drive high-contribution member growth. There’s optimism about future profitability as recurring revenue ramps and more legacy members convert. Retention insights are still in early days, and price increases are only mentioned as a possibility for the future.Q3 2025: The narrative doubles down: Travelzoo now frames itself as “the must-have membership for travel lovers,” intensifying the focus on exclusive offers, high spenders, and club value—distancing itself from price-sensitive travel. The company faces margin and cash flow compression from frontloaded marketing, but management remains confident that retention will prove the strategy right and profitability will rebound as recurring revenues mature. More attention is placed on retention mechanics (auto-renew), impending renewal “waves,” and the ability to raise membership fees soon. Macro headwinds in the UK/Europe are now discussed more candidly, and there’s more acknowledgment of near-term volatility—even as management insists this is a temporary effect required for long-term value creation.

Year-over-year comparison

In Q3 2024, Travelzoo was entering a strategic transition: preannouncing major changes as it prepared to shift its member base to a subscription/club fee model in January 2025. The company boasted high margins, robust profit, and a cash-generating business, but much of this was still legacy economic structure and near-term benefit from restrained expense and soft revenue expectations. The subscription promise was future-focused: “prepare for growth and recurring profitability.”

By Q3 2025, Travelzoo’s transformation faced real-world tests. The fee model is not hypothetical—now, the installed base must renew (and at higher prices soon). Management’s tone is less celebratory and more explanatory (at times defensive), justifying heavy acquisition and marketing costs despite shrinking margins and negative cash from ops. Attention pivots acutely to cohort renewal rates, customer stickiness, and the durability of the new recurring economics. Macro headwinds (UK/Europe vs. US) loom larger, while the company seeks confidence in high-value, affluent travelers as defensive insulation.

Final Takeaway

Travelzoo is in a growth and transformation phase, pivoting from a traditional ad-driven model to a recurring subscription-driven business built on high-value membership and exclusive deals. Recurring revenues and strong retention offer long-term upside, but short-term EPS/margin volatility and negative cash flow signal risks as the model matures. Real execution on member renewals and cost discipline in the next two quarters will determine if this is a temporary reset or a structural margin improvement story. Verdict: Hold with positive bias; upside hinges on sustained renewal and margin recovery.