Travelzoo (NASDAQ: TZOO) – Q2 2025 Earnings

Travelzoo (NASDAQ: TZOO) – Q2 2025 Earnings

Earnings Release Date: Jul. 23, 2025

Stock Price: $13.70

Market Cap: $159.1 million

Q2 2025 sales of $23.1 million vs $22.0 million in the prior year

Q2 2025 EPS of $0.25 vs $0.31 in the prior year

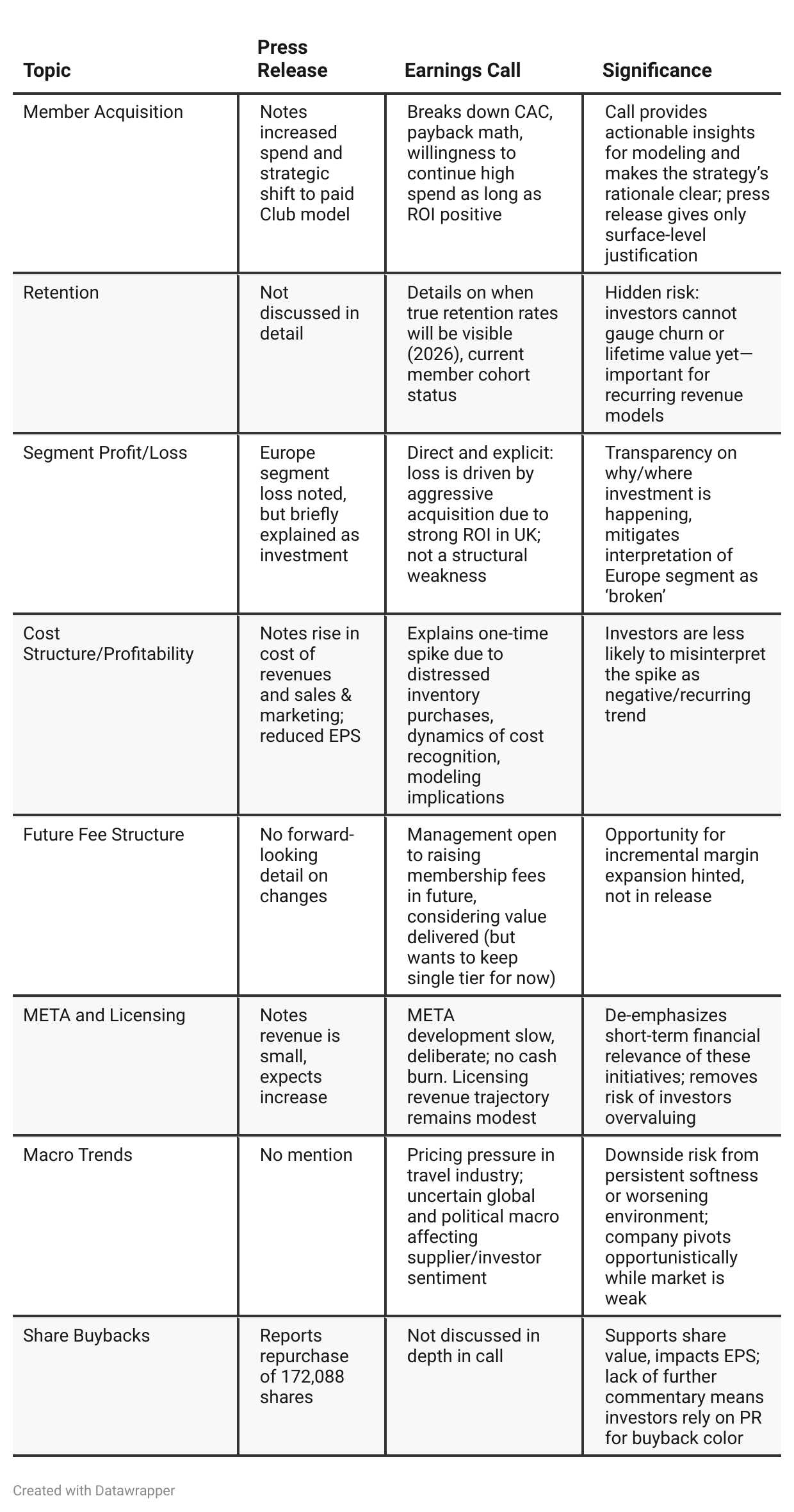

Press Release vs Call Transcript Comparison

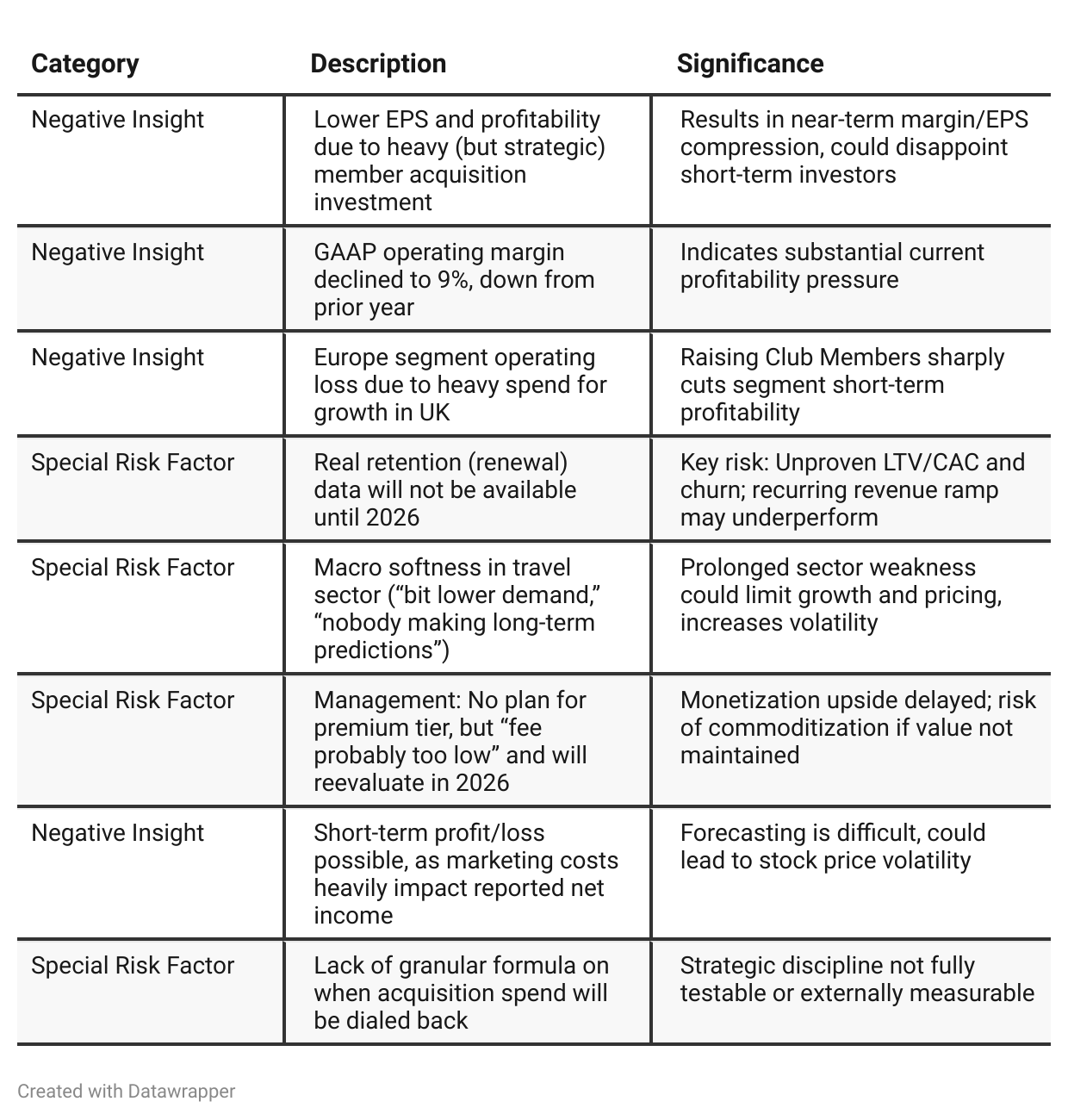

Cash/Balance Sheet Weakness: The press release reveals negative equity and declining cash—investors must consider leverage and liquidity risks, which are not discussed operationally in the call.

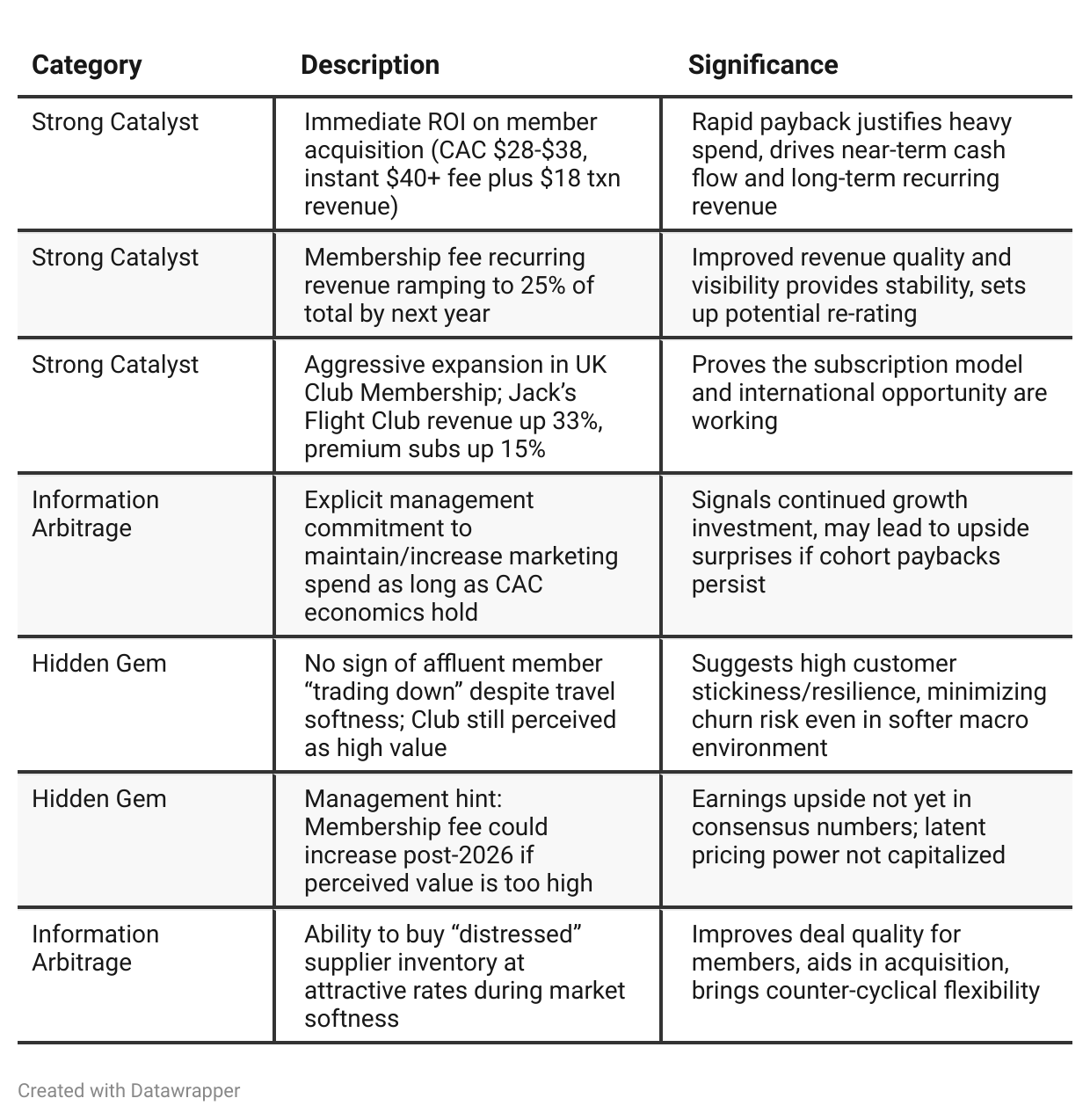

Deferred Revenue Building: Suggests a “bank” of future recognized revenue, providing some stability and predictability as membership matures.

Management Candor: Call management is frank about “cool head” discipline, adaptation to real-time CAC trends, and willingness to pull back if economics worsen.

Soft Macro Can Be Double-edged: Current soft conditions yield cheap inventory, but sustained softness could eventually drag on member renewal/engagement.

Lack of Premium Product… For Now: They acknowledge value is “probably too high” for fee, and fee hike is possible, revealing potential untapped margin lever.

No “Adjustment Fatigue”: Both documents adjust profit for stock comp, amortization, etc.—standard for U.S. tech, but investor caution is warranted on true cash profitability.

Positive Insights

Negative Insights

Tariff Risk

There are no mentions in the Travelzoo Q2 2025 earnings call of U.S. tariffs, trade policies, or related issues. Management did not discuss the impact of tariffs on company revenue, supply chain, or profitability, nor were there any questions from analysts on this topic.

Sentiment Analysis

The overall sentiment toward Travelzoo is bullish. Investors are highlighting strong financial metrics, the company’s transition to a recurring subscription model, rapid payback on customer acquisition, and buybacks as key positives. Several believe the stock is undervalued with significant upside potential if the membership strategy succeeds, and some share long-term price targets and growth projections. While a few raise concerns about historical performance, increased acquisition costs, or short-term volatility, the dominant view focuses on profitability prospects and the high-margin nature of the subscription business.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q1 2025: Travelzoo’s narrative focused on education: Management walked investors through the mechanics and rationale behind the business model transformation from a free/advertising model to a recurring subscription model. They emphasized the need for investment, explained temporary profit/margin pressure, and stressed strategic conversion of their legacy user base into Club Members. The overall tone was explanatory and cautiously optimistic, getting shareholders comfortable with a new direction, new accounting implications, and a longer-term, recurring revenue focus.Q2 2025: The company has shifted to proof and acceleration. Management is assertive about their aggressive acquisition strategy, underpinned by real data showing immediate payback and attractive economics for every new member added. They’re leveraging soft travel market conditions to accelerate growth, especially in Europe, at the temporary expense of margins. While there is acceptance of near-term volatility and some key metrics (e.g., retention rates) will only emerge in 2026, there is a sense of conviction and urgency to scale—pushing the narrative from “please understand our strategy” to “look, it’s working, and we’re going to push harder as long as it does.”

Year-over-year comparison

2024: Travelzoo was setting the stage for a major transition, operating with prudent optimism as it executed the new Club Member strategy and prepped for its make-or-break “conversion year” in 2025. The team was careful—about financials, about customer impact, and about not over-promising. The focus was on maintaining strong margins and cash as a foundation for change.

2025: A sharply more confident and aggressive stance—the company is going all-in on paid membership growth, with clear evidence that acquisition economics are compelling and that the new model is gaining traction. Management is now fighting for market share, acknowledging (and welcoming) current margin compression as part of the plan. The transition that was once theoretical is now real, tracked by hard numbers and purposeful action, with early signs of success but some critical execution risks (renewal/retention) yet to play out.

Final Takeaway

Travelzoo is in a growth investment phase pivoting to a recurring subscription/membership model. Management is executing a strategy of near-term profit sacrifice for highly efficient user acquisition with fast payback and strong potential for future recurring revenues and margin rebound—especially as membership fees are expected to comprise a quarter of future revenue. However, retention and full recurring model viability remain unproven until 2026 cohorts become visible. Investors should focus on cash flow trends, acquisition efficiency, and any updates on early renewal rates. Verdict: Hold—with substantial medium-term upside if subscriptions prove sticky, but uncertainty persists until cohort economics are visible.