Tyson Foods, Inc. (NYSE: TSN) – Q4 2025 Earnings

Tyson Foods, Inc. (NYSE: TSN) – Q4 2025 Earnings

Earnings Release Date: Nov. 10, 2025

Stock Price: $52.68

Market Cap: $18332.6 million

Q4 2025 sales of $13,860 million vs $13,565 million in the prior year

Q4 2025 EPS of $1.15 vs $0.92 in the prior year

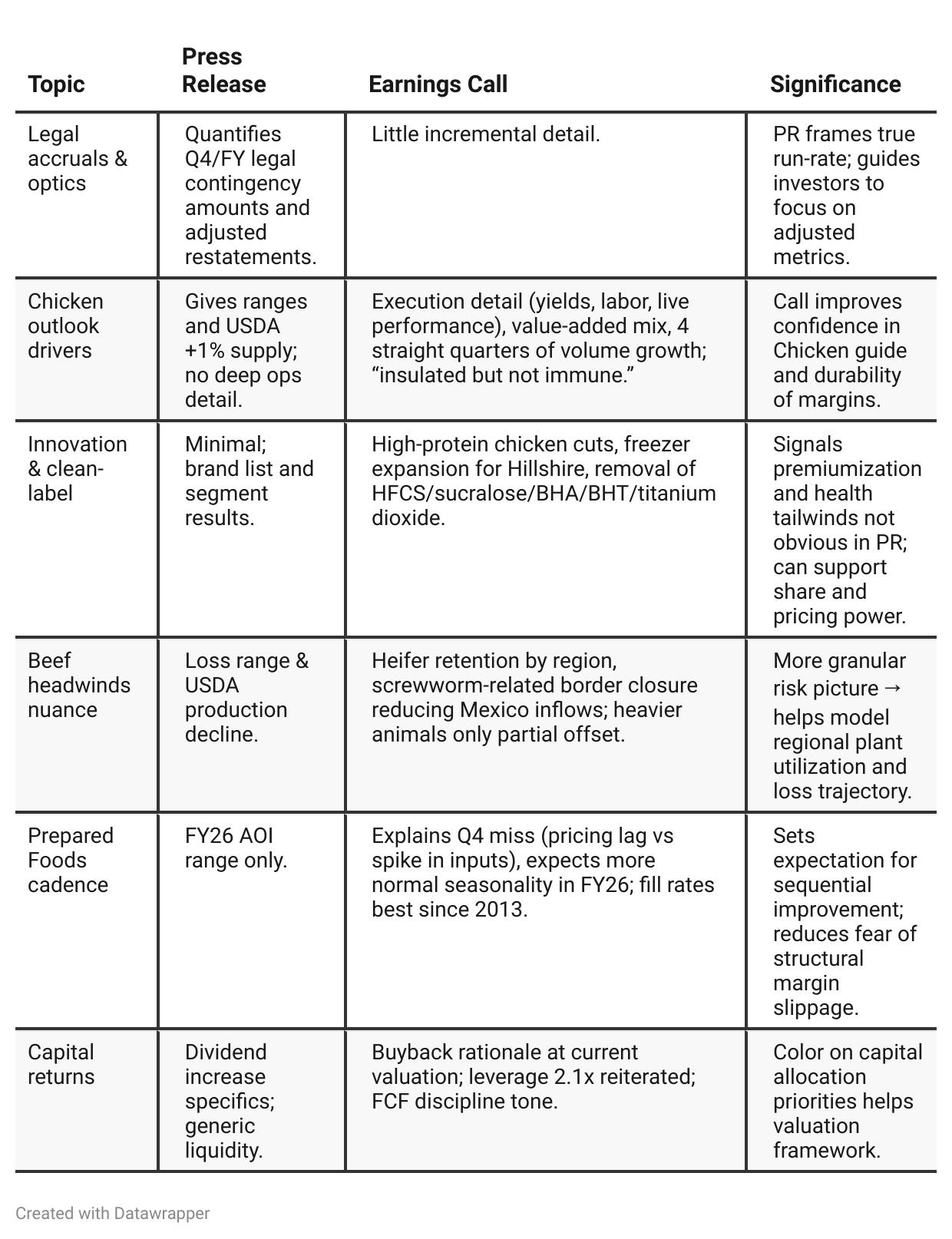

Press Release vs Call Transcript Comparison

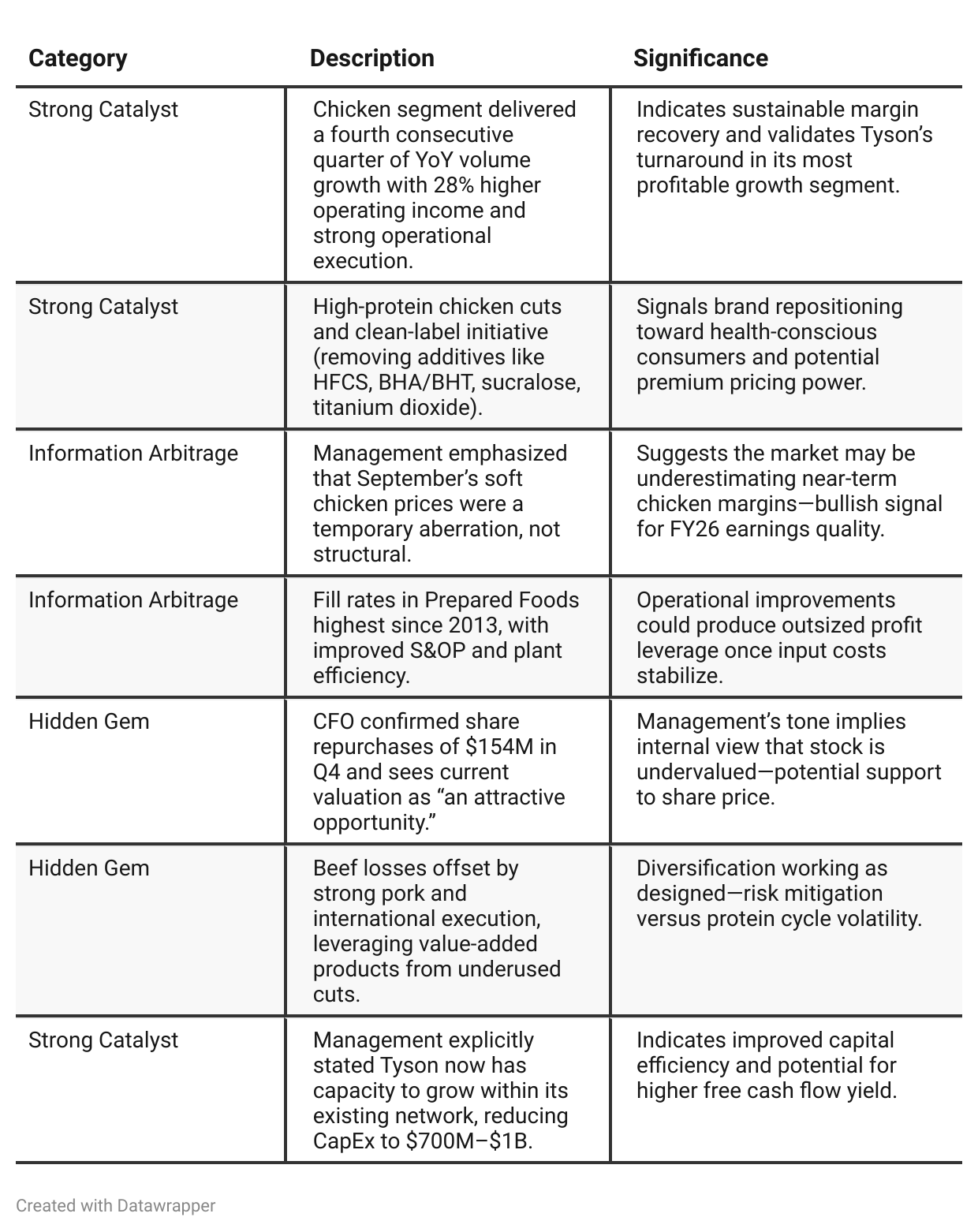

Portfolio hedge working as designed: Chicken strength + Prepared Foods resilience offset cyclical Beef trough.

Distribution/service recovery (best fill since 2013) + brand penetration (~72% of US households) suggests stickier retail demand into FY26.

Lower CapEx after a heavy five-year build implies room to grow within the existing network, aiding FCF and potential ongoing buybacks/dividends.

Positive Insights

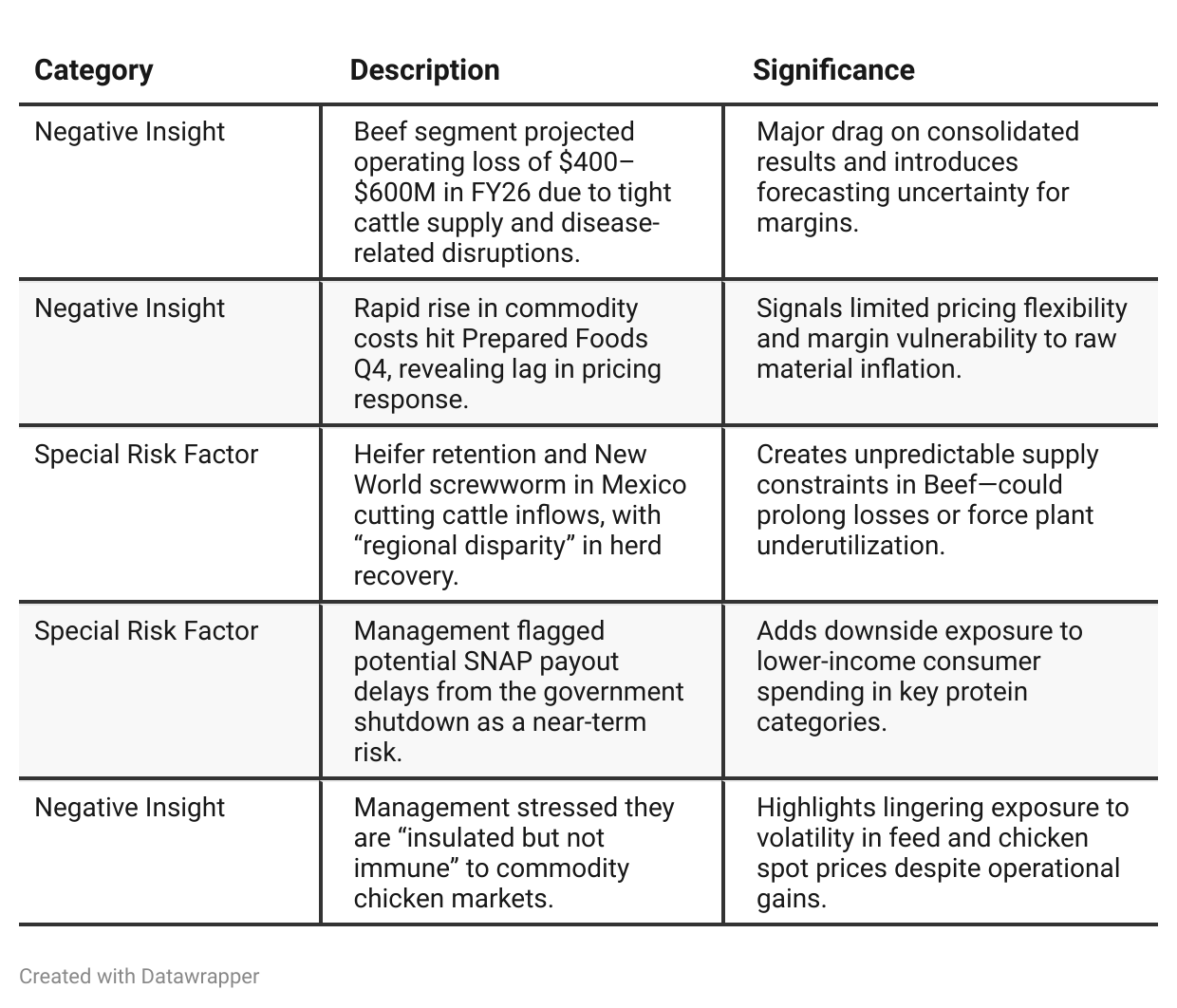

Negative Insights

Tariff Risk

Tyson management explicitly noted that tariffs are “less of an issue” in this cycle. No evidence of significant impact from U.S. trade policy on operations, pricing, or market share was mentioned. The company did not cite any mitigation measures, implying neutral to minimal exposure at present.

Conclusion: Tariff risk currently immaterial to Tyson’s 2026 outlook. Focus remains on domestic protein mix and operational execution.

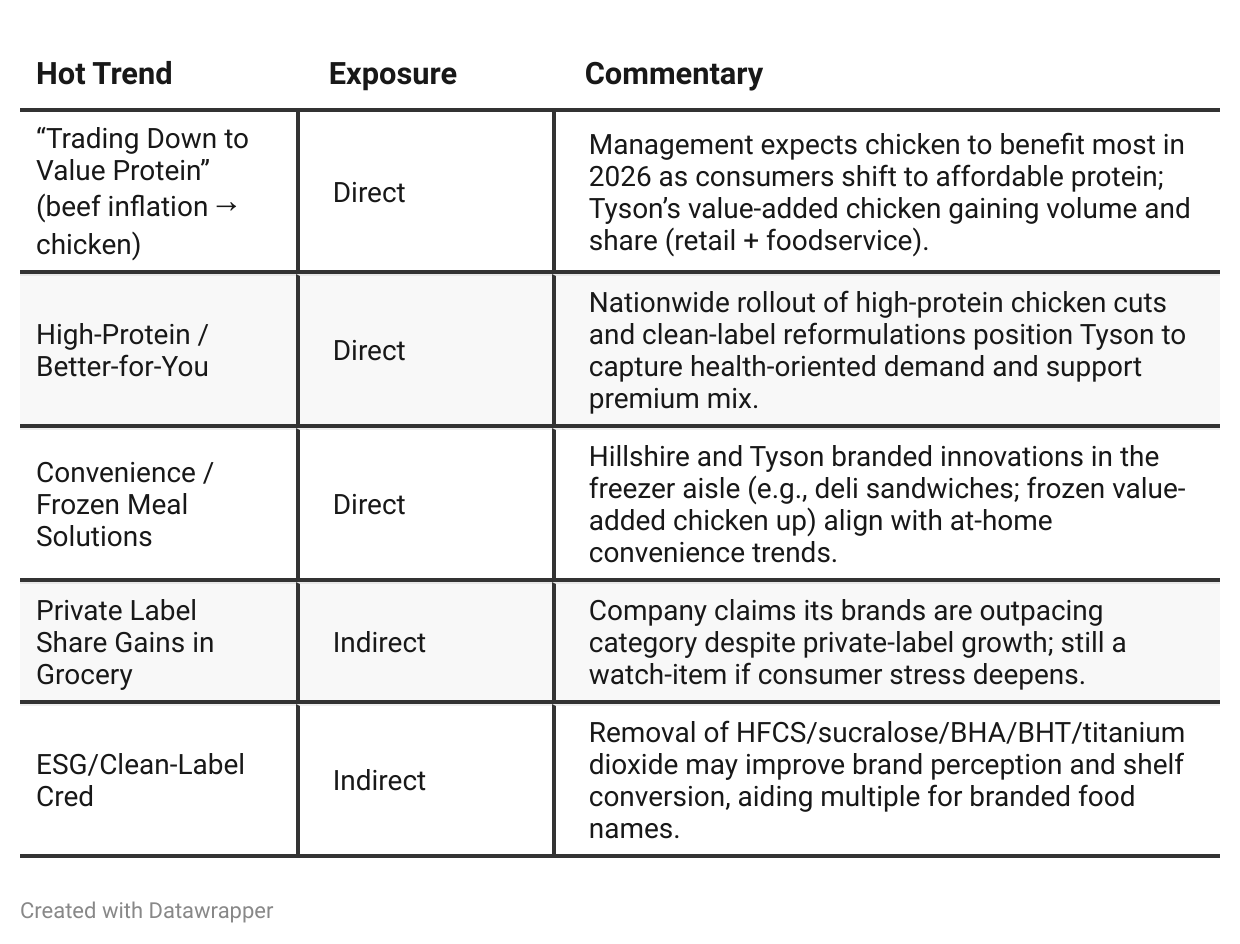

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

From Q3 to Q4, Tyson’s story moves from “validated turnaround & higher FY25 guidance” to “confidence in a brand/innovation-led FY26 with a clearer risk map.” Q3 was about operational wins (value-added mix, margin rebuild, buybacks resuming). By Q4, management layers on consumer-brand levers (clean-label, high-protein, Gen-Z reach), formalizes FY26 segment guides, and is more explicit on near-term headwinds (legal reserve optics, Prepared Foods cost lags, SNAP timing, Mexico border constraints). Chicken remains the core growth/earnings engine; Beef remains the cyclical drag, now described with finer regional and import dynamics.Year-over-year comparison

Between Q4 FY2024 and Q4 FY2025, Tyson Foods’ narrative transitions from turnaround and repair to renewal and acceleration.

In 2024, management’s focus was on stabilizing Chicken operations, cutting costs, and restoring credibility after a difficult 2023. The tone was operational, inward-looking, and framed around fixing execution problems.

By 2025, Tyson has regained control of its operations and earned the right to talk growth. The discussion shifts decisively toward innovation, brand leadership, and consumer relevance—with Chicken now a proven growth engine and Prepared Foods ready for mix-driven margin gains.

Risks evolve from internal execution to external factors (beef supply, macro headwinds, legal contingencies), reflecting a company that has structurally improved but still operates in cyclical markets.

The financial narrative matures from “stabilize cash” to “deploy cash”—with buybacks, sustained dividend growth, and reduced CapEx marking a transition to capital efficiency.

Final Takeaway

Tyson Foods (TSN) is in a stabilization-to-growth phase. Operational discipline and innovation are improving performance in Chicken and Prepared Foods, offsetting cyclical Beef headwinds. Management’s confidence in valuation and cash returns underscores balance sheet strength.

While protein demand and clean-label positioning offer tailwinds, investors must monitor commodity volatility and cattle supply constraints. Execution on cost control and Prepared Foods margin recovery will define FY26 outcomes.

Verdict: BUY, with moderate upside contingent on sustaining Chicken profitability and Beef loss containment.