Tyson Foods, Inc. (NYSE: TSN) – Q3 2025 Earnings

Tyson Foods, Inc. (NYSE: TSN) – Q3 2025 Earnings

Earnings Release Date: Aug. 4, 2025

Stock Price: $52.53

Market Cap: $18280.4 million

Q3 2025 sales of $13.8 billion vs $13.3 billion in the prior year

Q3 2025 EPS of $0.17 vs $0.54 in the prior year

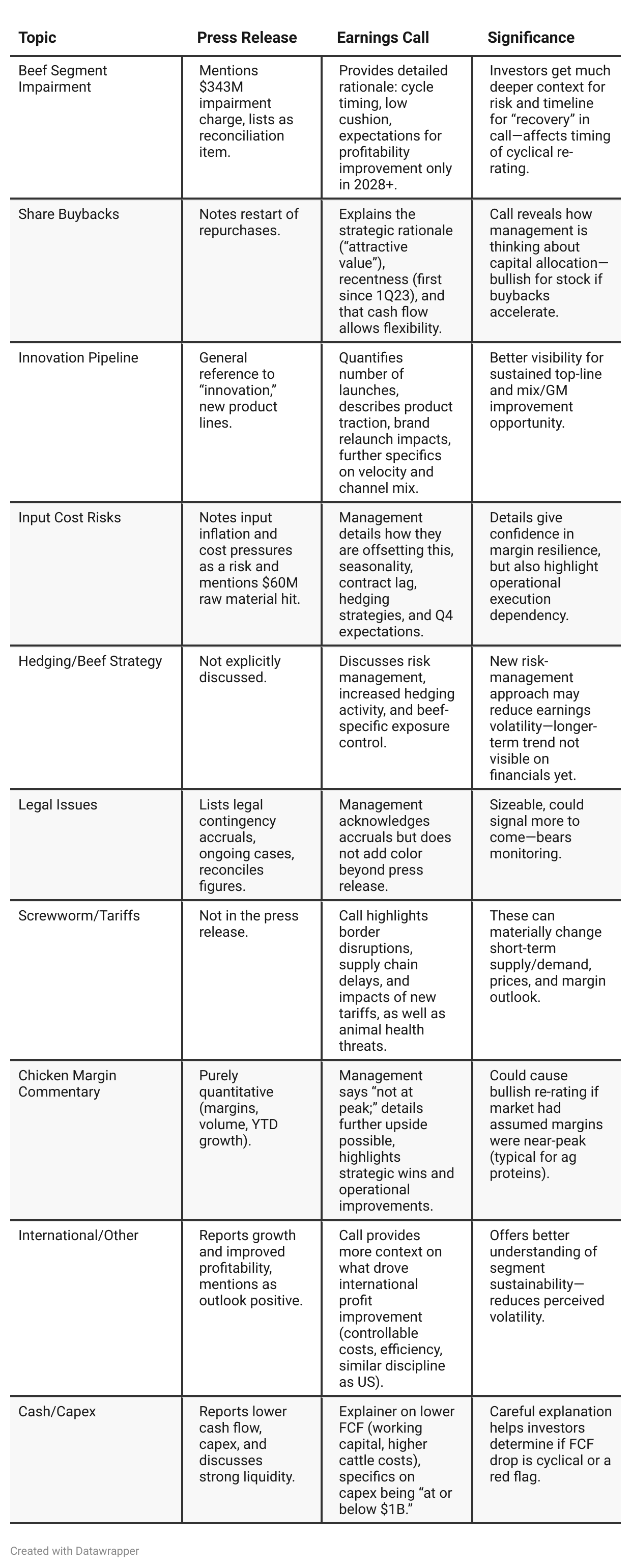

Press Release vs Call Transcript Comparison

Earnings Call opened up the “story behind the numbers”—why margin improvement may persist and risks of further beef volatility.

Press release is more quantitative, call is qualitative—call is essential to judge sustainability/quality of reported results.

Non-GAAP focus versus large GAAP adjustments in both—investors must be cautious about the true underlying earnings power.

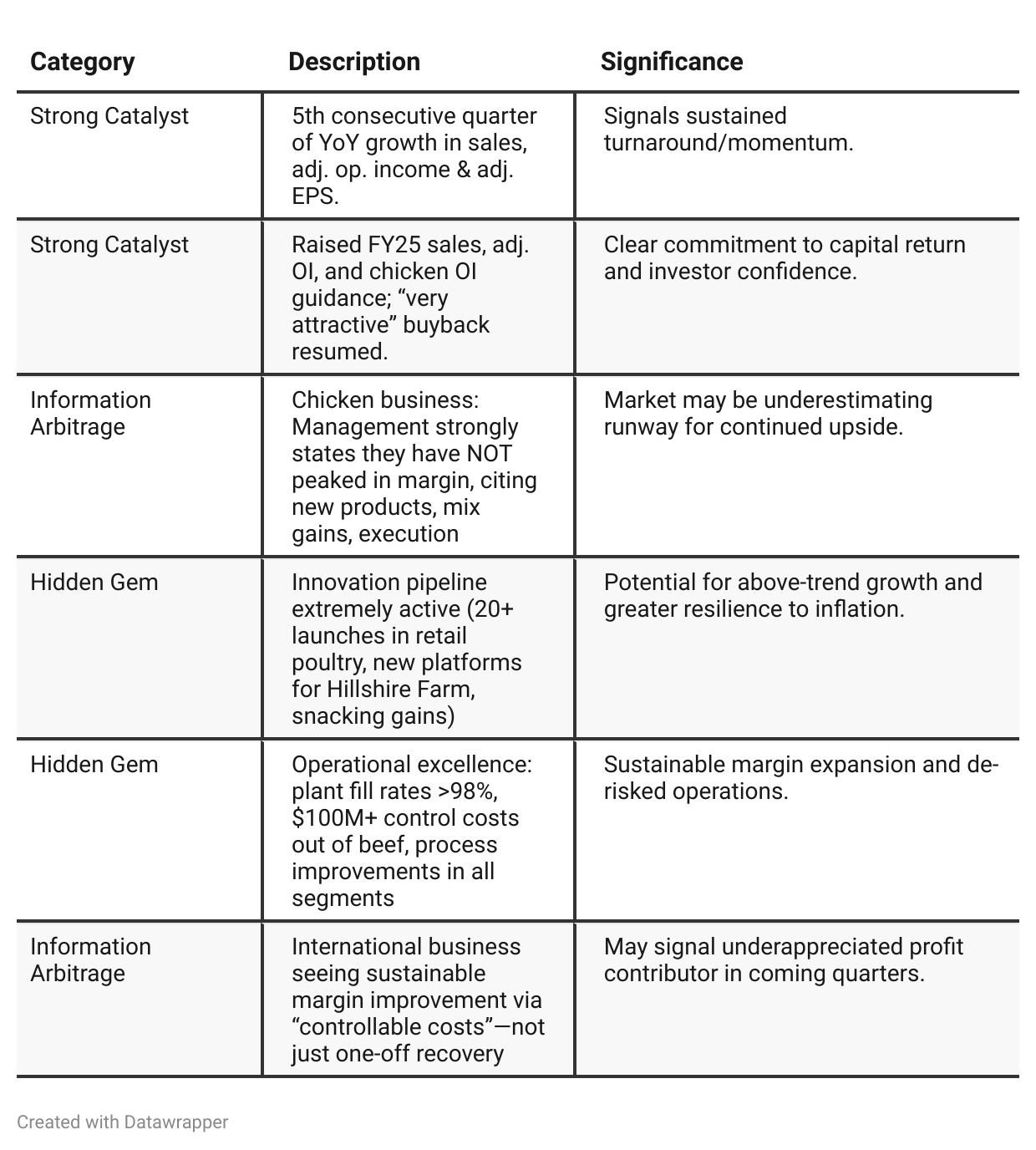

Positive Insights

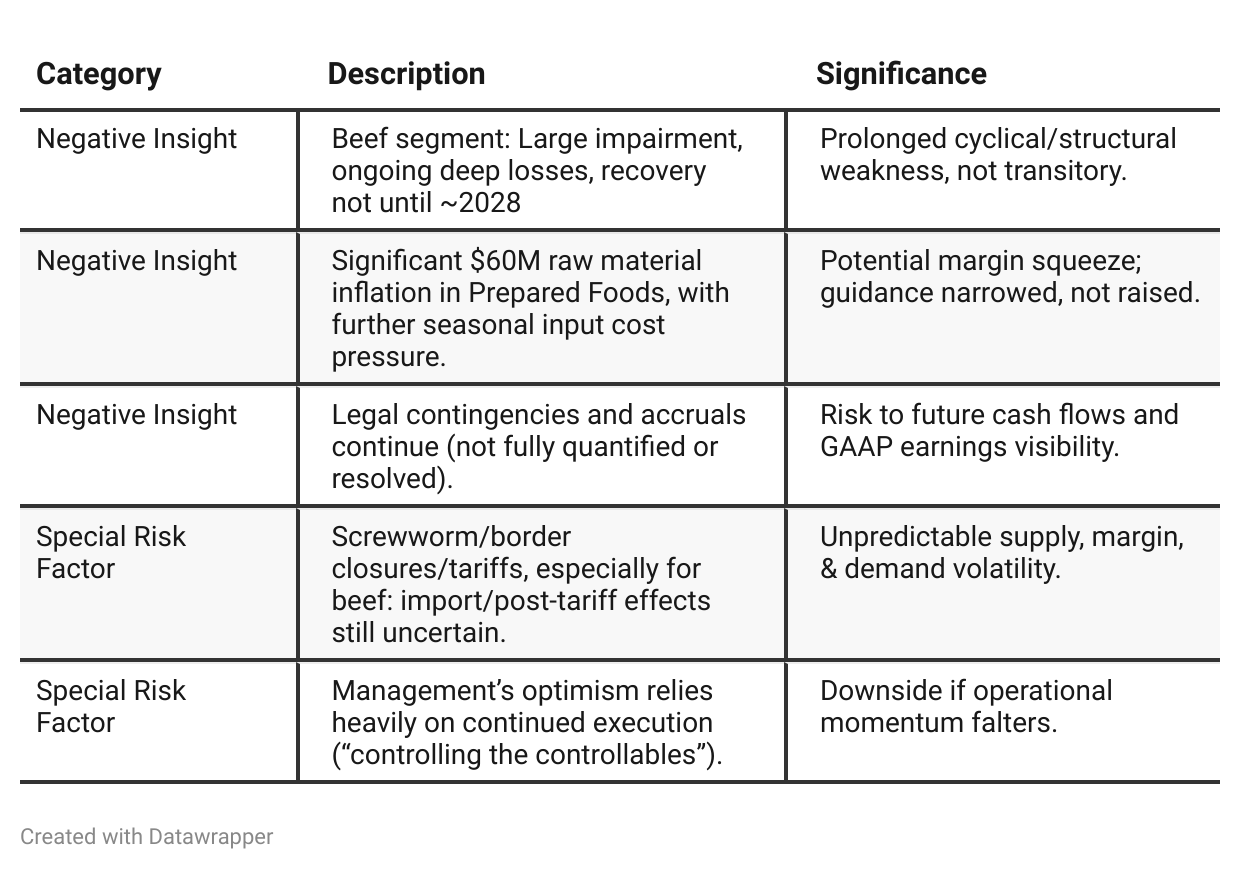

Negative Insights

Tariff Risk

Mentions: Tariffs on Brazilian beef brought up in Q&A; management notes timing lags (retail/wholesale impact delayed), with supply chain bottlenecks (esp. for Southern Hemisphere lean beef imports).

Impact on Profitability: Management says tariff’s price effects haven’t fully manifested in the market yet; significant inflation in beef trims already, so supply/demand imbalance could worsen or flip later.

Risk Mitigation Actions: No major mitigation disclosed, but close supply chain monitoring. They rely on data, hedging, and decisions to shift processing/fill rates to offset volatility.

Forward-Looking: Company acknowledges dynamic/challenging market, will continue to monitor and adjust. Tariffs may affect competitiveness and supply, especially if duration or intensity increases—potential for unexpected margin swings in beef especially; no clear move to offset risk through geographic/contractual shifts yet.

Sentiment Analysis

The overall sentiment toward Tyson Foods ($TSN) is bullish. Investors highlight better-than-expected earnings, strengthened performance in the chicken and prepared foods segments, raised full-year guidance, and a noticeable call option purchase, reflecting positive sentiment about the stock’s prospects. While there is awareness of continued beef segment challenges and rising cattle costs, the prevailing mood is optimistic, as evidenced by discussions of strong demand, favorable analyst reactions, share price gains, and express long positions.

Previous Earnings Call

Quarter-over-quarter comparison

Tyson’s narrative has evolved from a focus on foundational improvement and prudent, incremental progress in Q2 2025 to one of clear momentum and robust confidence by Q3 2025. Early in the year, management acknowledged significant operational achievements but was careful not to overcommit, holding guidance as macro and geopolitical uncertainties lingered. By Q3, the company’s tone has shifted to celebrating realized results—citing five consecutive quarters of growth, upwardly revised guidance, and a renewed commitment to capital returns through share repurchases. The messaging has crystallized around proven execution, rapidly expanding innovation, and continuous performance improvement in core segments (especially Chicken and Prepared Foods), even as they are frank about persistent risks in the Beef segment and broader market. In sum, the market story has moved from “potential and building discipline” to “delivering results and accelerating returns.”Year-over-year comparison

Q3 2024 marks Tyson in a turnaround phase—driving operational basics, managing through tough cattle cycles, and stabilizing the core businesses. The tone is cautiously optimistic; the company is restoring credibility, focusing on margin control, and offsetting macro headwinds (mainly from beef) through improvements in Chicken, Pork, and Prepared Foods. Growth is credited both to market tailwinds (lower grain) and internal discipline, but guidance remains restrained and risk-aware.

Q3 2025 sees Tyson transition to a confident execution phase. Management’s language is more assertive, celebrating multiple quarters of year-over-year growth, raising guidance directly, and initiating capital returns. The company positions itself as an industry leader not just in scale but in innovation, margin, and operational prowess. There’s more candor regarding segment headwinds (notably beef segment impairments and commodity inflation), but the overall narrative has shifted to “proven success” and “clear upside,” rather than “early recovery.” Now, Tyson is pushing for further margin expansion, brand leadership, and direct returns to shareholders, while remaining transparent about persistent—and newly emergent—macro risks.

Final Takeaway

Tyson Foods is in a clear recovery/operational transformation phase, driven by disciplined execution, margin expansion, and product innovation—especially in chicken and prepared foods. While beef remains a material headwind with a long recovery timeline, overall momentum, capital discipline, and management’s visible confidence via buybacks point to further upside. Execution on cost-control, innovation pipeline, and successful navigation of risks (legal, input inflation, animal disease, and tariffs) will be decisive for future performance. Verdict: Buy, with upside— as long as operational execution continues and legal/commodity risks do not intensify unexpectedly.