Sterling Infrastructure, Inc. (NASDAQ: STRL) – Q3 2025 Earnings

Sterling Infrastructure, Inc. (NASDAQ: STRL) – Q3 2025 Earnings

Earnings Release Date: Nov. 03, 2025

Stock Price: $377.90

Market Cap: $11522.5 million

Q3 2025 sales of $698.0 million vs $593.7 million in the prior year

Q3 2025 EPS of $2.97 vs $1.97 in the prior year

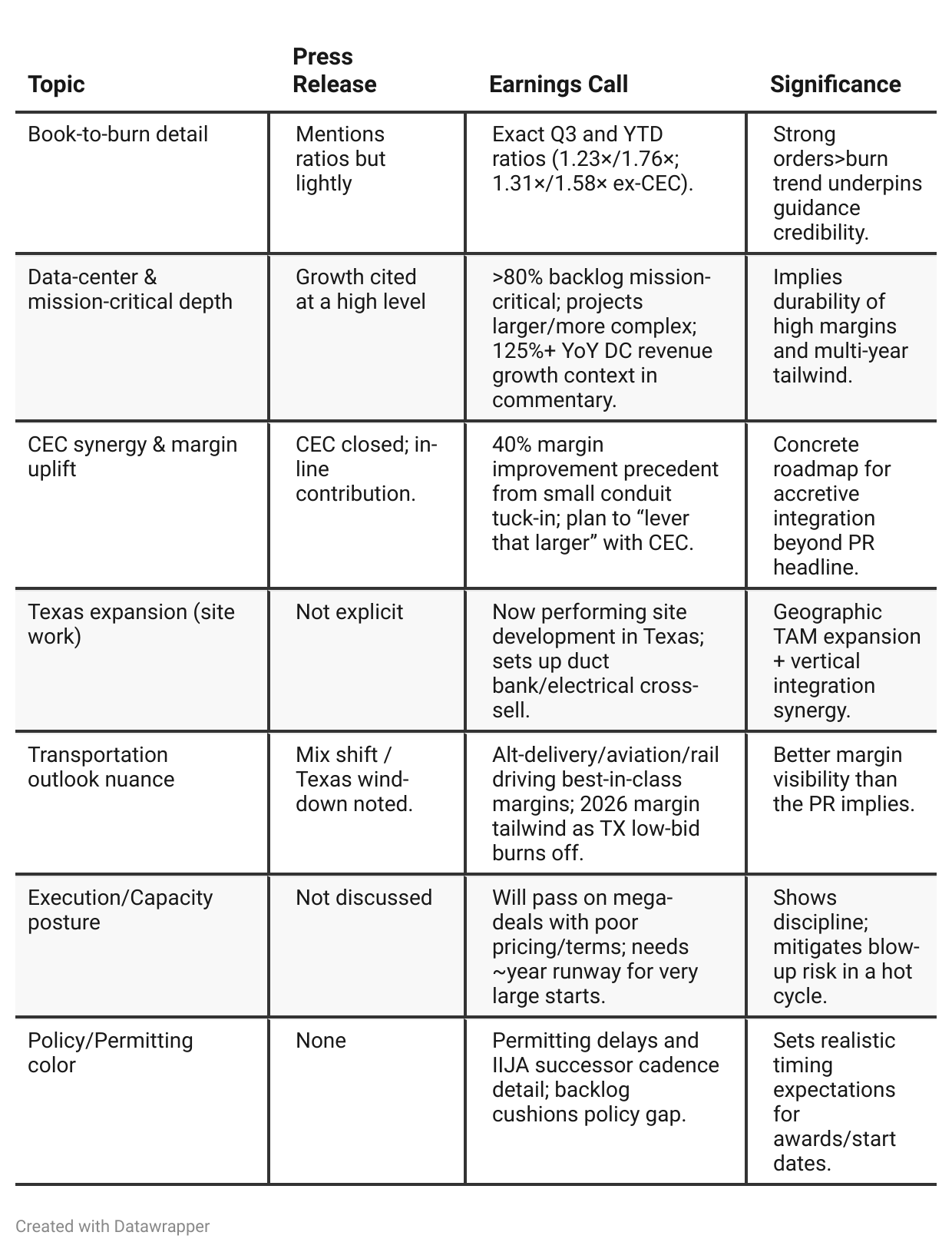

Press Release vs Call Transcript Comparison

Balance sheet/liquidity is a positive (cash $306M; revolver undrawn; net cash ~$12M), improving optionality for organic build-outs and tuck-ins.

Shareholder returns ongoing (buybacks); PR cites $4.7M repurchased in Q3 at $274.37 average; call notes YTD $48.5M at ~$136 avg (pre-run valuation), with $80.9M authorization left—suggests opportunistic approach.

Housing softness is contained to Building Solutions; diversified mix (E-Infrastructure, Transportation) more than offsets it near term.

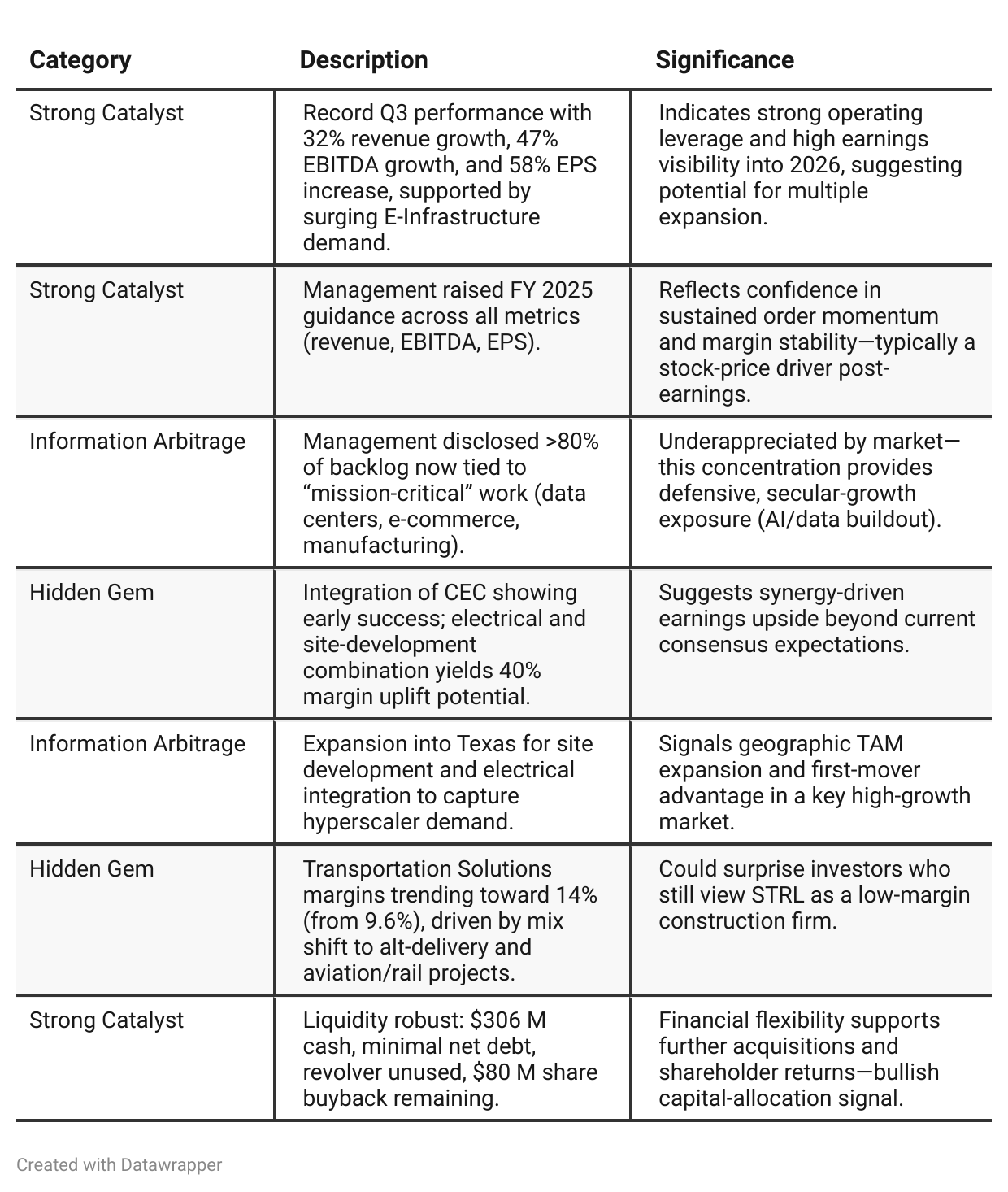

Positive Insights

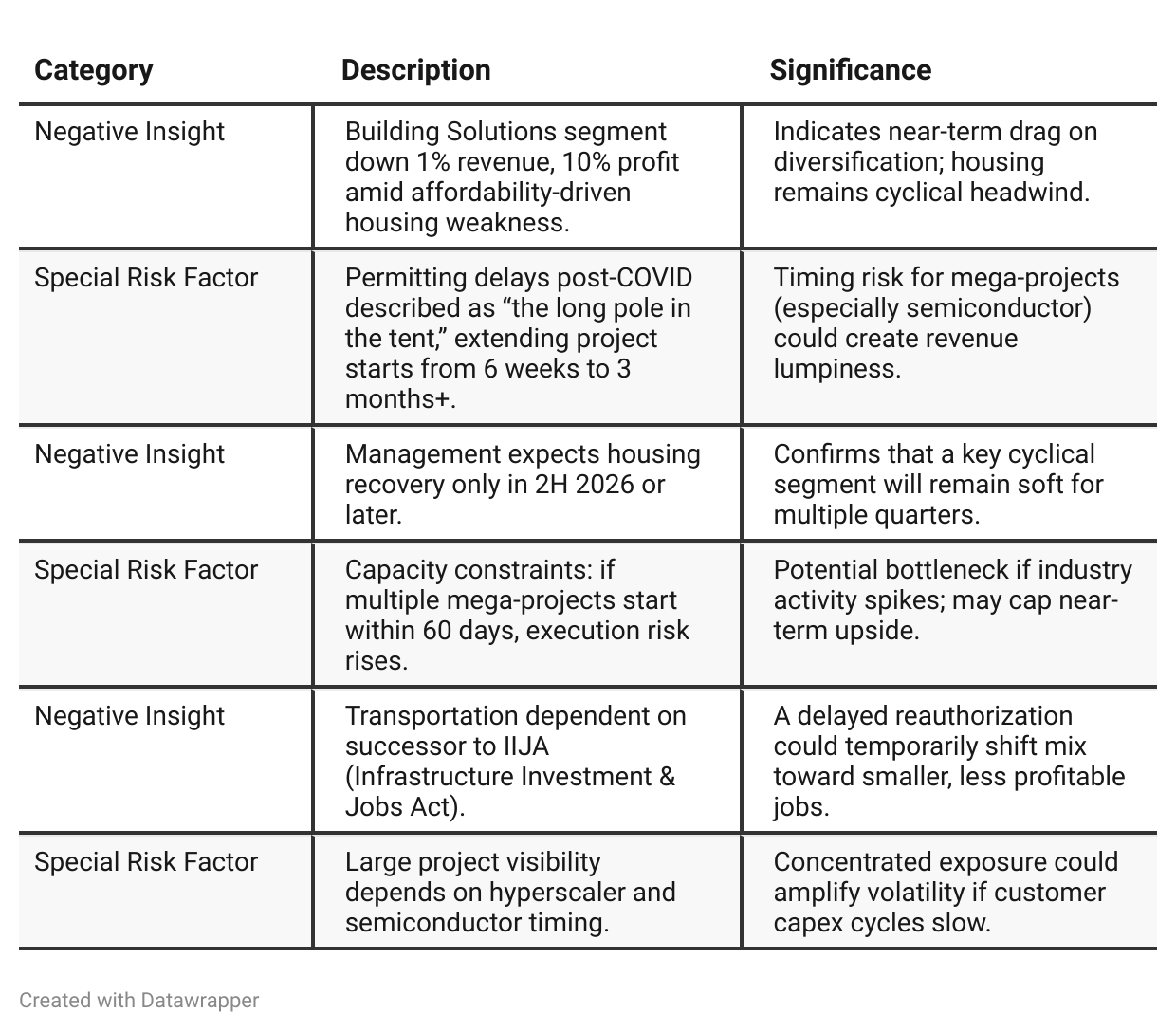

Negative Insights

Tariff Risk

The transcript contains no direct mention of tariffs or trade policy. However, management discussed onshoring/reshoring of chip plants and U.S. manufacturing megaprojects, which implicitly benefit from protectionist or pro-domestic-manufacturing policy.

Risk: If tariff regimes change or trade barriers ease, onshoring incentives could weaken, moderating demand for Sterling’s industrial projects.

Mitigation: Sterling’s focus on data centers and U.S. infrastructure insulates it from import-export volatility.

Outlook: Neutral to positive—company indirectly benefits from sustained domestic investment trends supported by current trade posture.

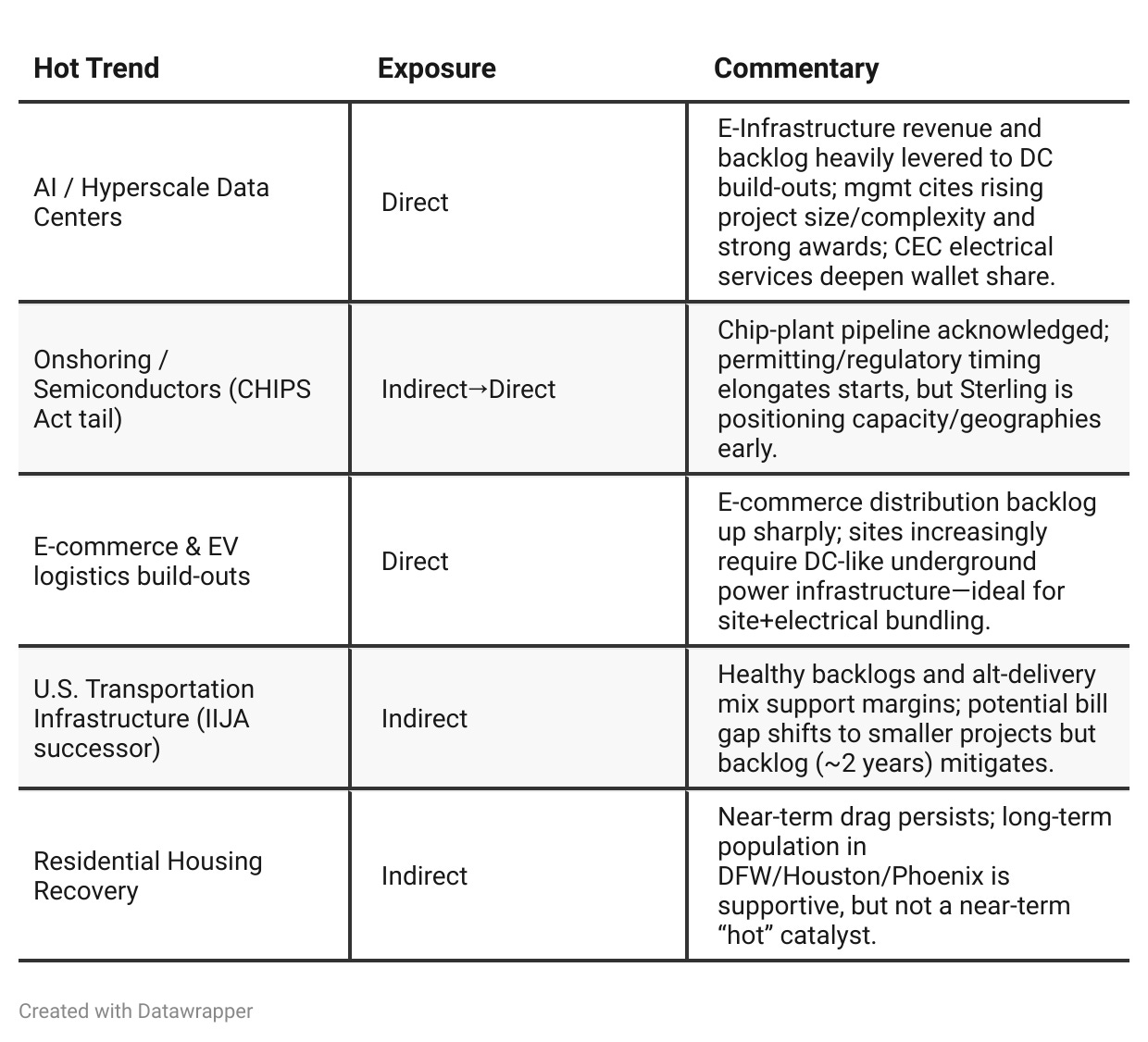

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2’25: “Scaling the playbook.” Sterling highlights surging E-Infrastructure margins, rising data-center exposure, plans to enter Texas/Northwest, and a pending CEC deal expected to unlock end-to-end solutions and faster timelines. Guidance is raised, but CEC is still outside the numbers.Q3’25: “Executing at scale—with guardrails.” CEC is closed and contributing; Texas site work is already underway; visibility pools are materially larger; and management pairs bullish demand (DCs, e-commerce, future semis) with explicit bid discipline and candid timing risks around permitting. Guidance is raised again, now with CEC and stronger book-to-burn.

Year-over-year comparison

Q3 2024: “Accelerating Momentum.”

Sterling positions itself as a fast-growing, high-margin infrastructure builder benefiting from AI, data centers, and on-shoring trends. Management is focused on expanding organically and hunting for an electrical-services acquisition (later to become CEC). Housing weakness is acknowledged but framed as temporary. The message: profitable growth with optionality.Q3 2025: “Executing Scale and Integration.”

Sterling evolves into an integrated, platform-level infrastructure specialist. The CEC deal closes, expanding vertical scope and margin potential. The narrative now centers on execution at scale, synergy realization, and guardrails around bidding discipline. Management’s tone reflects maturity: emphasizing selectivity, transparency on permitting risk, and sustained capital returns. The company projects confidence built on data, not just outlook.

Final Takeaway

Sterling Infrastructure (STRL) is in a growth and margin-expansion phase, propelled by surging E-Infrastructure demand (AI/data centers, e-commerce logistics) and disciplined project selection. While Building Solutions remains constrained by housing affordability, strong backlogs, CEC synergies, and diversified end-markets provide resilience. Execution on integration and project timing will be key to sustaining EPS momentum through 2026.

Verdict: BUY, with upside tied to continued data-center buildout and policy stability.