Sterling Infrastructure, Inc. (NASDAQ: STRL) – Q2 2025 Earnings

Sterling Infrastructure, Inc. (NASDAQ: STRL) – Q2 2025 Earnings

Earnings Release Date: Aug. 4, 2025

Stock Price: $263.05

Market Cap: $7998.8 million

Q2 2025 sales of $614.5 million vs $582.8 million in the prior year

Q2 2025 EPS of $2.31 vs $1.67 in the prior year

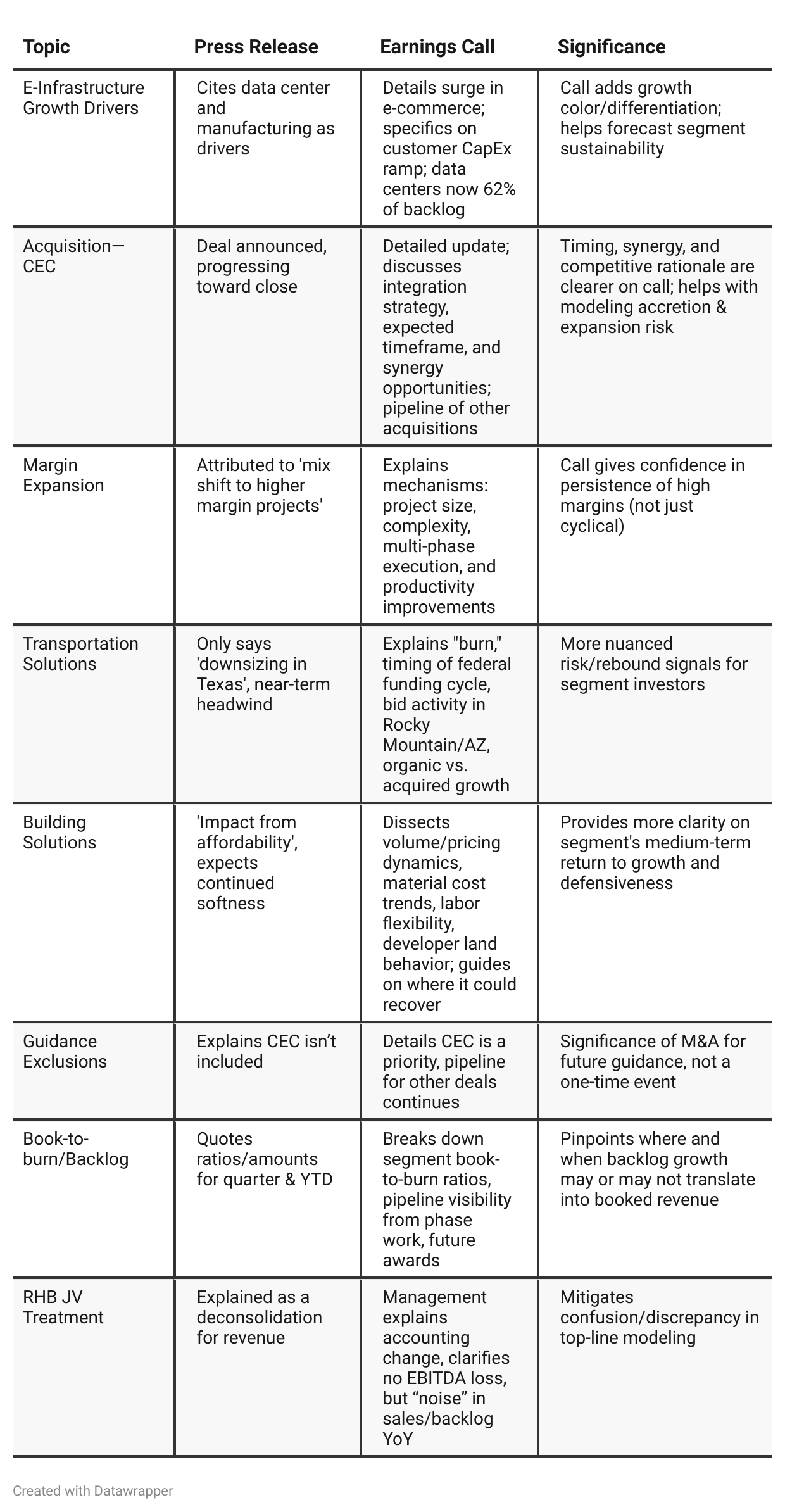

Press Release vs Call Transcript Comparison

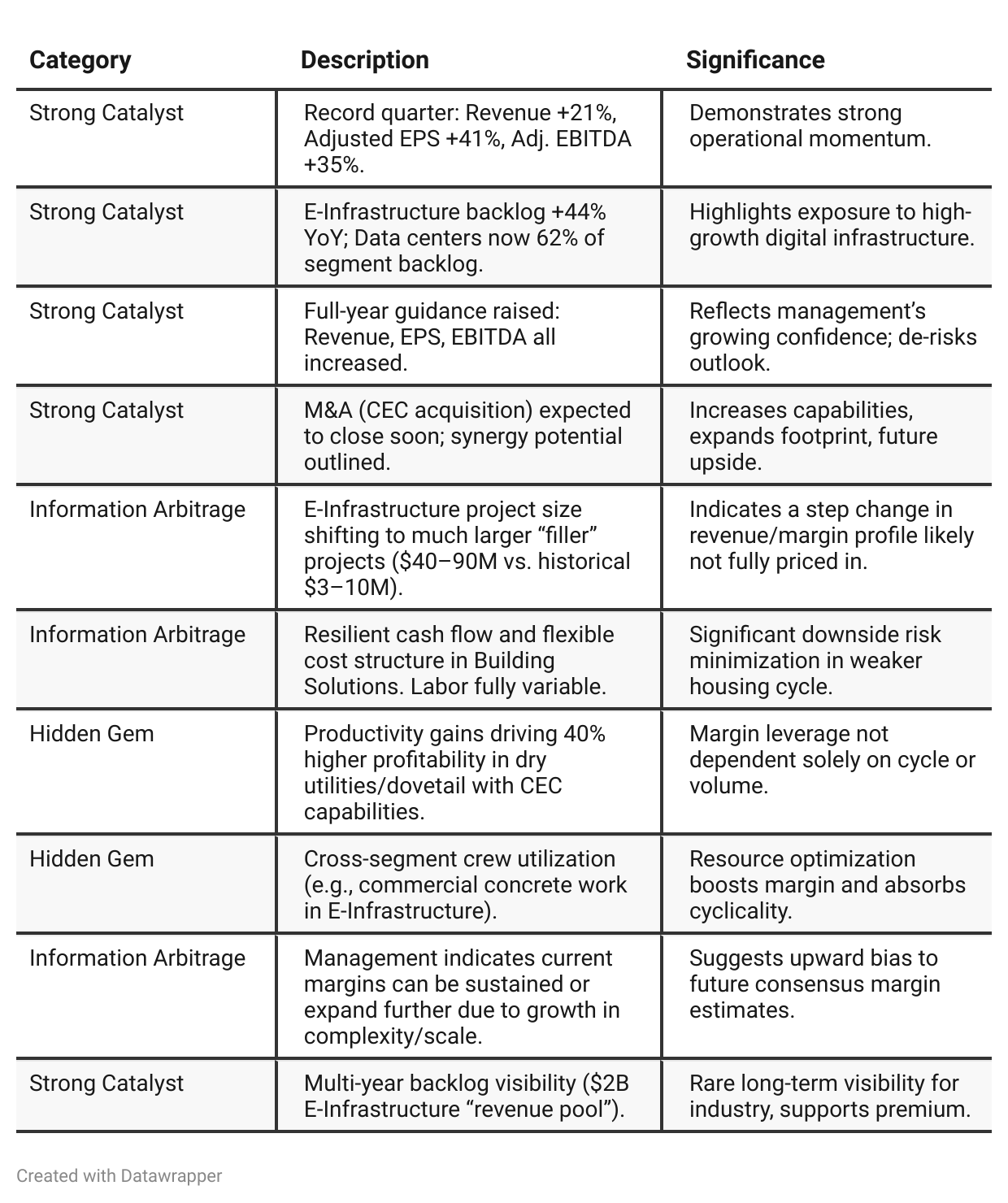

Financial Flexibility: High net cash ($401M), unused revolver, strong cash generation mean organic/inorganic growth can continue and offer downside protection.

Capital Allocation: Active share buybacks in Q1, none in Q2—management tracks valuation/opportunity, but investors should watch for consistency and signals.

Competitive Moat: Barriers raised via scale, complexity, mission-critical execution, and now (pending) ability to offer end-to-end via CEC.

Visibility: Multiyear revenue “pool” in E-Infrastructure approaches $2B—unusually long forward sight for an infrastructure company.

Potential inflections: E-commerce distribution work is not only recovering, but with bigger/higher-margin projects than previous cycles.

Organic vs. Acquired Expansion: Approach tailored by geography and project mix, reducing single-pronged expansion risk.

Management Tone: Confident, specific, highlights ability to improve returns, not just chase revenue—aligned with value creation.

Positive Insights

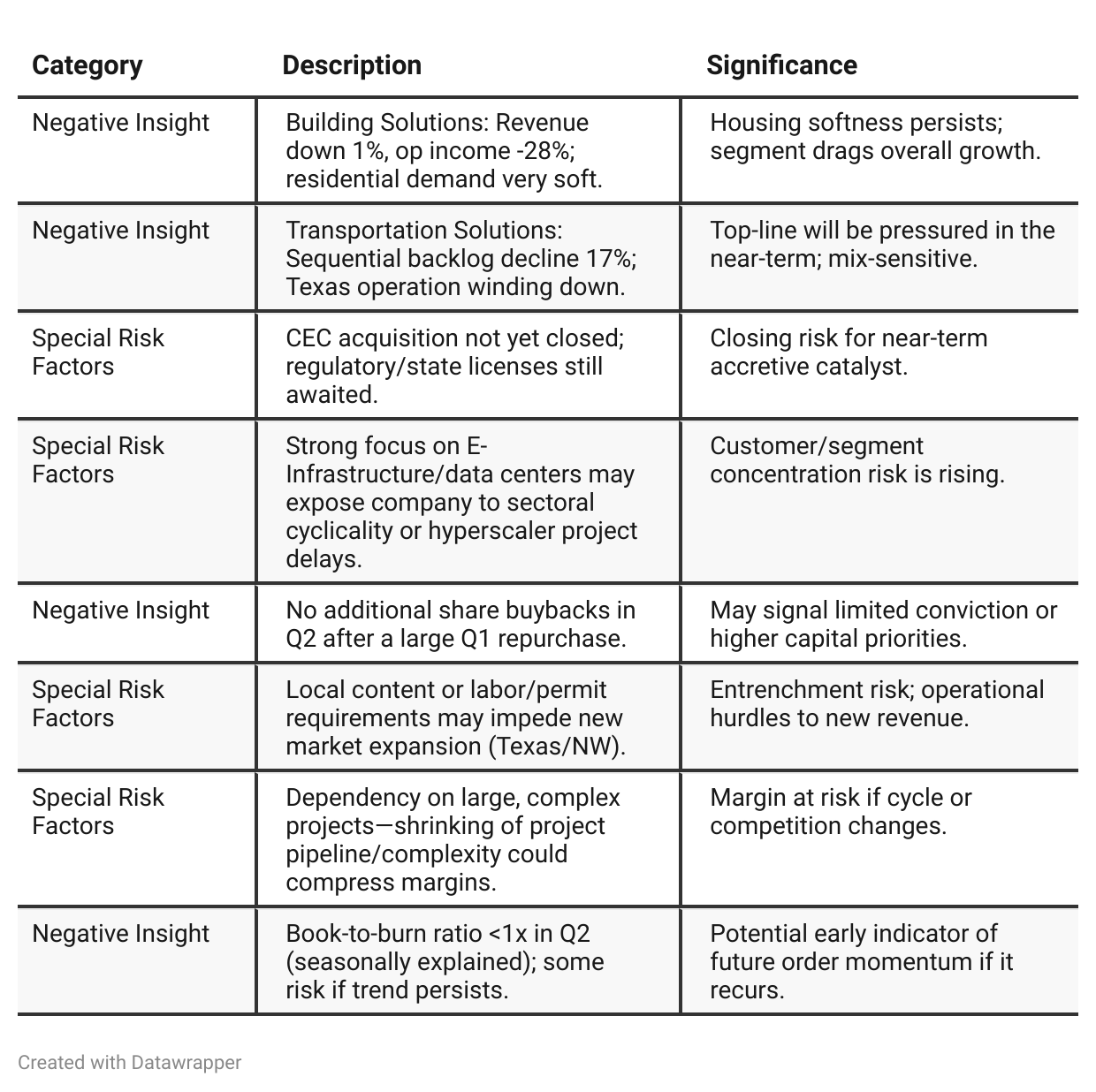

Negative Insights

Tariff Risk

No direct mention of U.S. tariffs or trade policies, nor any discussion of impacts on supply chain, contract pricing, or market share due to tariffs in the call.

No stated mitigation actions (supply chain adjustments, alternative sourcing, or price escalators) in response to tariffs.

Previous Earnings Call

Quarter-over-quarter comparison

Sterling Infrastructure’s 2025 narrative has shifted from a confident but measured optimism in Q1—cognizant of macro/tariff risk, and anchoring the story on backlog, margin recovery, and prudent M&A (e.g., the Drake acquisition)—to a noticeably more energized, opportunity-driven story in Q2. The Q2 call doubles down on growth, not only celebrating outperformance but also raising the bar with upgraded guidance. Management’s message has evolved from “managing risk and building a strong foundation” to “scaling up to capture extraordinary sector opportunities” (especially in data centers, mega-projects, and e-commerce), while actively de-emphasizing external risks. The CEC acquisition has gone from a stated “priority” to the centerpiece of Sterling’s next phase, designed to cement its moat and pull further ahead of competition through integration and service breadth. Meanwhile, the tone toward residential softness has shifted from “watchful and patient” to “accepting, flexible, and conservative in forecasts.” The company’s growth now feels propelled by industry trends and internal capability, with management more vocal and direct about competitive advantages and the road map for geographic and offering expansion.Year-over-year comparison

In Q2 2024, the company is focused on careful margin optimization, portfolio mix discipline, and leveraging a strong but cautious multi-year backlog in the face of sector cyclicality and shifting macro conditions (interest rates, land and labor availability, project phasing). The story is of a company executing well on the foundations, mindful of risk, stage-gating growth to maintain returns, and capitalizing on secular trends in infrastructure and onshoring—while remaining careful with capital and acquisitions.

By Q2 2025, Sterling is not just managing growth but accelerating it. The narrative is outwardly bullish, celebrating bigger and more complex projects, surges in e-commerce work, and growing strategic customer relationships. The company’s sights and execution have shifted to capturing greater value per project through vertical integration (electrical, mechanical via CEC), leveraging scale to further raise margins, and optimizing across divisions. Financials (especially margins and EPS) are highlighted aggressively, with clear evidence of upward guidance and a sense of operational momentum. Competition is less about price, more about speed/complexity/service breadth, and risks are relatively muted—with the exception of continued headwinds in residential. Capital deployment is focused on transformative acquisition (CEC), and the message is that Sterling has moved beyond defense and selective growth into true leadership in the critical infrastructure sector.

Final Takeaway

Sterling Infrastructure is in a growth acceleration phase, capitalizing on secular demand for mission-critical data centers and infrastructure with sector-leading margins and a strong multi-year backlog. While its E-Infrastructure exposure and pending CEC acquisition are clear catalysts, continued softness in Building Solutions and the timing of M&A integration warrant monitoring. Execution on hyperscaler-driven projects and expansion into new geographies will be critical for sustaining the current growth trajectory. Verdict: Buy, with substantial long-term upside if current growth and margin trends persist and CEC closes as expected.