Sensus Healthcare (NASDAQ: SRTS) – Q3 2025 Earnings

Sensus Healthcare (NASDAQ:SRTS) – Q3 2025 Earnings

Earnings Release Date: Nov. 06, 2025

Stock Price: $3.52

Market Cap: $57.5 million

Q3 2025 sales of $6.9 million vs $8.8 million in the prior year

Q3 2025 loss per share of ($0.06) vs EPS of $0.07 in the prior year

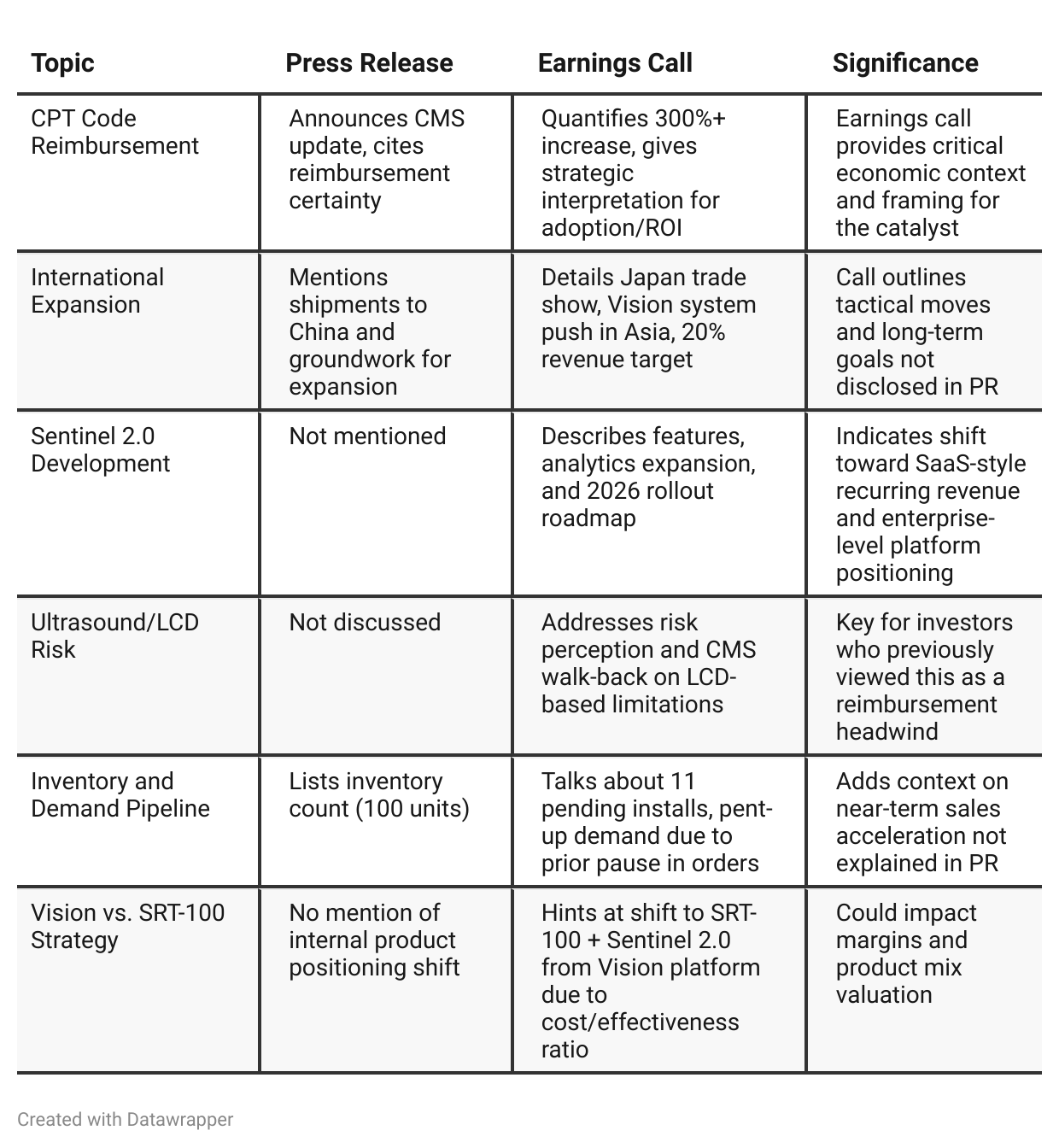

Press Release vs Call Transcript Comparison

The press release lays out the high-level financials and regulatory catalyst, but the earnings call delivers the real investor intelligence—quantifying reimbursement changes, framing market psychology, and signaling strategic pivots (Sentinel 2.0, international growth, and potential product mix shift).

The most critical gap between the two is the lack of discussion in the press release around Vision vs. SRT-100 positioning and the future revenue model, which could materially affect margin expectations and valuation frameworks. Investors focused solely on the press release would miss these inflection points.

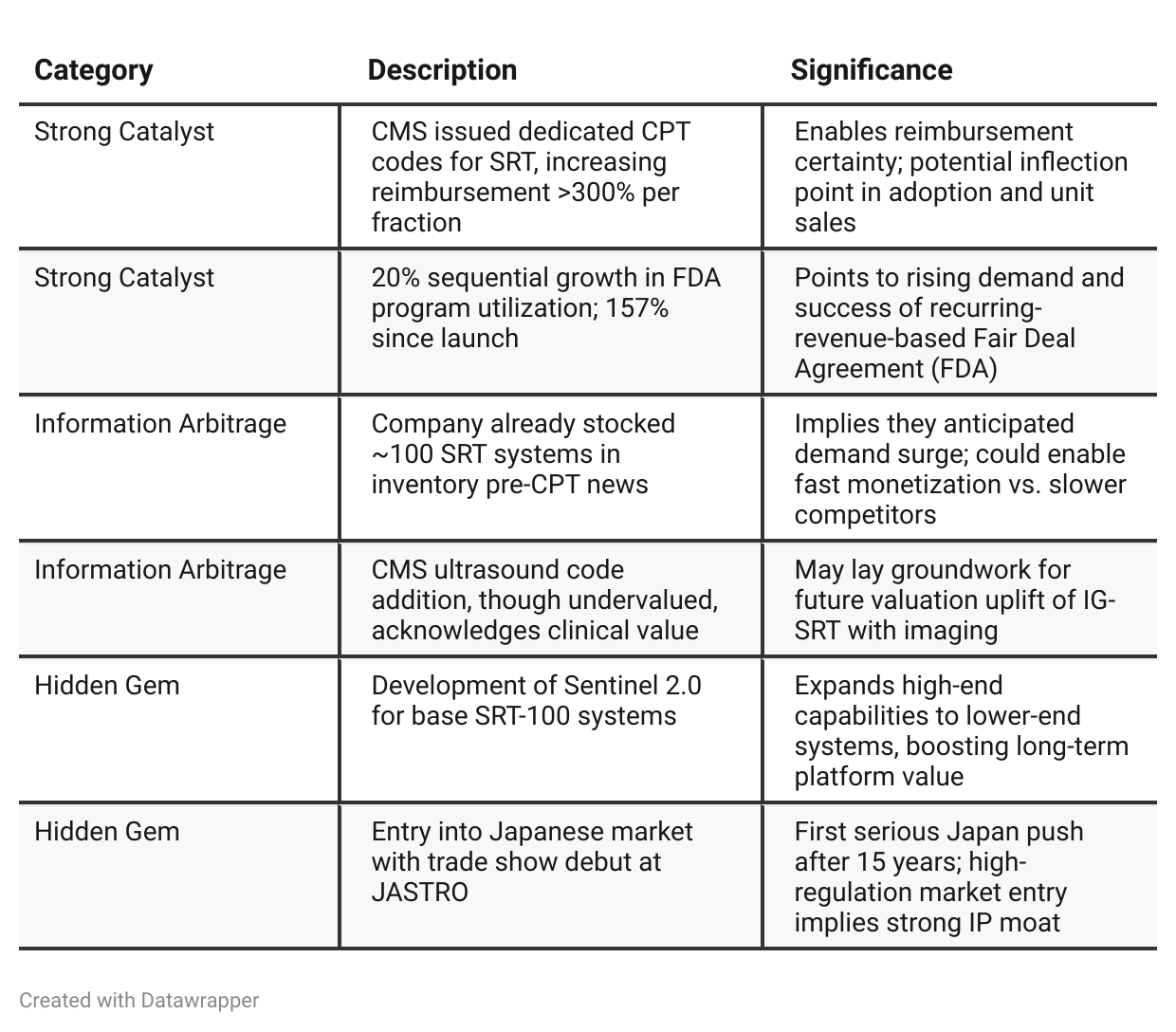

Positive Insights

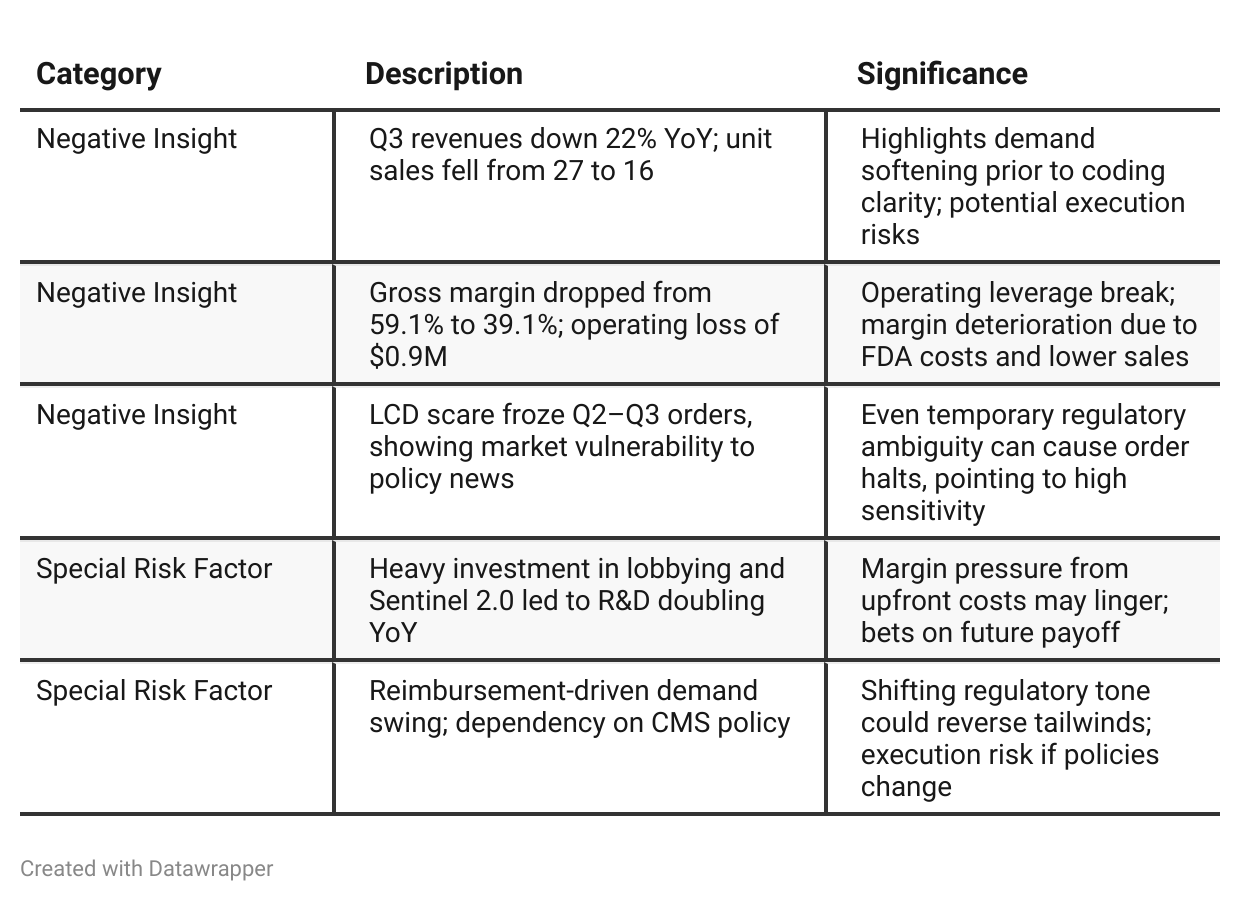

Negative Insights

Tariff Risk

No mentions of tariffs, trade policy, or cost implications tied to U.S. trade regulations.

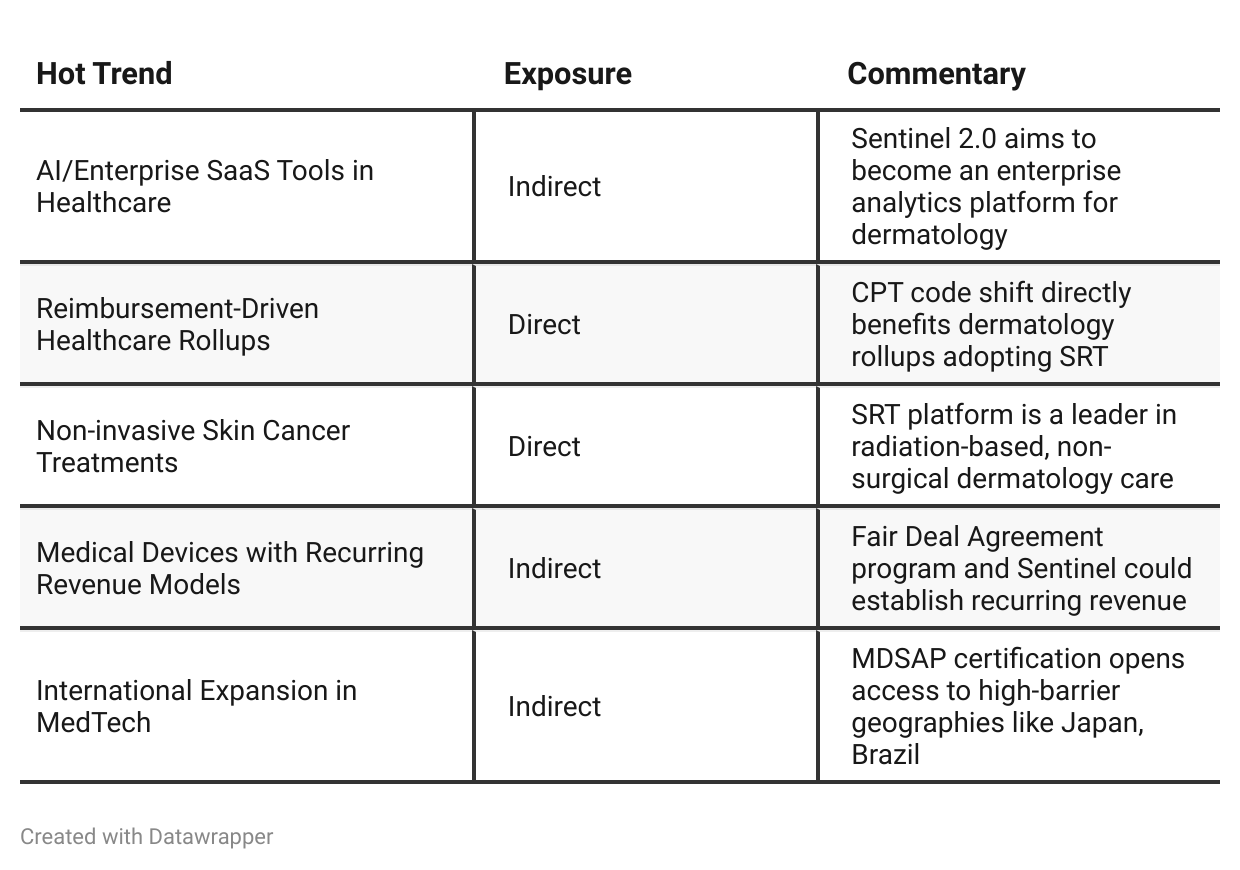

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Q2 2025 Analysis)

Between Q2 and Q3 2025, Sensus Healthcare transitioned from damage control to offensive execution. In Q2, the company faced a sudden disruption from a proposed LCD targeting ultrasound use in skin cancer treatment, leading to a customer pause and uncertainty. The messaging was cautious and defensive, focusing on lobbying, maintaining relationships, and navigating ambiguity.

By Q3, the narrative shifted dramatically. CMS finalized new CPT codes for superficial radiotherapy, including a >300% reimbursement increase that leveled the playing field between dermatology offices and hospitals. This removed a major friction point in adoption and validated SRT’s role in noninvasive skin cancer care.

Management now speaks confidently about pent-up demand, expansion into Japan, leveraging Sentinel 2.0 to scale, and a return to growth. The tone is one of vindication and readiness for commercial acceleration.Year-over-year comparison

Between Q3 2024 and Q3 2025, Sensus Healthcare’s narrative has shifted from a product-driven, sales-growth story to a strategically validated platform story. While Q3 2024 emphasized rapid revenue and unit growth fueled by bulk SRT system sales and a major customer agreement (Platinum Dermatology), Q3 2025 reflects the early monetization and scaling pains of a shift toward a recurring revenue model built on Fair Deal Agreements and software infrastructure.

Despite a temporary step back in revenue and margin, the company now benefits from a structural reimbursement tailwind with newly issued CPT codes, reinforcing the legitimacy and ROI of its SRT technology.

The messaging has matured from “winning deals” to “owning the category” — emphasizing durable adoption, scalable infrastructure (Sentinel 2.0), and a long runway of demand from both domestic and international markets.

Final Takeaway

Sensus Healthcare is in a growth re-acceleration phase, driven by the game-changing finalization of CPT reimbursement codes for its core technology.

While Q3 results reflect a sales dip due to temporary order halts during policy uncertainty, the coding clarity is likely to drive a rebound in Q4 and 2026. Key execution areas include international expansion, Sentinel 2.0 rollout, and translating CPT momentum into recurring revenue.

Verdict: Buy, with upside potential hinging on the demand ramp and margin recovery from higher reimbursed volumes.