Sensus Healthcare, Inc. (NASDAQ: SRTS) – Q2 2025 Earnings

Sensus Healthcare, Inc. (NASDAQ: SRTS) – Q2 2025 Earnings

Earnings Release Date: Aug. 7, 2025

Stock Price: $5.33

Market Cap: $86.9 million

Q2 2025 sales of $7.3 million vs $9.2 million in the prior year

Q2 2025 EPS of -$0.06 vs $0.10 in the prior year

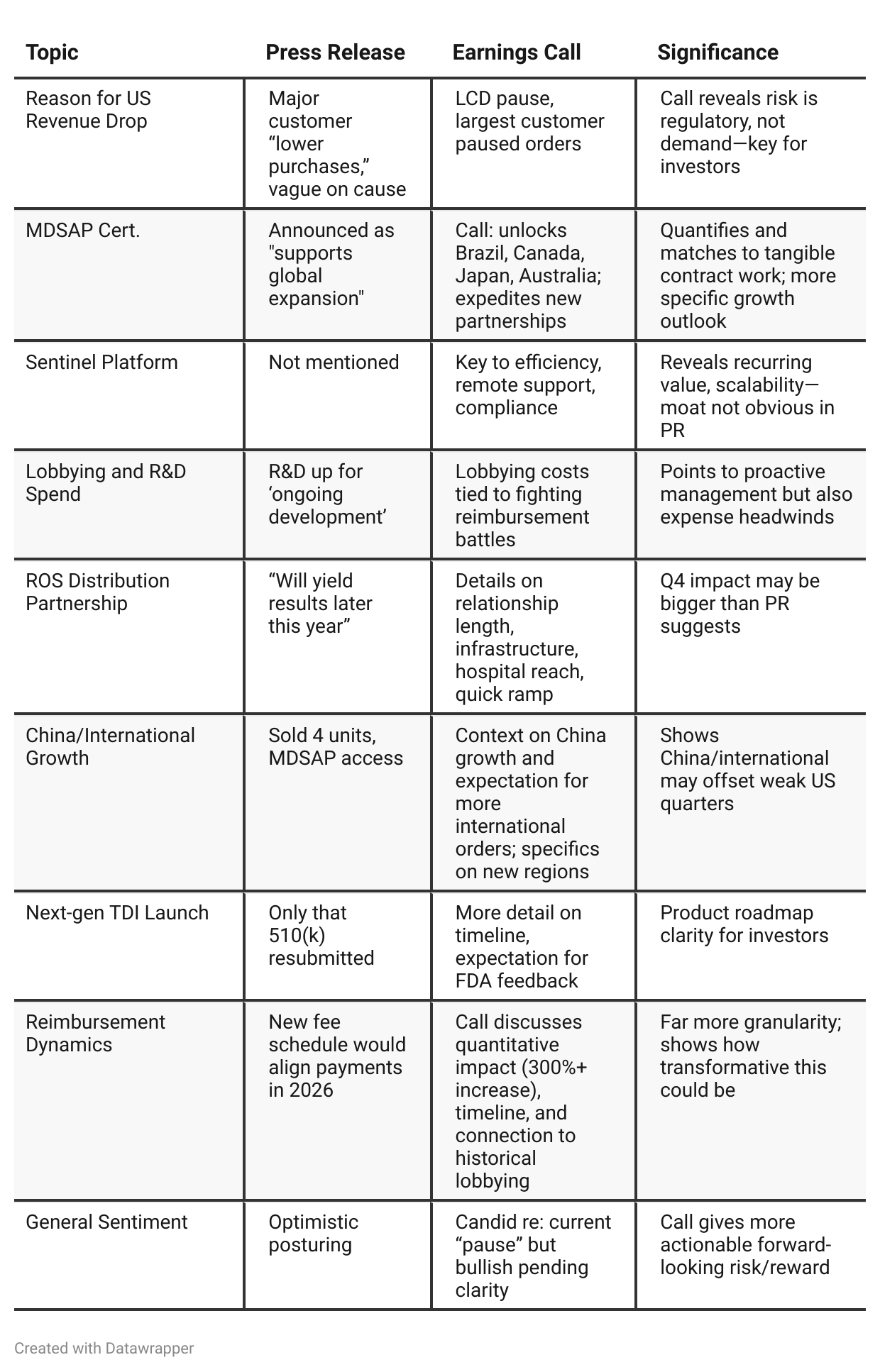

Press Release vs Call Transcript Comparison

Investor risk profile: Current upside is very dependent on the CMS decision—investors must price regulatory resolution risk.

Execution quality: Management appears proactive (heavy lobbying, maintaining customer relationship, pressing internationally), but cost structure is being stretched by regulatory and R&D defense.

Margins Outlook: High lobbying and R&D costs are likely to persist until regulatory uncertainty resolves; international gross margins are not disclosed and may differ from US.

Balance sheet: Ample cash ($22M, no debt) provides a cushion for near-term headwinds, though net cash is slightly down.

Opportunity: If CMS rules positively, snap-back in capital sales (esp. to paused, large customer) plus international expansion could drive sharp financial recovery.

Product/partnership pipeline: Next-gen device and strengthened distribution give long-term potential, but execution risk remains until these bear fruit in numbers.

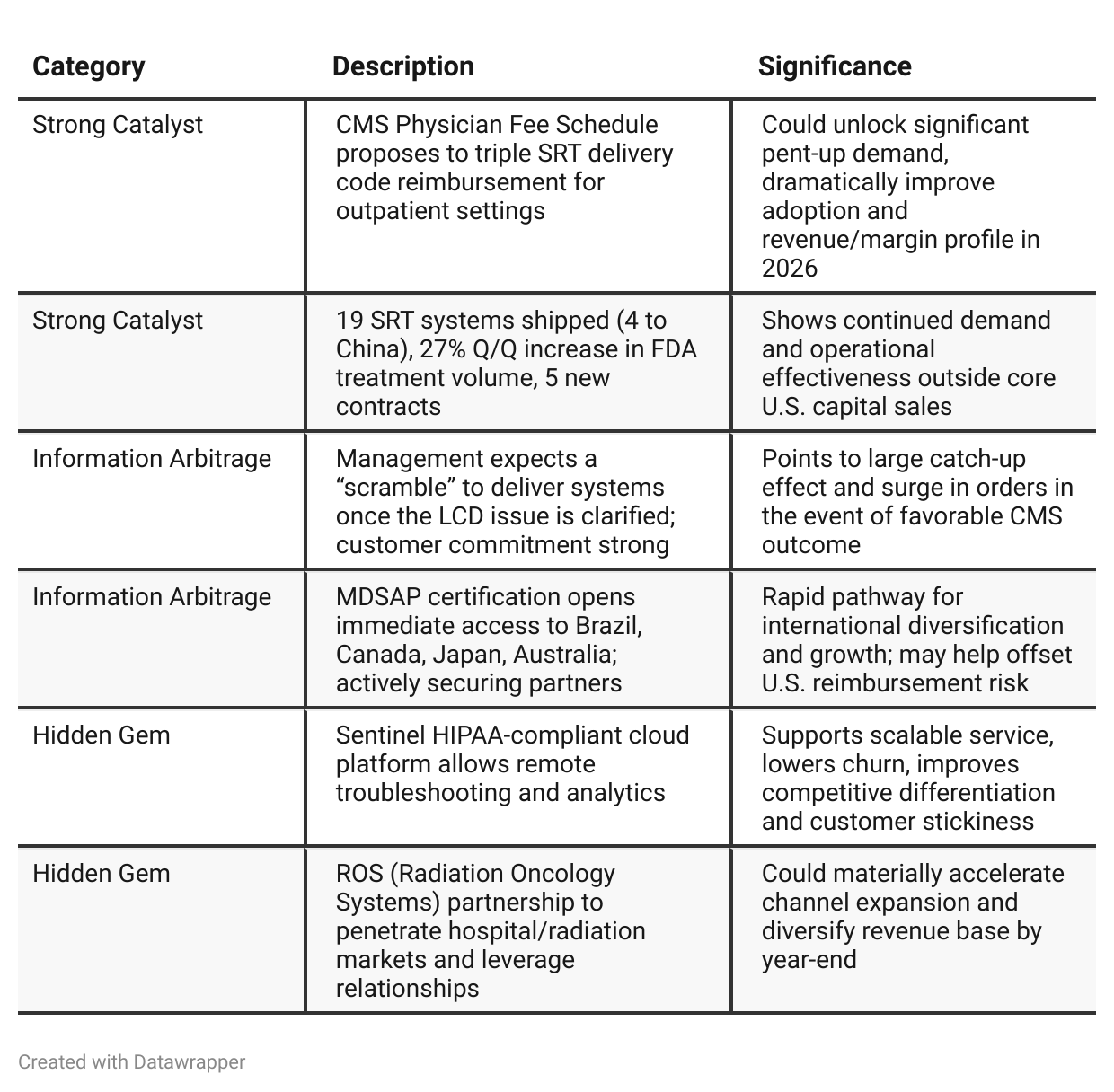

Positive Insights

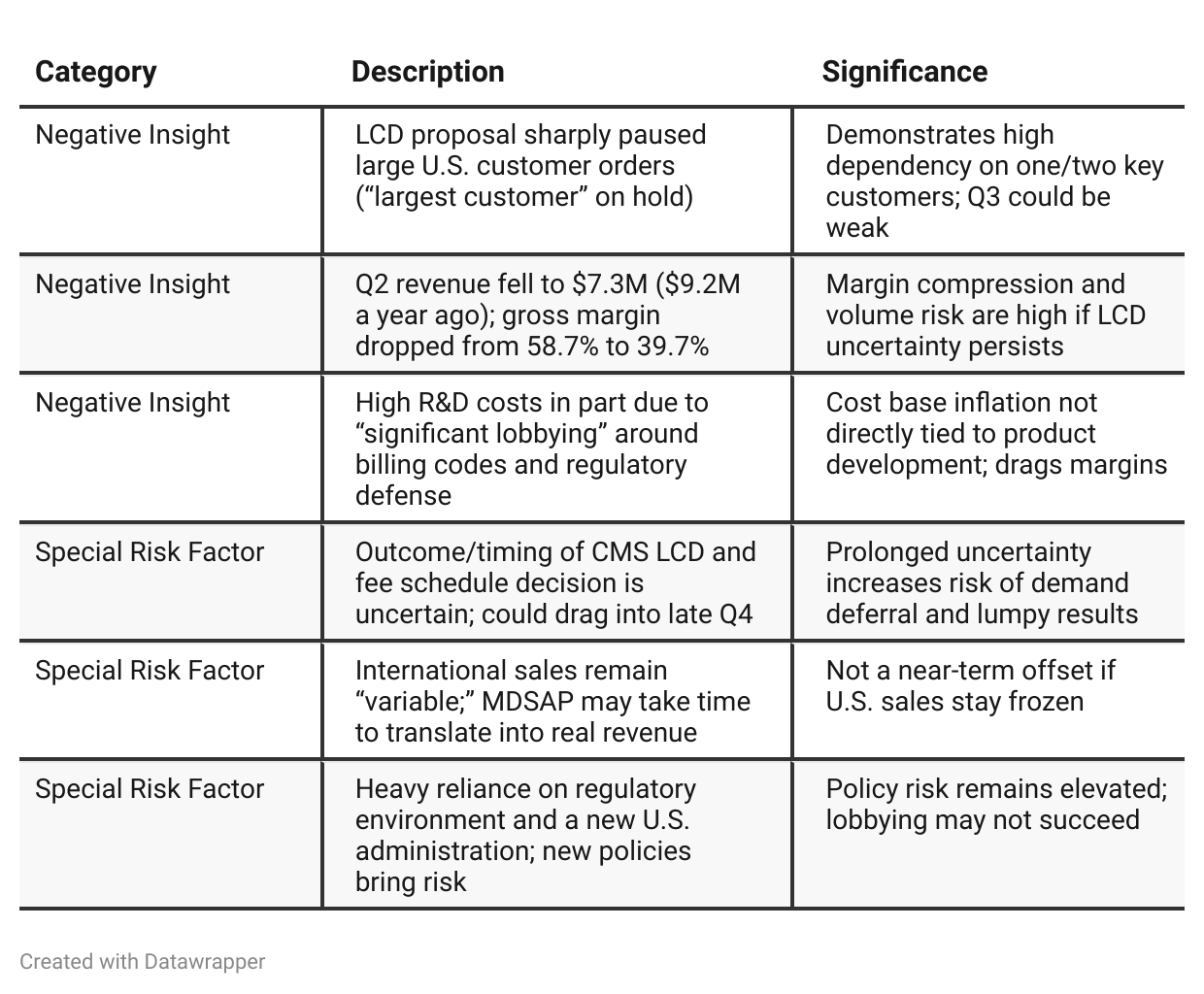

Negative Insights

Tariff Risk

There were no material mentions of U.S. tariffs or trade policies in the transcript.

The only international risks discussed related to regulatory certification and market access (MDSAP), not tariffs.

No discussion of plans to shift supply chain, production, or adjust contracts in response to tariffs.

No indications of recent or expected financial impact from tariffs, or impact on market share or innovation.

Sentiment Analysis

The overall sentiment toward Sensus Healthcare (SRTS) is predominantly bearish. The dominant mood is driven by the stock’s sharp drop after disappointing Q2 earnings, with several investors citing negative reactions to missed revenue and earnings targets, ongoing reimbursement uncertainty, and delays in U.S. sales acceleration. While a few bullish comments highlight long-term international expansion and innovative sales strategies, the prevailing tone centers on immediate downside, market impatience, and reduced analyst price targets. In summary, short-term investor confidence has been shaken by recent developments, outweighing positive references to future potential.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q1 2025 Call: Sensus Healthcare began the year with confidence, touting aggressive investments in sales, marketing, and product innovation as staging grounds for accelerating recurring revenue, international growth, and overall financial improvement. Management painted a picture of temporary weakness driven by deliberate spending, not structural issues, and forecasted a rapid return to growth and profitability, hinging on their Fair Deal Agreement pipeline.Q2 2025 Call: By the next quarter, optimism was tempered by a regulatory curveball: a sudden Medicare LCD proposal triggered a pronounced pause in capital purchases, especially from a major U.S. customer. The company’s tone shifted to managing through uncertainty—maintaining a solid recurring revenue base and engaging in extensive lobbying to defend reimbursement. They emphasized international growth opportunities, new global certifications, and partnerships as partial offsets. Ultimately, management’s narrative evolved from “strategic growth investments driving a near-certain rebound” to “navigating a pivotal, high-stakes regulatory risk, with future results hinging on external resolution but longer-term optimism intact if headwinds are overcome.”

Year-over-year comparison

In Q2 2024, Sensus Healthcare was executing on all cylinders—reporting rapid sales growth, strong profitability, and a successful rollout of its Fair Deal Agreements to diversify and stabilize revenues. The narrative was upbeat: innovation, expanding business models, and growing global presence were all delivering results, with 2025 forecast as a year of expanding recurring revenue and continued dominance in non-melanoma skin cancer treatment.

By Q2 2025, the company’s narrative has shifted sharply as a regulatory shock (Medicare LCD proposal) freezes U.S. sales momentum, particularly from key customers. While management stays constructive—touting commitment from customers, a robust product suite, and new international certifications—they are simultaneously on the defensive, managing costs, lobbying for policy changes, and candidly acknowledging financial softness. CEO messaging pivots from “capturing opportunity” to “navigating disruption and fighting for business continuity,” hoping for a policy resolution that could either trigger a recovery or amplify further risk.

Final Takeaway

Sensus Healthcare is in a transitional phase, waiting on pivotal U.S. regulatory (CMS) decisions that will determine the near-term fate of its domestic sales pipeline. The company’s proactive international expansion and tech/service differentiators provide upside optionality, but current U.S. sales are highly at risk due to external reimbursement uncertainties. Investors should focus on tracking regulatory updates, customer ordering behavior, and the speed with which international sales ramp. Verdict: HOLD, with substantial upside if U.S. reimbursement headwinds are removed and international trends accelerate.