Spok Holdings, Inc. (NASDAQ: SPOK) – Q3 2025 Earnings

Spok Holdings, Inc. (NASDAQ: SPOK) – Q3 2025 Earnings

Earnings Release Date: Oct. 29, 2025

Stock Price: $16.41

Market Cap: $337.0 million

Q3 2025 sales of $33.9 million vs $34.9 million in the prior year

Q3 2025 EPS of $0.15 vs $0.18 in the prior year

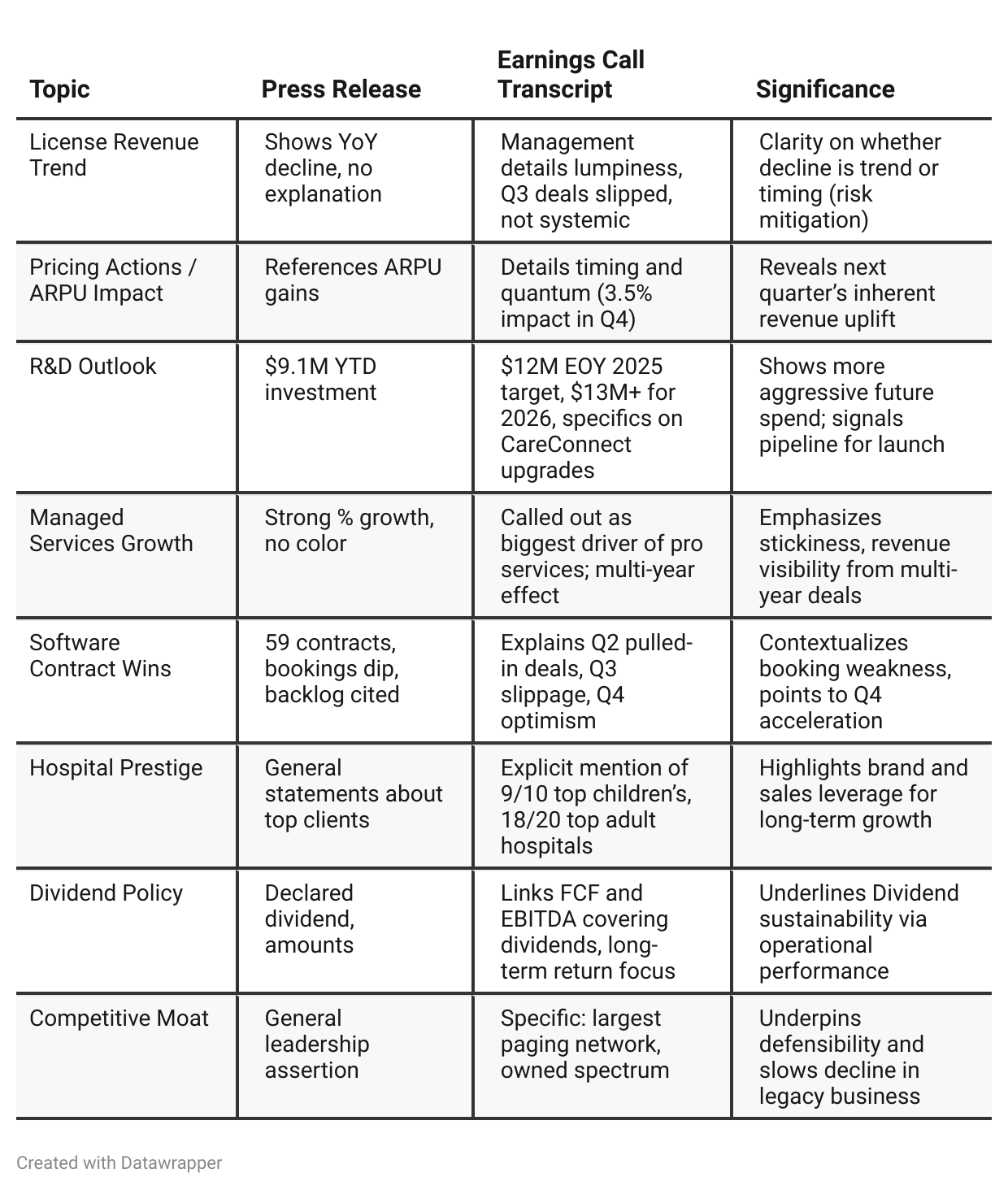

Press Release vs Call Transcript Comparison

Management Tone: Both documents reinforce a measured optimism. The call transcript, however, is much more candid about quarter-to-quarter lumpiness, and more detailed on the rationale for current (soft) bookings.

Capital Allocation: Call emphasizes how adjusted EBITDA is used to fund dividends, with historical context for returns to shareholders; this appeals to yield investors.

Product Strategy: Call provided much greater detail on the product portfolio (Console, Messenger, Mobile), and their role in hospital workflow—a potential lead-in for cross-selling/up-selling opportunities.

Competitive Positioning: Press release claims “global leadership”; call transcript substantiates it with evidence, such as hospital adoption stats and the value of network/spectrum holdings.

Visibility: Management is bullish on Q4, citing a strong pipeline. In contrast, the press release limits itself to the statistics without forward-color.

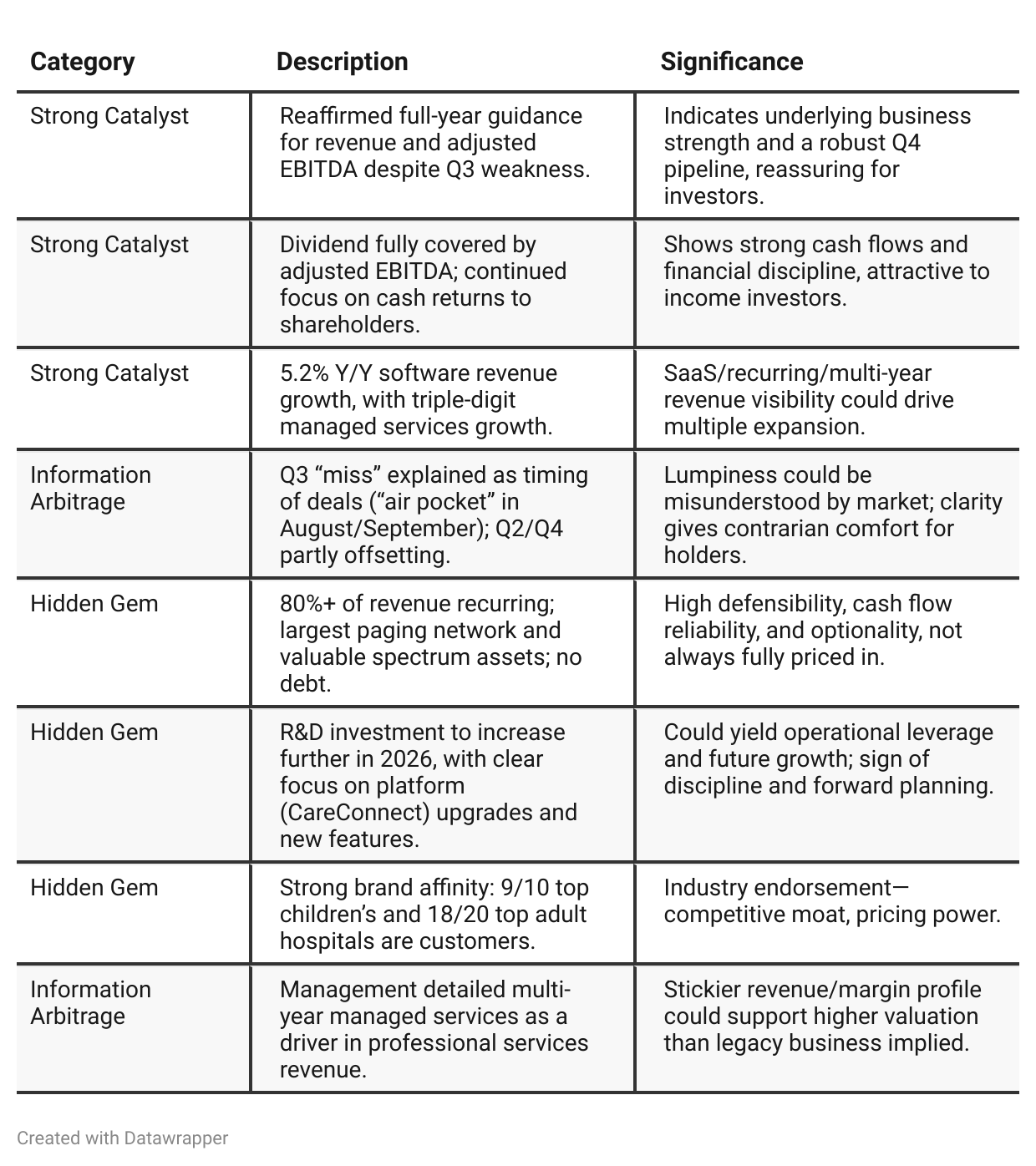

Positive Insights

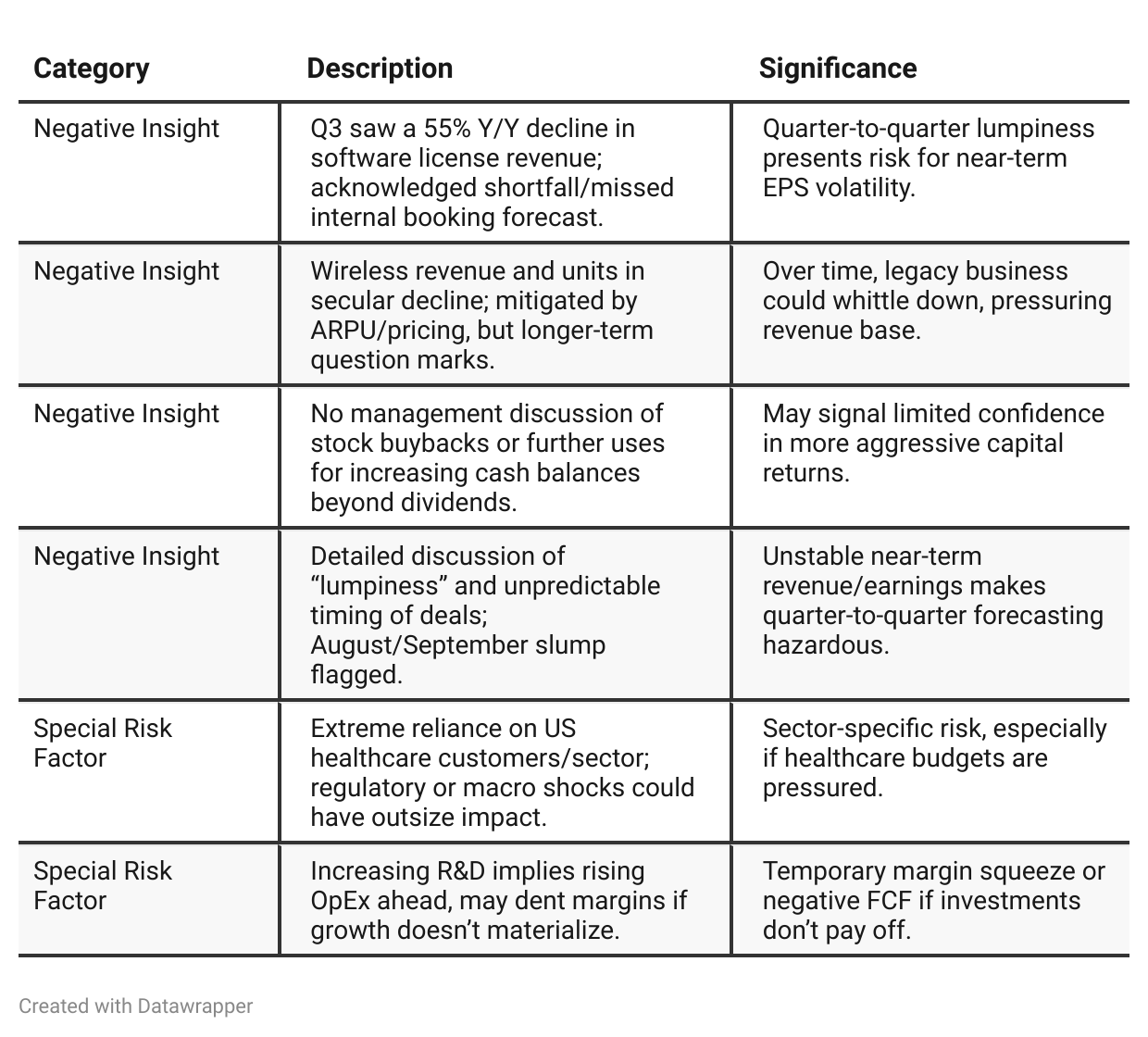

Negative Insights

Tariff Risk

Mentions of US tariffs/trade policy:

There are no explicit references to tariffs or trade policy in the transcript.

No discussion of supply chain disruption, input cost pressures, or overseas procurement.

All operational commentary focuses on software/professional services and US healthcare.

Interpretation:

Currently, tariff risk does not appear to be material to Spok’s business model based on company commentary.

However, investors should remain watchful in case essential hardware, network equipment, or software components are sourced internationally—future filings should be scanned for any updates or new risks in this area.

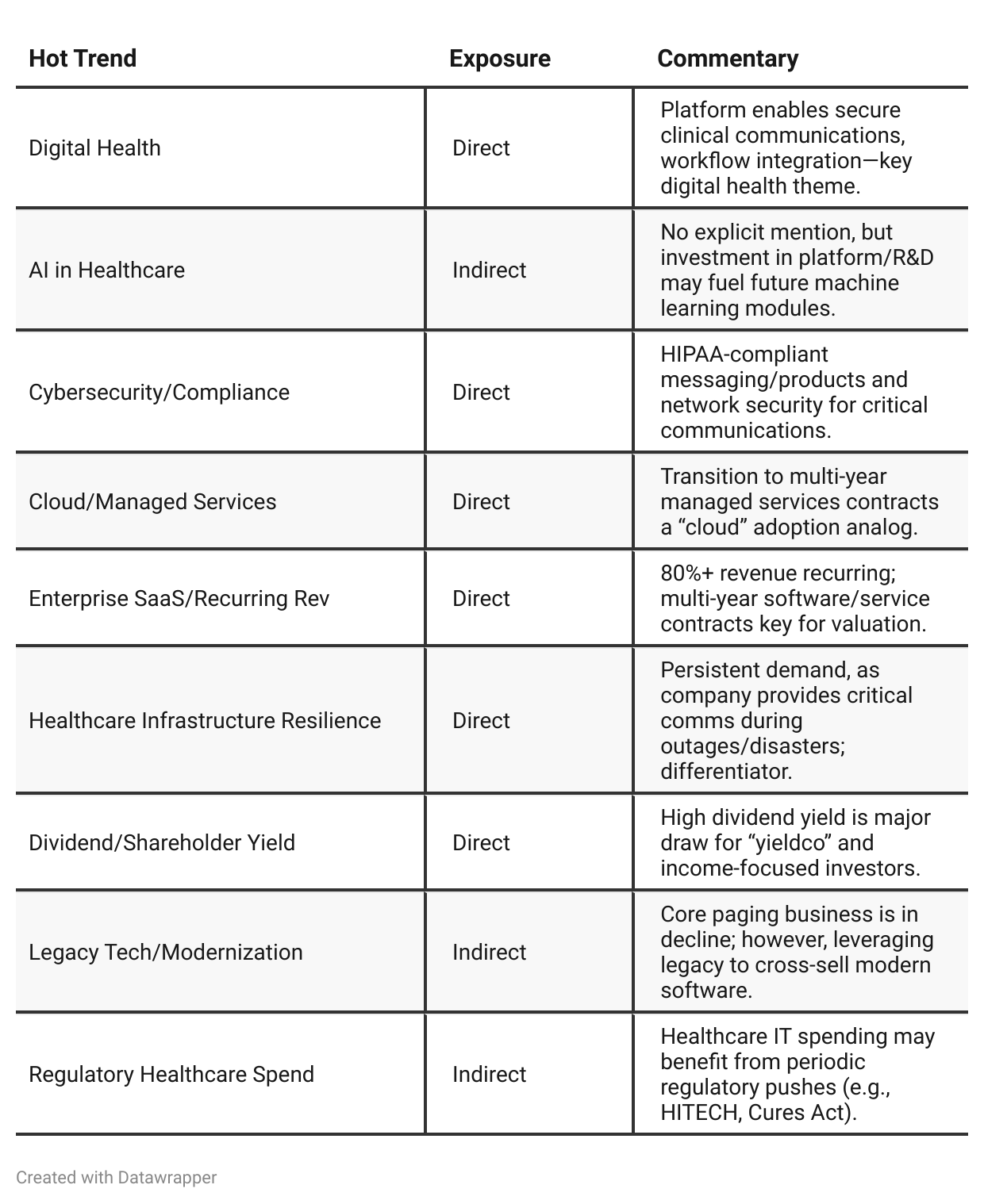

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025 paints Spok as a company in acceleration mode—celebrating robust software bookings, double-digit revenue growth, and the ability to outpace its own expectations. Management is energetic, tough on competitors, raising guidance, and highly focused on capital returns and growth investments in R&D and AI, backing a narrative of scaling success.By Q3 2025, the narrative matures: management adopts a more tactically defensive tone, transparently acknowledging short-term softness driven by deal timing, but carefully explaining that key strategic tenets (cash generation, capital return, pipeline, brand moat, platform investment) remain intact. Despite choppiness, they underscore the business’s resilience, defend their recurring revenue model, and double down on future guidance with a message of stability and long-term optimism as they head toward Q4 and 2026.

Year-over-year comparison

Q3 2024: Spok comes across as a confident, growing, and focused company with momentum in software bookings, backlog, and ARPU. Management is visible about operational wins, product launches, and market share expansion, especially in large hospitals. They are also open about experimenting in the small hospital segment with cloud solutions and targeting international markets in the APAC region. Capex and R&D increases are clearly tied to a roadmap of new product solutions. The story is one of operational execution and measured, continual growth.

Q3 2025: The narrative matures into one of resilience, predictability, and long-term endurance. Management balances ongoing pride in the company’s recurring revenue base, customer loyalty, and innovation investment with a need to explain quarterly volatility (“lumpiness”) in deals and license revenue. There is more emphasis on guidance reaffirmation, cash discipline, and dividend sustainability, and less on new wins, competitive battles, or international expansion. Concrete near-term catalysts (price increases, large deals in pipeline) are called out, but the undercurrent is one of maintaining trust in the “compounding” model rather than breakout growth.

Final Takeaway

Spok Holdings (SPOK) is in a stabilization and selective growth phase, leaning heavily on recurring healthcare communications revenue and moving to expand managed services/software. While Q3’s timing issues undermined results, management’s candor and reaffirmed guidance suggest this is not structural. Key risks remain around the roll-off of legacy wireless revenue and execution of booked pipeline. Execution on Q4 conversion, realized benefits from R&D investment, and sustained cash/dividend generation will be critical to upside. Verdict: Hold with a positive bias—but a confirmed strong Q4 showing could justify an upgrade to Buy.