Spok Holdings, Inc. (NASDAQ: SPOK) – Q2 2025 Earnings

Spok Holdings, Inc. (NASDAQ: SPOK) – Q2 2025 Earnings

Earnings Release Date: Jul. 30, 2025

Stock Price: $17.03

Market Cap: $349.3 million

Q2 2025 sales of $35.7 million vs $34.0 million in the prior year

Q2 2025 EPS of $0.22 vs $0.17 in the prior year

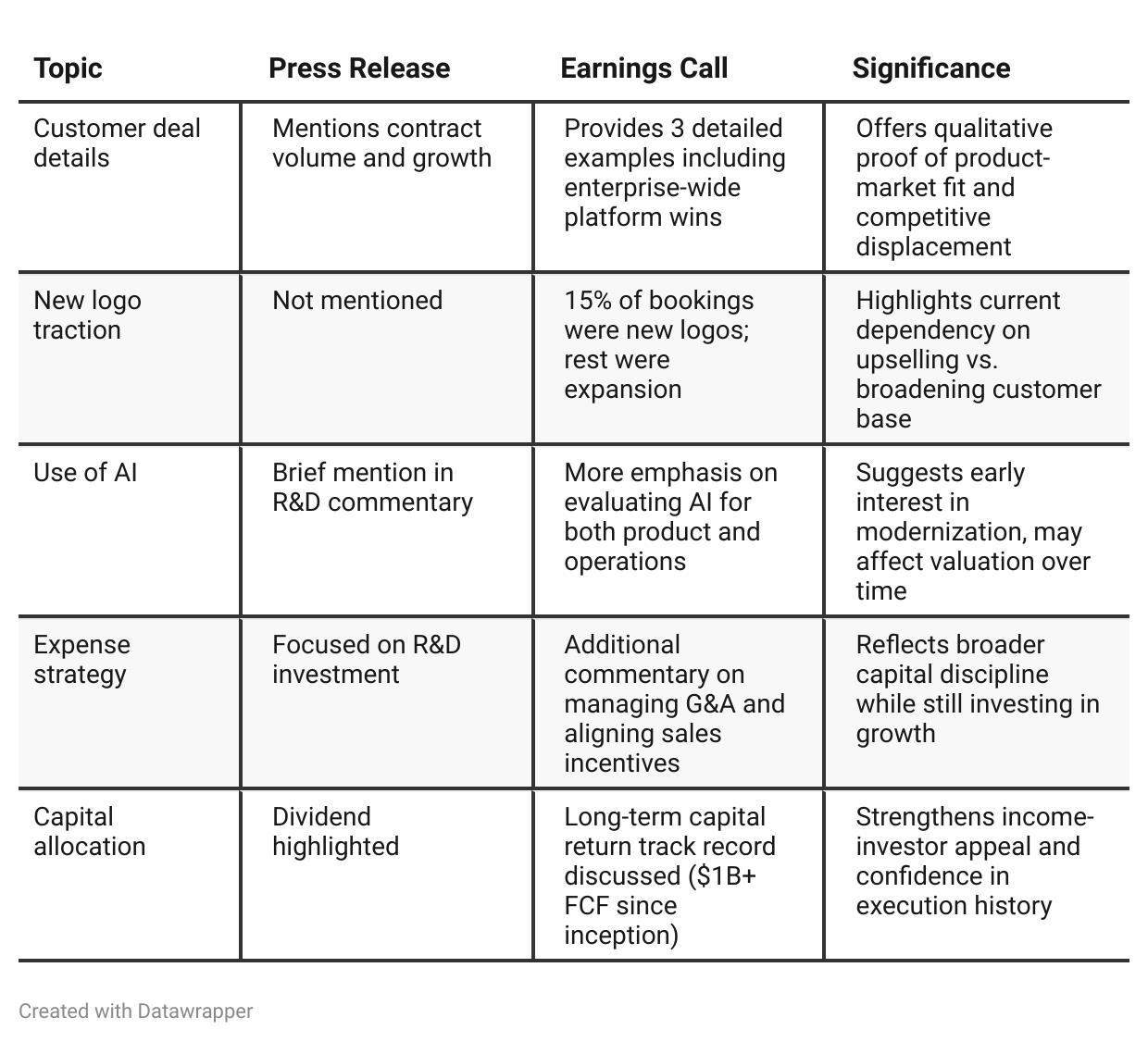

Press Release vs Call Transcript Comparison

The press release emphasizes headline results—strong YoY growth, rising bookings, and raised guidance—while the earnings call adds essential color around customer wins, execution strategies, and future priorities like AI and new logo development.

The contrast highlights a core narrative: Spok is no longer just a pager business but is transitioning into a software-first platform. However, the pace of that transition—and the mix between growth and legacy revenues—requires close attention.

The earnings call’s deeper operational transparency gives investors higher confidence in the company’s strategic direction and its ability to maintain shareholder returns while investing for the future.

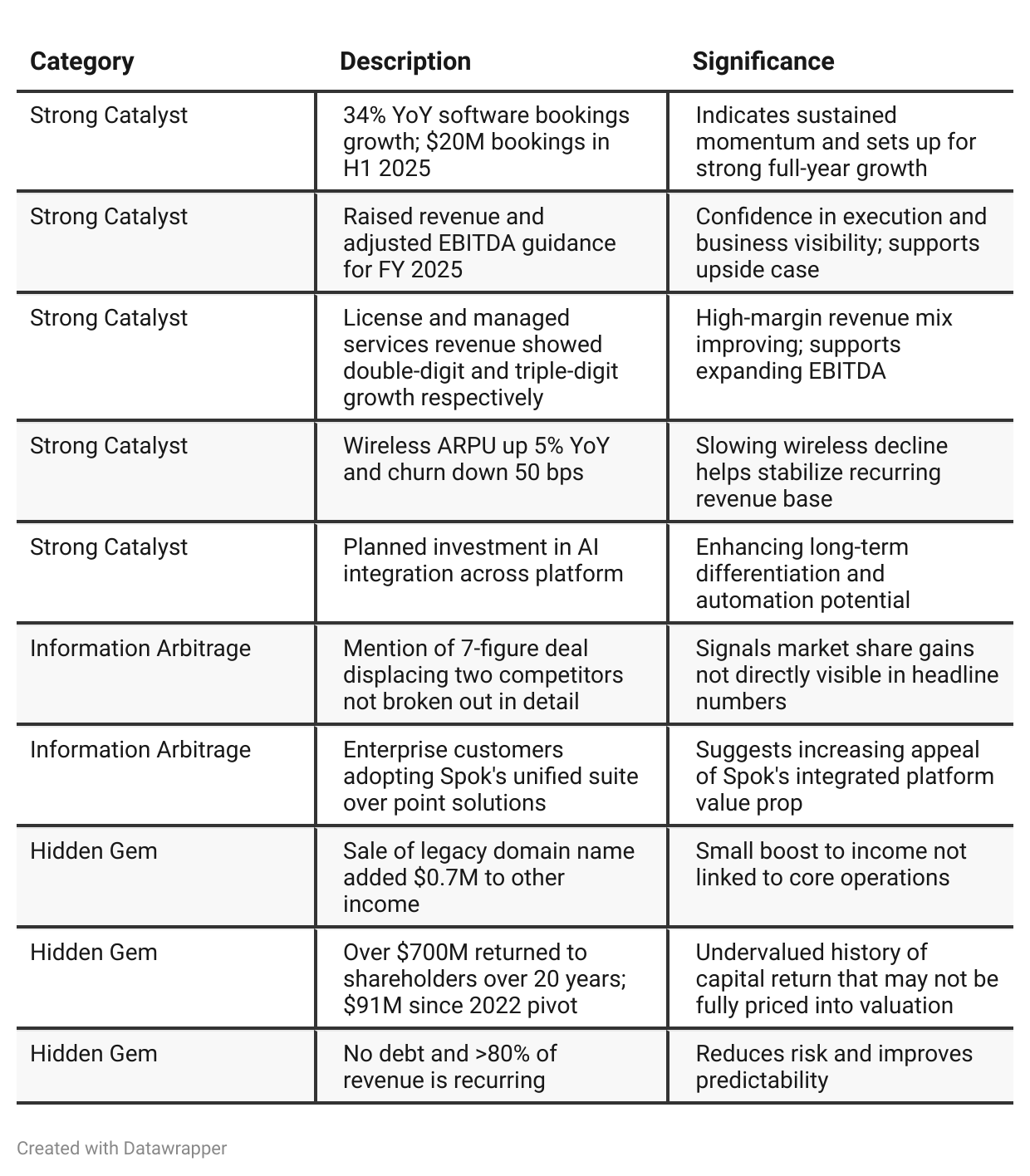

Positive Insights

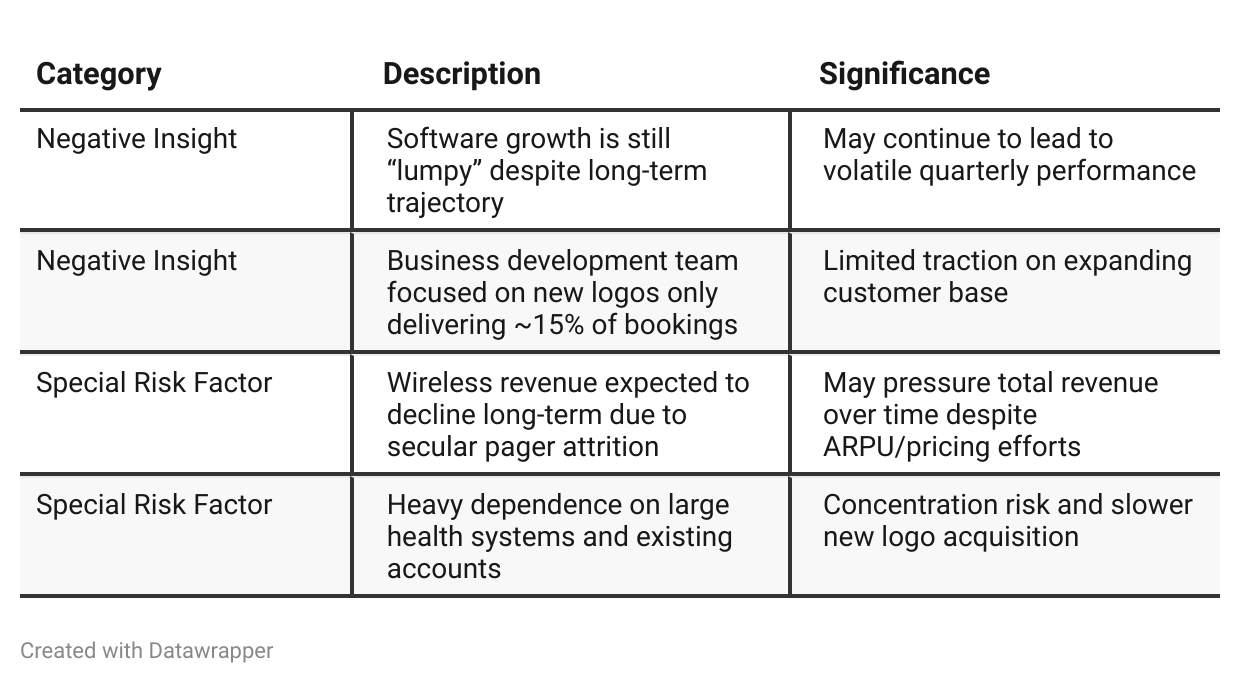

Negative Insights

Tariff Risk

There were no direct or indirect references to tariffs, trade policies, or international supply chain concerns in the transcript. Spok's customer base is U.S.-focused, particularly health systems, and no global sourcing issues or foreign dependency risks were disclosed.

Previous Earnings Call

Quarter-over-quarter comparison

From Q1 to Q2 2025, Spok Holdings evolved its narrative from a cautious optimism rooted in maintaining momentum and managing downside risk, to a confident, forward-leaning posture fueled by strong execution. The company shifted from reiterating conservative guidance amid macro uncertainty to raising full-year expectations for both revenue and EBITDA.

The second quarter showcased acceleration in software bookings, an uptick in enterprise contract sizes, and clearer articulation of competitive wins. The tone shifted from defending the durability of the legacy wireless business to leaning into software-led growth, with a growing emphasis on AI-driven innovation and new logo acquisition.Spok’s story in 2025 is transforming from one of defensive cash-flow management to offensive strategic expansion in healthcare communications.

Year-over-year comparison

From Q2 2024 to Q2 2025, Spok’s narrative shifted from maintaining cautious optimism amid difficult YoY comps to confidently asserting renewed growth momentum. In 2024, management leaned heavily on Spok’s value as a utility-like provider and its capital-return strategy to reassure investors.

By 2025, the company began touting tangible gains: large multiyear software deals, AI plans, and triple-digit growth in managed services. While wireless headwinds remain, they are now framed as being successfully offset by pricing, ARPU improvements, and bundled solutions.

The company’s messaging has matured into a more growth-forward posture, signaling that its strategic pivot is bearing fruit.

Final Takeaway

Spok Holdings is in a stable growth phase, driven by software revenue acceleration and disciplined expense control. While wireless revenue faces long-term secular decline, strong pricing power and a sticky customer base help offset this.

The company’s focus on enterprise solutions, cash generation, and returning capital to shareholders underpins its long-term thesis. Execution on AI integration and expansion beyond the installed base will be key to valuation re-rating.

Verdict: Buy, with upside potential if new customer acquisition accelerates and software growth sustains.