Gibraltar Industries, Inc. (NASDAQ: ROCK) – Q3 2025 Earnings

Gibraltar Industries, Inc. (NASDAQ: ROCK) – Q3 2025 Earnings

Earnings Release Date: Oct. 30, 2025

Stock Price: $67.13

Market Cap: $1996.1 million

Q3 2025 sales of $310.9 million vs $277.1 million in the prior year

Q3 2025 EPS of $1.11 vs $1.10 in the prior year

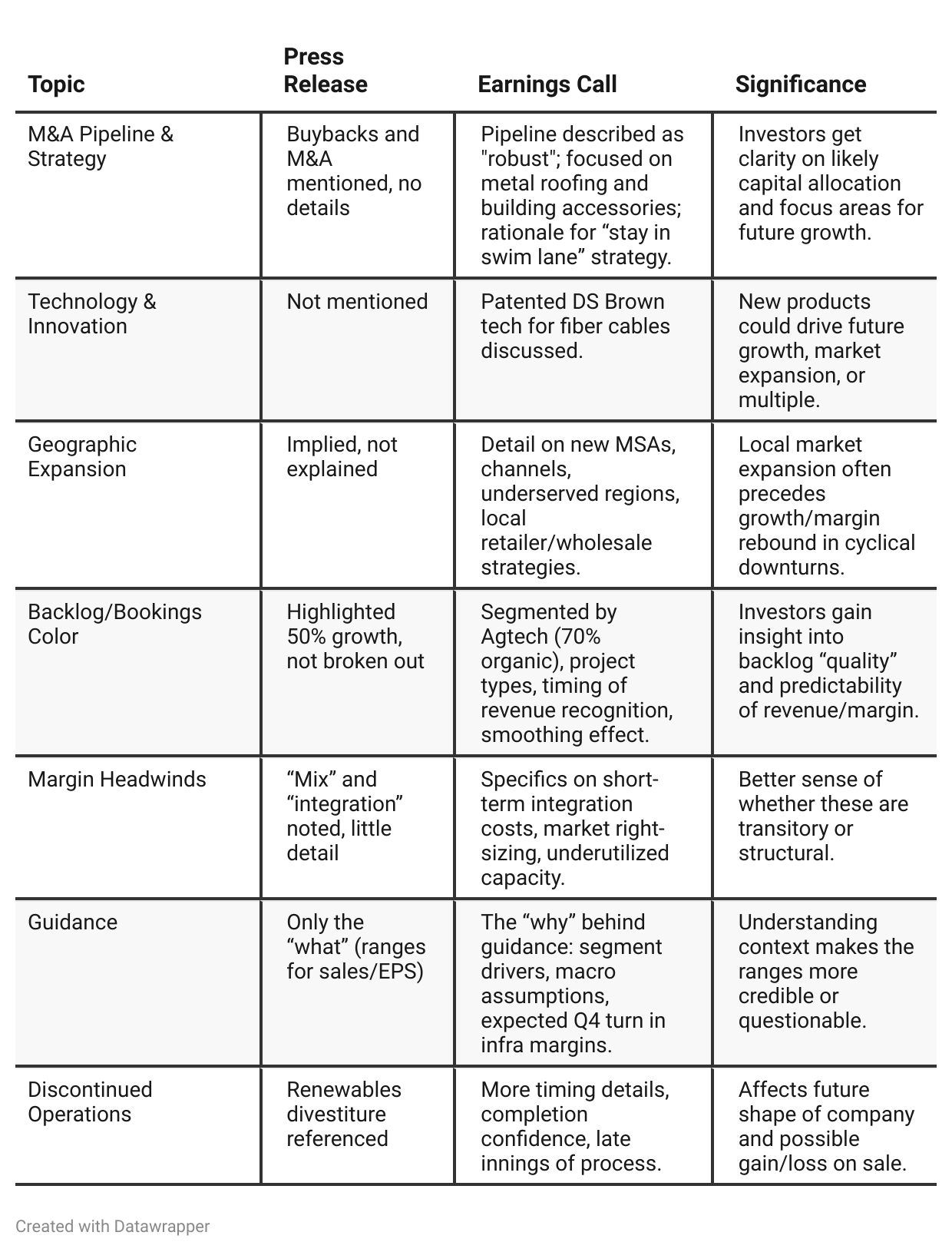

Press Release vs Call Transcript Comparison

Earnings Call Gives More Forward-Looking Detail: The transcript contains richer forward-looking commentary on operational efficiency, cadence, and risk than the relatively numbers-focused press release.

Synergy/Integration Focus and Timing: The company is undertaking major integration/systemization work in residential (metal roofing), with costs front-loaded and benefits lagging but potentially substantial.

Candid View on Market Conditions: Management is open about macro and project headwinds (e.g., inventory right-sizing, labor availability, weather reducing roof damage/repairs).

Efficiency and Balance Sheet Strength: Commentary on untapped revolver, debt-free status, and capital allocation (buybacks and M&A) as a strategic buffer in downturns.

Segment Portfolio Simplification: Renewables divestiture reflects renewed focus on 3 remaining segments; implies improved capital efficiency and focus.

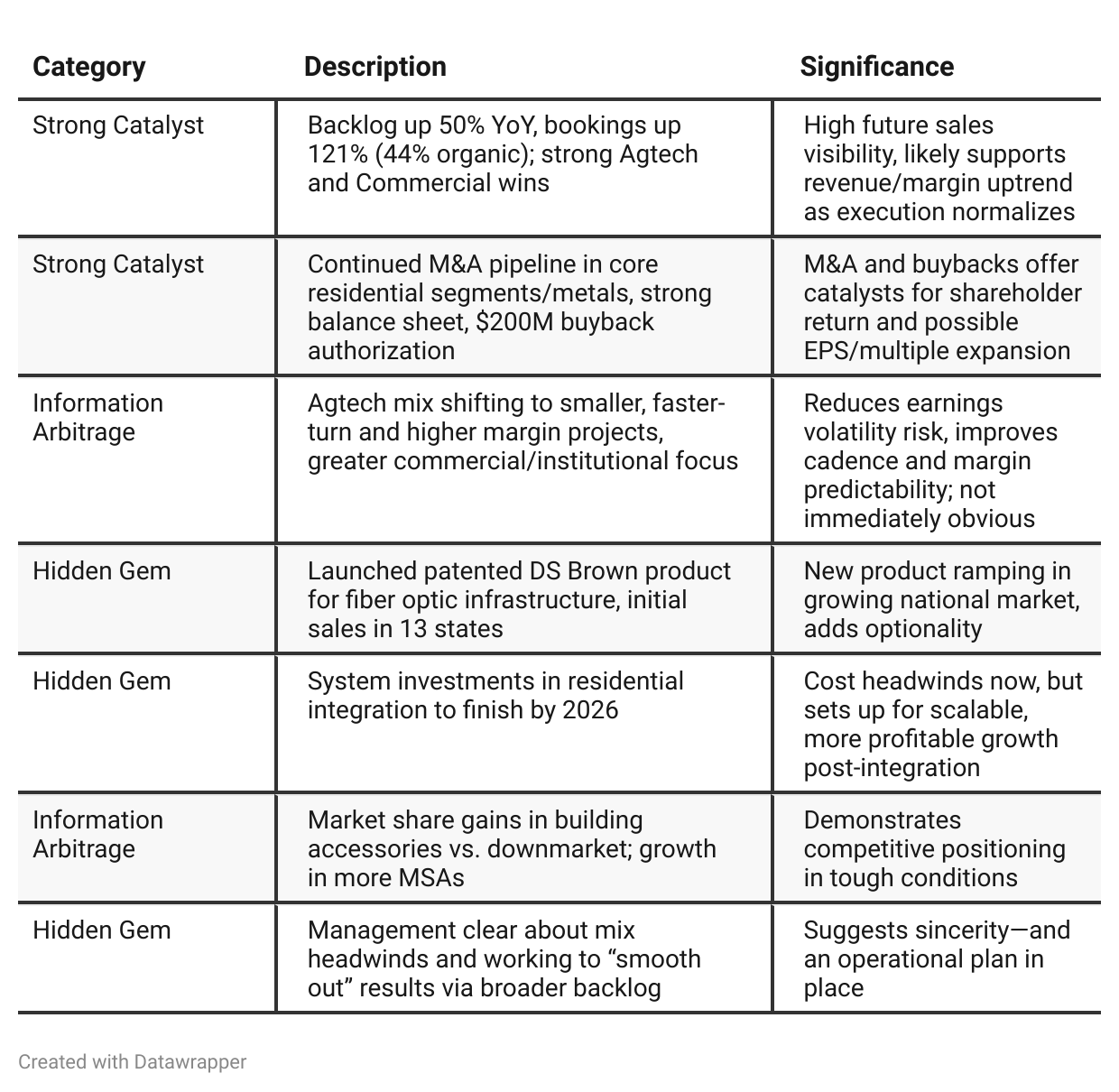

Positive Insights

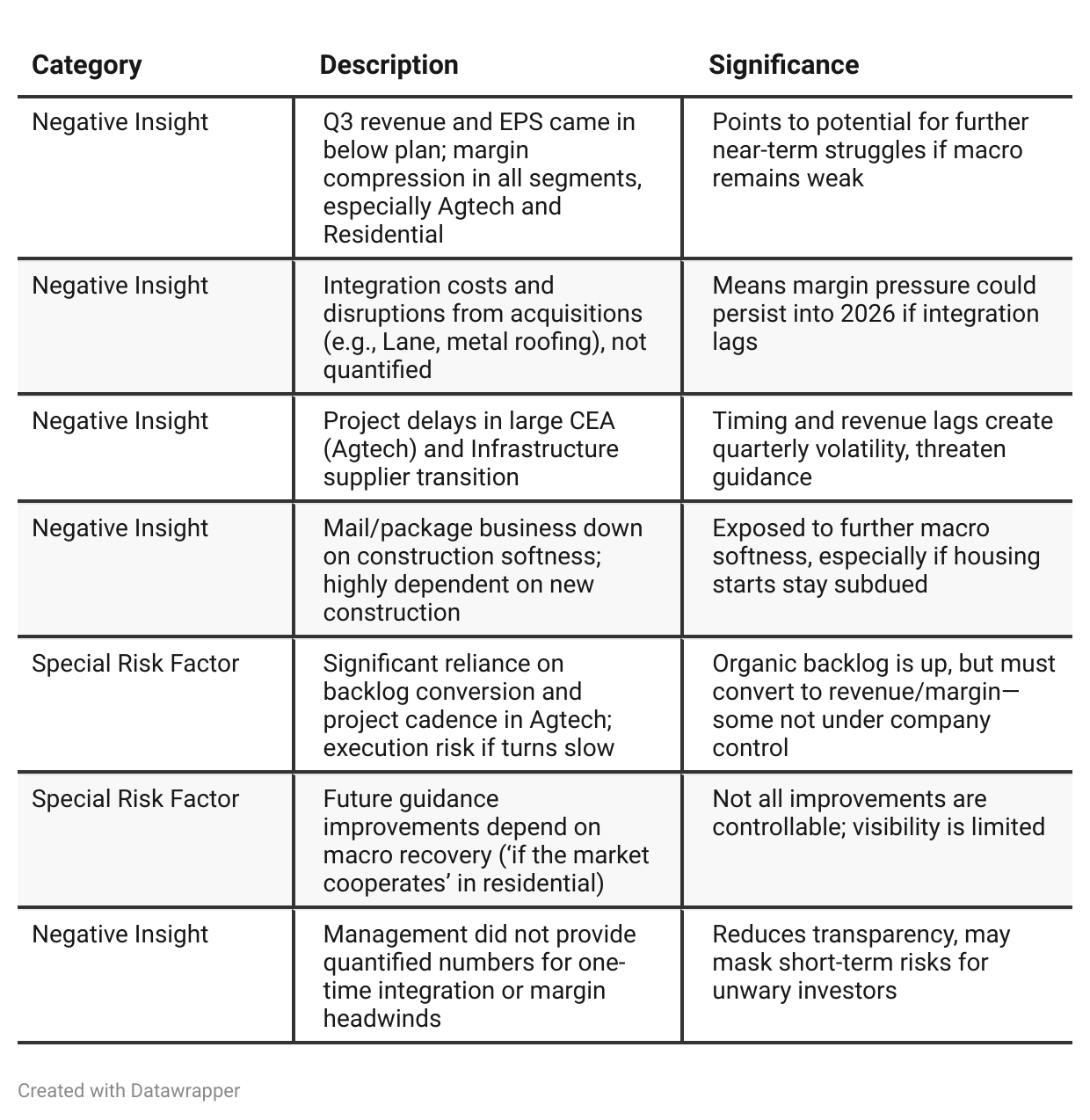

Negative Insights

Tariff Risk

Transcript Commentary:

Management stated, “some of the tariffs we’ve all been dealing with, we’ve made it somewhat of a non-issue, but you still got to go execute things like pricing, cost reduction, 80-20 initiatives, and I think the team’s done a pretty good job of neutralizing as much as they can in that macro environment…”

No forward-looking specific discussion on tariffs, trade policy, or possible new impacts.

Analysis:

Tariffs and Trade are an ongoing background risk, previously absorbed via pricing and cost initiatives. Gibraltar is not currently experiencing acute margin pressure due to tariffs, nor are they highlighted as a future risk by management.

No mention of supply chain shifts, renegotiated contracts, or new tariff-driven pricing actions in the current transcript.

Management is confident in operational execution as the primary tool for offsetting these headwinds.

Implications: While tariffs are always a macro headline risk, Gibraltar’s management views them as manageable for now via pricing/cost discipline. There are no new or acute trade/tariff risks visible in this quarter’s transcript. Stay alert for any changes in future guidance or segment disclosures if trade environment shifts.

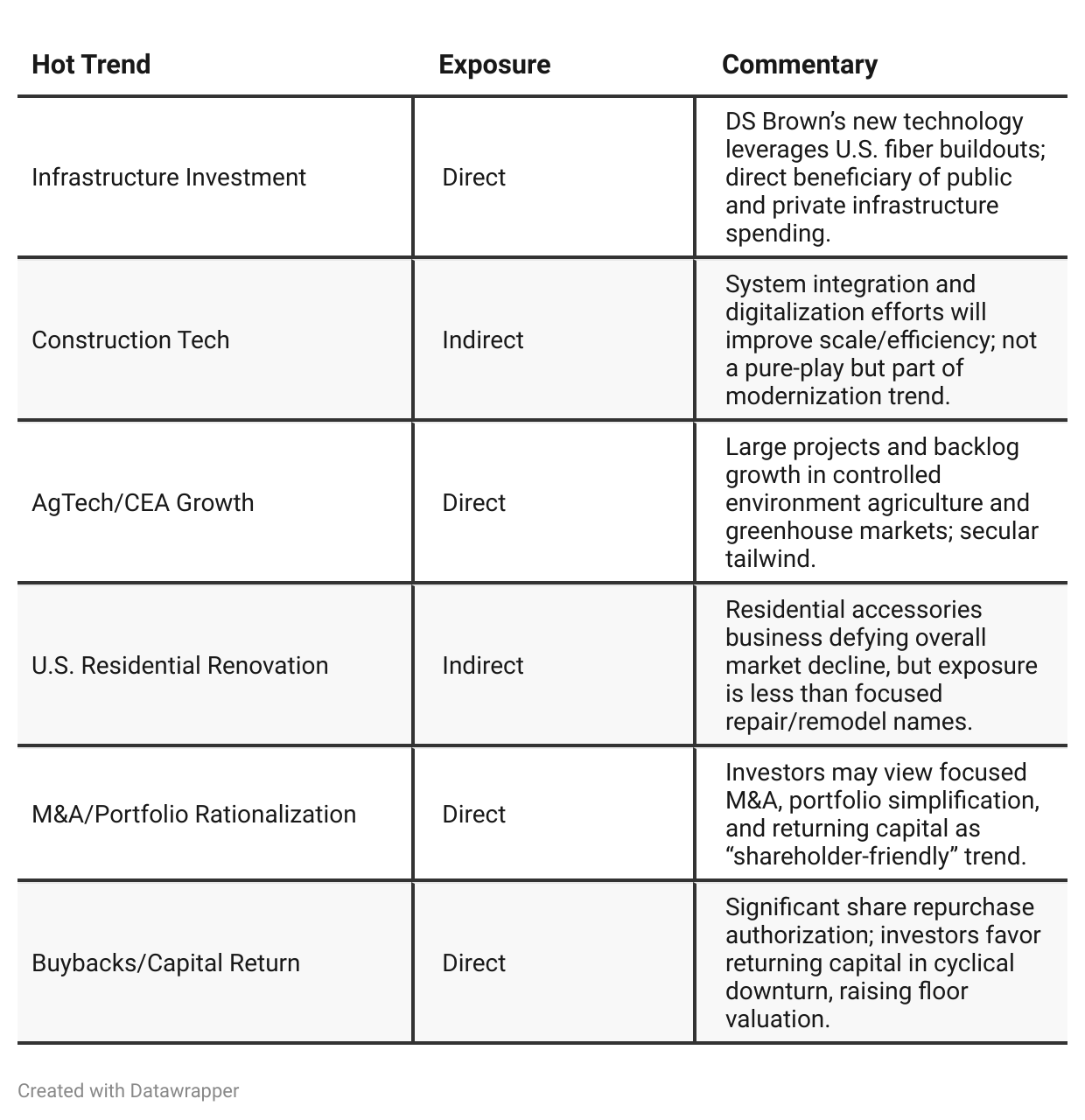

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025: Gibraltar delivered strong results despite market headwinds, fueled by a decisive strategic pivot — exiting renewables to focus on building products and structures. Management was ebullient about portfolio simplification, new M&A, and robust expansion initiatives. There was a strong forward-looking tone: “We’re outpacing the market, investing for growth, and optimizing our channels and brands for a long runway of value creation.”Q3 2025: As the year progressed, macro headwinds and project timing issues became more acute: end-markets remained weaker-for-longer, and project delays (particularly in ag tech) suppressed near-term growth and compressed margins. Management shifted to a more cautious and realistic tone, focusing on resilience and execution in a tough environment — all while underlining the success of their diversification and backlog-building strategies. Cash generation and balance sheet strength were again central, as were the long-term benefits of accelerated integration and strategic M&A within focused “swim lanes.” The narrative is now one of delivering through turbulence while positioning for scalable, margin-accretive recovery as markets and investments normalize.

Year-over-year comparison

Q3 2024: Gibraltar is emerging from a challenging quarter, with solar weighing heavily on overall results. Management is focused on operational discipline, product innovation, and geographic expansion in the core residential and ag tech businesses. Reliable cash flow and profit growth (when excluding renewables) demonstrate the strength of the diversified model. The outlook is one of resilience—steering successfully through headwinds—while confidently preparing for a turnaround in core markets and the solar sector post-tariffs/regulatory actions.

Q3 2025: One year later, Gibraltar has decisively shifted to a transformation and future-proofing narrative. The renewables segment is being exited, and the entire focus is on scaling and integrating core businesses (residential, ag tech, infrastructure) with a much sharper M&A and systems focus. While headwinds in core markets persist, the company emphasizes backlog, bookings, and operational tempo as drivers for medium-term acceleration. Discussions of customers, markets, and competition have become more nuanced, with greater region/channel granularity. Margins face near-term pressure, but management conveys confidence that portfolio optimization, backlog diversity, and foundational investments (systems, local reach, new products) position Gibraltar for outperformance as market cycles turn.

Final Takeaway

Gibraltar Industries (ROCK) is in an operational transformation and growth phase, prioritizing margin recovery, backlog conversion, and disciplined M&A. While a rising backlog, expanding product pipeline, and strong balance sheet underpin long-term opportunity, near-term earnings are pressurized by macro softness, integration headwinds, and execution risk on large projects. Execution on systems integration, effective conversion of backlog, and realization of M&A synergies will be critical for share price upside. Verdict: HOLD—with potential for upgrade if margin/acquisition execution accelerates or housing end-markets inflect.