Gibraltar Industries, Inc. (NASDAQ: ROCK) – Q2 2025 Earnings

Gibraltar Industries, Inc. (NASDAQ: ROCK) – Q2 2025 Earnings

Earnings Release Date: Aug. 6, 2025

Stock Price: $64.42

Market Cap: $1914.3 million

Q2 2025 sales of $309.5 million vs $273.6 million in the prior year

Q2 2025 EPS of $1.13 vs $1.02 in the prior year

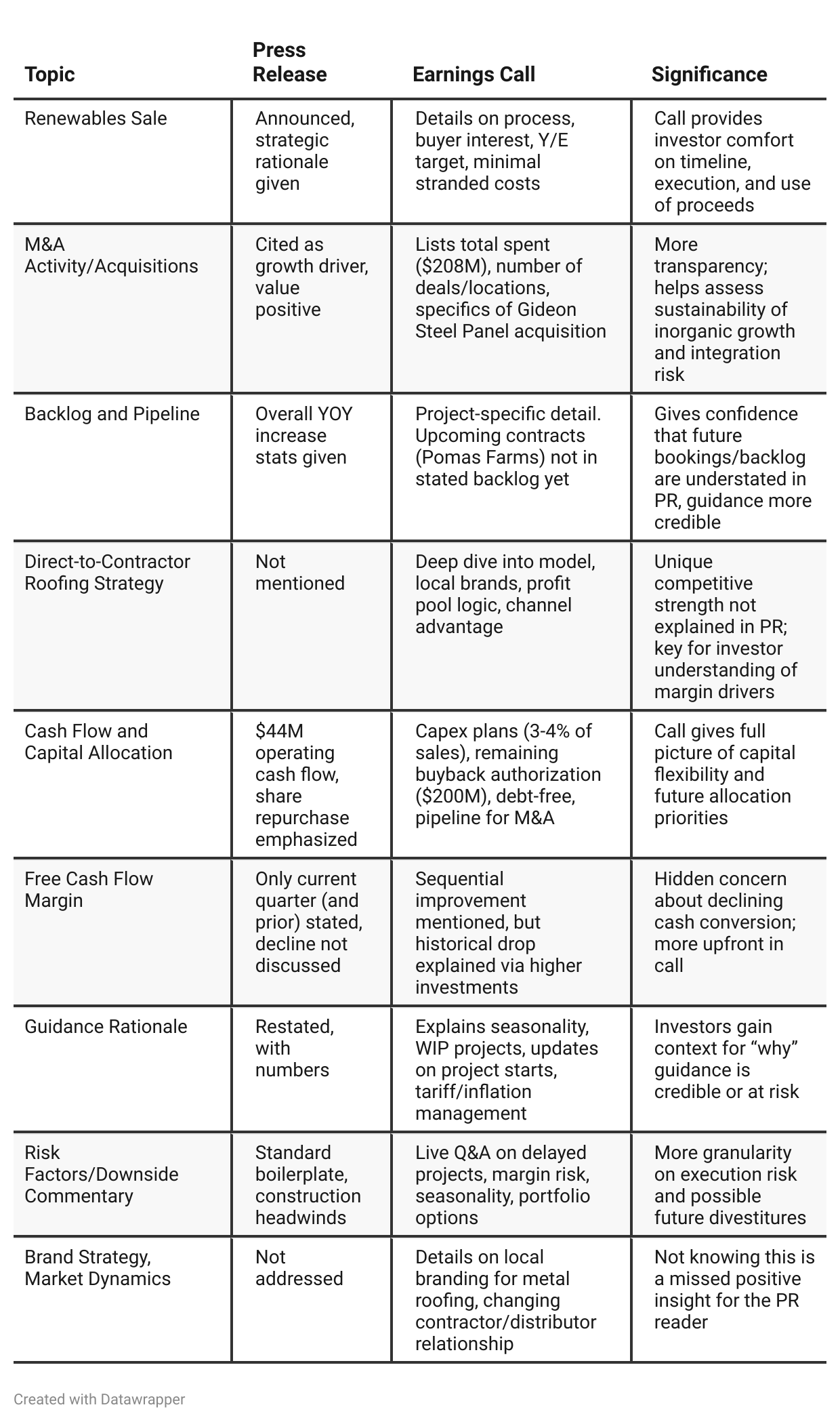

Press Release vs Call Transcript Comparison

Management Tone: The call demonstrates high confidence and command of operating details, which offsets some concerns about project delays and free cash flow underperformance. The PR, while positive, lacks this reassurance.

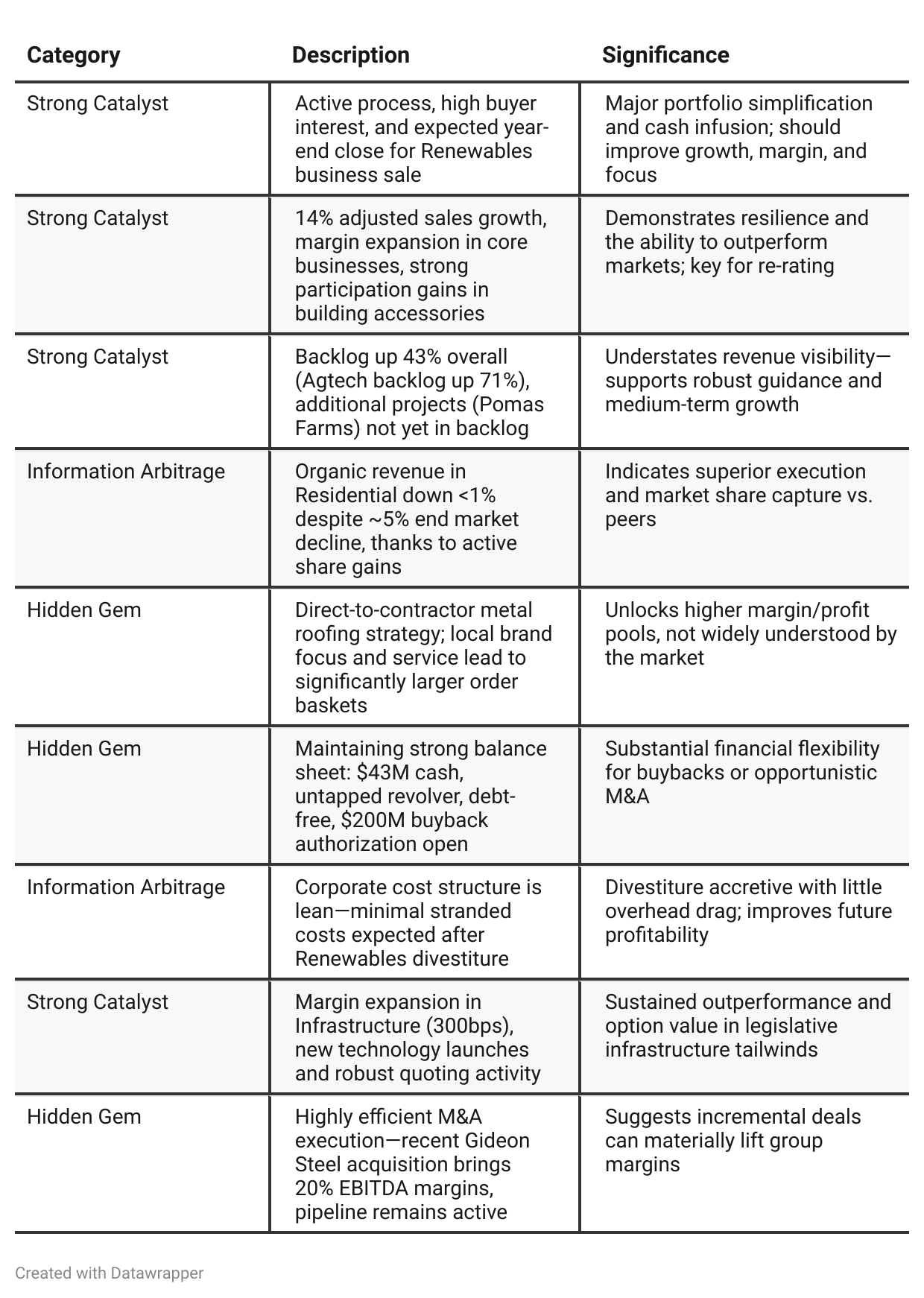

Operational Focus: The call gives significant insight into “participation gains” (market share capture in down markets), which is a critical investment thesis in cyclical industries.

Portfolio Agility: The call reveals openness to monetization of “Infrastructure” and an advanced approach to asset allocation—signs of optionality for investors.

Integration/Acquisition Execution: While both documents flag M&A as a growth driver, only the call offers validation (Gideon acquisition performance, Lane Supply integration, existing management retained).

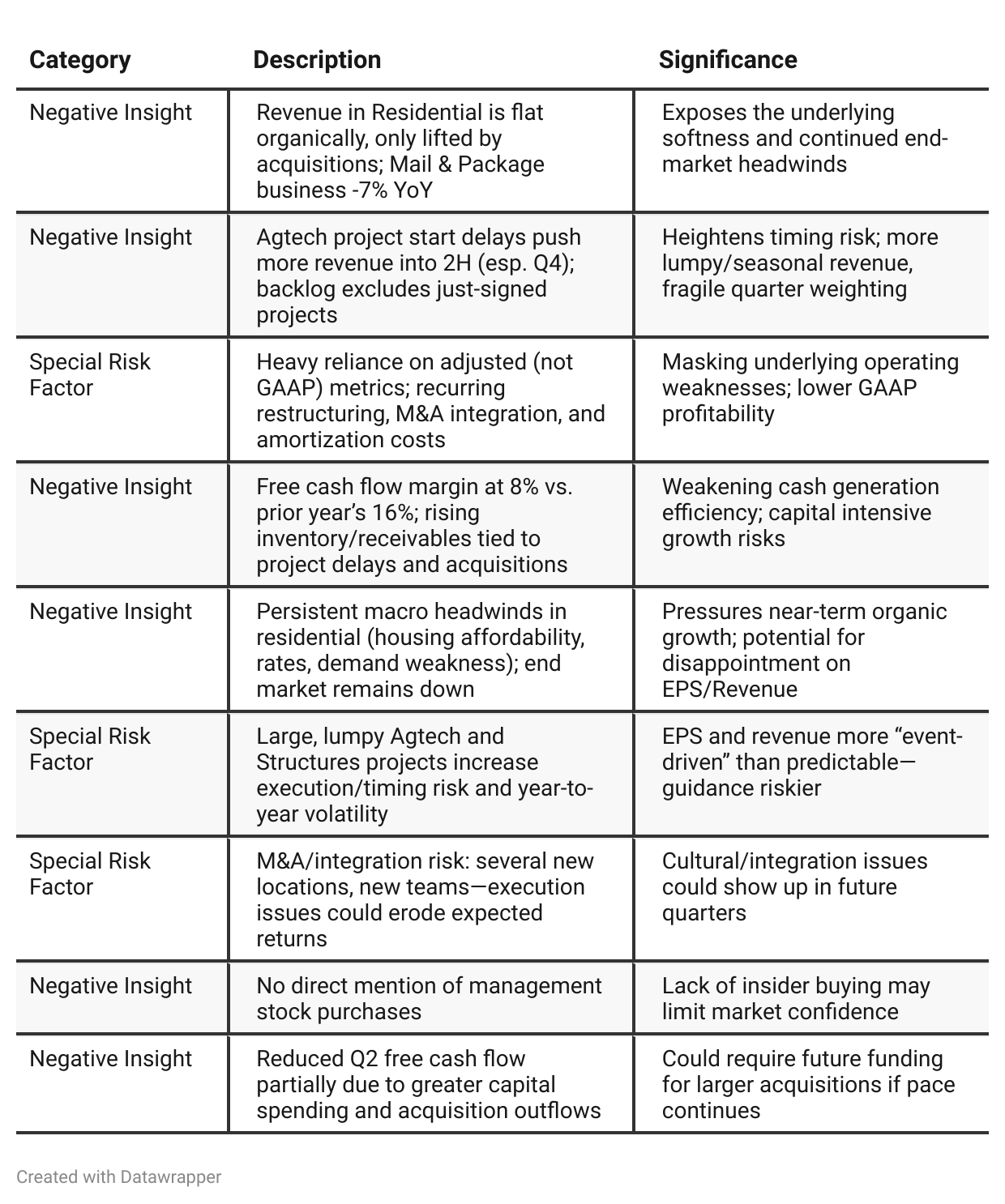

Adjusted vs. GAAP Metrics: There’s liberal use of “adjusted” numbers to tell a positive story, but the call more openly acknowledges restructuring, integration, and non-recurring costs as ongoing issues.

Unstated Press Release Risks: The PR understates the increasing working capital investment (receivables, inventory)—a common risk during M&A or project ramp-up cycles.

Positive Insights

Negative Insights

Tariff Risk

Discussion of Tariffs: Management described tariffs as a “dynamic environment,” but emphasized that impacts have been “minimized” to date through robust week-to-week tracking, supply chain flexibility, and contract clauses tied to commodity indexes.

Actions Taken:

Active tracking by component and country of origin (HTS code).

Real-time pricing adjustments and cost recovery built into contracts.

Supply chain discipline and local sourcing focus.

Impact on Revenue/Supply Chain/Profitability: Minimal impact mentioned for the current year; implied that systems in place (vs. 2021-22 inflation spike) are effective.

Competitive Positioning: Leadership conveyed confidence that their pricing and cost processes gave them an edge in managing tariffs.

Forward-Looking: Management does not expect material tariff headwinds for the rest of the year, but continues to monitor developments week-to-week, indicating vigilance and readiness to pivot as policy shifts.

Sentiment Analysis

The overall sentiment toward $ROCK (Gibraltar Industries) is bullish. Investors express enthusiasm about the stock’s fundamentals, such as strong cash flow, low debt, attractive valuation, and ties to robust sectors like infrastructure and housing, which are poised for growth. Users highlight value buys, expectations of price appreciation, and favorable risk/reward, signaling optimism and confidence in the stock’s upward potential.

Previous Earnings Call

Quarter-over-quarter comparison

Between the Q1 and Q2 2025 calls, Gibraltar Industries’ narrative has evolved from one of cautious optimism and risk management in a volatile, uncertain environment (with all segments, including Renewables, part of the plan), to a phase of focused transformation and higher confidence. The company announced a definitive strategic shift to divest Renewables and concentrate resources on higher-growth, higher-margin core businesses. Operationally, Q2 messaging is more aggressive on outperformance and proactive expansion, particularly via M&A, with clear communication on direct-to-contractor differentiation and margin drivers. Financially, the focus has tightened around adjusted results and core business performance, with less emphasis on managing headwinds and more on executing a simplified growth agenda.Year-over-year comparison

From Q2 2024 to Q2 2025, Gibraltar’s narrative transforms from resilient operator in a volatile, regulation-heavy, and often externally constrained industry, to focused portfolio manager executing on a deliberate shift toward higher-margin, higher-predictability segments.

In Q2 2024, management is keenly aware of crosscurrents—demand softness, destocking, regulatory/tariff headwinds—but stresses their ability to “outperform the market” and improve margins via process, product, and regional expansion. Renewables, though pressured, is still central to reporting and planning.

By Q2 2025, the company is signaling a new phase: shedding Renewables, celebrating “simplification,” and positioning “Building Products” and “Structures” as strategic, high-visibility growth engines. There’s clear progress in backlog, M&A impact, geographic/channel/brand strategy, and the message is one of proactive control—“we are shaping our destiny” as opposed to enduring external headwinds.

Final Takeaway

Gibraltar Industries is in a restructuring and growth optimization phase, focusing on divesting non-core assets and scaling its core building products and structures businesses. While backlog growth and strategic execution in direct-to-contractor channels create positive catalysts, execution risk in large project timing, free cash flow softness, and persistent demand headwinds in residential remain concerns. Investors should closely track the Renewables divestiture progress, FCF trends, and backlog conversion in Agtech and Infrastructure for future stock performance. Verdict: Hold, with upside contingent on deliverable M&A integration and backlog realization.