CPI Card Group Inc. (NASDAQ: PMTS) – Q3 2025 Earnings

CPI Card Group Inc. (NASDAQ: PMTS) – Q3 2025 Earnings

Earnings Release Date: Nov. 04, 2025

Stock Price: $17.53

Market Cap: $199.0 million

Q3 2025 sales of $138.0 million vs $124.8 million in the prior year

Q3 2025 EPS of $0.19 vs $0.11 in the prior year

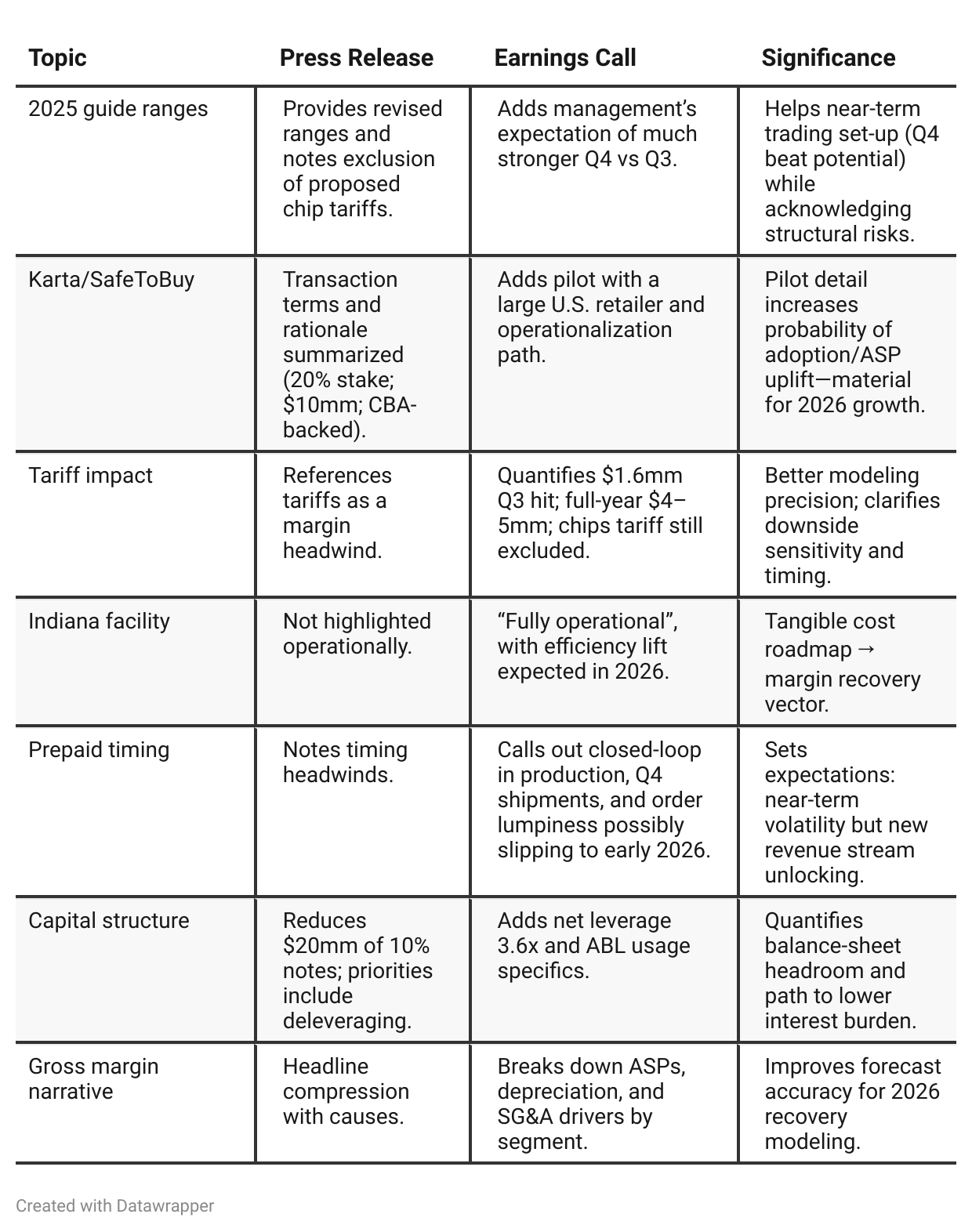

Press Release vs Call Transcript Comparison

The Card@Once SaaS installed base (>17k at >2k FIs) reinforces a recurring revenue layer that’s less cyclical than card manufacturing; could support a quality-of-revenue multiple if margins normalize.

Mgmt highlights eco-focused offerings and healthcare vertical expansion—helps multiple by leaning into secular narratives (sustainability, healthcare payments).

Industry backdrop remains healthy: U.S. card-in-circulation +7% 3-yr CAGR (Visa/Mastercard).

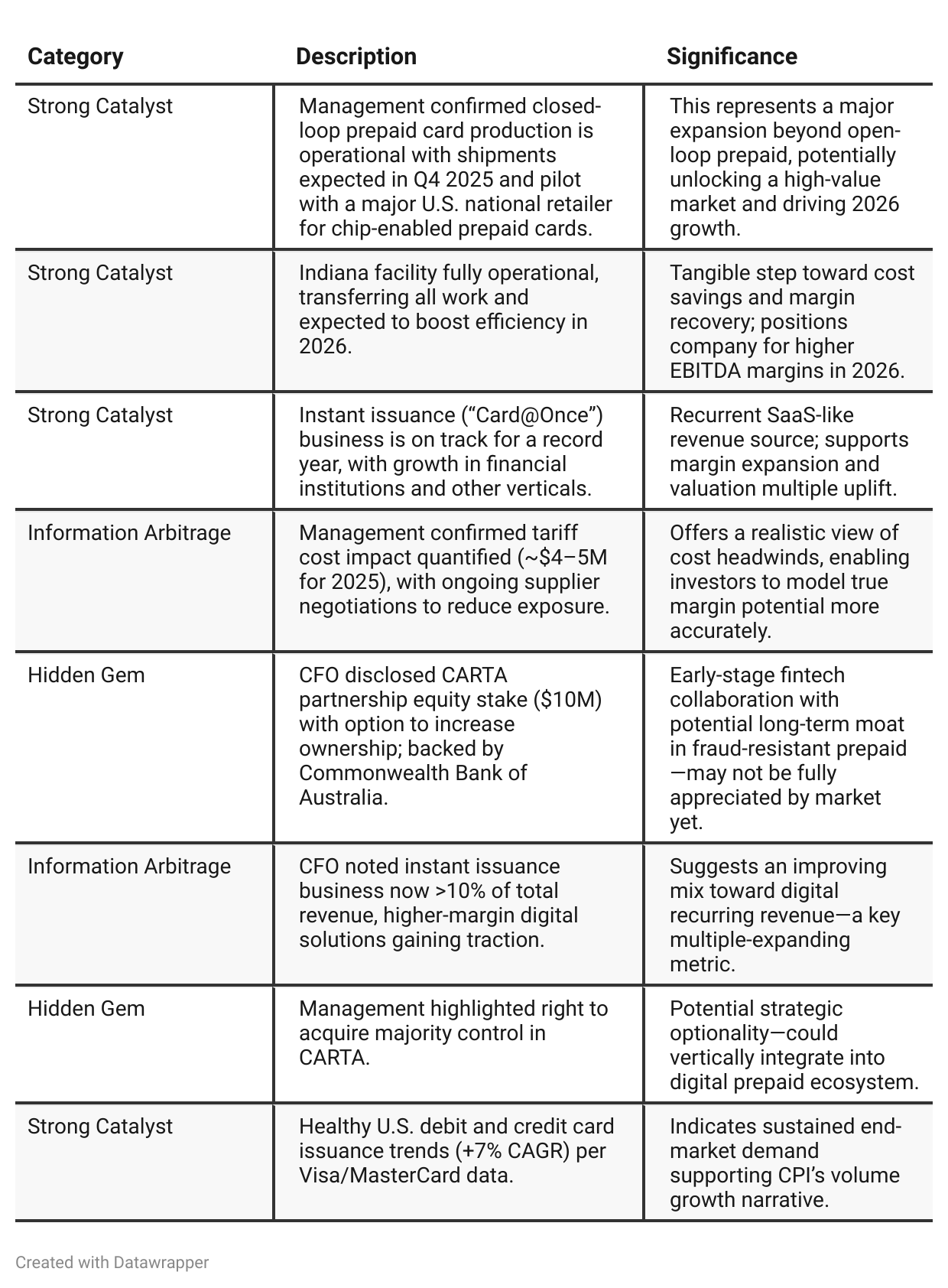

Positive Insights

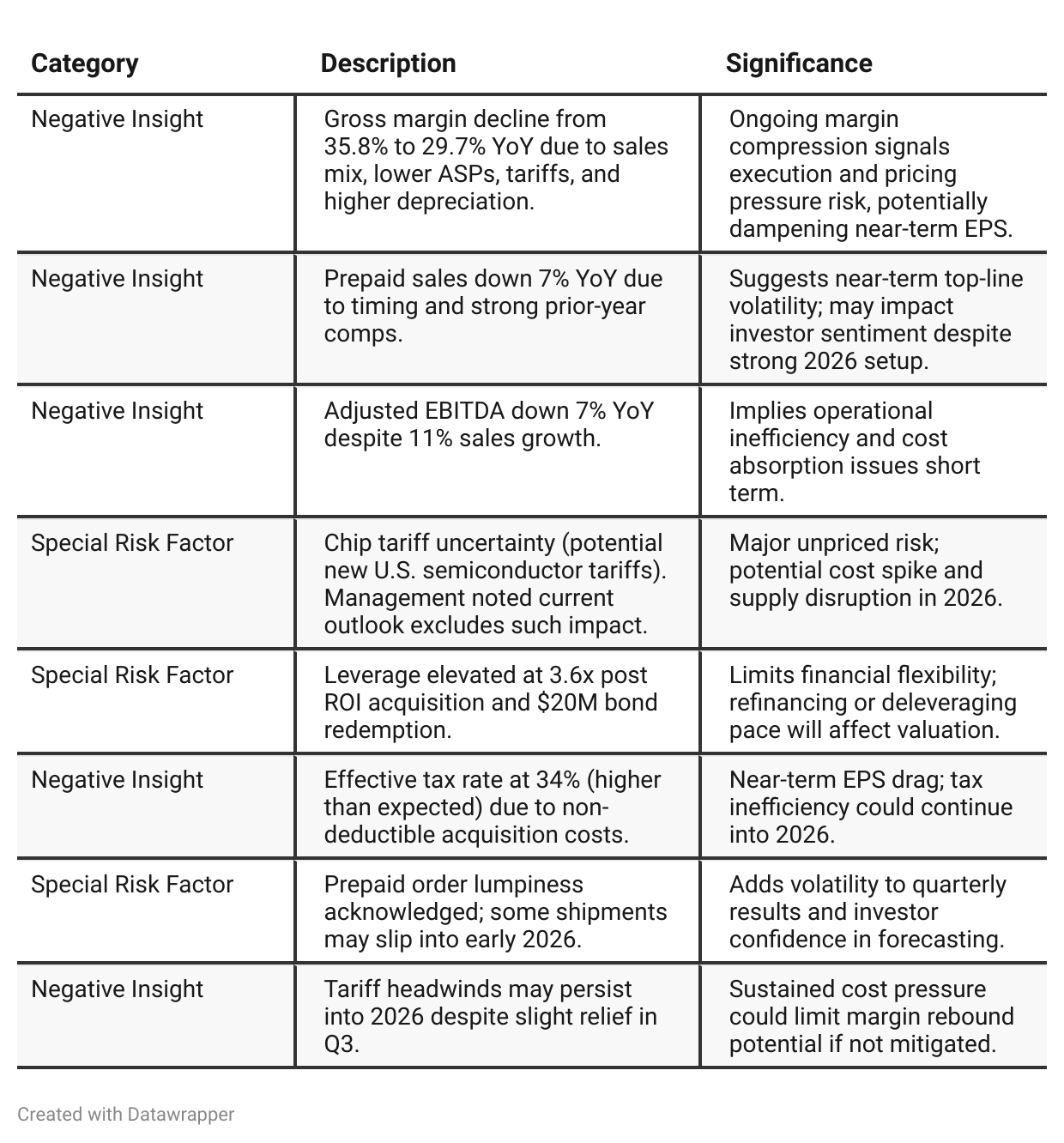

Negative Insights

Tariff Risk

Current Situation: $1.6M tariff expense in Q3, full-year $4–5M expected.

Future Risk: Potential U.S. semiconductor tariffs remain unimplemented but could affect chip inputs in 2026.

Mitigation Actions:

Buying chips at higher-than-normal inventory levels to front-run potential tariffs.

Suppliers may be U.S.-based, possibly exempt.

Actively negotiating with suppliers to offset costs.

Potential Effects:

If tariffs enacted, margin compression across industry—CPI would not be uniquely disadvantaged.

Near-term cash flow hit, but longer-term manageable given balanced supply chain.

Investor View: Tariffs are a contained but persistent risk, to be monitored for escalation into 2026 guidance.

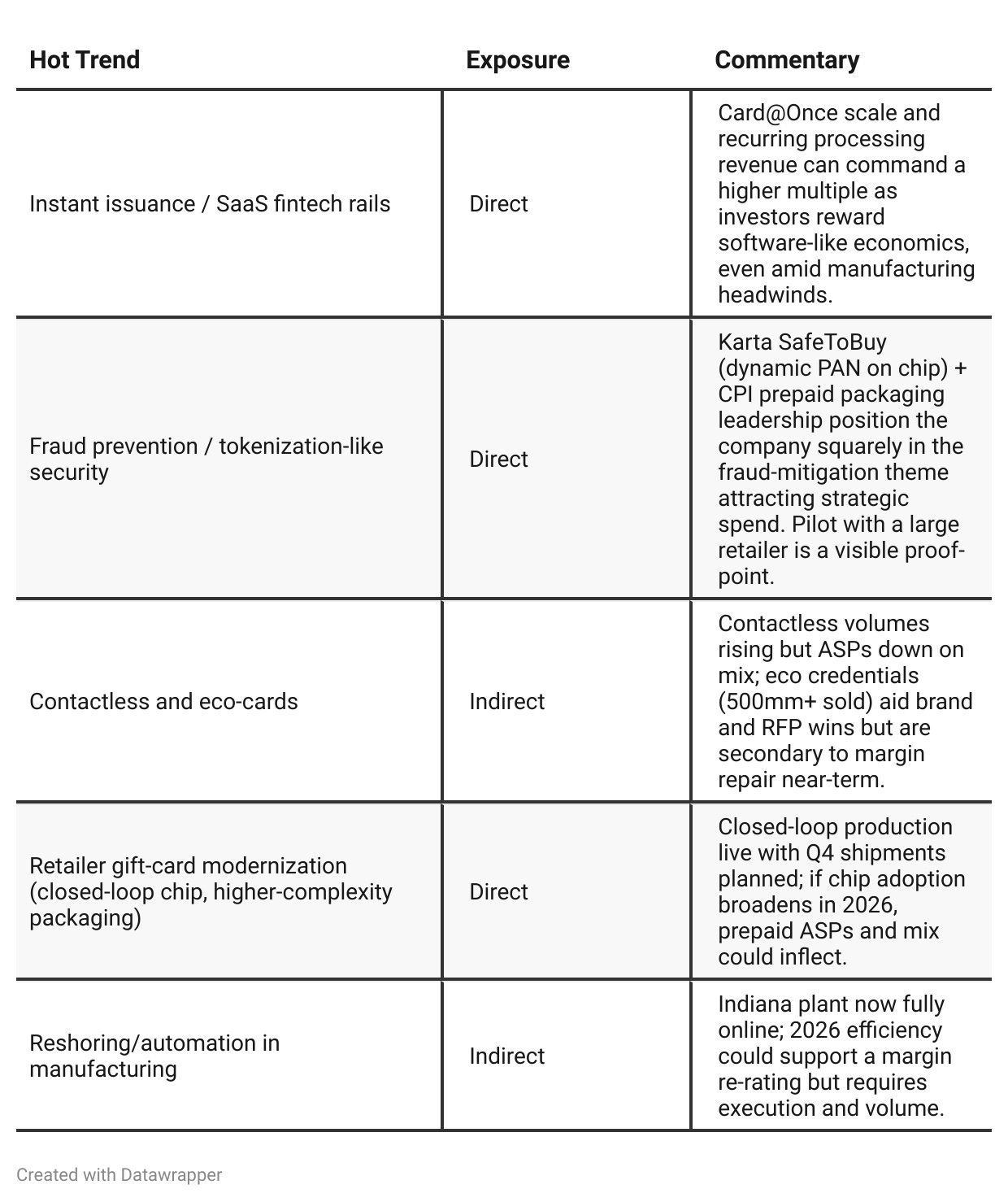

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025 – Expansion & Integration Phase:

CPI Card Group was celebrating growth momentum — strong double-digit sales, integration of the ArrowEye acquisition, new markets (government, healthcare, metal cards), and investments in the Indiana facility. The tone was energetic and confident, though somewhat defensive on tariffs and accounting changes. The company positioned itself as an expanding player diversifying across verticals.Q3 2025 – Transition & Strategic Execution Phase:

By Q3, the tone shifts to disciplined execution and digital leverage. The company highlights the operational completion of major investments and begins showing tangible progress — a fully functional Indiana facility, the CARTA partnership, and closed-loop prepaid rollout. Management acknowledges margin and cost headwinds, showing a more mature, realistic, and data-driven communication style.The narrative evolves from “We’re investing for growth” → “We’re executing, managing costs, and preparing for digital-led profitability.”

Year-over-year comparison

Q3 2024 – Momentum & Expansion

CPI presented itself as an innovative growth company, emphasizing rapid top-line expansion (+18%) and strategic diversification. Management’s messaging centered on winning share, launching eco-friendly products, and embracing new tech (antenna-integrated chips, RippleShot fraud tools). Tone was confident, buoyed by refinancing success and margin improvement.

Q3 2025 – Execution & Realignment

The story transitions toward execution discipline and risk management. Management acknowledges margin compression, tariff costs, and order timing delays, while pointing to 2026 efficiency recovery via the Indiana plant and digital expansion (CARTA partnership, closed-loop prepaid).

The tone is more grounded, data-driven, and long-term. CPI now positions itself not merely as a card manufacturer, but as a technology-enabled payment solutions provider.

Final Takeaway

CPI Card Group (PMTS) is in a strategic transition phase, shifting from manufacturing-heavy to tech-enabled, higher-margin digital solutions. Strong catalysts—instant issuance growth, prepaid chip rollout, and efficiency gains—provide a clear margin-recovery roadmap into 2026. However, investors should remain alert to tariff risks, margin compression, and high leverage.

Verdict: BUY, contingent on Q4 delivery and 2026 execution. Upside driven by prepaid digitization and cost efficiencies; downside from tariffs or delayed prepaid demand normalization.