CPI Card Group Inc. (NASDAQ: PMTS) – Q2 2025 Earnings

CPI Card Group Inc. (NASDAQ: PMTS) – Q2 2025 Earnings

Earnings Release Date: Aug. 8, 2025

Stock Price: $18.62

Market Cap: $210.3 million

Q2 2025 sales of $129.8 million vs $118.82 million in the prior year

Q2 2025 EPS of $0.04 vs $0.51 in the prior year

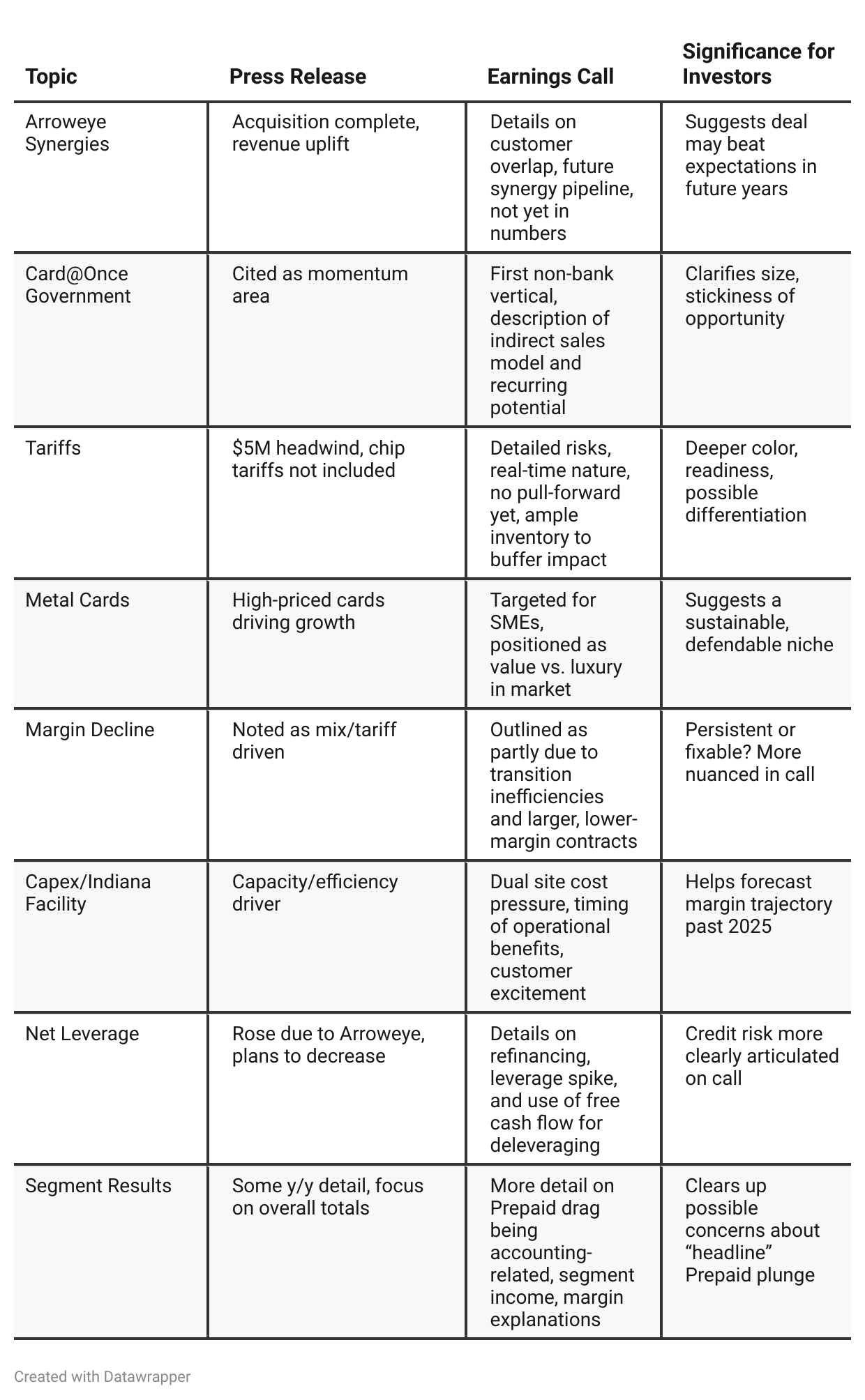

Press Release vs Call Transcript Comparison

Press Release is Marketing-Heavy: Focuses strongly on innovation, market expansion, environmental products, and positioning Arroweye as an unmitigated success.

Earnings Call is Operationally Detailed: Management sounds more cautious, drilling into real-time risks (tariffs, margin mix, dual facilities), and provides more clarity on timelines for improvement, synergy timing, and specific cost pressures.

Risk Communication Differs: Press release puts all major caveats in regulatory boilerplate; the call is much more specific about 2025 margin and leverage weaknesses, and the industry-wide nature of key risks.

Segment Numbers Require Adjusted Reading: The "as reported" drop in Prepaid and GAAP net income y/y would look grim unless the full context is taken from the call (and tables)—showing these are largely non-cash and one-time effects.

Long-Term Growth Signals: Emerging verticals like government and healthcare, new product lines (metal, digital), and cross-selling into Arroweye’s customer base are discussed more explicitly as growth runways in the call.

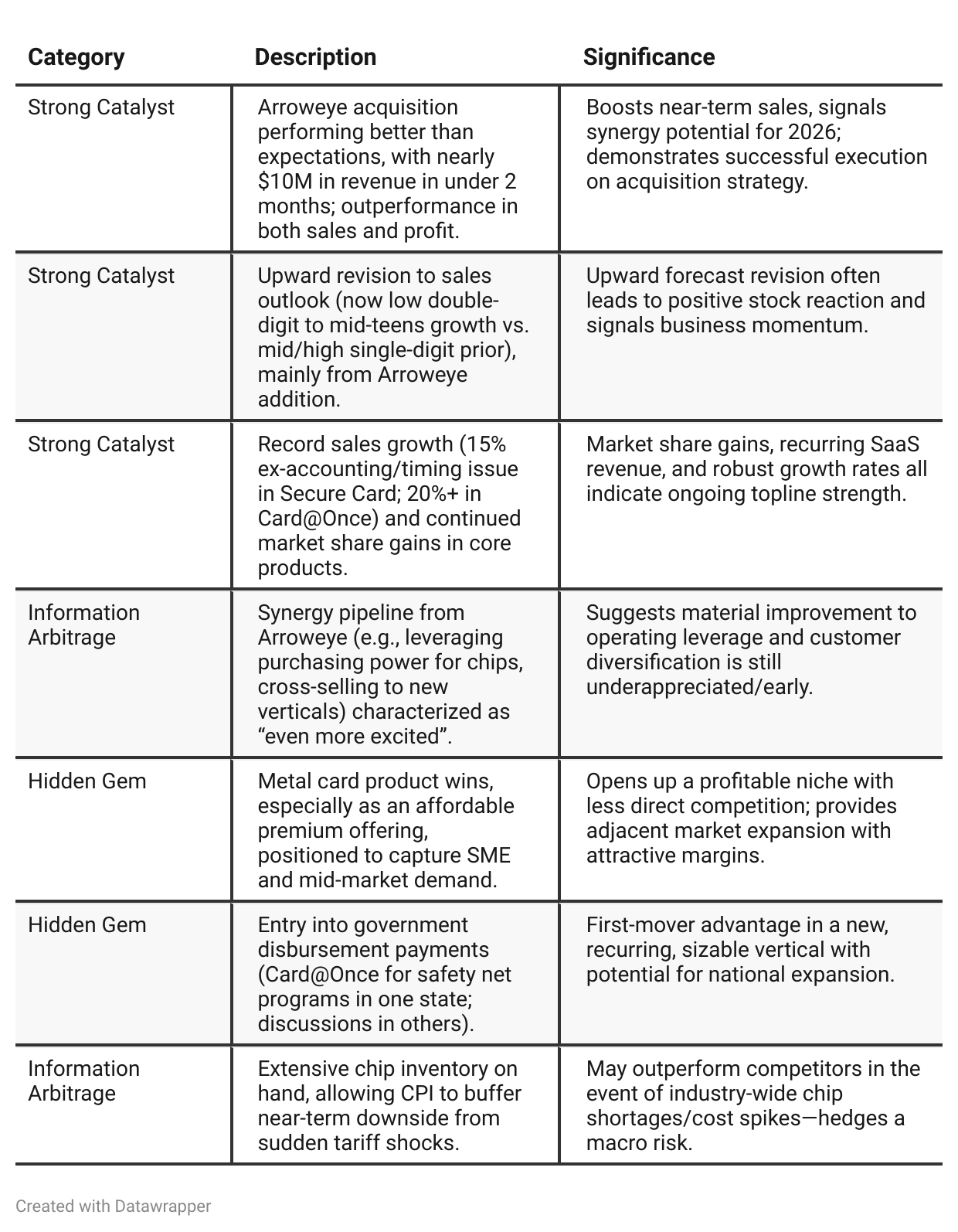

Positive Insights

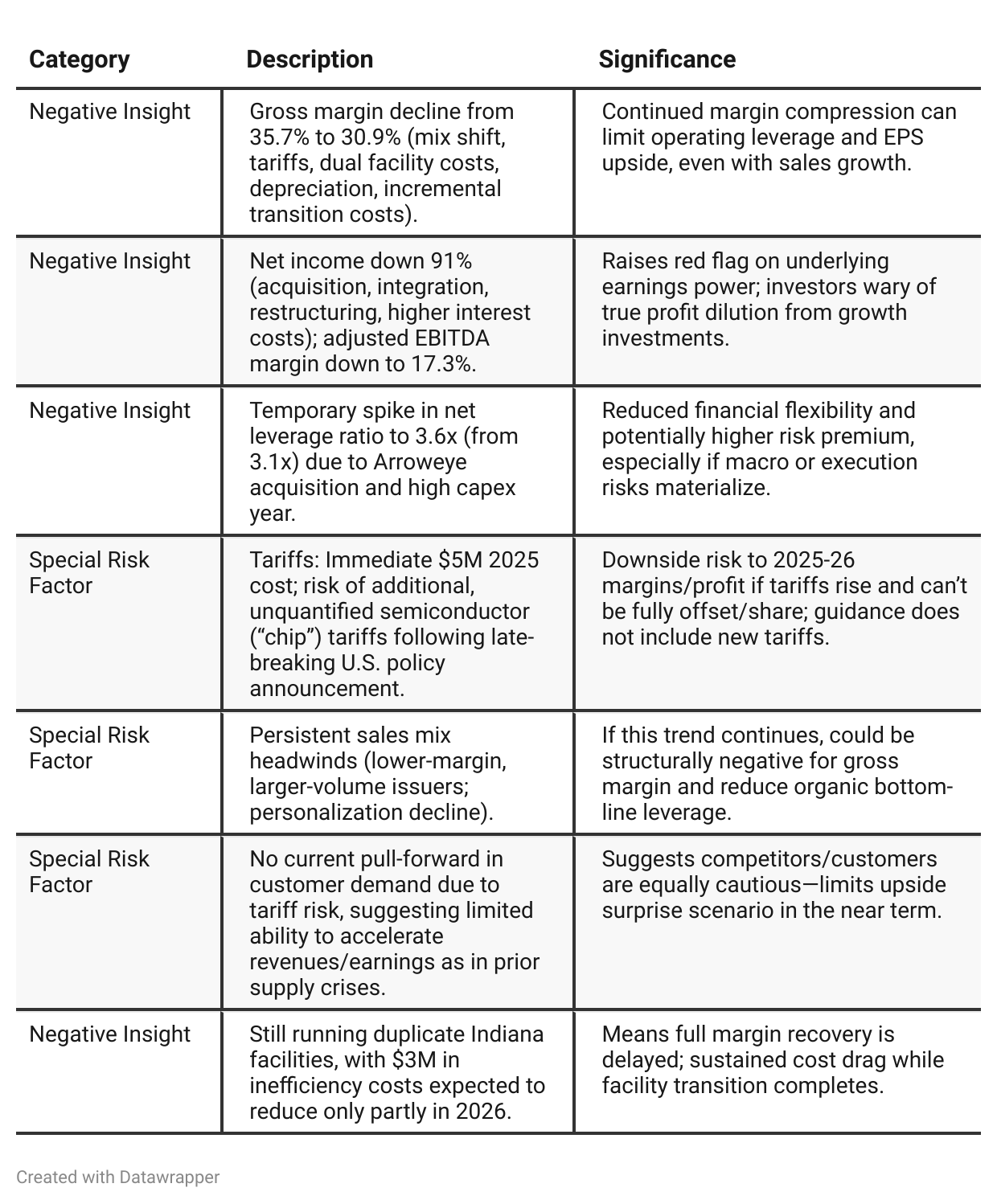

Negative Insights

Tariff Risk

Current Impact: Tariffs are a $5M headwind in 2025 and have contributed to margin pressure, already factored into guidance.

New Risks: Proposed chip tariffs could create further downside, but the exact impact is unknown and not in current guidance.

Mitigation: CPI has built ample chip inventory (buffering near-term risk) and is leveraging supplier relationships and customer partnerships to offset some costs.

Industry Context: Any major tariff effects would hit the whole sector, but CPI’s inventory provides short-term protection.

Watch Points: If new tariffs are implemented and can’t be offset or passed through, margin and profit recovery could be delayed.

Sentiment Analysis

The overall sentiment toward PMTS is bearish. While there are isolated bullish notes such as a chairman stock purchase and some positive technical trades, the majority of expressed sentiment reflects concern over sharp stock declines, warnings about risk (“RUG vibes”), and regrets from fundholders. Analyst price target cuts due to tariff impacts and integration costs, along with skepticism about stability and safety, reinforce a prevailing caution and negativity in investor sentiment despite a few optimistic voices.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q1 2025 set the stage with prudent optimism, highlighting strong sales, the Arroweye acquisition as a transformative step into broader markets, and caution over margin headwinds, tariffs, and integration costs. Strategy was consistent: invest for long-term growth, diversify products/customers, and control costs.Q2 2025 tells a more dynamic story: Arroweye is already outperforming on both revenue and synergies, driving an upward revision to revenue guidance. At the same time, the narrative pivots from one of integration to acceleration, with notable growth in new verticals and niche products (e.g., metal cards, government). However, cost headwinds—especially from rising tariffs and facility transition inefficiencies—have intensified and are now at the forefront of discussion, alongside frank acknowledgment of near-term margin and profit challenges. The company’s message has moved from establishing a platform for future growth to managing success amid external and internal cost turbulence. The balance of opportunity and risk is more pronounced, but the confidence in long-term positioning is stronger.

Year-over-year comparison

Q2 2024 was about re-establishing stability and setting the groundwork for future growth, with careful optimism rooted in recovering markets and successful core execution. The company focused on product and customer innovation within its traditional card business, was managing through a CEO transition, and had begun to dip its toes into adjacencies like healthcare and digital cards—while cautioning these would take time to become material.

By Q2 2025, CPI Card Group’s story has evolved into one of aggressive execution on transformation: the Arroweye acquisition has turbocharged both financials and customer diversification faster than anticipated, new product lines like metal cards and government disbursement solutions are gaining traction, and forward guidance reflects this new momentum. However, the company is now also contending with real and rising cost headwinds, both internal (integration/transition expenses) and external (tariffs, new policy risks), forcing a franker dialogue about margin pressures and the need for future operational efficiency.

Final Takeaway

CPI Card Group is navigating a growth and integration phase, successfully executing on key acquisitions and expanding into new verticals like digital, government, and healthcare payments. However, operational headwinds—most notably from sustained margin pressure, transitional costs, elevated leverage, and rising tariff uncertainty—act as a near-term ceiling on valuation and earnings momentum. Progress on operating efficiency, clear evidence of Arroweye synergy realization, and cost mitigation will be pivotal for upside. Verdict: Hold, pending better clarity on margins and risk management.