Nine Energy Service, Inc. (NYSE: NINE) – Q3 2025 Earnings

Nine Energy Service, Inc. (NYSE: NINE) – Q3 2025 Earnings

Earnings Release Date: Oct. 30, 2025

Stock Price: $0.72

Market Cap: $29.6 million

Q3 2025 sales of $132.0 million vs $138.2 million in the prior year

Q3 2025 EPS of ($0.35) vs ($0.26) in the prior year

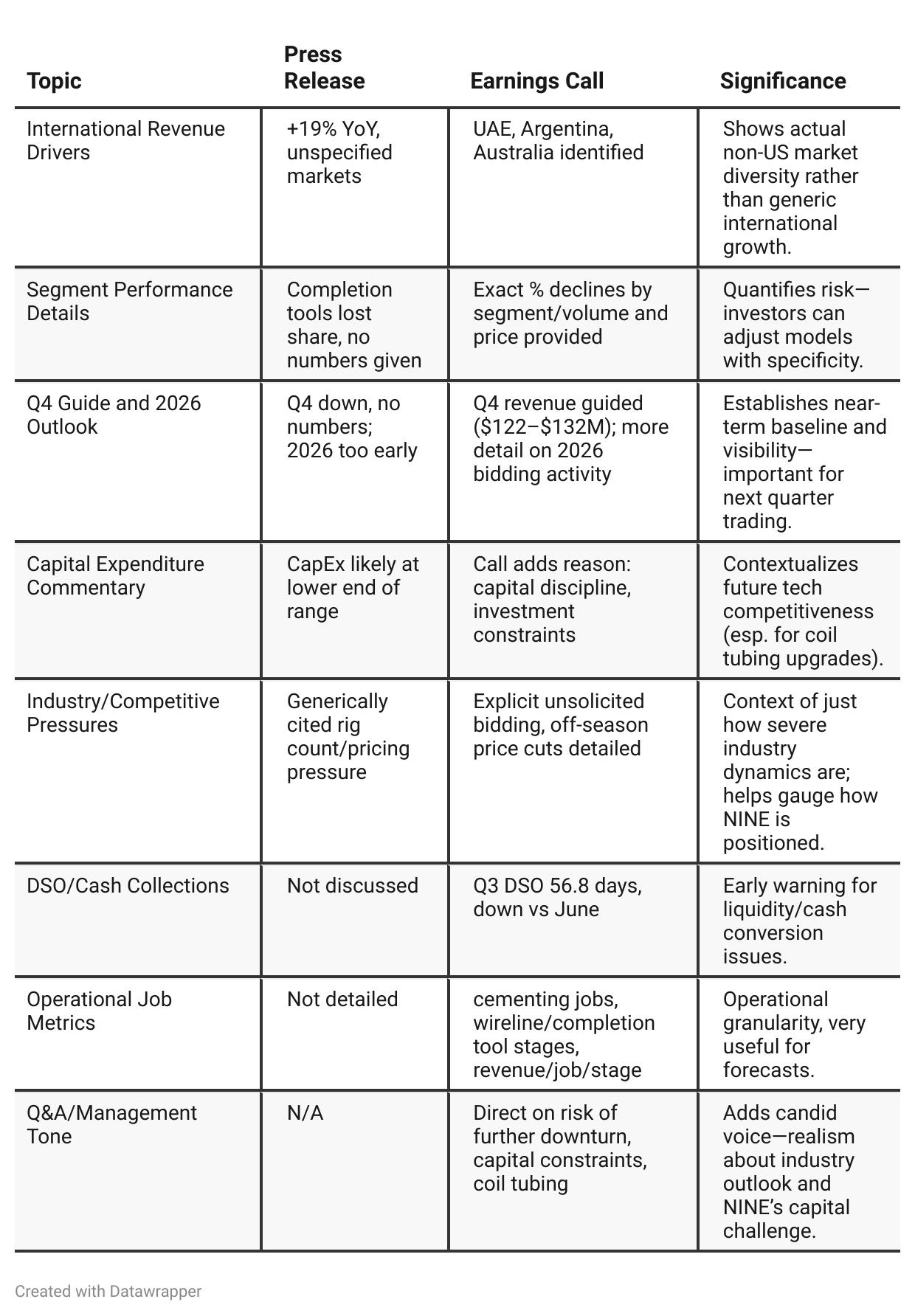

Press Release vs Call Transcript Comparison

Liquidity: Both documents flag risk, but only the call explains the magnitude/timing of borrowing reductions. Future asset sales or equity raise risk increases.

Earnings Visibility: The call clarifies that low-to-no visibility exists for 2026, so investors should use caution beyond Q4.

Operational Excellence: Landmark cement job in Haynesville is stressed in both, but call provides more technical details. For investors, this suggests technical leadership but is likely not enough to overcome broad sector headwinds without market recovery.

Growth levers: International segment is the only real growth engine, offsetting steep declines domestically. Attention should be paid to those geographies and sector spending plans.

Capex Constraints: The call is more explicit about how underinvestment may cause not just industry tightness in the future, but disadvantage NINE if more advanced tools are needed and there’s no capital to deploy.

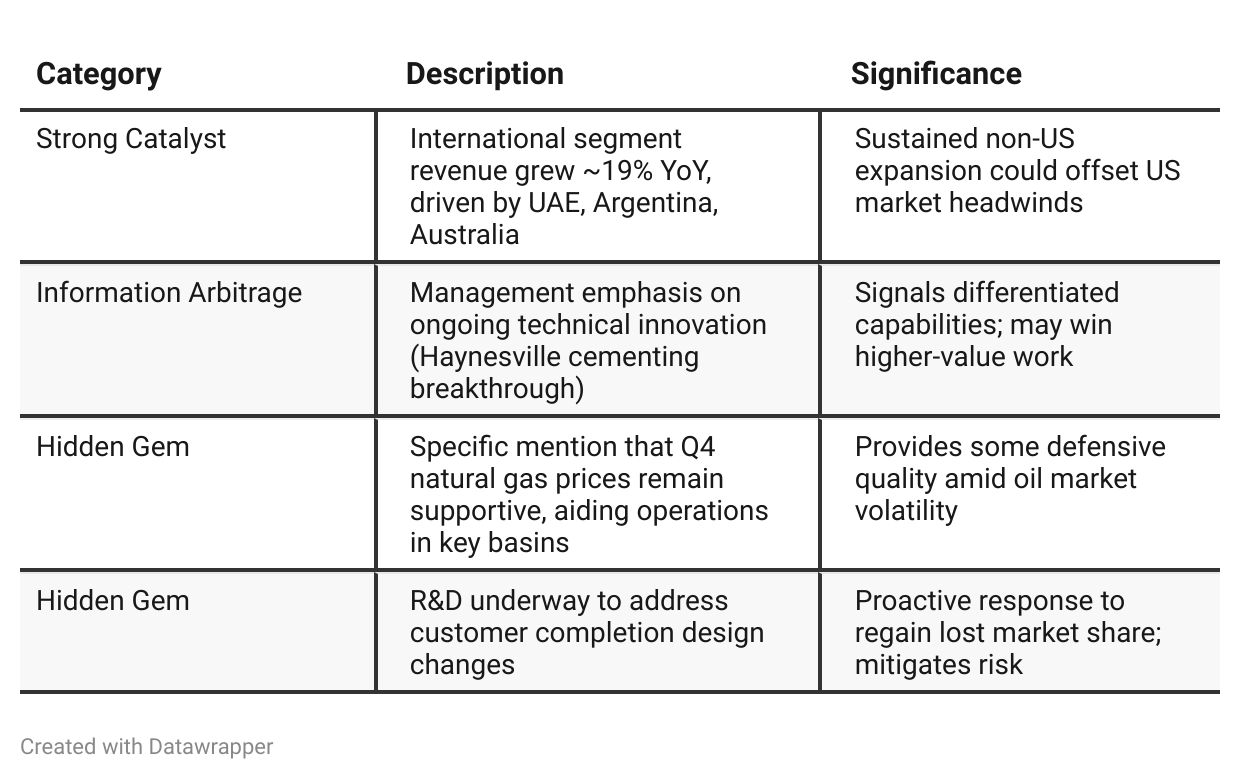

Positive Insights

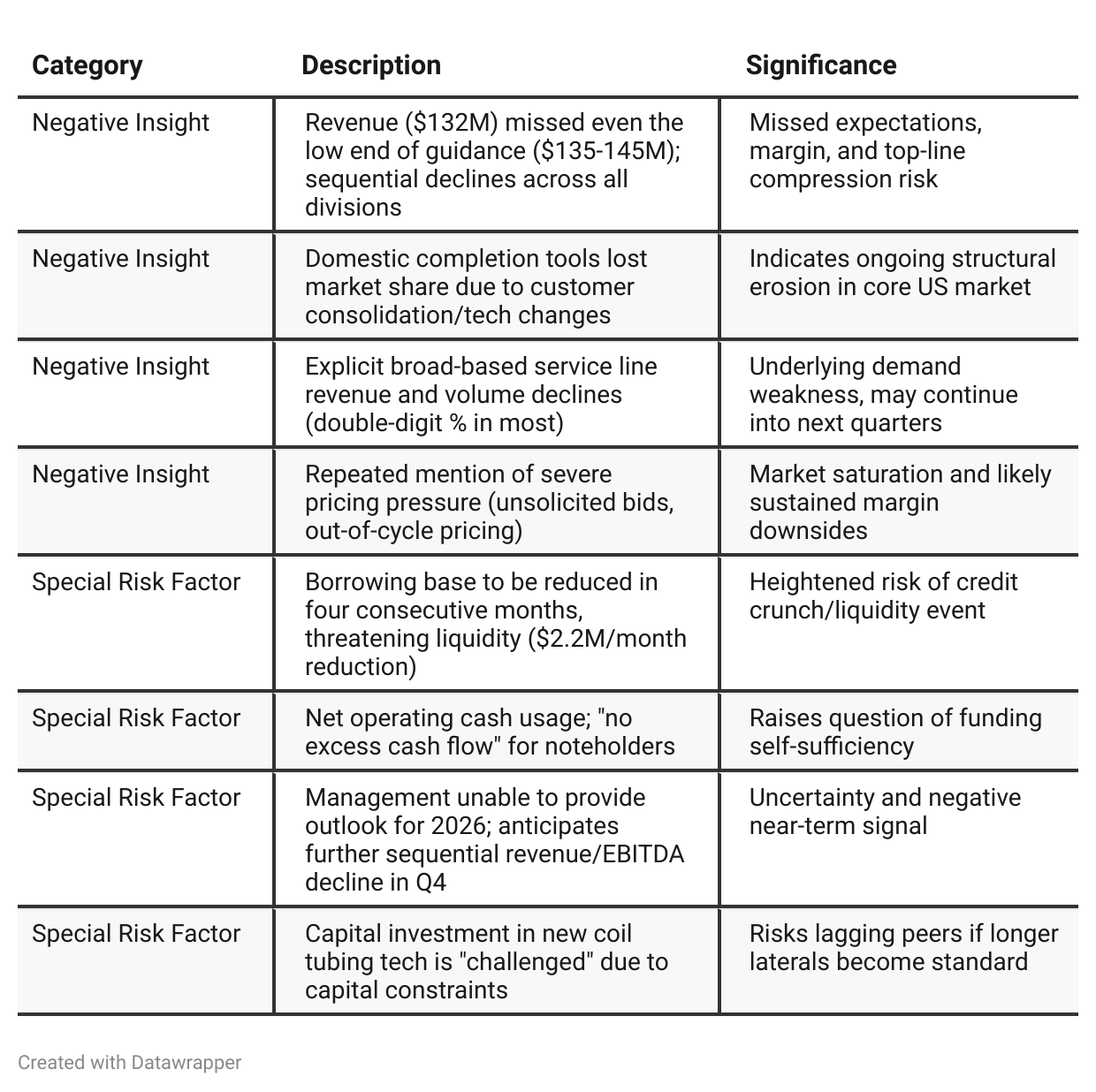

Negative Insights

Tariff Risk

Tariff Mentions/Impact:

Management specifically cited “announcement of tariffs” as a driver of Q2–Q3 pricing pressure, compounding rig declines and oil price volatility.

No explicit detail is provided on what tariffs, but context suggests US trade policy is causing higher costs or market disruption.

Impacts:

Cited as one contributing factor to lower demand and increased price competition.

May be affecting competitiveness and/or contract pricing in the Permian and other saturated basins.

Mitigation/Actions: No clear discussion in transcript of supply chain shifts, contract reworking, or price increases to offset the effect of tariffs.

Forward-Looking Statements: No projections, but inclusion in earnings rundown signals ongoing attentiveness and possible further downside if tariffs persist or widen.

Competitive Position: Implied loss of market share and/or inability to fully pass through costs.

Conclusion: Tariffs contributed to margin compression and amplified existing demand/pricing risk. Company responsiveness is so far passive—no distinctive mitigation strategy laid out. Unless supply/demand balances out or tariffs ease, this remains a structural hurdle to improved profitability.

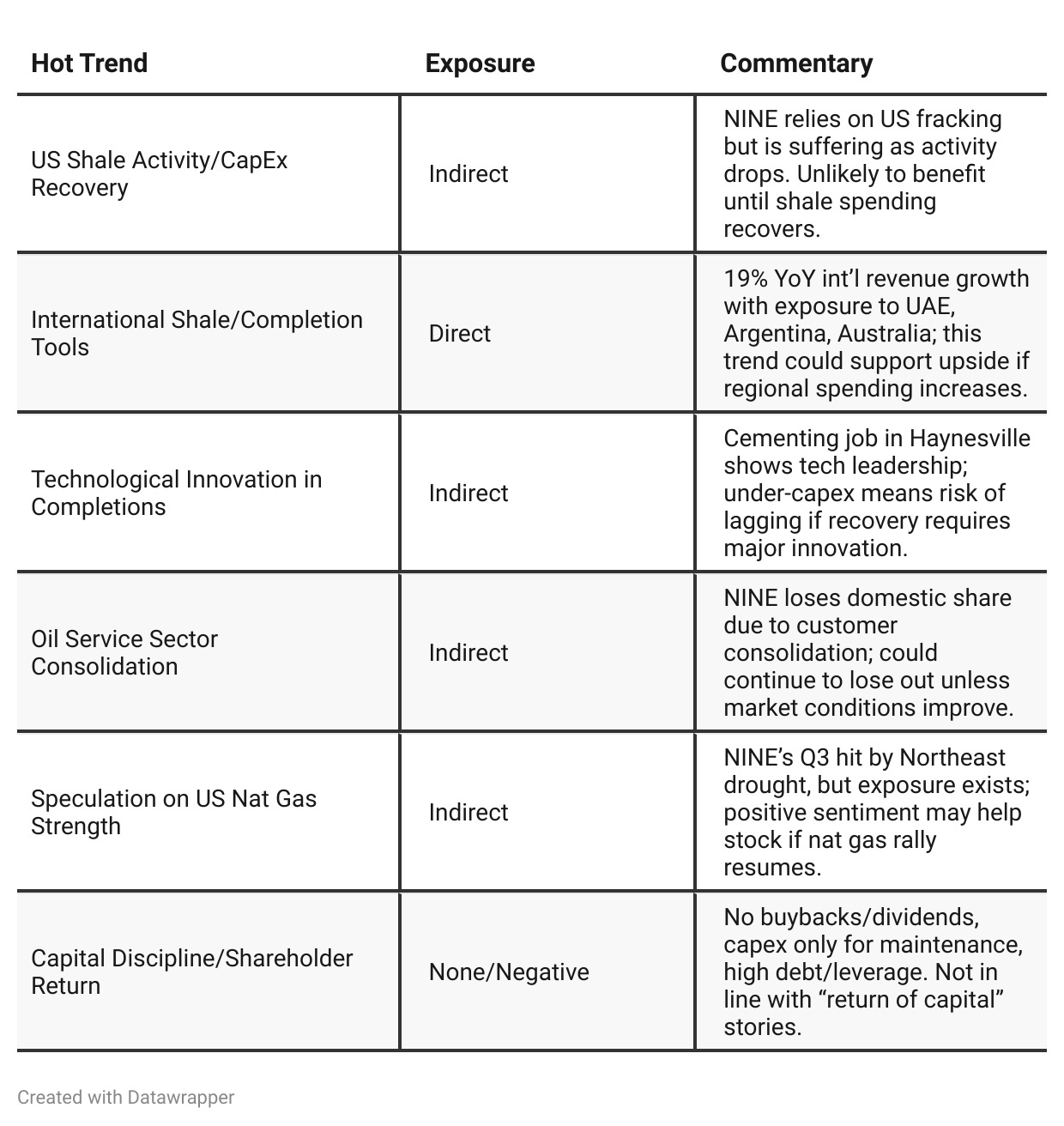

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025: Nine Energy maintained a cautious optimism, highlighting success in international tool sales, strong cost control, and the potential for incremental growth should activity rebound—especially in natural gas basins. The company played “offense and defense,” investing in capabilities and adapting to portend a more resilient, diversified business model even as the US market softened. Messaging included a notable forward focus (Q1 2026), new facility investments, and steady liquidity.Q3 2025: The tone shifted to realism and defense. Revenue missed already-reduced guidance, operating and cashflow metrics turned negative, and every product/service line declined sequentially—with no segment spared. Liquidity is now a risk, with detailed warnings about reduced borrowing base and no excess cash. The strategic narrative now emphasizes survival (cost control, immediate R&D pivots), dealing with unprecedented pricing and activity pressure, and a much shorter planning horizon. International growth remains a minor bright spot, but the overall message is one of bracing for continued turbulence with less certainty about timing or catalysts for a rebound.

Year-over-year comparison

Q3 2024: Nine Energy Service delivered a message of disciplined execution, proactive market share capture, aggressive cost reduction, and readiness for a cyclical upturn—demonstrated by outperformance on both growth and margin. The narrative focused on resilience, customer wins, and differentiated technology, with stable (but cautious) financial outlook and optimism for a modest pickup with improved commodity prices.

Q3 2025: The company’s tone shifted to defensive realism. Industry softness deepened and broadened, costing Nine both volume and share, compressing margins, and introducing increasingly acute pricing and liquidity risks. The company is now in crisis management mode—prioritizing cash preservation, urgent adaptation to new customer/market requirements, and capital constraint navigation, with innovation and international growth as faint bright spots. The upbeat, “primed for next up-cycle” narrative of 2024 has yielded to a focus on survival until industry conditions improve.

Final Takeaway

Nine Energy Service is in a clear defensive/restructuring phase, amid severe US market headwinds and deteriorating liquidity. While international growth and technical accomplishments are positives, the company faces substantial risk from sequential revenue drops, tightening access to capital, and industry-wide price wars. Near-term results are likely to remain challenged. Investors should monitor funding, liquidity moves, and successful execution of international expansion and tech development. Verdict: Hold—with high near-term risk, limited visibility, and potential for further downside unless sector or financial conditions improve.