Nine Energy Service, Inc. (NYSE: NINE) – Q2 2025 Earnings

Nine Energy Service, Inc. (NYSE: NINE) – Q2 2025 Earnings

Earnings Release Date: Aug. 5, 2025

Stock Price: $0.73

Market Cap: $29.7 million

Q2 2025 sales of $147.3 million vs $132.4 million in the prior year

Q2 2025 EPS of -$0.25 vs -$0.40 in the prior year

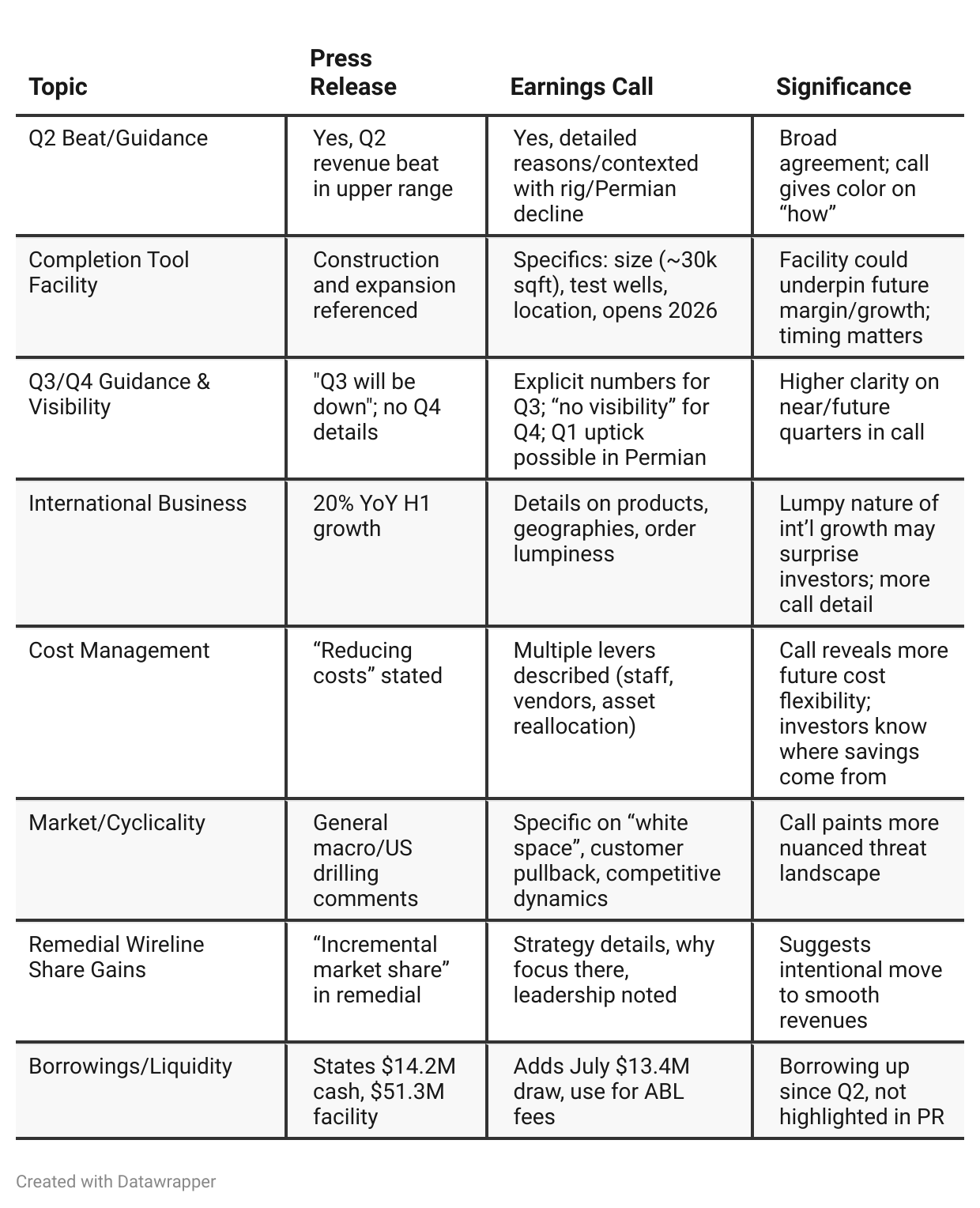

Press Release vs Call Transcript Comparison

Earnings call is more candid, forward-looking and operational. It provides greater transparency on internal measures, external risks, and the company’s narrative for cross-cycle performance.

International growth’s “lumpiness” may make quarter-to-quarter forecasting volatile—the call makes this clear, while the release simply touts growth.

Cost cutting details indicate management is tackling both fixed and variable costs. This gives investors pointers on how earnings might flex with revenue downside.

Timing and scale for new asset investments (like the Completion Tool facility) are better disclosed in the call; this helps investors factor in future growth or margin tailwinds.

Risks related to commodity prices, client behavior and macro play a more pronounced role in the call, impacting risk tolerance, valuation, and scenario modeling.

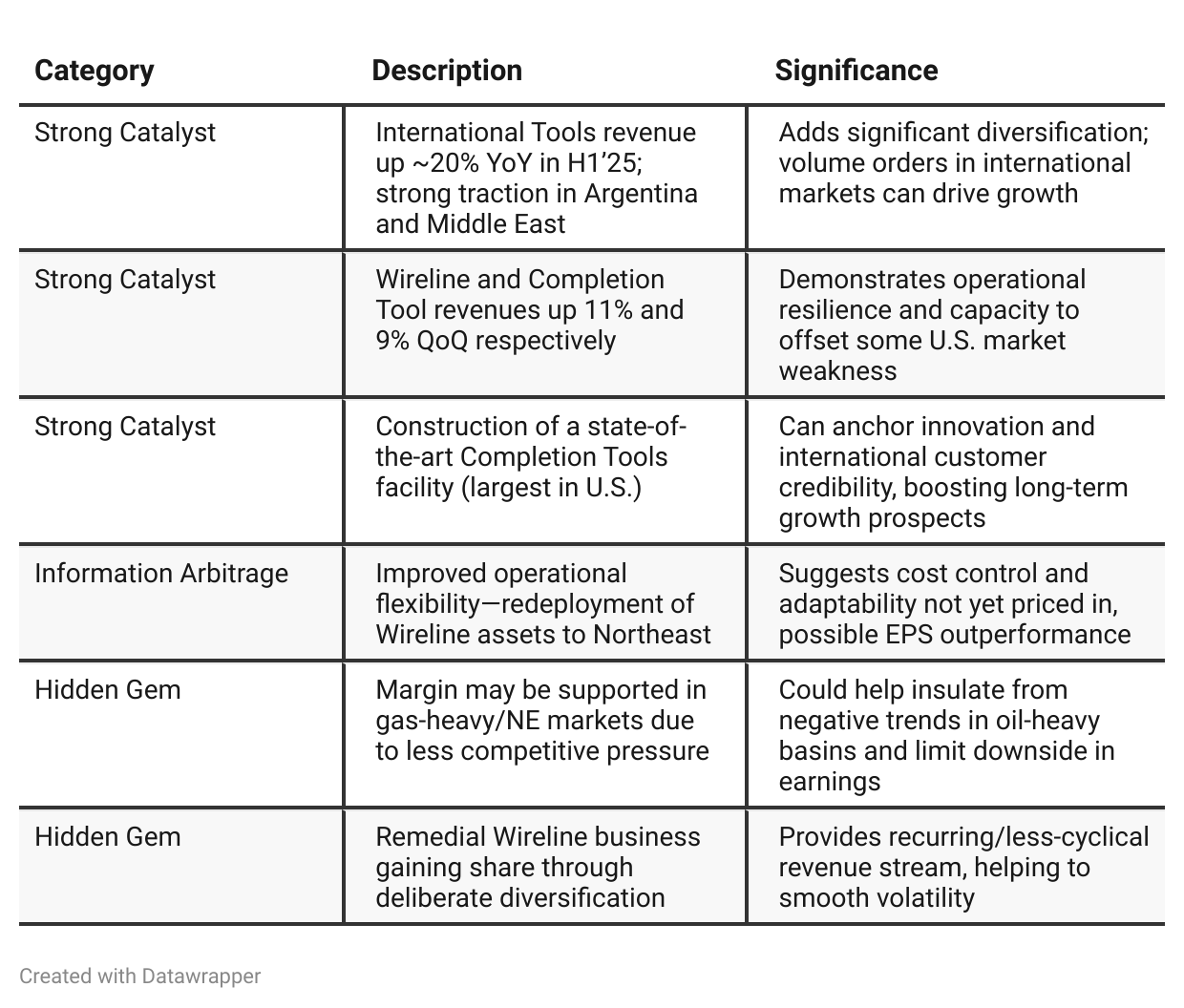

Positive Insights

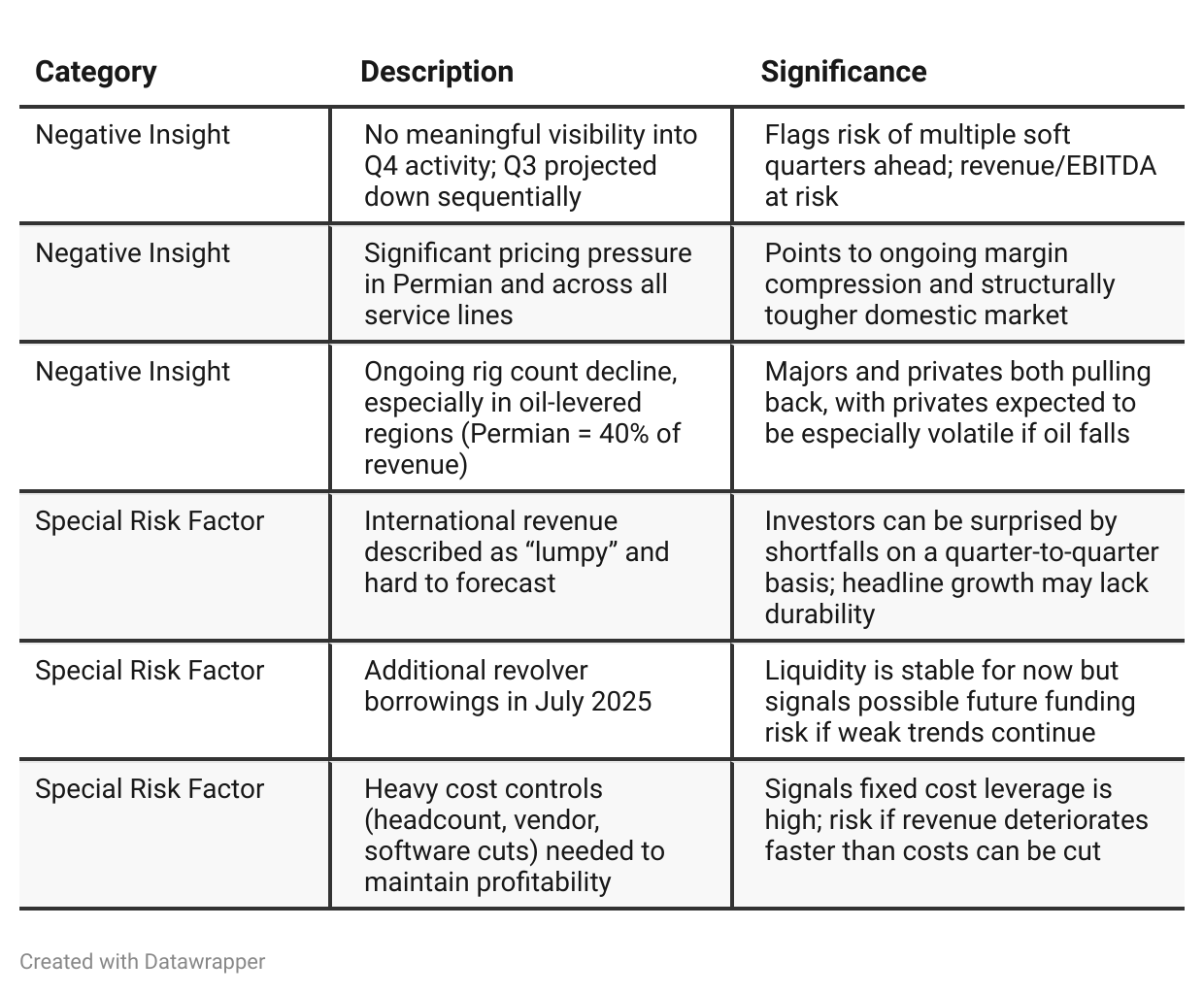

Negative Insights

Tariff Risk

Tariffs were cited as a direct factor in driving Q2 oil price declines and raising cost structure.

“In April, following the announcement of new tariffs, oil prices declined…”

“…the decline in commodity prices, increased costs due to tariffs…resulted in…activity and CapEx declines, significant rate declines.”

Actions Taken:

No explicit mention of sourcing changes, supply chain shifts, or contract negotiations to mitigate tariff impact.

Management describes cost-reduction broadly (vendors, fleet, personnel, consultants) but does not segment these out as tariff-specific mitigations.

Effects:

Margins are under pressure across service lines as both volume and price are squeezed.

U.S. activity and customer spending dampened due to compounded impact from tariffs and macro; this has a cascading effect given Nine’s exposure to Permian and oil-levered basins.

No mention of specific effect on market share or innovation, but cost management and international expansion implicitly provide partial offsets.

Forward-Looking:

Management warns of continuing effects if commodity prices or tariffs move further against them, particularly impacting private operator activity.

No quantified projections of tariff cost drag. No positive outlook or optimism related to tariff developments.

Sentiment Analysis

The overall sentiment classification is bullish. The comment highlights $NINE's notable activity as a USDUC deployer with a substantial figure mentioned, suggesting a positive view of the company's operational capabilities or recent performance.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

In Q1 2025, Nine Energy Service struck an optimistic tone, celebrating market share gains, growing service revenues, and new financial flexibility from a recent refinancing. Management saw opportunity in their technology portfolio, international ambitions, and diversification into natural gas markets, while acknowledging early signs of macro and tariff-related headwinds.By Q2 2025, the company’s narrative shifted notably—external pressures, especially a sharp rig count reduction in the U.S. and increased pricing competition, forced management’s focus to shift toward defending margins, managing asset utilization, and cost rationalization. While international growth and natural gas basin exposure offer bright spots, management is forthright about unpredictable international revenue, emerging “white space” (i.e., underutilization), and little short-term demand clarity. The story evolves from measured expansion and tactical offense to urgent defense and resilience amid contracting activity.

Year-over-year comparison

In Q2 2024, Nine Energy Service’s management struck a tone of “resilient optimism,” stressing their operational agility, niche strengths like refrac, and long-term tailwinds from U.S. gas demand—framing market difficulties as temporary, surmountable hurdles for a well-prepared management team.

By Q2 2025, the narrative has changed to a more sober and pragmatic one: while celebrating tactical wins (international growth, remedial wireline), management is more candid about the unpredictable landscape—a result of deeper rig declines, pricing pressures, and external shocks like tariffs. Strategic priorities have shifted decisively toward margin defense, cost discipline, and liquidity preservation, with less faith in a near-term recovery and more focus on nimble adaptation.

Final Takeaway

Nine Energy Service is in a profitability defense and selective growth phase, focusing on international expansion, gas basin resilience, and cost discipline. While international and remedial wireline traction are positives, structural risks from U.S. oil market softness, unpredictable international order flow, and liquidity demands remain. Execution on cost management, international pipeline, and demand visibility will be key. Verdict: Hold, with upside if international and gas-driven growth proves sustainable and downside if domestic or liquidity pressures worsen.