National CineMedia, Inc. (NASDAQ: NCMI) – Q3 2025 Earnings

National CineMedia, Inc. (NASDAQ: NCMI) – Q3 2025 Earnings

Earnings Release Date: Oct. 30, 2025

Stock Price: $4.14

Market Cap: $387.9 million

Q3 2025 sales of $63.4 million vs $62.4 million in the prior year

Q3 2025 EPS of $0.02 vs ($0.04) in the prior year

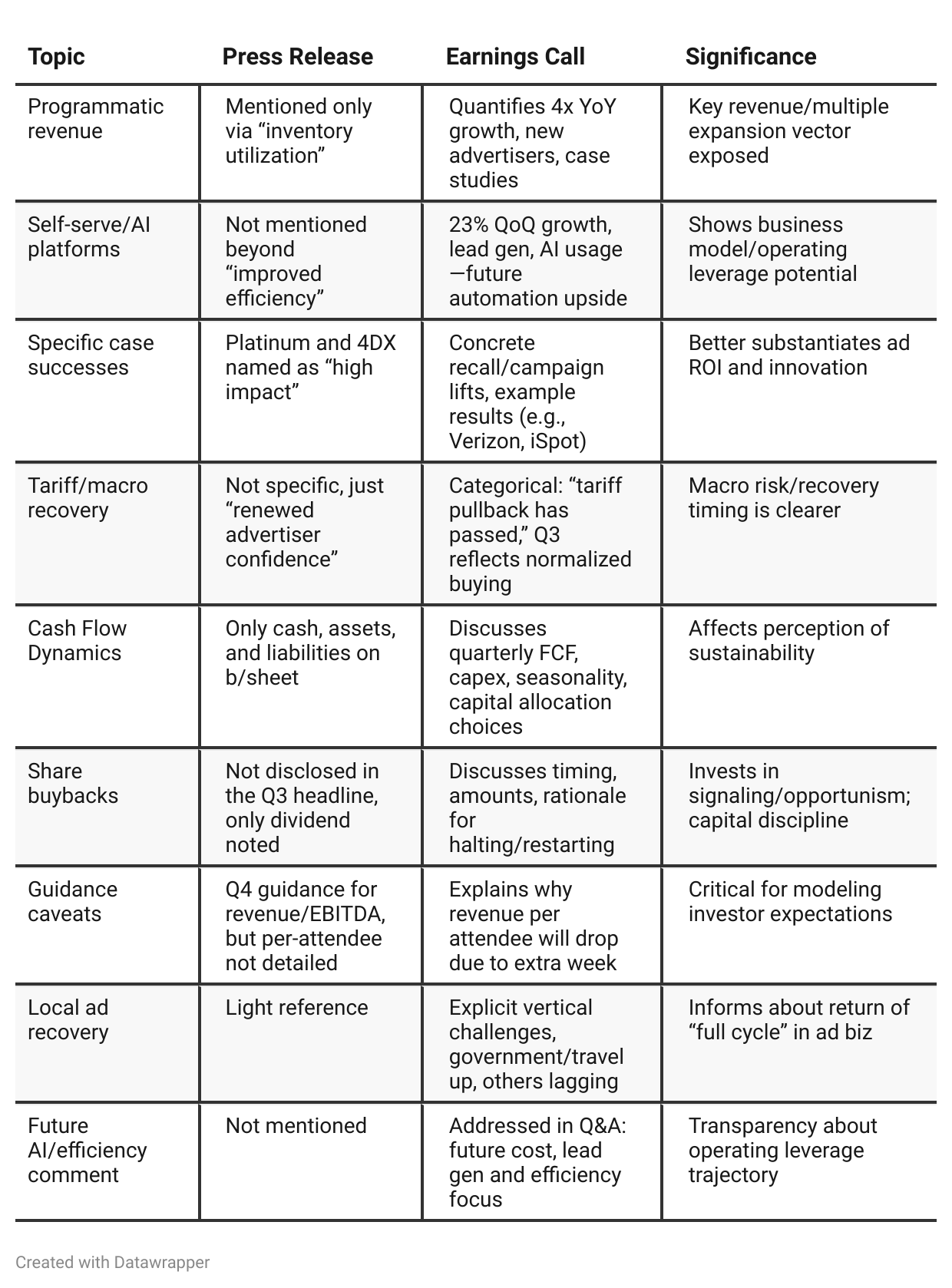

Press Release vs Call Transcript Comparison

The call presents a much more comprehensive bull case for technology/data adoption, platform reach, and new client entry—key for growth and re-rating narratives.

Both documents highlight improved utilization, but only the call breaks down channel/segment/technology drivers.

Buybacks, cash discipline, and capital allocation priorities are made much more explicit on the call—a positive for those watching for shareholder-aligned management.

Transparency about Q4 guidance drivers (revenue per attendee expectation down due to extra week) could prevent “model surprises” and supports management credibility.

Risk discussion is more nuanced in the call, with candid commentary on seasonal, macro, local category, and cash flow volatility.

Both indicate heavy reliance on blockbusters and tentpoles for Q4 optimism—seasonal risk remains.

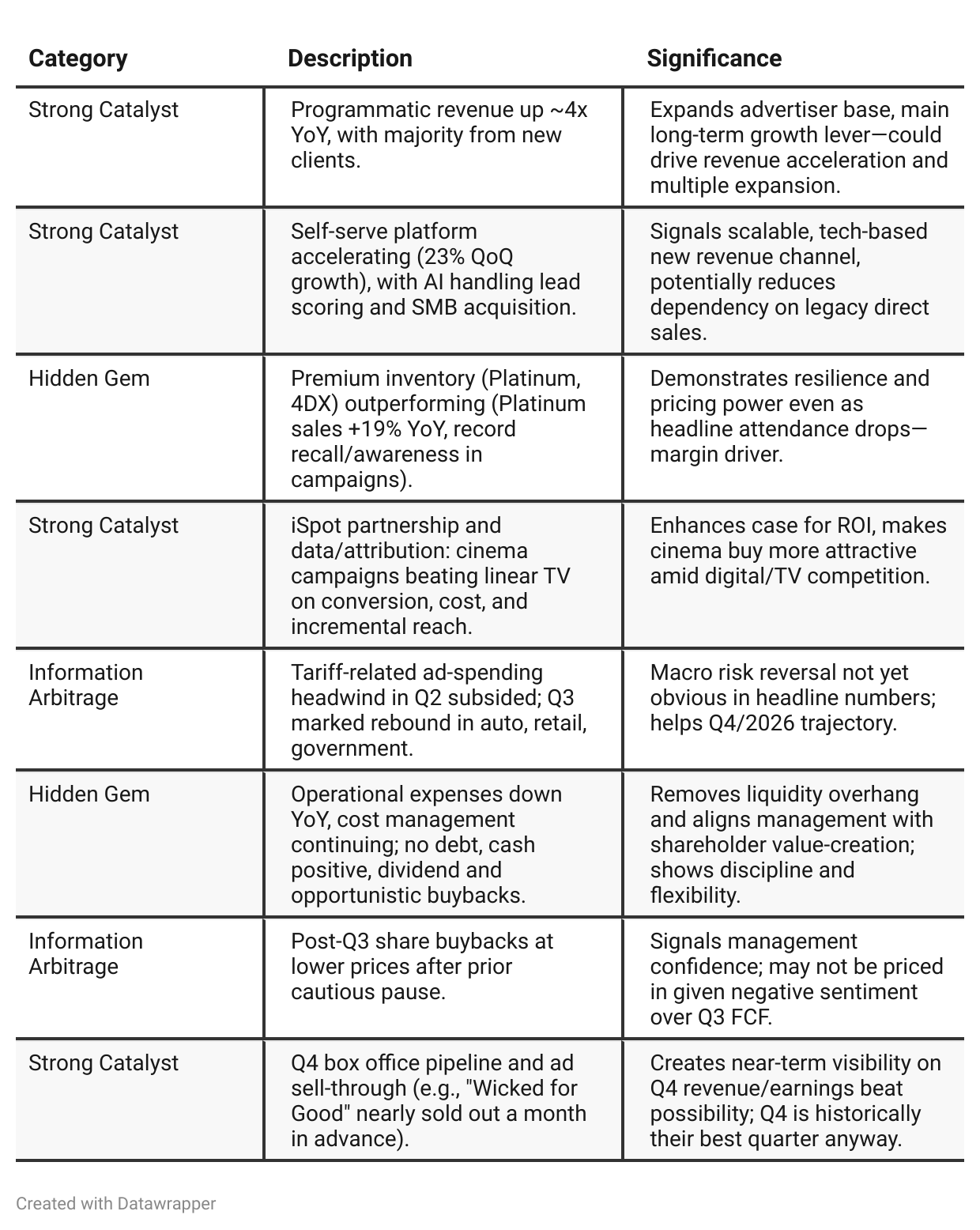

Positive Insights

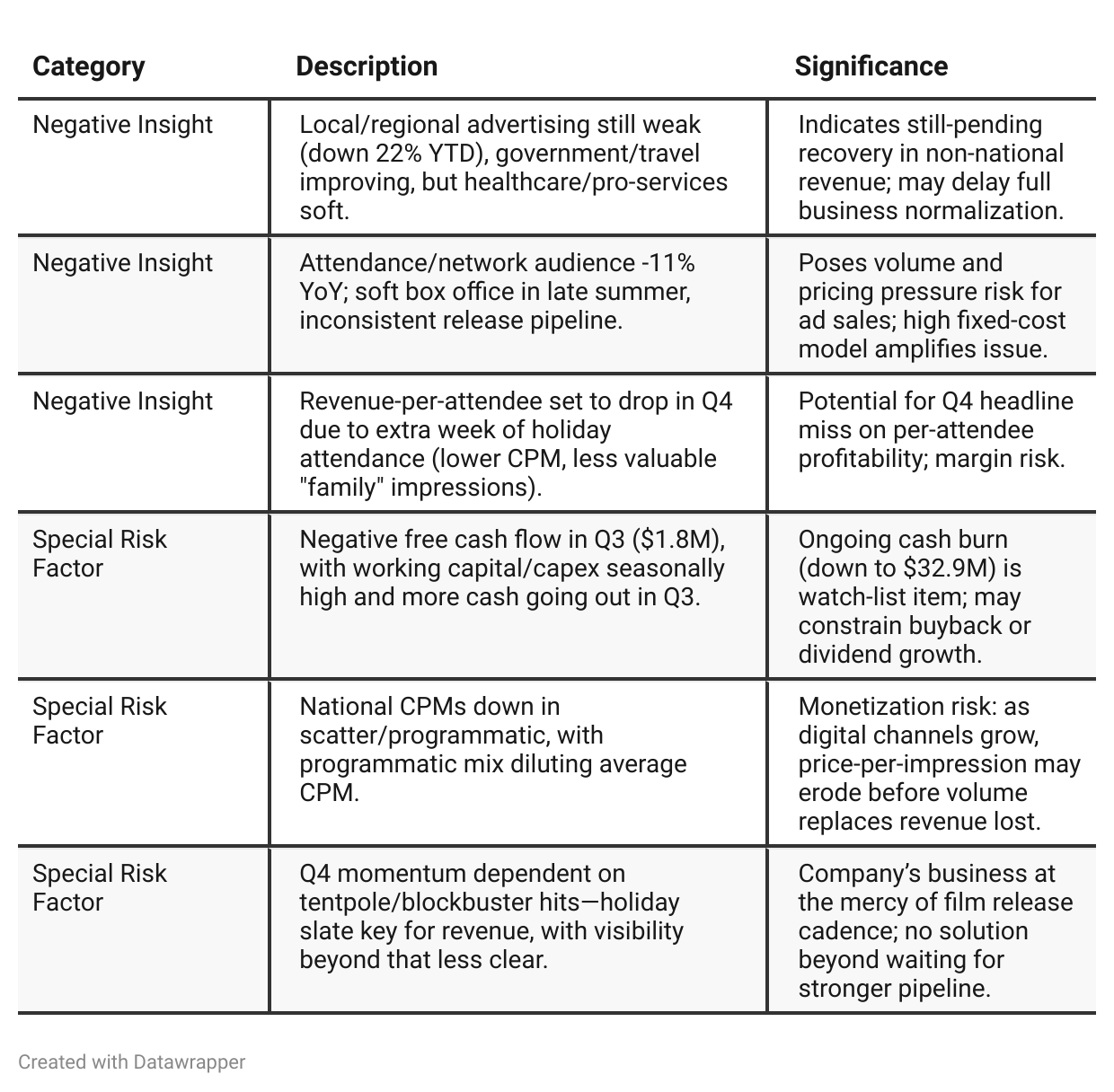

Negative Insights

Tariff Risk

Tariff Discussion: Call explicitly noted a “tariff-related pullback” earlier in the year, with Q3 seeing advertiser demand rebound as that uncertainty receded. Tariffs primarily affected Q2, impacting auto, retail, and other categories.

Company Response: No mention of supply chain changes or price renegotiations, as NCMI’s exposure is on the demand (advertiser) side, not physical goods/imports.

Forward Guidance/Projections: Management expects Q4 and 2026 momentum as macro and tariff policy uncertainty fades, with advertisers now “back.” No direct forecast of renewed tariff impacts, but the company implies current macro and tariff risks are low.

Competitive/Innovation: No evidence that tariffs affected market share or innovation.

Summary: Tariff effects were clearly a temporary headwind; resolution and stabilization are now a tailwind for ad demand in H2 and beyond.

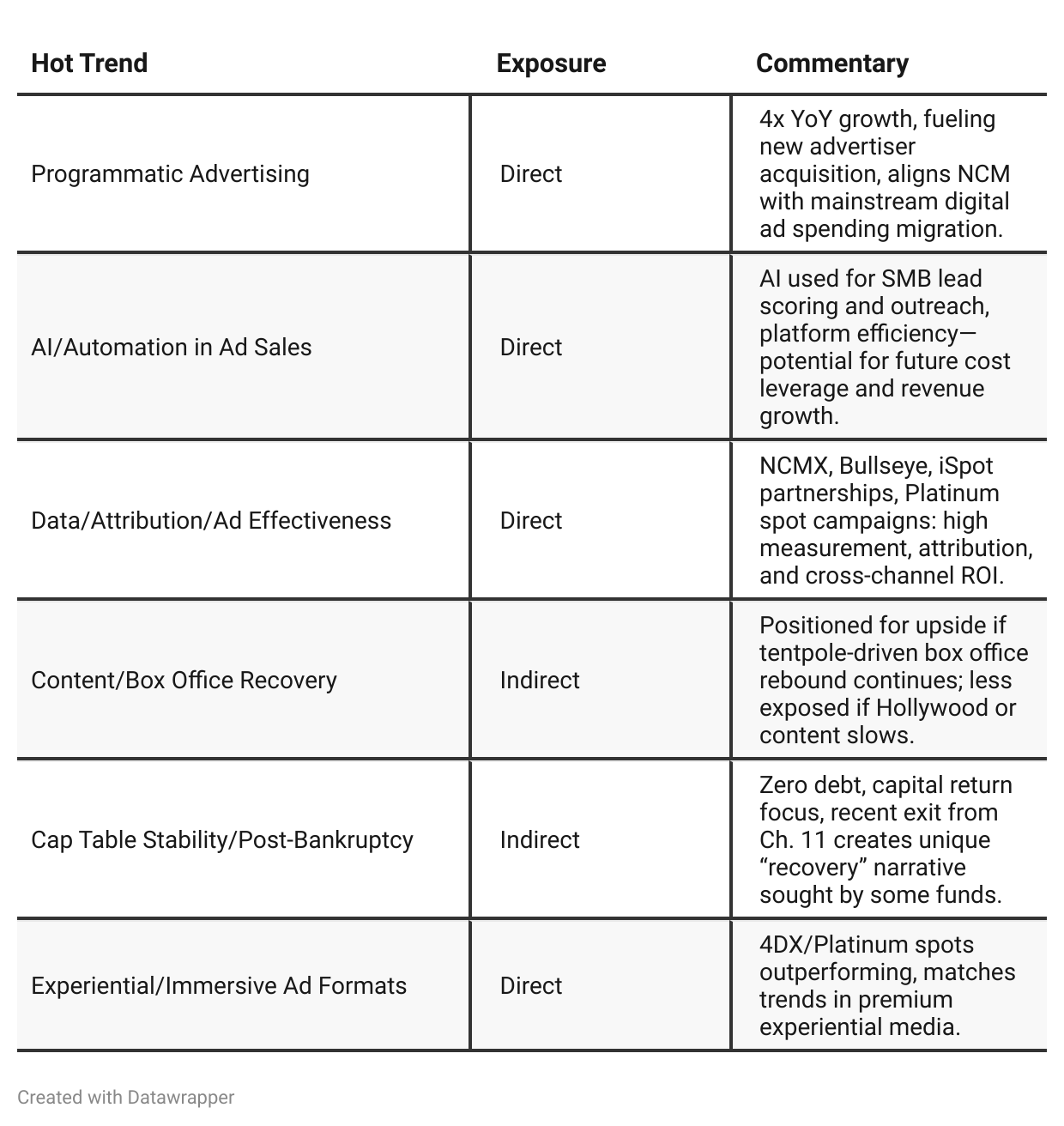

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025: NCMI’s call is characterized by realism and damage control. Management admits earnings “did not meet... expectation,” mainly blaming a sudden pullback in advertising due to tariffs and macro unease, which especially hit key categories (auto, government, CPG). There’s explanation on underwhelming attendance monetization despite box office hits, and on delays in spending for programmatic/sales transformation and tech investments. Emphasis is placed on future opportunity: the rebound is expected but not yet realized; optimism is tied to pipeline and recovery, not results.Q3 2025: Tone and content clearly transition to constructive—optimism is now underpinned by actual numbers: national ad revenue up, programmatic up ~4x, record recall in premium placements, AI/self-serve contributing to local expansion. Tariff and macro headwinds have dissipated, advertisers are back. Discussion moves from “fixing” to “delivering” (e.g., higher utilization, broadening client base, campaign effectiveness proof points). The company is explicit about near-term seasonal/operating margin risks (revenue per attendee dilution in Q4), driving management credibility and transparent guidance. Forward tone is “momentum,” “positioned for growth,” and “Q4/Q1 set up well,” conditioned on blockbuster slate sustaining audience and advertiser demand.

Year-over-year comparison

Q3 2024: NCMI was celebrating a surge in box office, youthful/demographically powerful audience draws, record Platinum sales, and a sense of sustained and broad-based cinematic resurgence. The story was about reaching younger viewers with unbeatable attention and measurement, with future growth expected from experiential content, digital innovations, and expanding advertiser categories. Caution was muted; the focus was on industry recovery and NCM’s strategic role within it.

Q3 2025: The narrative matured: NCMI acknowledges softness in attendance and continued local ad drag, but demonstrates that its digital strategy (i.e., programmatic, self-serve, AI CRM) is taking hold. Optimism is rooted in the company’s ability to offset box office volatility with operational levers—platform innovation, measurement partnerships, and direct client wins through digital. Messaging shifted from box office-driven tailwinds to performance-driven execution and monetization per attendee, with a transparent discussion of both opportunity and constraint (seasonality, Q4 mix, operating margin). The future story is now more data- and technology-driven, focused on diversifying demand, reducing cyclicality, and proactively managing capital.

Final Takeaway

National CineMedia (NCMI) is in a digital growth transition phase, pivoting to programmatic, self-serve, and data-driven ad solutions in response to industry headwinds from declining theater attendance and changing ad buyer habits. While premium inventory and digital innovation are yielding top-line momentum and expanding the client base, risks remain around margin dilution from digital mix, ongoing free cash outflows, local ad softness, and upcoming quarters’ dependence on tentpole-driven box office recovery. Execution on programmatic monetization and return to FCF generation are critical to unlocking further upside. Verdict: Hold—with upside if ad innovation and box office momentum prove sustainable.