National CineMedia, Inc. (NASDAQ: NCMI) – Q2 2025 Earnings

National CineMedia, Inc. (NASDAQ: NCMI) – Q2 2025 Earnings

Earnings Release Date: Aug. 5, 2025

Stock Price: $4.75

Market Cap: $446.4 million

Q2 2025 sales of $51.8 million vs $54.7 million in the prior year

Q2 2025 EPS of ($0.11) vs ($0.09) in the prior year

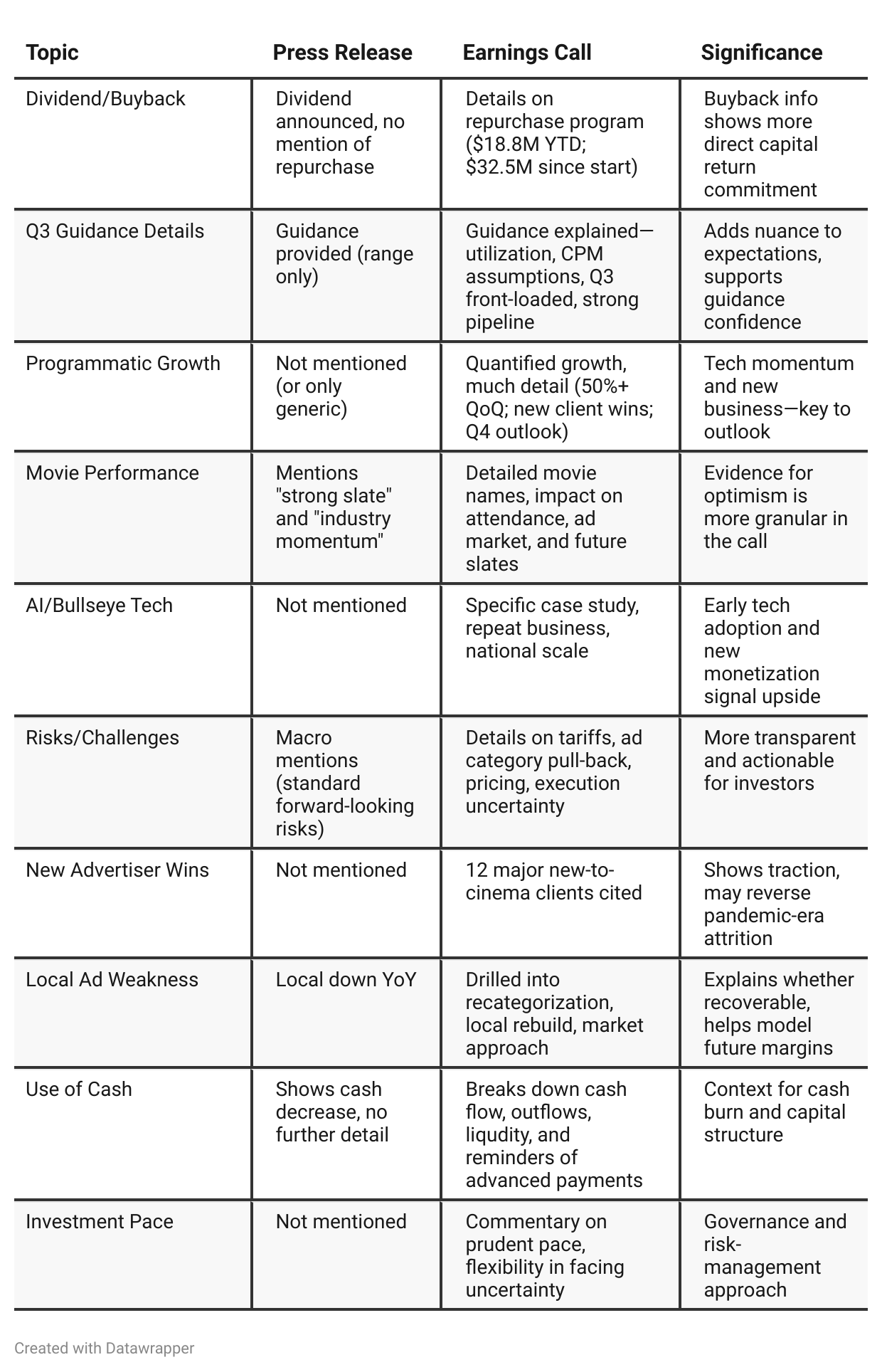

Press Release vs Call Transcript Comparison

Press Release Focuses on Optics: Shares headline challenges and optimism broadly, but lacks specificity on actions, real pain points, or execution details.

Earnings Call is More Nuanced: Provides rich context—challenges, competitive dynamics (CTV, programmatic shift, audience trends), as well as management’s agility in operating the business (investment timing, variable cost approach).

Investor Takeaways:

Growth will be uneven: High attendance is great, but monetization per attendee is challenged. Recovery depends both on box office and resilience in ad market pricing.

Tech adoption is vital: NCM needs programmatic penetration, local delivery, and data-driven targeting to win as media spend shifts.

Capital allocation remains a focus: Dividend and buyback discipline are positive, but need to be balanced against cash burn (esp. after a loss quarter).

Visibility and Forecasting at Risk: Upfront-to-scatter shift means the business will remain "lumpy." Guidance is useful, but volatility risk is real.

Execution and Communication: The willingness to pause/unpause investments and pivot strategy is good, but persistent uncertainty could frustrate long-term investors.

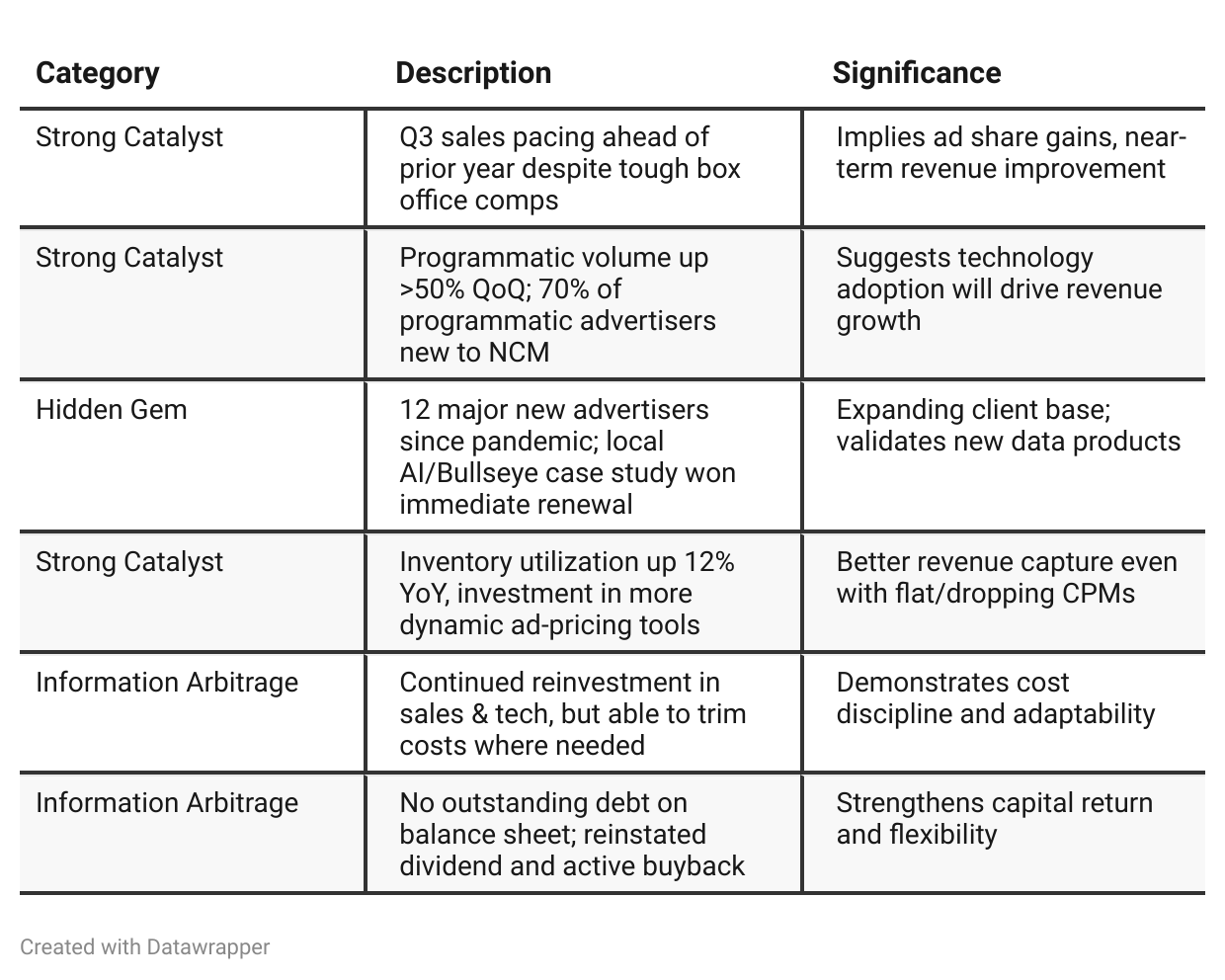

Positive Insights

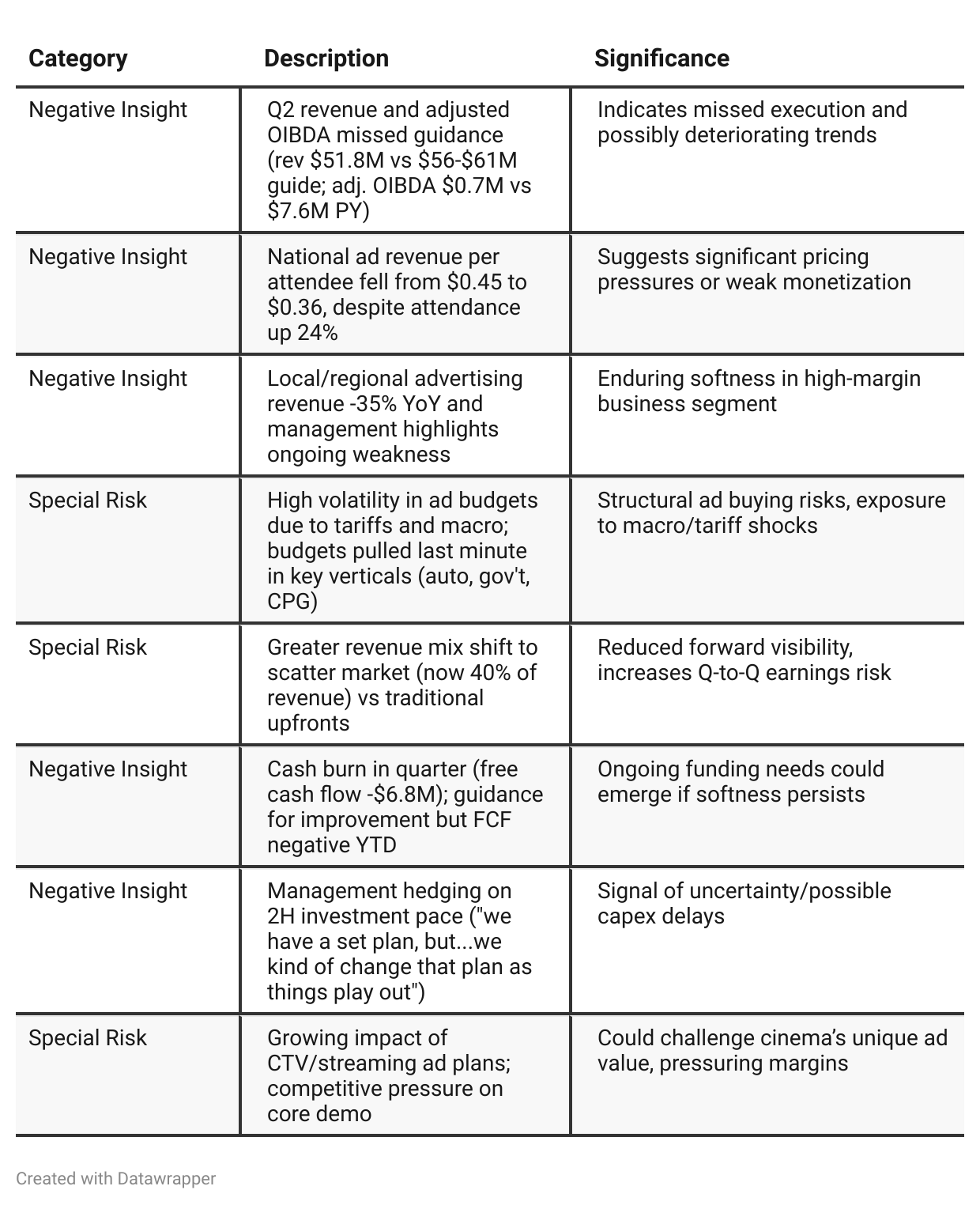

Negative Insights

Tariff Risk

Actions/Mitigation:

Company is moving toward more dynamic ad inventory/pricing and programmatic solutions to adapt to short-term market swings.

Continues to diversify by onboarding new programmatic and local advertisers, increasing platform resonance with performance buyers.

No mention of shifting contracts, renegotiating ad rates, or other drastic measures on pricing/supply chain addressed directly.

Forward-Looking:

Recovery in ad budgets in Q3 is dependent on tariffs and macro environment remaining stable; management explicitly says further major tariff developments could reverse the recent improvement.

Management is cautious in forecasting H2 and beyond, emphasizing that confidence is "barring any major tariff issues or economic ones related to the tariffs."

No explicit discussion of potential for passing cost increases onto customers or changing pricing strategies in response to tariffs.

Market Share/Competitive Impact:

No clear change in market share discussed, but company does highlight that advertisers came back strongly once tariff uncertainty receded.

There is no mention of supply chain disruption (as a service business), but the company’s end-market (advertisers in autos, CPG, government) remains highly sensitive to tariff-driven budget shifts.

Sentiment Analysis

Overall sentiment toward NCMI is bullish. The relevant commentary highlights positive factors such as the company’s leading market share, strong free cash flow conversion, exclusive long-term contracts, successful debt restructuring, and leverage to a rebounding box office environment. Investors also express personal interest in adding to their positions or already owning shares, signaling optimism about the stock’s prospects.

Previous Earnings Call

Quarter-over-quarter comparison

In Q1 2025, National CineMedia struck a confident tone, spotlighting strong industry partnerships, a deepening pipeline, and bold innovation in tech and data products—despite recognizing near-term weakness as transitory and emphasizing shareholder returns and the promise of upcoming blockbusters. By Q2 2025, the narrative had shifted toward pragmatic realism: management openly addressed a tougher macro and ad market environment, missed top- and bottom-line targets, and clearly articulated operational and monetization challenges. However, there was also evidence of tactical adaptation—leveraging programmatic and AI-led products, cost management, and flexible investment in response to evolving conditions. The story moved from long-term optimism and a “recovery is coming” mindset, to near-term humility, greater transparency, and a focus on demonstrating that the business can weather variability and capitalize quickly when market conditions improve.Year-over-year comparison

Q2 2024: National CineMedia tells a story of robust execution and resiliency—despite strike-related headwinds, it boasts superior monetization, strong advertiser demand, new platform innovations, and capital return acceleration. The tone is proud and future-oriented, leveraging both audience and technology edge.

Q2 2025: The company is more sober, openly confronting macro headwinds that pressure its business—even positive surprises at the box office aren’t fully translating into revenues due to pricing/ad demand softness. While the long-term strategy is intact—relentless innovation, tech/platform push, and capital returns—the focus right now is on adapting to volatility, shoring up local/regional advertising, and extracting every monetization lever available. Optimism remains, but it is cautious, pragmatic, and conditional on market normalization.

Final Takeaway

National CineMedia is in a stabilization and technological transition phase, focused on rebuilding momentum through programmatic ad expansion, new client wins, and an innovative local ad offering. Although positive H2 guidance and capital returns signal confidence, ongoing volatility in ad budgets, persistent pricing pressure, and local weakness mean a full recovery is not yet in hand. Execution on Q3/H2 revenue growth and monetization, alongside continued programmatic progress, will be critical. Verdict: HOLD, with the path to Buy dependent on confirmed improvement and better visibility.