Miller Industries, Inc. (NYSE: MLR) – Q3 2025 Earnings

Miller Industries, Inc. (NYSE: MLR) – Q3 2025 Earnings

Earnings Release Date: Nov. 05, 2025

Stock Price: $39.31

Market Cap: $449.9 million

Q3 2025 sales of $178.7 million vs $314.3 million in the prior year

Q3 2025 EPS of $0.27 vs $1.33 in the prior year

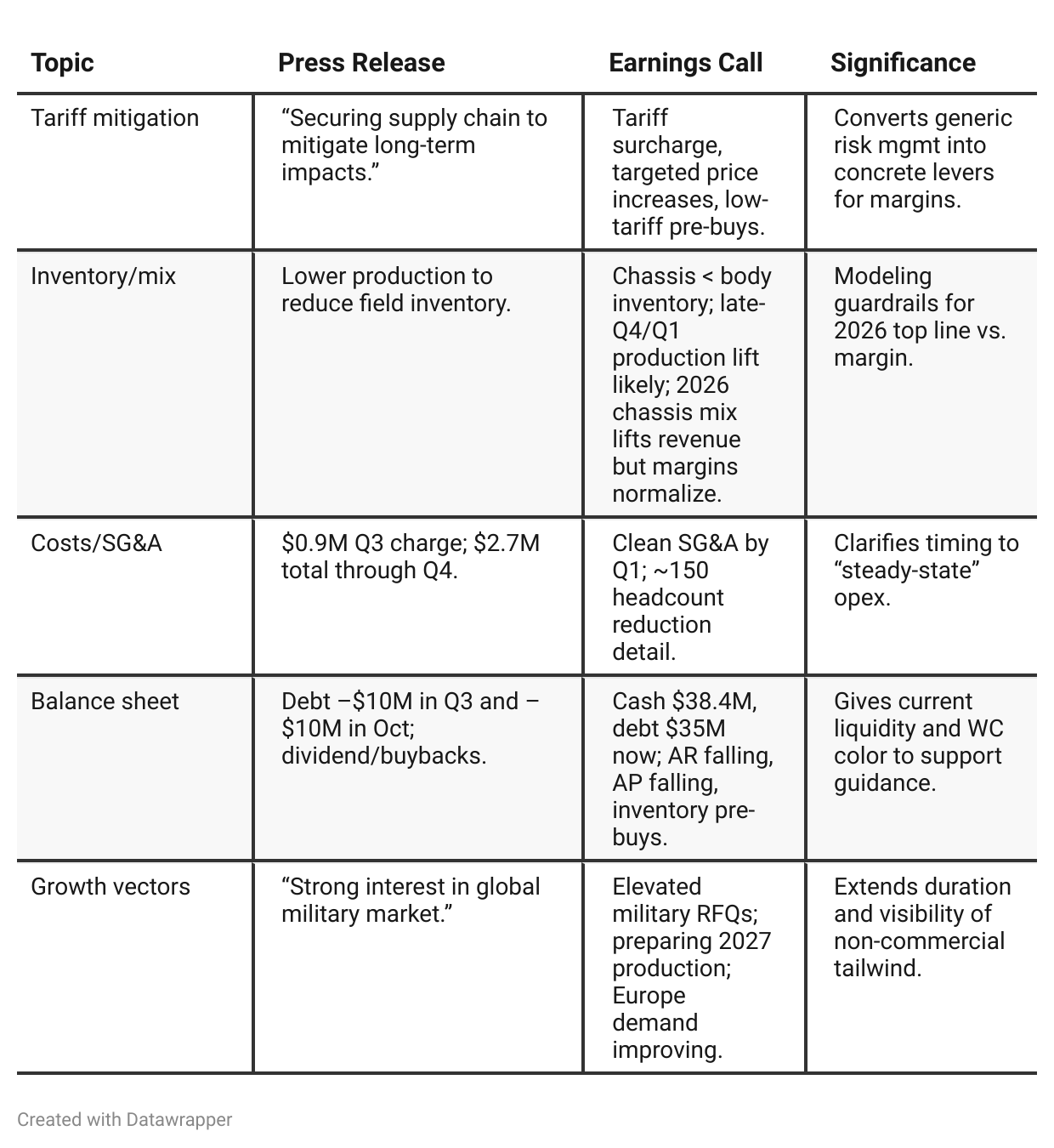

Press Release vs Call Transcript Comparison

Q4 seasonality explicitly quantified on the call (shortest quarter; plant maintenance/shutdowns), which helps explain potential sequential softness not obvious from the PR headline.

Distribution health datapoint: order entry still slightly below weekly retail; management wants those to align before increasing production—disciplined throttle, not volume at any cost.

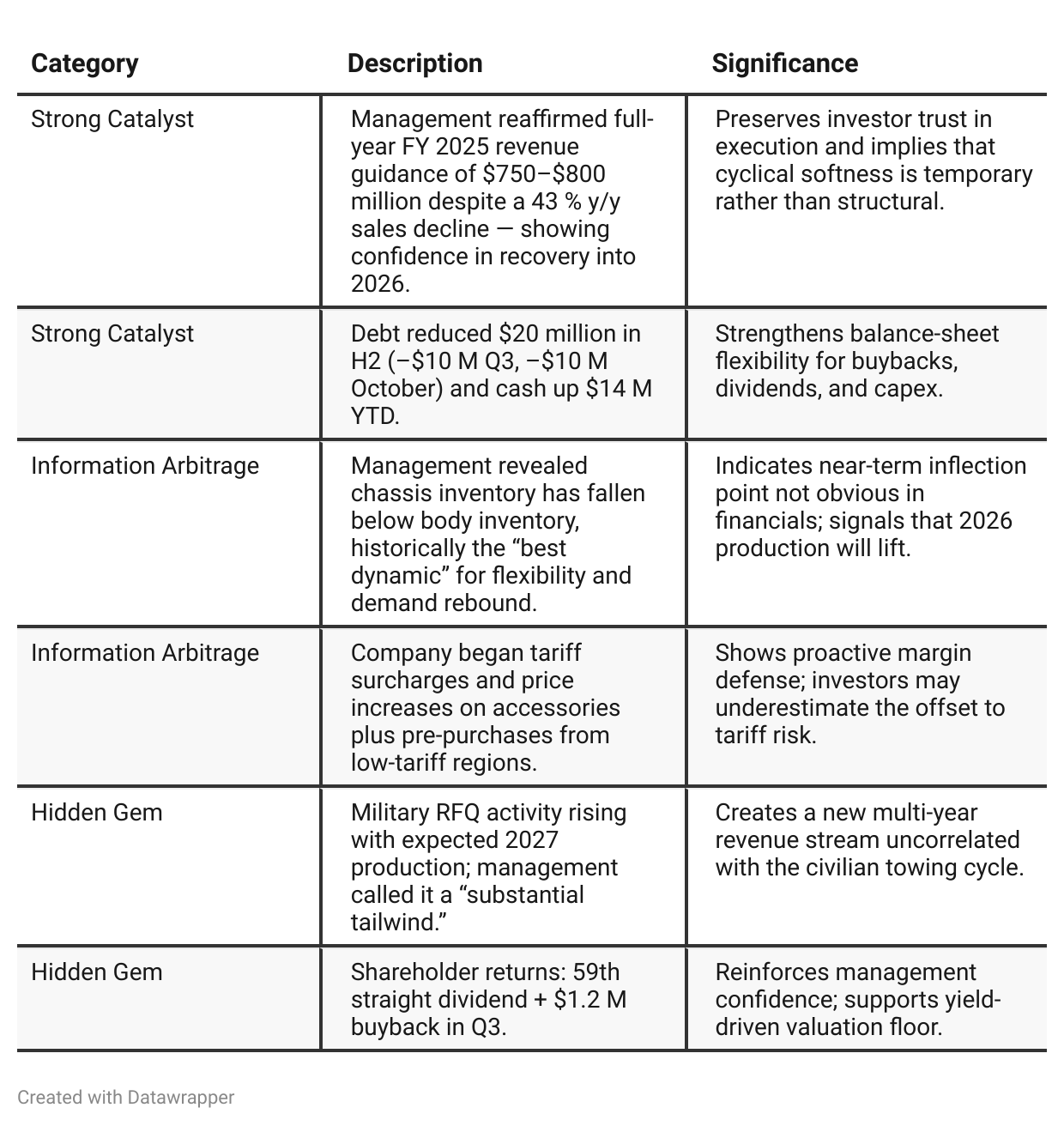

Positive Insights

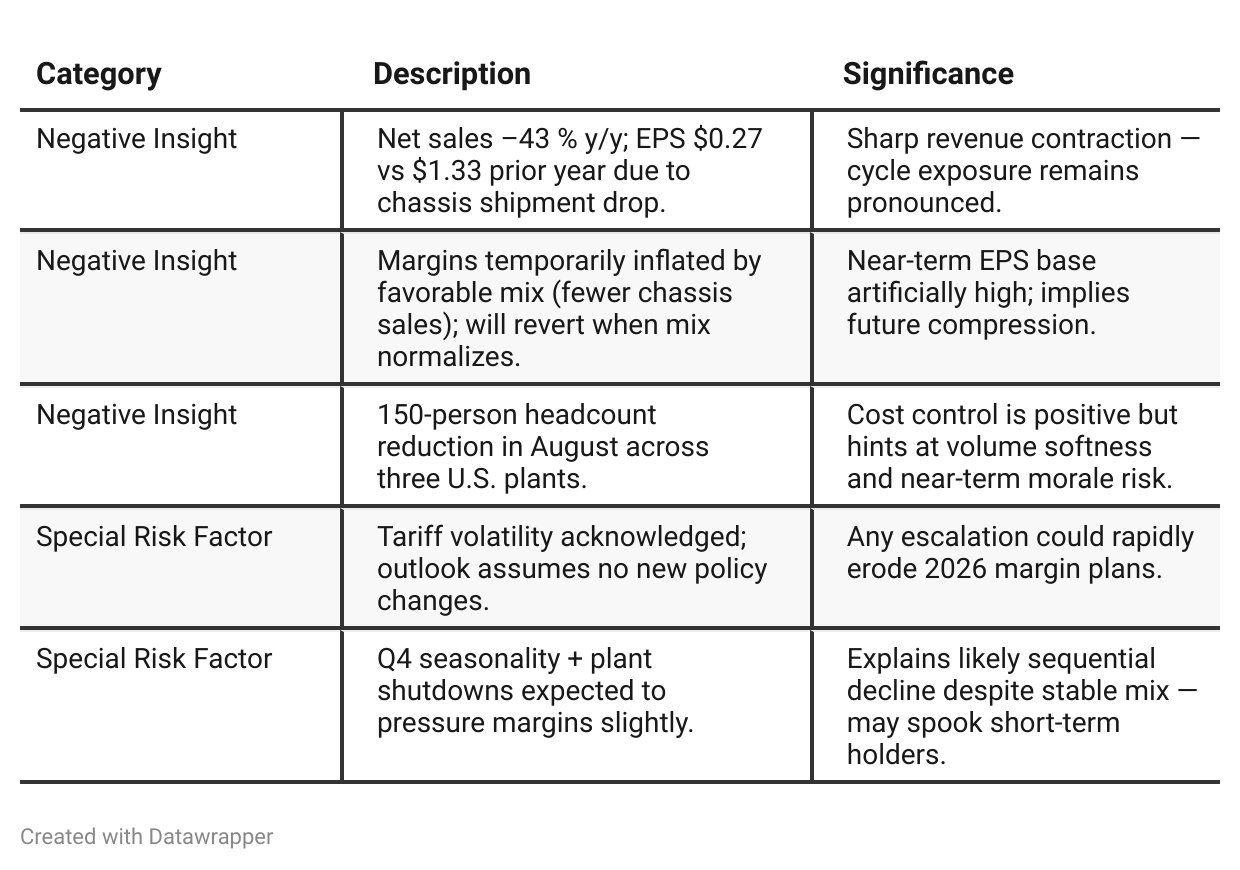

Negative Insights

Tariff Risk

Management directly addressed U.S. tariffs:

Implemented tariff surcharge on all new orders,

Raised prices on parts and accessories,

Pre-purchased key materials from low-tariff regions,

Assumed “no change in current regulations” for guidance purposes.

Analysis:

Their strategy blends pricing power and supply-chain hedging to maintain margins. While a new tariff round could pressure working capital and cash flow, the current approach shows mature risk management and suggests that margin impact would be contained rather than destructive.

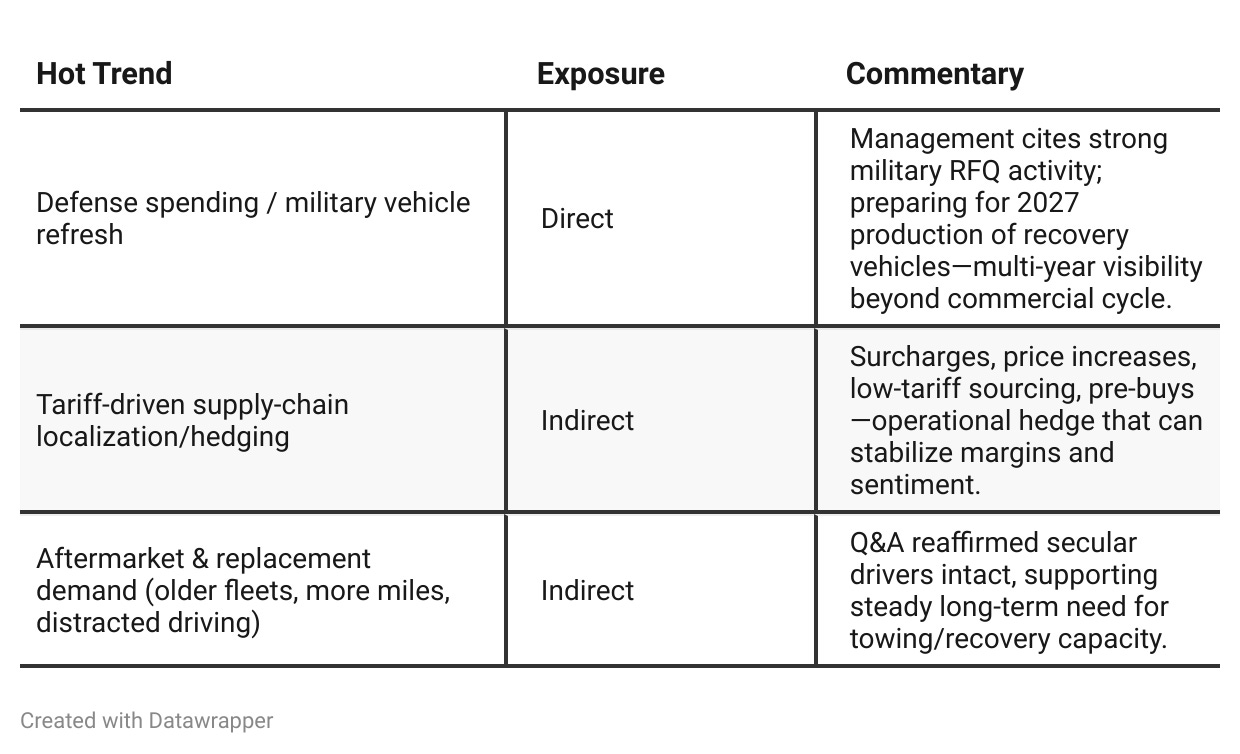

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025: Management triages the downcycle — trims FY25 revenue outlook, suspends EPS guidance, throttles production to drain channel inventory, and rolls out a tariff/price mitigation plan while building cash and cutting debt.

Q3 2025: Management executes the reset — headcount/retirement actions taken, chassis inventory crosses below body (a historical green light), liquidity strengthens, buybacks accelerate, and the defense pipeline becomes a tangible 2027 opportunity. Near term, margins fade as mix normalizes; medium term, 2026 volumes and military add a second engine.Year-over-year comparison

Q3 2024:

Miller Industries was operating in a strong demand environment, clearing pandemic-era bottlenecks and highlighting sustained replacement needs. Management’s focus was on production efficiency, capacity, and sustaining record results. Tone: “steady expansion and margin discipline.”Q3 2025:

The narrative shifts sharply to resilience and positioning. Management acknowledges the cyclical downturn, details decisive cost cuts and workforce actions, and underscores a clean balance sheet. The tone blends realism with cautious optimism: the company is weathering short-term pressure but sees a clear setup for recovery in 2026 and a structural defense-market tailwind by 2027.

Final Takeaway

Miller Industries (NYSE: MLR) is in a stabilization-to-expansion phase, emerging from a cyclical demand dip with a deleveraged balance sheet, strong cash flow, and improving inventory mix. The company’s proactive tariff strategy and rising military demand provide visibility into a multi-year recovery. While margins may contract short-term as chassis mix normalizes, the structural drivers for tow-truck replacement remain intact. Verdict: BUY, with moderate upside as 2026 volumes recover and defense orders materialize.