Miller Industries, Inc. (NYSE: MLR) – Q2 2025 Earnings

Miller Industries, Inc. (NYSE: MLR) – Q2 2025 Earnings

Earnings Release Date: Aug. 6, 2025

Stock Price: $41.39

Market Cap: $474.2 million

Q2 2025 sales of $214.0 million vs $371.5 in the prior year

Q2 2025 EPS of $0.73 vs $1.78 in the prior year

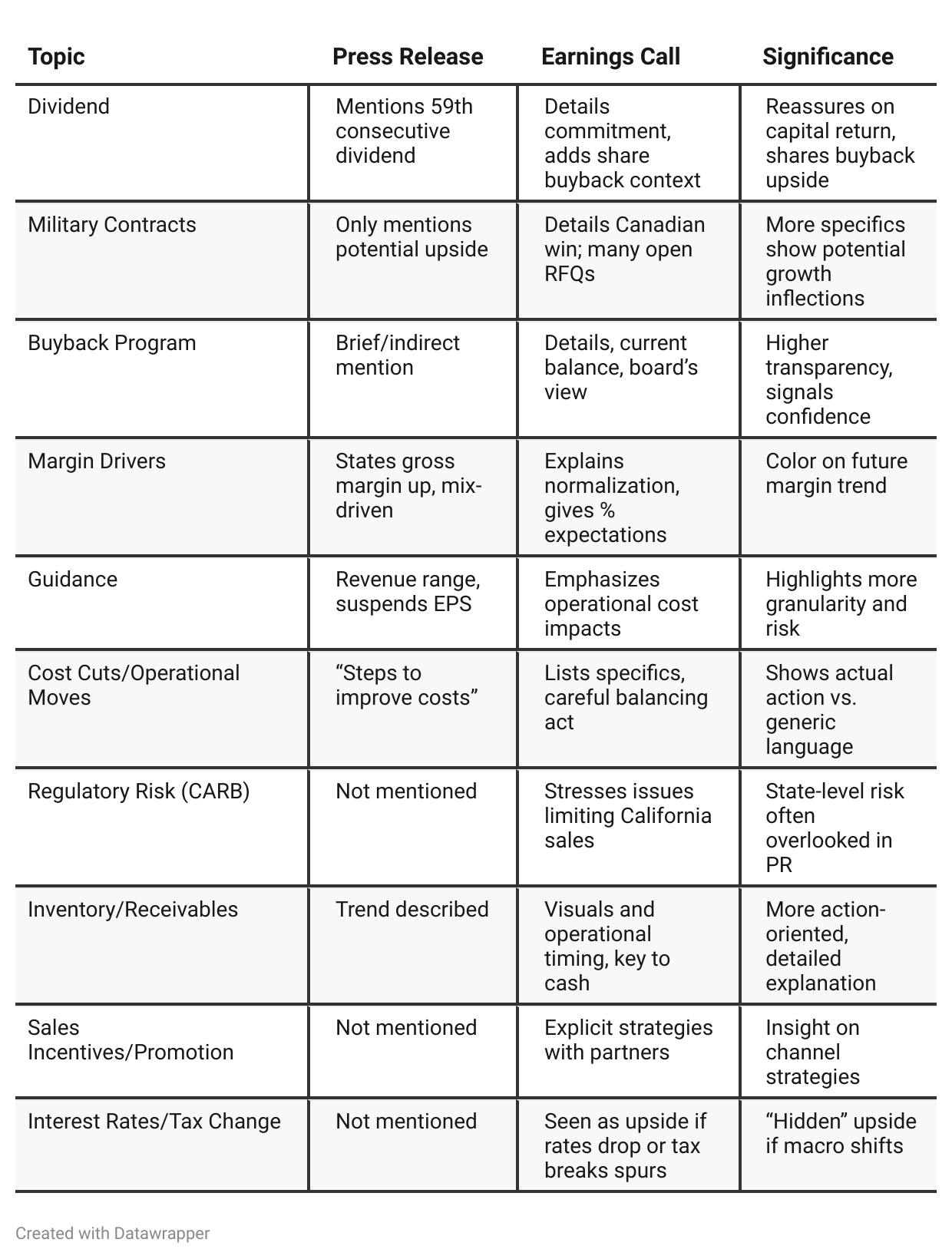

Press Release vs Call Transcript Comparison

Earnings call offers nuanced operational detail and future levers (e.g., planned cost cuts, how incentives are being deployed, anticipation of an interest-rate-driven bounce, specific regulatory bottlenecks in CA). These may or may not materialize in numbers yet—but are vital for forecasting.

Management’s tone more defensive and tactical in the call vs. the measured optimism in the press release. Recognizing this “up-close” operating vigilance versus the “front-office” confidence is important.

EPS guidance suspension and discussion of potential H2 losses are strong signals to curb near-term bullishness pending further color in future updates (potential setup for disappointment or, conversely, surprises if market conditions improve quickly).

Balance sheet strength (cash generation, debt reduction) is more pronounced in the call, indicating room for weathering a prolonged downturn.

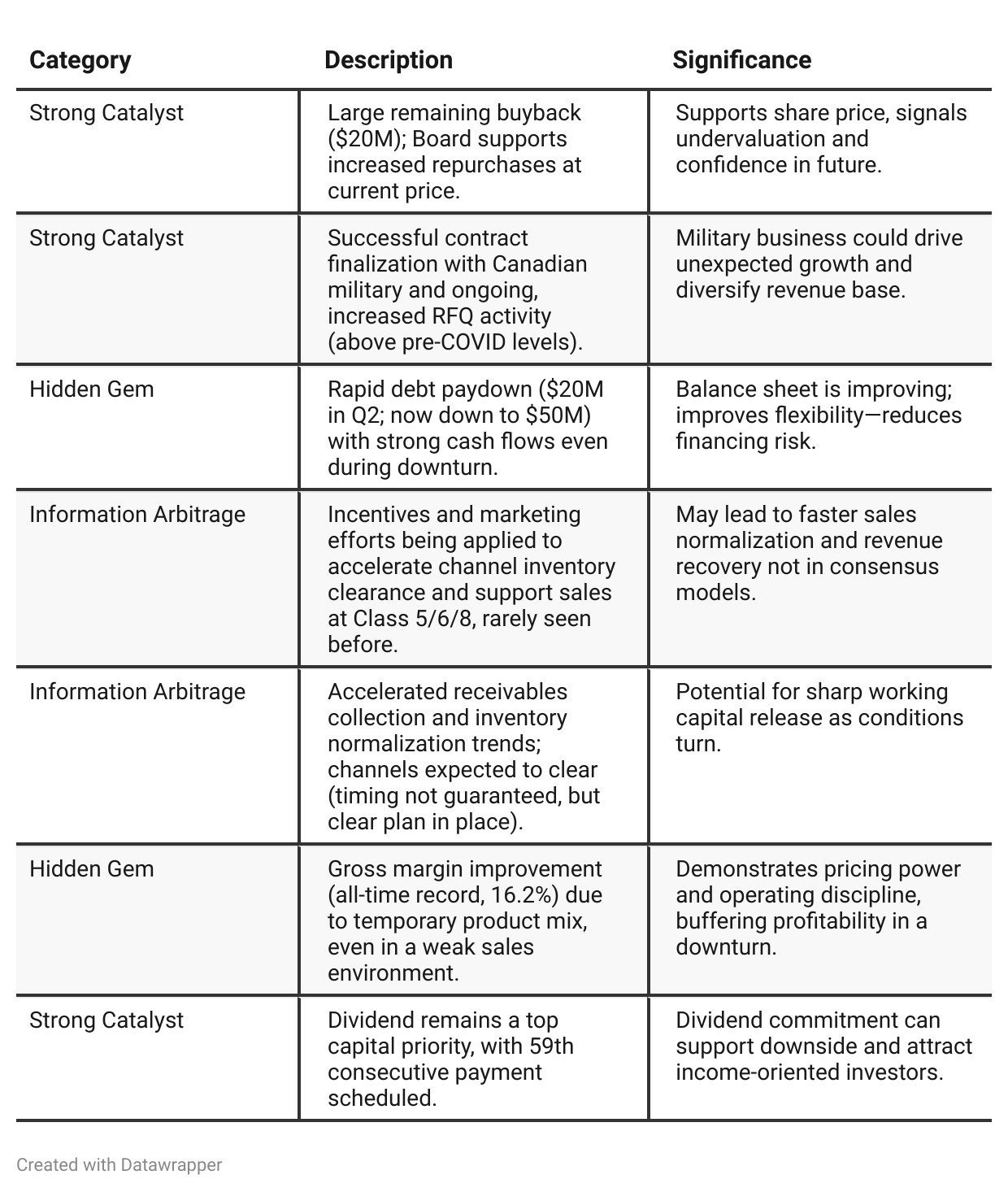

Positive Insights

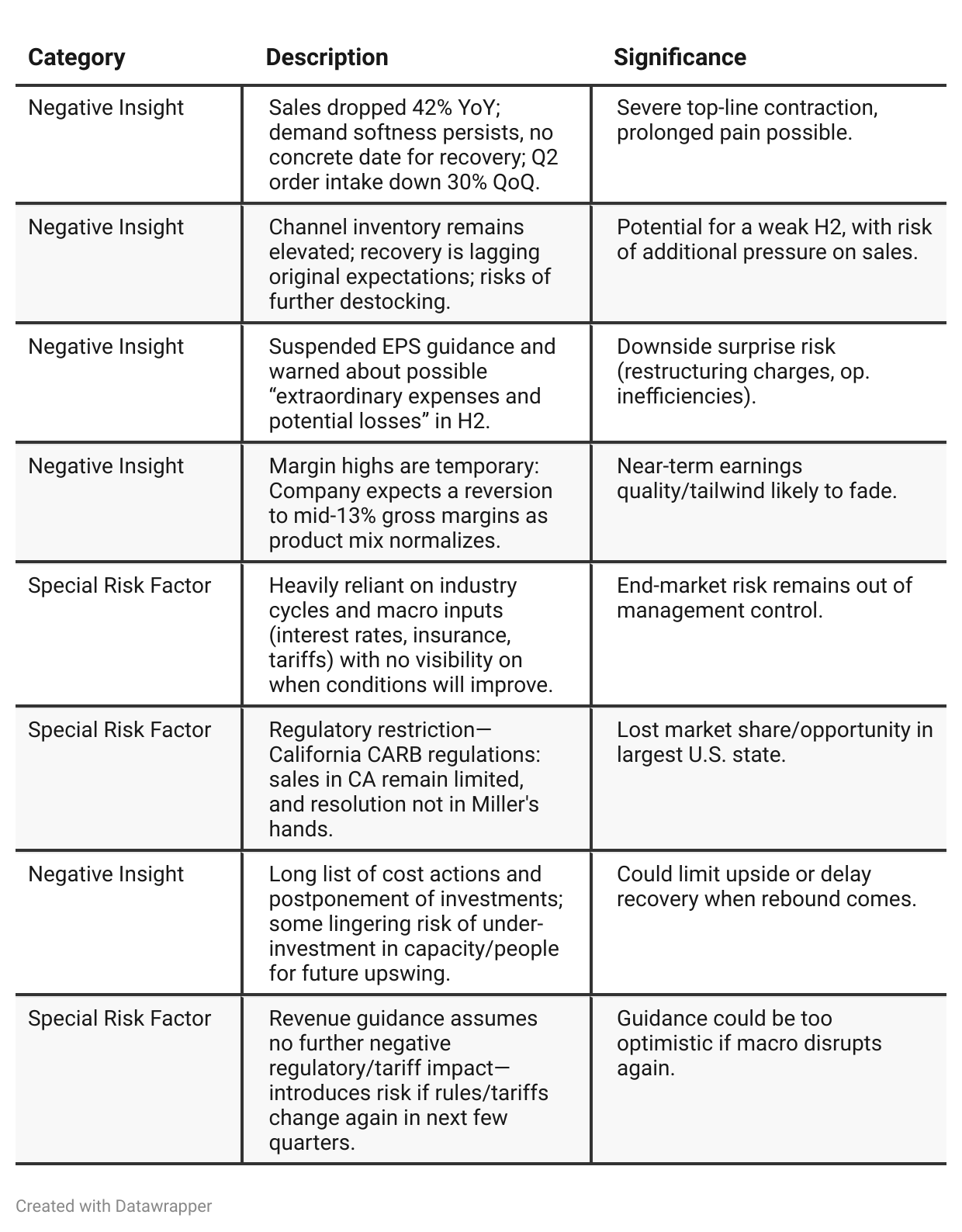

Negative Insights

Tariff Risk

Tariffs as a Headwind: Management repeatedly cites tariffs as a contributor to elevated end-user costs, higher cost of ownership, and ongoing softness in demand. They mention specifically “tariff-related price increases” impacting both their own costs and the willingness of customers to purchase new equipment.

Mitigation Actions: The company has implemented tariff surcharges on all new manufactured product orders and has raised prices on parts and accessories to help offset these tariff-related costs. They are securing their supply chain to mitigate longer-term tariff risks, though specifics on supply chain adaptation are not detailed.

Impact on Revenue and Profitability: Tariffs have increased product prices, which has contributed to reduced order intake (~30% decline in Q2) and inventory buildup in the distribution channel. This pricing pressure creates downside risk to revenue and margins if customers continue to defer purchases or if Miller cannot fully pass through the increased costs.

Effects on Market Share and Innovation: The call does not mention direct loss of market share or reduced ability to innovate due to tariffs. The company’s actions are focused on cost pass-through and supply chain stabilization rather than new competitor threats or innovation slow-downs.

Forward-Looking Statements: Management states that their revised revenue guidance “anticipates no changes in the current regulations or unknown effects of rapidly evolving tariff situation.” This is a clear caveat: any new, unexpected, or escalated tariff actions could quickly invalidate their outlook and further pressure profitability.

Sentiment Analysis

The overall sentiment toward $MLR is bullish. Several investors explicitly express buying intentions and confidence in the stock, with statements about accumulating more shares and viewing it as undervalued, despite recent negative headlines about layoffs and sales declines. The willingness to build or hold long positions outweighs concern over recent operational challenges, indicating optimism for a rebound or undervalued opportunity.

Previous Earnings Call

Quarter-over-quarter comparison

In Q1 2025, Miller Industries conveyed cautious optimism: progress on inventory normalization, supply chain management, and capital returns indicated confidence in weathering macro volatility, with management reiterating guidance and targeting renewed growth in 2026. By Q2 2025, the narrative shifted as persistent demand headwinds, prolonged channel inventory, and higher macro pressures forced management into a defensive posture. The company reduced sales forecasts, suspended EPS guidance out of prudence for upcoming operational changes, and placed new emphasis on cost-cutting and liquidity. While long-term confidence and capital return commitment were reiterated, the mood shifted clearly from proactive positioning to resilience and risk management amid ongoing uncertainty.Year-over-year comparison

Miller Industries’ narrative shifted dramatically between Q2 2024 and Q2 2025. In Q2 2024, the company was riding a wave of record demand and profitability, projecting double-digit growth, expanding margins, and talking up investments in capacity and productivity. The focus was on fueling growth and rewarding shareholders.

By Q2 2025, the company is in retrenchment mode: aggressively managing costs, slashing guidance, suspending profit outlooks, safeguarding liquidity, and shifting the focus from growth to near-term survival through a pronounced market slump. Regulatory and macro headwinds have moved from background risks to central challenges that dominate strategy and tone. The company remains committed to long-term fundamentals and capital returns, but the narrative is now one of defensive resilience and careful positioning for an eventual recovery, with an open admission that timing is highly uncertain.

Final Takeaway

Miller Industries is in a stabilization phase, defending margins and liquidity amid a severe industry downturn and inventory glut. While capital returns, cash flow discipline, and a stronger balance sheet provide downside support, a lack of near-term earnings visibility and demand softness remain the dominant risks. Execution on inventory normalization, cost controls, and tracking the pace of order recovery—alongside mitigating regulatory and tariff headwinds—will be critical for future performance. Verdict: HOLD, with potential upside if industry conditions normalize or military contracts materialize, but with clear near-term caution advised.