Limbach Holdings, Inc. (NASDAQ: LMB) – Q3 2025 Earnings

Limbach Holdings, Inc. (NASDAQ: LMB) – Q3 2025 Earnings

Press release and earnings call link

Earnings Release Date: Nov. 04, 2025

Stock Price: $93.45

Market Cap: $1086.5 million

Q3 2025 sales of $184.6 million vs $133.9 million in the prior year

Q3 2025 EPS of $0.73 vs $0.62 in the prior year

Overview: Limbach (Nasdaq: LMB) is a building-systems solutions firm that designs, builds, services and retrofits mission-critical mechanical/electrical/plumbing (MEP) infrastructure for owners of complex facilities. End-markets include healthcare, industrial/manufacturing, data centers, life science, higher ed, and cultural/entertainment.

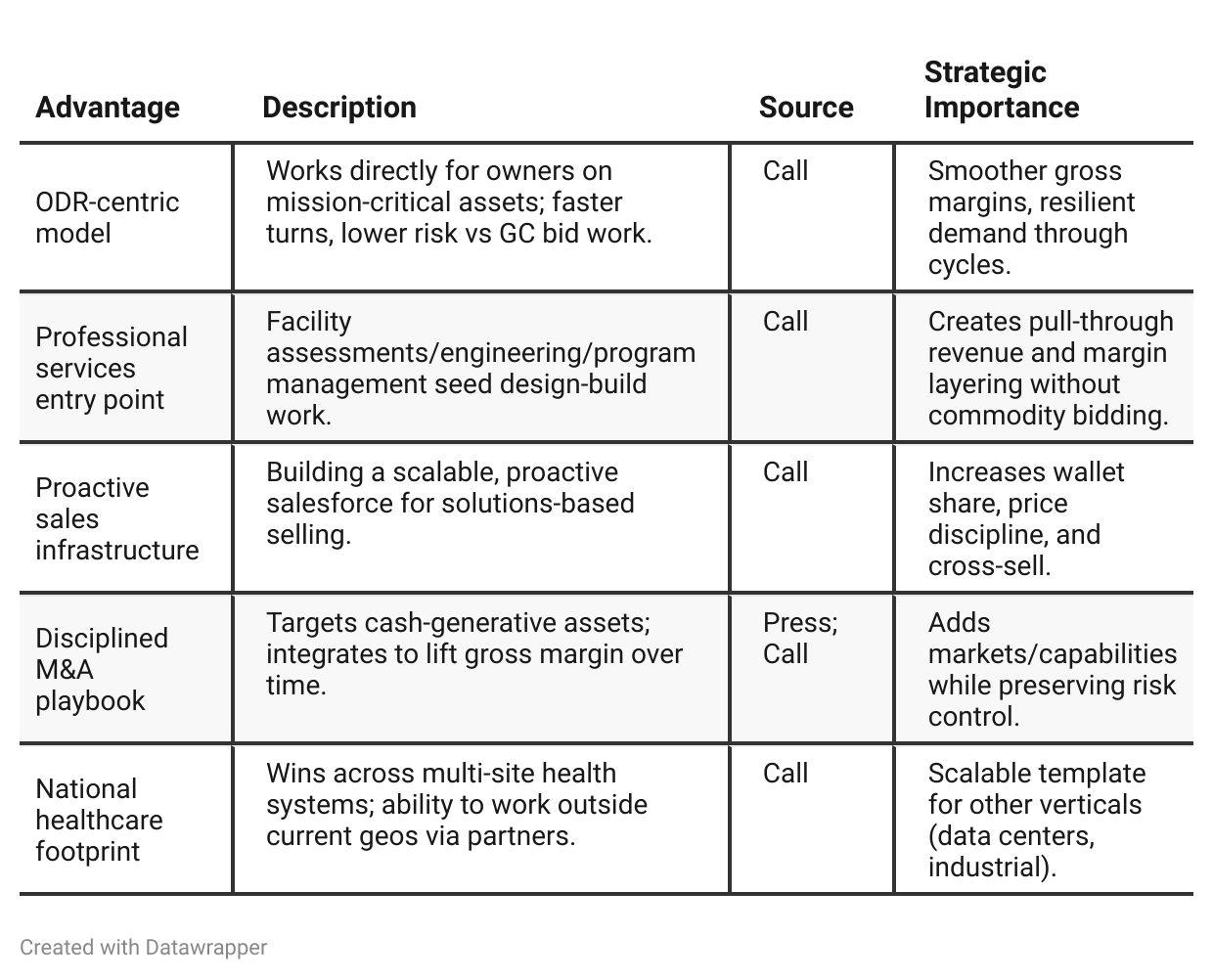

Revenue drivers: Mix is intentionally shifting toward ODR (Owner Direct Relationships—work performed directly for building owners) vs GCR (General Contractor Relationships—project work bid under a GC). In Q3’25 ODR = ~77% of revenue.

Main customers / end-market base: National healthcare systems, industrial plants (notably shutdown/maintenance periods), selective data-center operators, plus life science/higher-ed.

Market positioning: Emerging owner-focused consolidator with a multi-year pivot from traditional E&C (engineering & construction) bidding to recurring, lower-risk owner-direct work and tuck-in M&A.

Recent financial trajectory: Q3’25 revenue +37.8% Y/Y; ODR +52%; net income +17%; Adj. EBITDA +26% (margin compression from a newly acquired, lower-margin unit). FY25 revenue/Adj. EBITDA guidance reaffirmed.

Near-term themes (from mgmt): 1) Integration of Pioneer Power (acquired July 2025) with a plan to lift margins; 2) scaling a proactive sales model; 3) emphasizing professional services (facility assessments, engineering) to seed higher-margin projects; 4) ODR mix 70–80% for FY25, with ODR organic growth targeted at 20–25%.

Competitive Advantage Insights

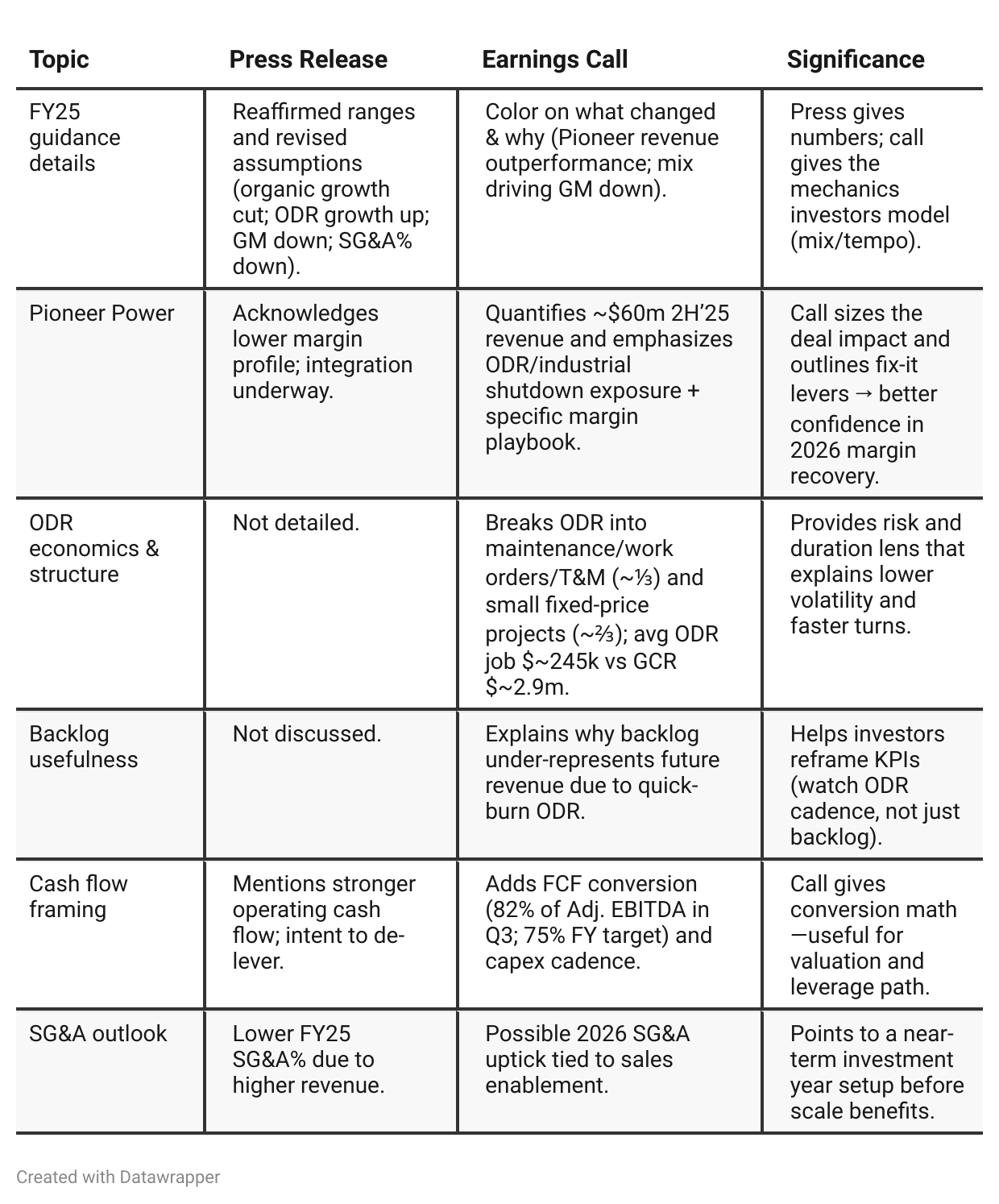

Press Release vs Call Transcript Comparison

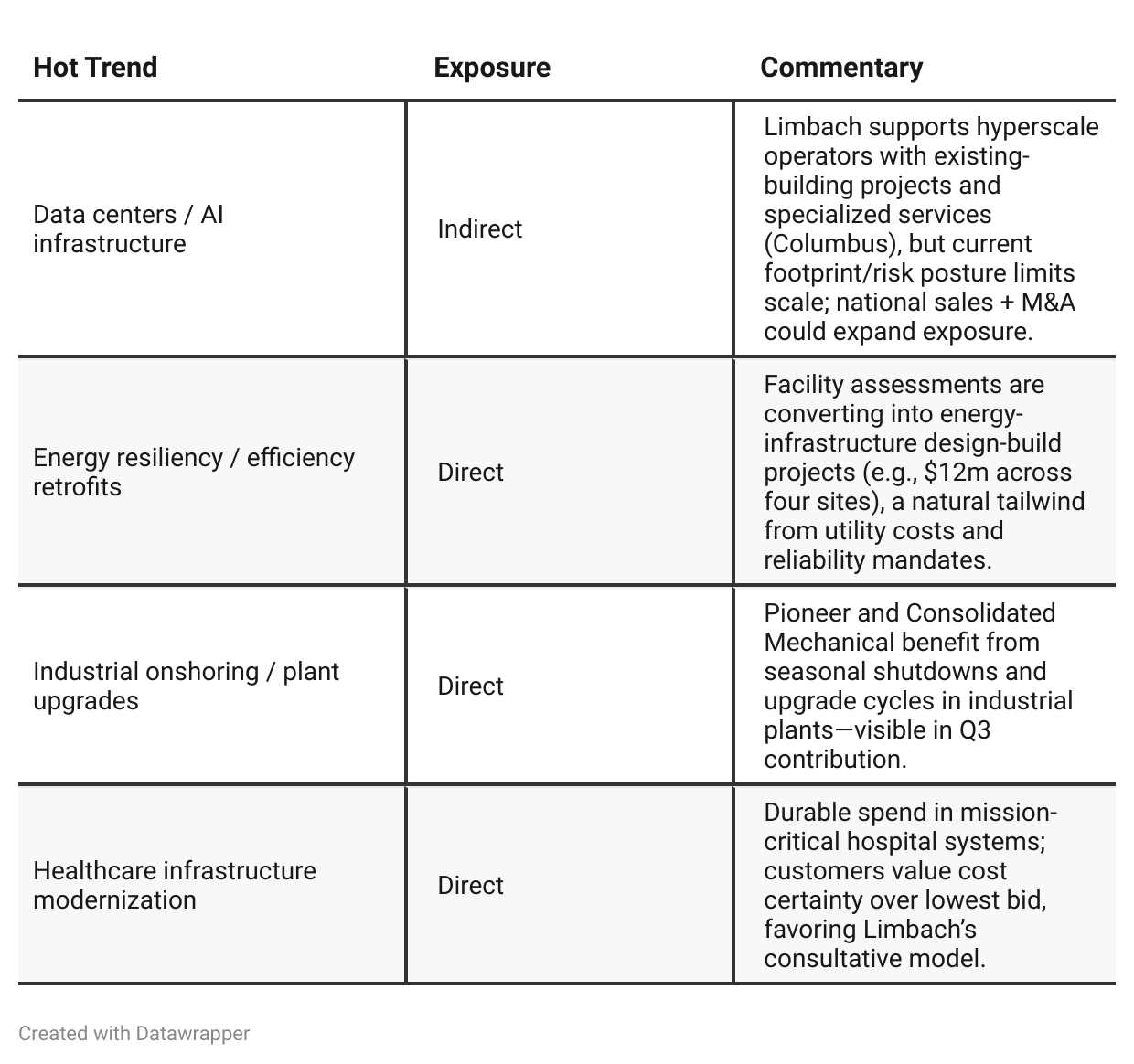

Vertical demand signals: The call details national healthcare wins (20 facility assessments → $12m projects across four sites, 3 outside current footprint) and outlines a template for expanding professional services into data centers and industrials—none of which is in the PR.

Sales model maturation: Call highlights three-year build-out of proactive sales and sales enablement focus for 2026—key to mix improvement and price discipline.

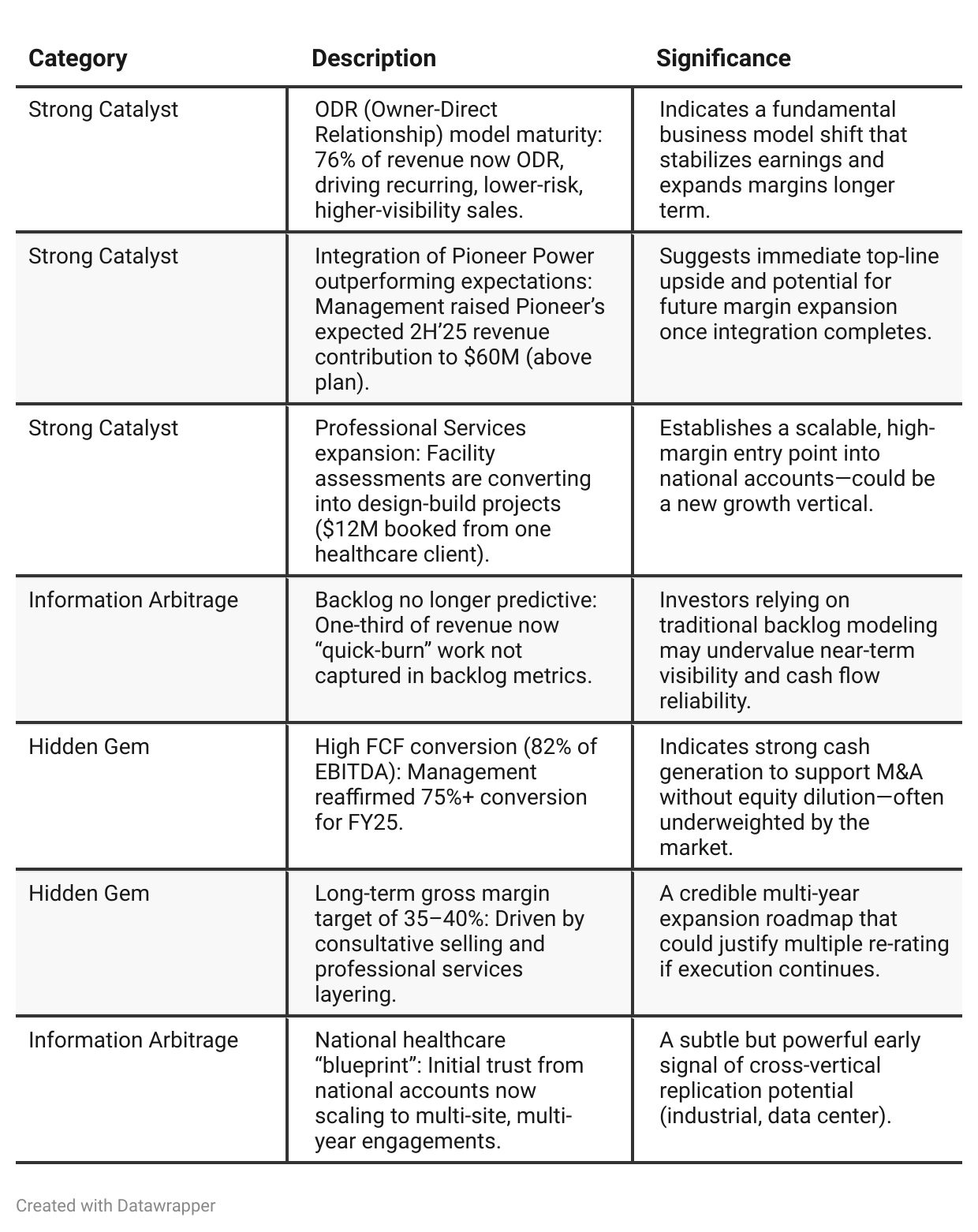

Positive Insights

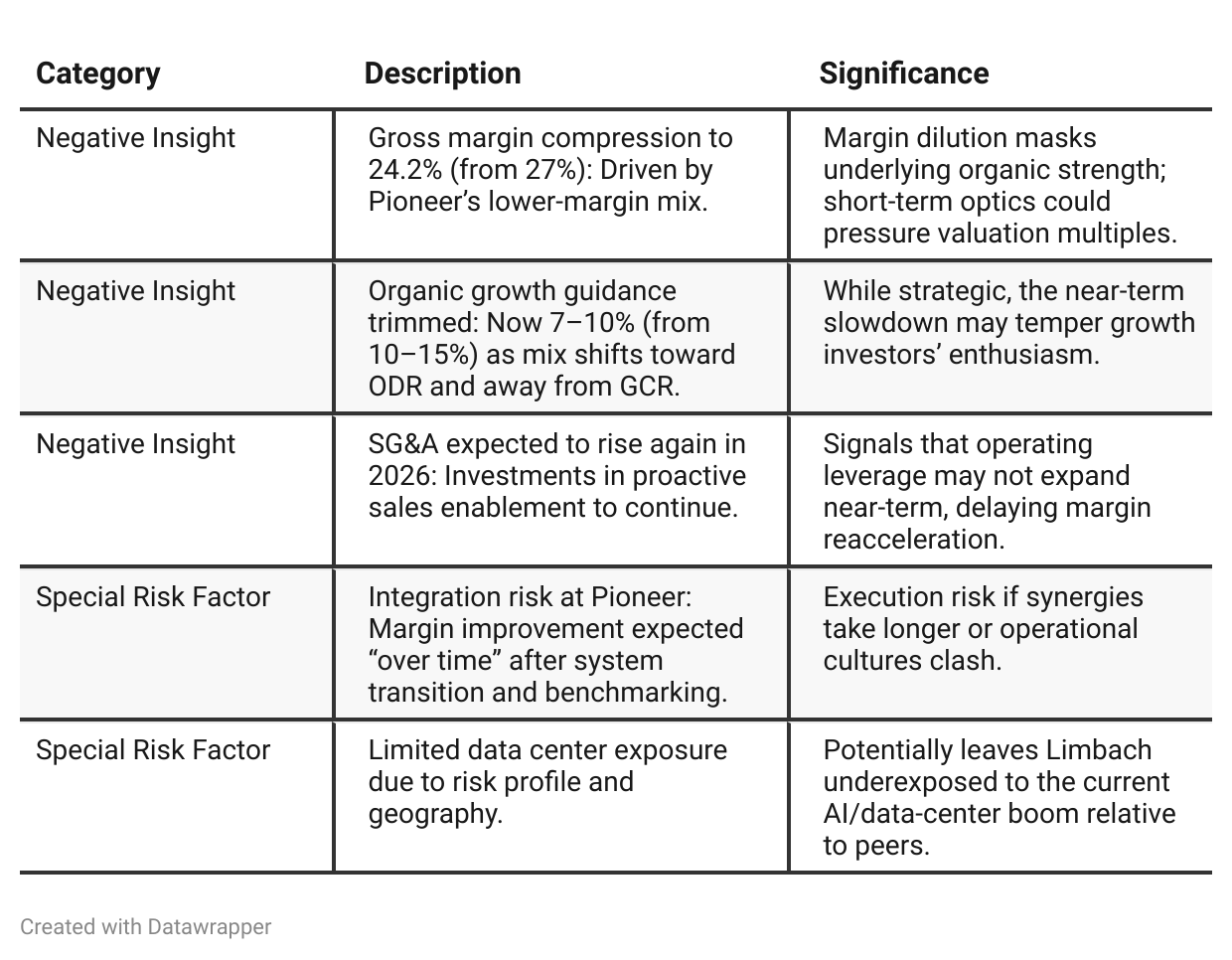

Negative Insights

Investor Underappreciation Signals

✅Backlog is the wrong KPI now — ODR’s quick-burn mix means revenue is increasingly book-and-burn inside the quarter, so traditional backlog screens understate forward visibility; investors may be overlooking this until management’s repeated reminders reset modeling.

✅Pioneer revenue is bigger than feared — Second-half Pioneer contribution of ~$60m is ODR-heavy and tied to durable industrial shutdown cycles; the market may still anchor to margin drag and miss the top-line step-up that funds deleveraging until margin-improvement milestones show up.

✅Professional services as a margin wedge — National facility assessments and engineering work are creating design-build pull-through (e.g., $12m awards) that layer margins; because it’s not broken out in the PR, many may miss this structural driver until disclosure accumulates.

✅High FCF conversion discipline — 82% Q3 Adj. EBITDA conversion and a 75% FY target support ongoing revolver paydown; screens focused on GAAP margins may underweight cash conversion until several quarters establish the pattern.

Tariff Risk

The transcript contained no references to tariffs or trade policy. There was no indication that U.S. tariffs, supply-chain restrictions, or import costs materially affect operations. Limbach’s exposure is primarily domestic, service-based, and centered on mission-critical facility work (healthcare, industrial, education). Therefore, tariff risk is minimal, and no mitigation strategies (such as supplier shifts or pricing adjustments) were discussed.

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Earlier (Q2’25): “We’ve built the strategy (ODR shift, proactive sales, disciplined M&A), staffed for it (40 sales hires, new SVP), and set conservative guidance while we integrate our largest acquisition (Pioneer). Expect heavier 2H weighting.”Current (Q3’25): “The strategy is operating at scale. Here’s exactly how ODR creates durable, quick-turn revenue that doesn’t show up in backlog; here’s how national assessments are already converting to funded projects; Pioneer’s revenue is ahead of plan; guidance stands with revised internal drivers; cash conversion is strong; and we’re investing in sales enablement for 2026.”

Year-over-year comparison

Q3 2024: Limbach presented itself as a disciplined operator mid-transformation—migrating from cyclical contracting to a recurring, owner-direct model. The focus was proving the ODR thesis, embedding sales culture, and building credibility for future M&A scale.

Q3 2025: The narrative matures into that of a cash-flow-driven platform company. Management articulates not just strategy but systems and data—revealing ODR composition, FCF metrics, and sales enablement investments. The company’s story shifts from “trust us, it works” to “here’s how and why it works.”

Final Takeaway

Limbach Holdings is in a growth-through-transition phase, shifting from traditional contracting (GCR) to an asset-owner partnership model (ODR). Strong execution, disciplined M&A, and superior cash flow underpin its stability. While margin compression clouds optics, underlying economics are improving. Execution on Pioneer integration and professional services scaling will be key to realizing its long-term 35–40% gross margin goal.

Verdict: Buy, with potential for 20–30% upside over 12–18 months if ODR margin expansion becomes evident by mid-2026.