Limbach Holdings, Inc. (NASDAQ: LMB) – Q2 2025 Earnings

Limbach Holdings, Inc. (NASDAQ: LMB) – Q2 2025 Earnings

Earnings Release Date: Aug. 5, 2025

Stock Price: $134.12

Market Cap: $1559.1 million

Q2 2025 sales of $142.2 million vs $122.2 million in the prior year

Q2 2025 EPS of $0.64 vs $0.50 in the prior year

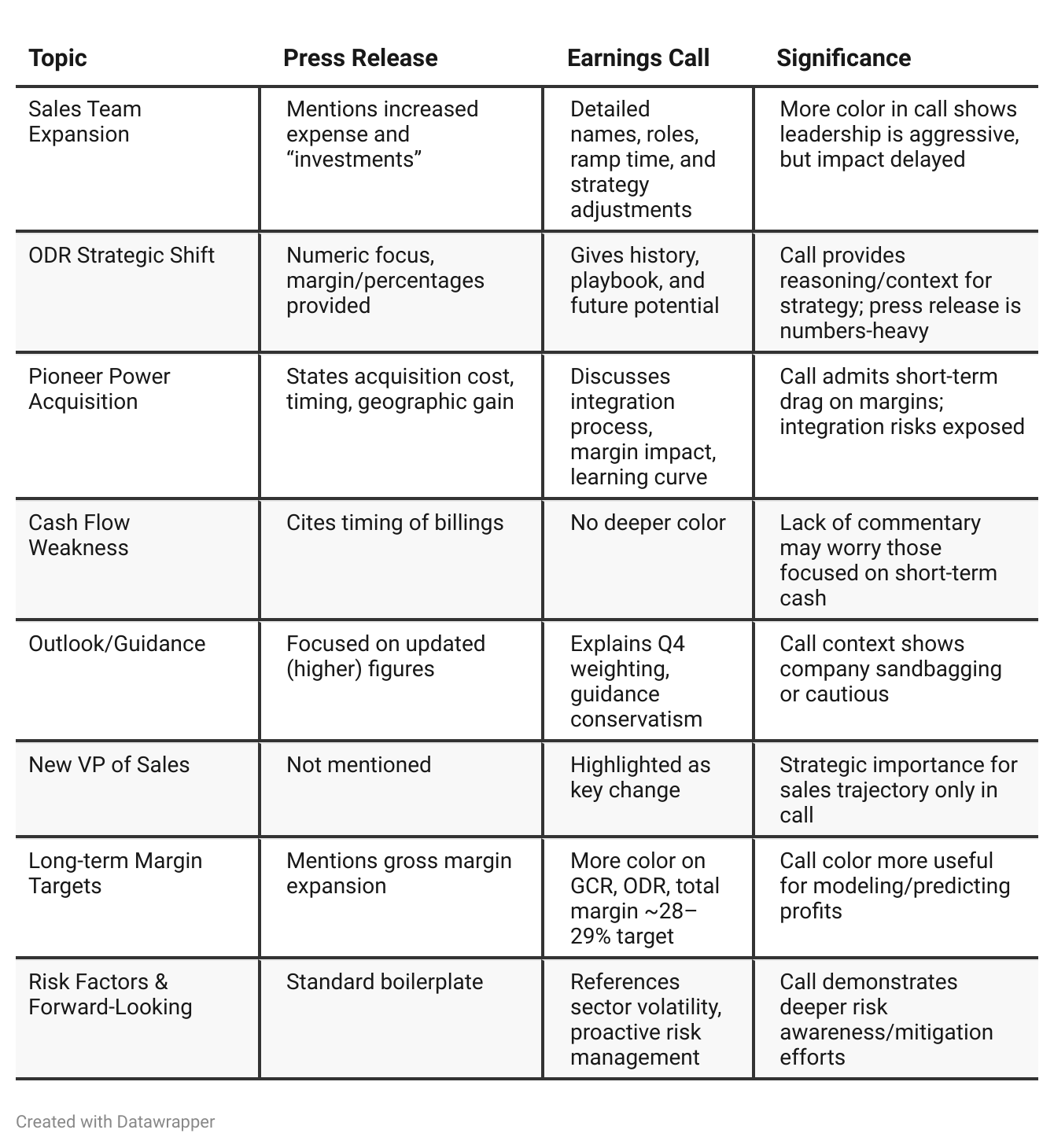

Press Release vs Call Transcript Comparison

Press Release is Number-Driven and Upbeat: Focused on topline, margin, EPS growth, and deal completion. All attention is on positive trajectory; risks and integration details are minimized.

Earnings Call is Qualitative and Transparent: Management directly addresses potential short-term headwinds (margins, M&A learning curve), discusses macro uncertainty, sectoral exposure, and integration timeline.

Integration Risk is Only in Call: Essential for investors to recognize that acquisition synergies, especially on margins, will not materialize immediately, leaving open the possibility of near-term disappointment.

Sales Structure Evolution is Detailed in Call Only: The move to a 'financial sale' approach and focus on national account strategies points to a more sophisticated sales org—but is not an immediate catalyst, reinforcing long-term thesis.

Press Release Omits Short-Term Margin Headwinds and Ramp: Numbers look great, but speedbumps are only admitted in Q&A and prepared remarks.

Quarterly Results Heavily Weighted Toward Q4: This nuance, shared only in the call, is crucial for modeling and avoiding misinterpretations in Q3.

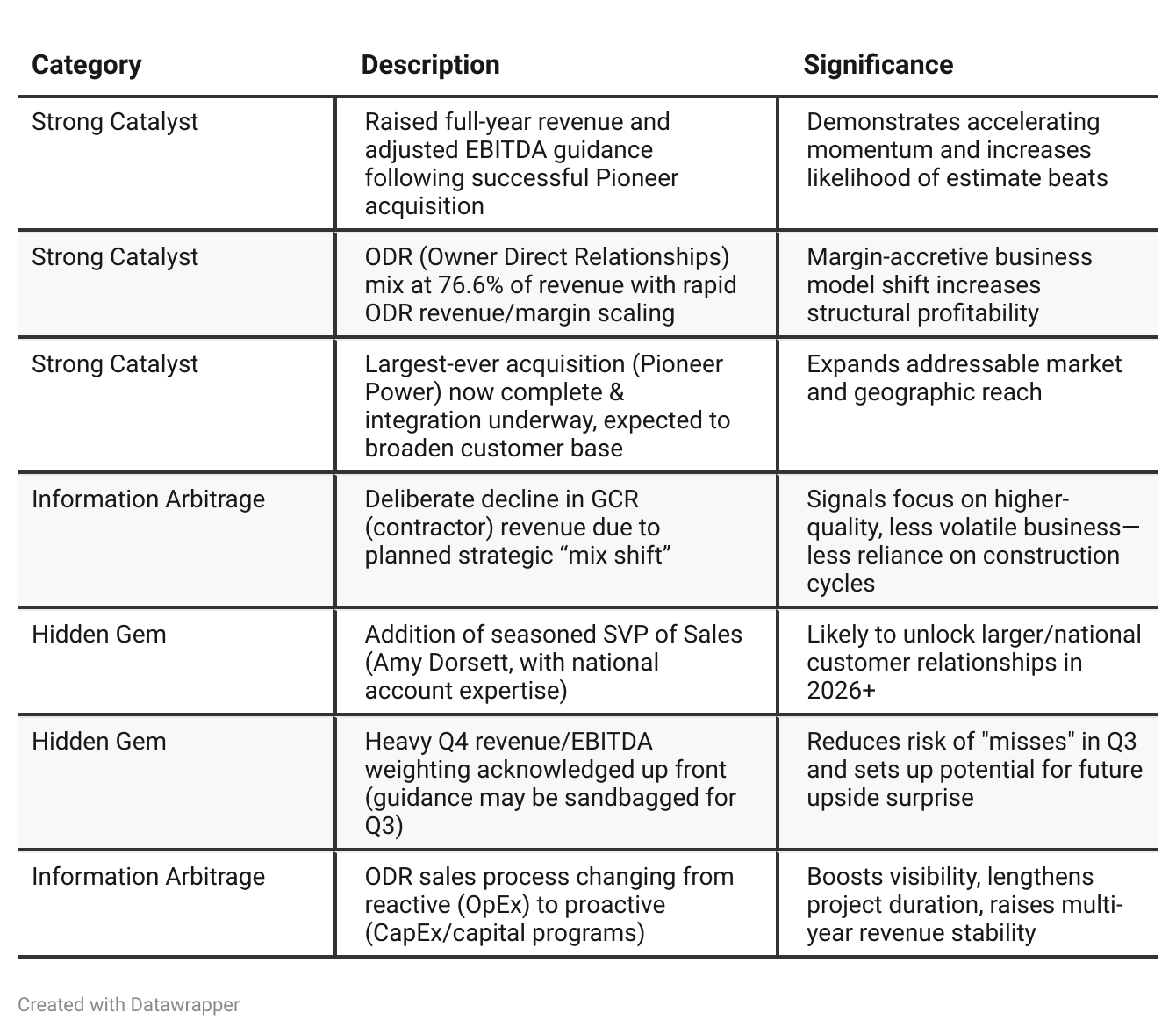

Positive Insights

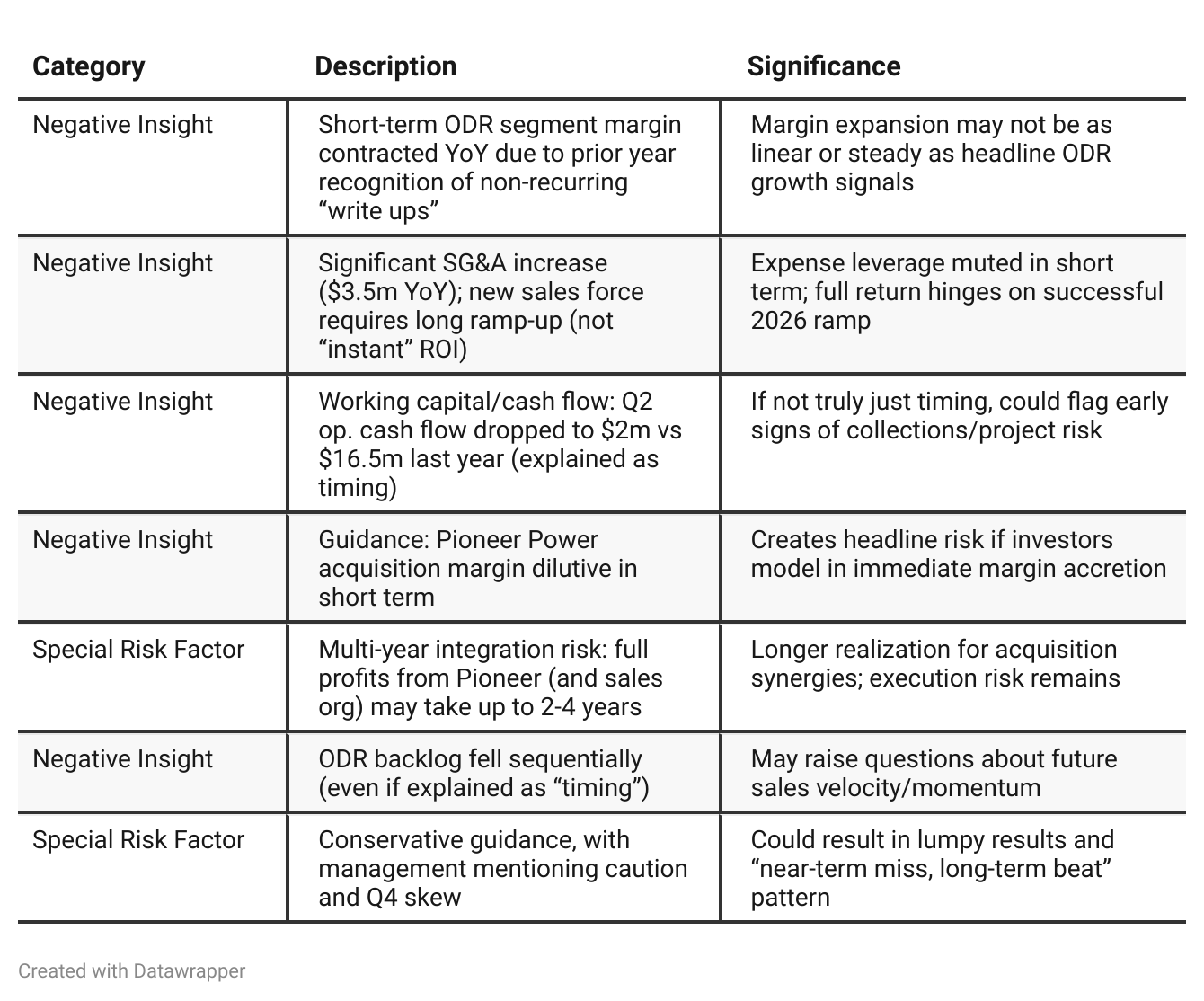

Negative Insights

Tariff Risk

No mention of tariffs, trade policy, or supply chain disruption due to tariffs was made anywhere in the earnings call transcript. There is no discussion of international sourcing, tariff-related cost impacts, or explicit actions being taken to mitigate possible trade policy risks. Consequently, there is no evidence that tariffs are currently a risk factor influencing Limbach’s revenue, profitability, or market strategy, nor is there any stated impact on their competitive position or innovation pipeline related to U.S. trade policy. Investors should confirm with future filings/calls if the macro/trade environment changes or if the company increases its exposure to international supply chains.

Sentiment Analysis

The overall sentiment toward $LMB is bearish. While a few investors note that the stock’s valuation is becoming more attractive after a pullback and acknowledge management's reputation, most commentary highlights significant concerns: accusations of aggressive accounting, weak disclosure, questionable governance, margin compression, and revenue and cash flow disappointments. The term “short candidate” comes up repeatedly, and several explicitly discuss initiating or recommending short positions, citing overvaluation and risk factors. Though some see potential long-term value, the prevailing tone is skepticism and caution, with multiple posts emphasizing downside risk and a lack of visible upside catalysts.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: Limbach presented itself as a company hitting its stride: ODR is working, financial results are strong, growth is broad-based, and investments in sales and selective M&A offer further upside. The narrative was celebratory and expansionary, with potential headwinds (tariffs, macro) brushed aside as manageable.Q2 2025: The company’s narrative becomes more nuanced and operational. While celebration of growth continues, management is clearly focused on risk management, the complexity of integrating its largest acquisition (Pioneer), and the realities of ramping up a much larger salesforce. There is a new strategic layer: maturing ODR relationships, evolving sales to drive proactive, multi-year budgeting with customers, and executing on a broader national/national account strategy. Q2 messaging is more transparent about timing risks (guidance conservatism, Q4 weighting) and the long-term nature of realizing integration benefits, while reiterating the core confidence in the ODR/relationship-driven business model.

Year-over-year comparison

Q2 2024: Limbach is a company executing on a clear transformation playbook. The story centers on the success of shifting to ODR for better margins and stability, building a robust service offering, and strategically expanding through carefully chosen acquisitions. Leadership is optimistic—strategy is working, metrics are up, and momentum is strong.

Q2 2025: The narrative matures. The strategy’s successes have culminated in ODR becoming dominant, but the company is now playing a more complex game: integrating a large acquisition, accelerating the sophistication of its sales and customer management, and promoting a more nuanced, value-added, and proactive relationship with key customers. Leadership’s tone is more transparent about timing, risks, and required patience for new initiatives to bear fruit. The company is not just transforming; it’s evolving its operational model and scaling complexity, with an eye toward sustainable value in a competitive, technical marketplace.

Final Takeaway

Limbach Holdings is in a growth/expansion phase, pivoting aggressively to Owner Direct Relationships (ODR) for higher quality, recurring revenue. The company’s largest-ever acquisition (Pioneer Power) and a substantial build-out of its sales team are clear investments in scale and capability, though these steps bring near-term margin and integration risks. While core guidance has been raised, management signals conservatism and a Q4-weighted year, underscoring the need for execution on integration and sales ramp. Investors should closely monitor margin trends, cash flow normalization, and progress on ODR strategic initiatives.

Verdict: HOLD (with a positive bias if coming quarters confirm integration and cashflow upside). Upside hinges on disciplined execution and conversion of recent investments into sustainable EPS growth.