KORU Medical Systems, Inc. (NASDAQ: KRMD) – Q3 2025 Earnings

KORU Medical Systems, Inc. (NASDAQ: KRMD) – Q3 2025 Earnings

Press release and earnings call link

Earnings Release Date: Nov. 12, 2025

Stock Price: $3.73

Market Cap: $172.3 million

Q3 2025 sales of $7.5 million vs $8.0 million in the prior year

Q3 2025 EPS of ($0.05) vs ($0.12) in the prior year

Overview:

KORU Medical Systems develops and markets subcutaneous infusion systems (Freedom60®/FreedomEdge®) for home- and clinic-based drug delivery, primarily used for immunoglobulin (IG) therapy and growing applications in oncology and rare diseases.

Revenue Drivers:

Core driver is the Subcutaneous Immunoglobulin (SCIg) franchise, with growing revenue from Pharma Services & Clinical Trials (PST) collaborations that enable drug-device pairings for biopharma clients.

Customer Base:

Primarily specialty pharmacies, distributors, and biopharma partners; end-users are patients with immune deficiencies or chronic diseases requiring regular infusions.

Market Positioning:

A niche leader in manual/mechanical subcutaneous infusion systems—simpler, lower-cost alternatives to electronic pumps—expanding globally and into oncology.

Recent Financial Trajectory:

Q3 2025 revenue up 27% YoY to $10.4M, with improving profitability (net loss cut by half and positive adjusted EBITDA). Guidance raised to $40.5–$41M FY25 revenue (+20–22% YoY). International business up 230%, driving growth despite domestic softness.

Strategic Focus:

Accelerating international expansion (especially Europe’s prefilled syringe transition), advancing oncology infusion entry, expanding pharma collaborations, and improving manufacturing efficiency to sustain margins.

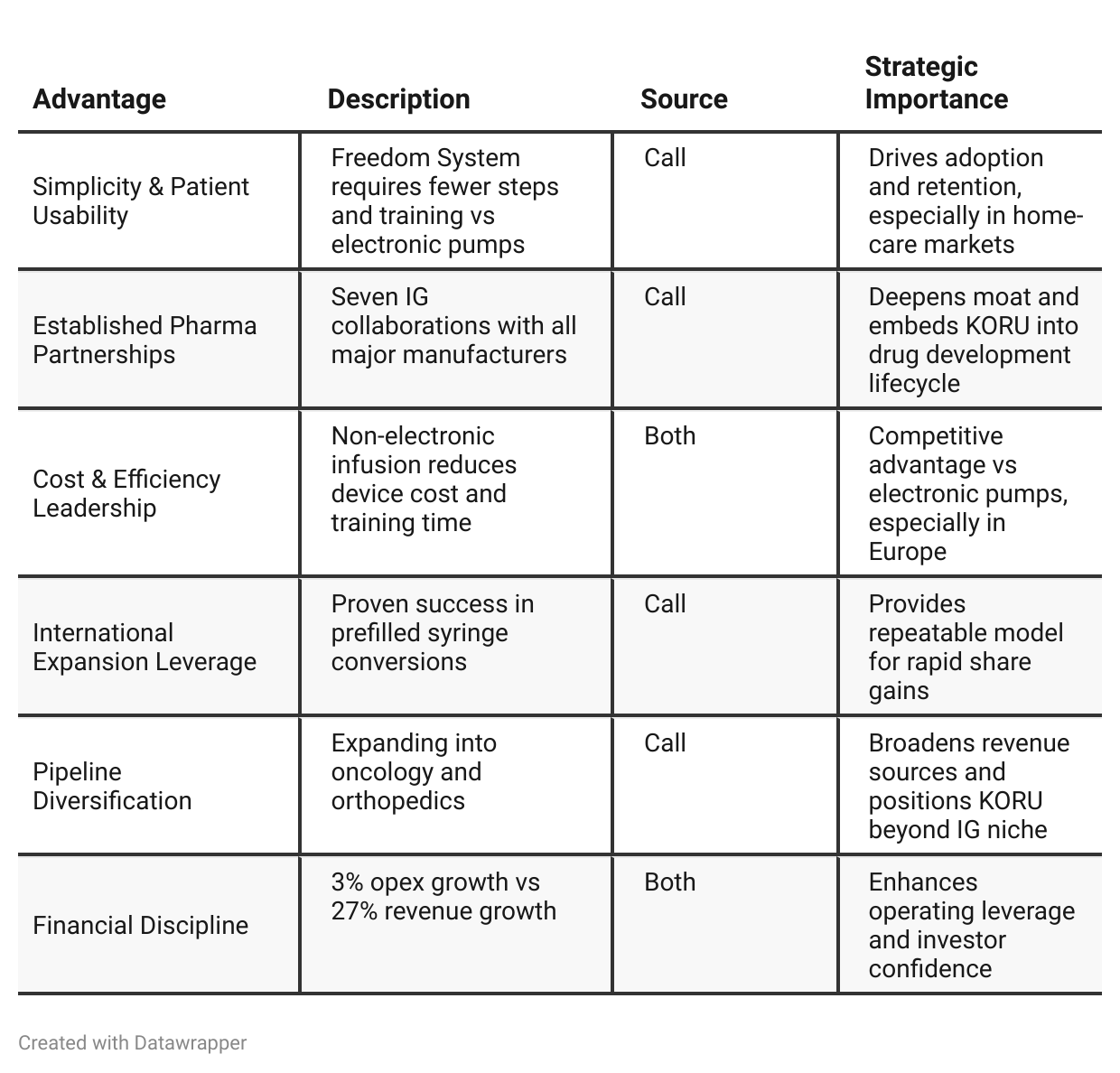

Competitive Advantage Insights

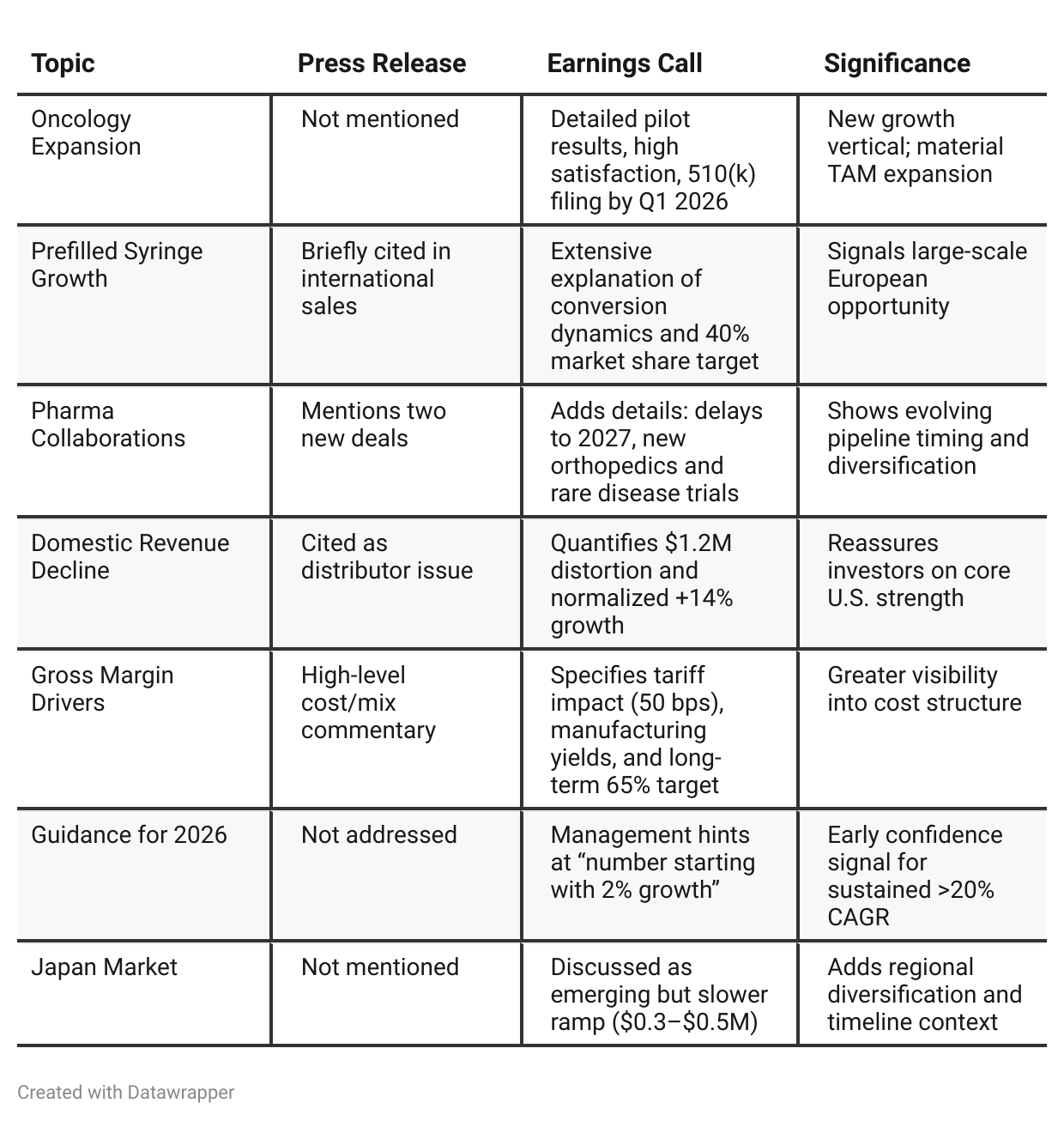

Press Release vs Call Transcript Comparison

Management emphasized operational discipline—operating expenses rose only 3% vs 27% revenue growth.

Pipeline breadth: seven active IG collaborations and nine non-IG projects position KORU as a platform company, not just a device maker.

Oncology validation offers entry into a $138M consumables market by 2030, a significant multiple to current revenue base.

SID (secondary immunodeficiency) trials by pharma partners could unlock reimbursement expansion in 2027—medium-term catalyst.

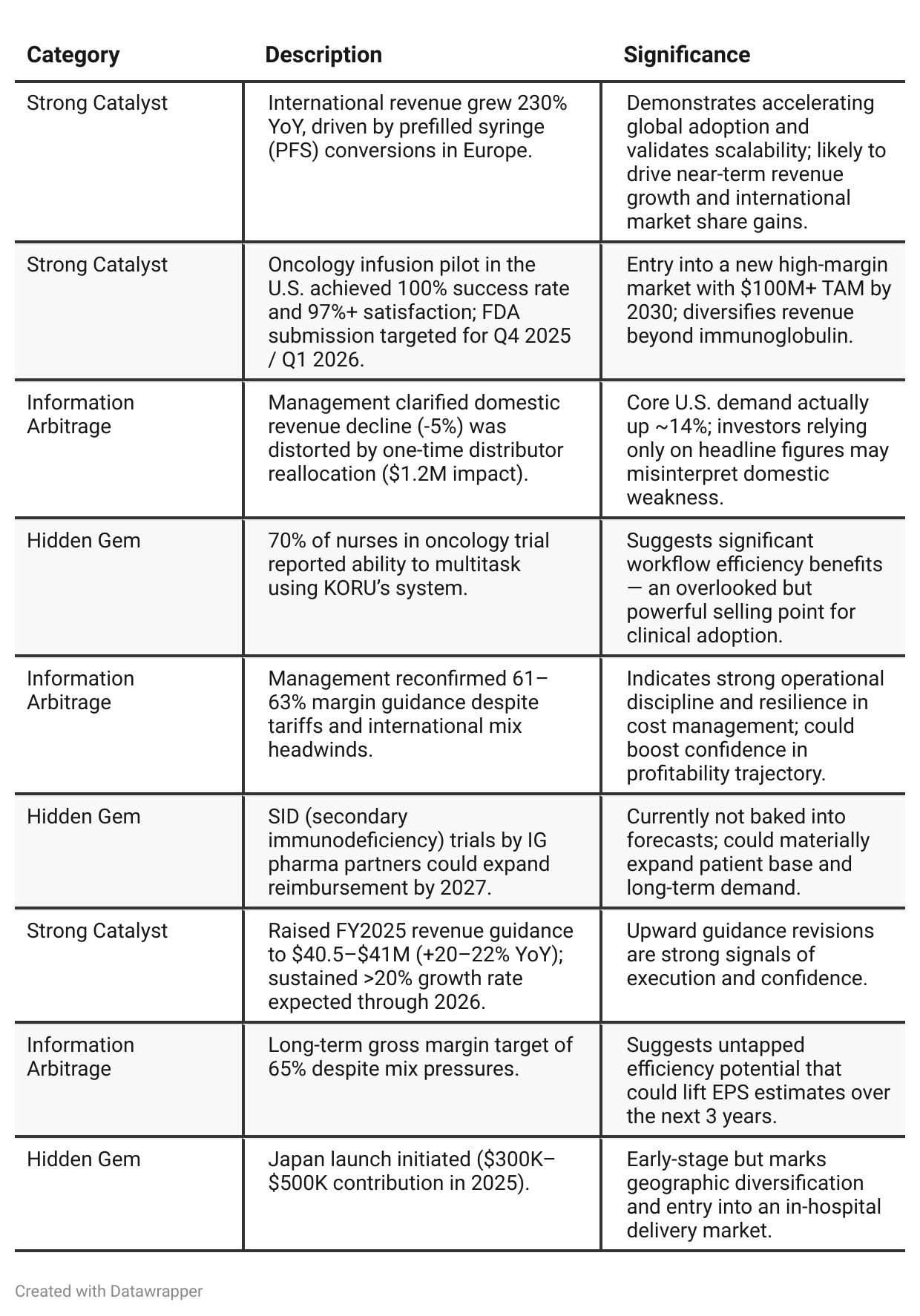

Positive Insights

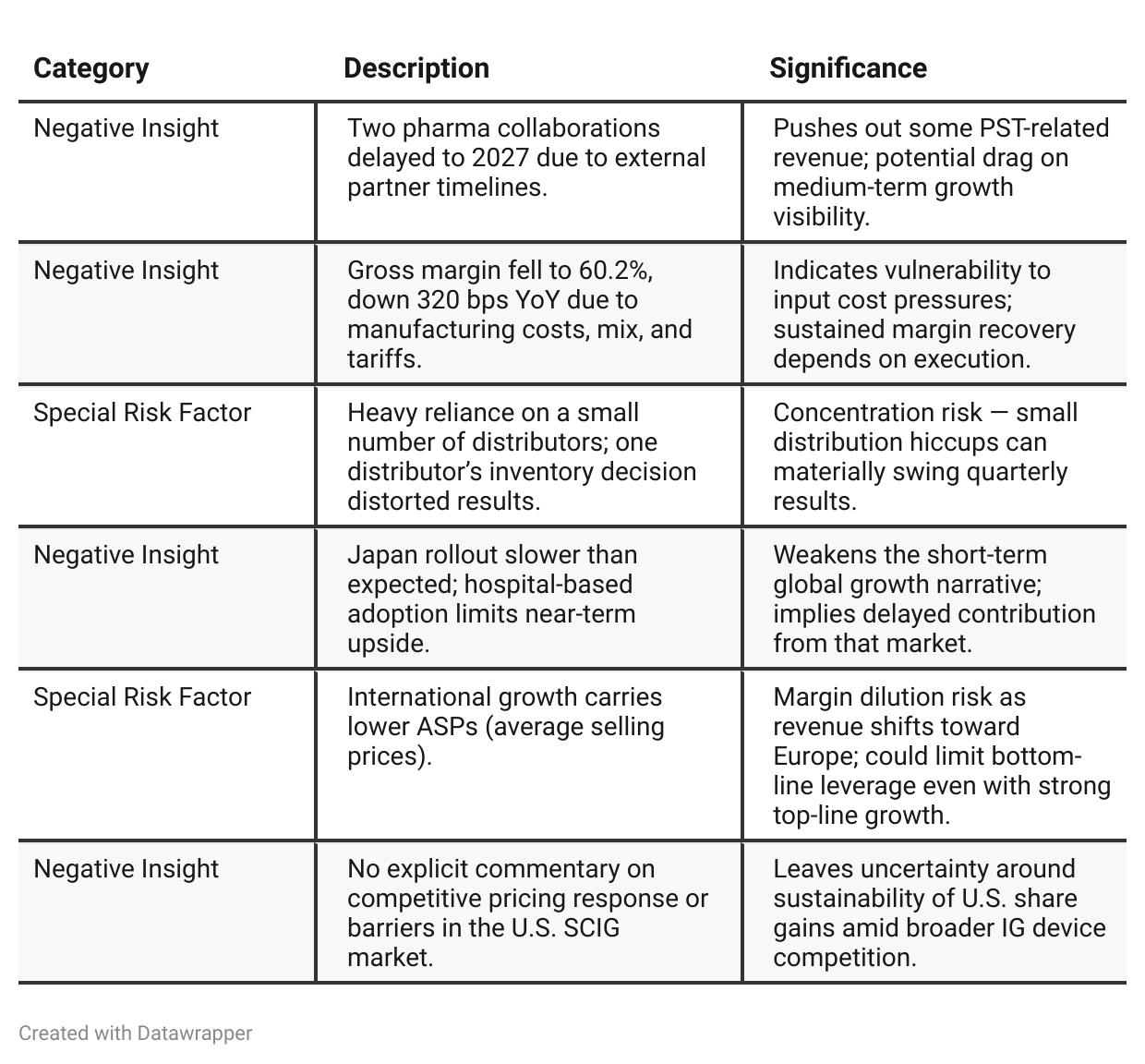

Negative Insights

Investor Underappreciation Signals

✅ Prefilled Syringe Conversion Momentum — European market shift from vials to prefilled syringes could double KORU’s international share; investors may be underestimating the speed and profitability of this transition until multiple countries convert.

✅ Oncology Infusion Market Entry — Successful U.S. pilot (100% safety, strong workflow efficiency) sets stage for FDA clearance in 2026; investors may overlook this new $100M+ TAM opportunity until regulatory approval is formalized.

✅ Normalized U.S. Growth Hidden by Distributor Mix — Reported -5% domestic revenue masks ~+14% true demand growth; investor models likely underestimate recurring U.S. momentum due to accounting timing.

✅ Margin Recovery Path to 65% — Despite mix and tariffs, management reaffirmed 61–63% FY margin and outlined multi-year efficiency programs; the market may still price KORU as a sub-60% GM company.

✅ SID Reimbursement Expansion Potential — Growing secondary immunodeficiency trials may unlock new patient segments by 2027; currently not reflected in guidance but could add multi-year tailwind.

Tariff Risk

The CFO explicitly cited “tariff impacts of approximately 50 basis points” on gross margin. Management reaffirmed its margin guidance despite these headwinds and indicated operational improvements and supplier management to offset costs.

No mention was made of supply chain relocation or pricing adjustments, implying absorption rather than pass-through of costs for now.

While current impact is modest, the company’s international scaling increases exposure to raw material or cross-border tariff volatility.

Mitigation Strategy: efficiency initiatives and higher-volume leverage; however, tariffs remain a low but persistent risk to achieving long-term 65% margins.

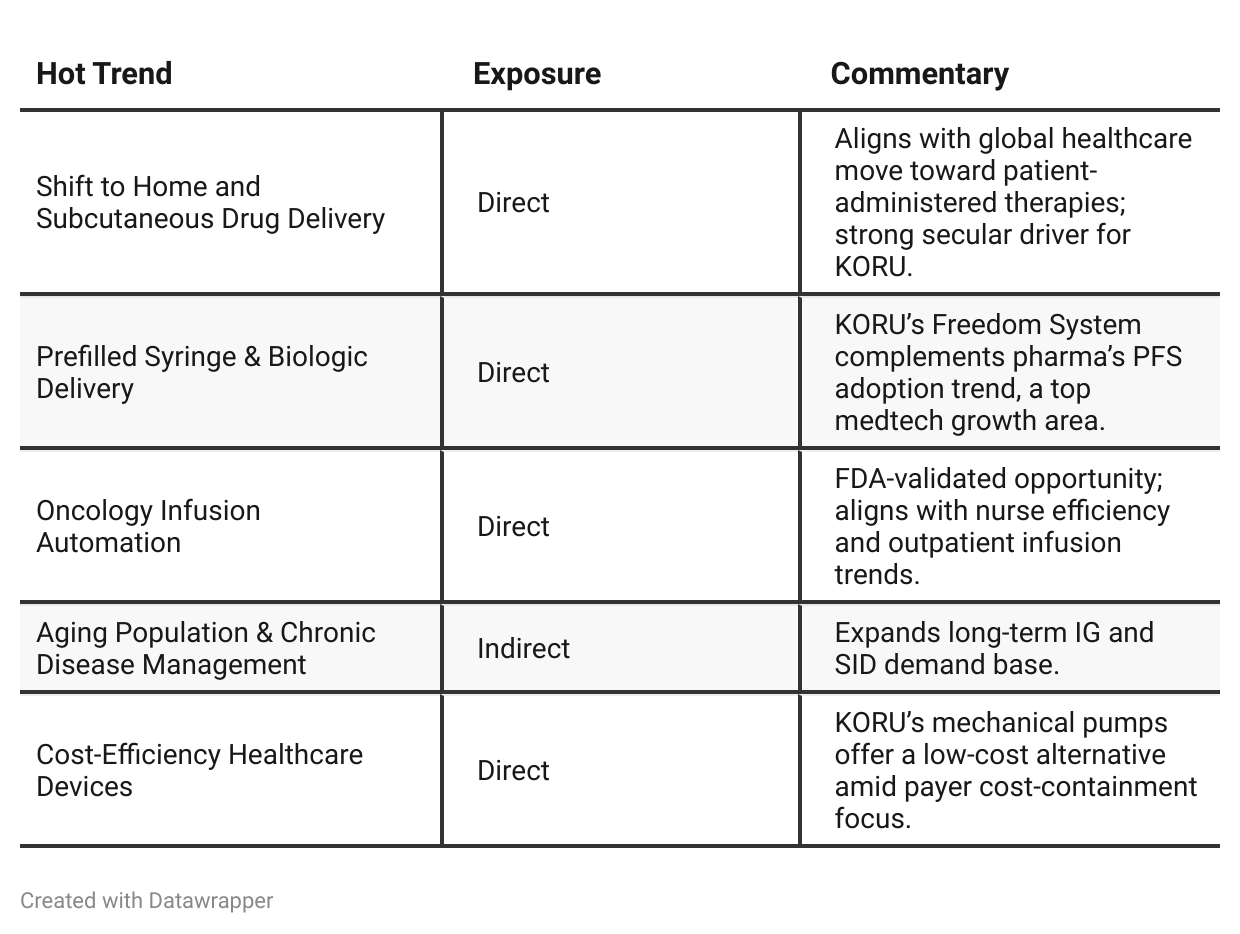

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025 Story:KORU Medical positioned itself as a steady, operationally disciplined company proving that it can scale profitably. Management emphasized efficiency, cost control, and building the foundation for consistent growth — a “steady-as-she-goes” quarter. The tone was pragmatic: focused on sustaining margins and incremental progress in partnerships and international entry.

Q3 2025 Story:

The narrative evolves into one of momentum, diversification, and confidence. Management communicates that the foundation laid in Q2 has now yielded tangible expansion — record revenues, successful oncology trials, new partnerships, and raised guidance. The messaging has broadened from “stability and proof” to “execution and expansion.”

Year-over-year comparison

Q3 2024 Story:

KORU was a profitable-growth-in-progress company, focused on proving operational strength and funding itself. The leadership tone was confident yet pragmatic — focused on achieving breakeven, deepening core SCIG penetration, and building a pipeline foundation for Vision 2026. New markets like Japan were future-oriented goals, not yet revenue drivers.

Q3 2025 Story:

KORU has transformed into a scaling growth platform with expanding global reach and diversification into new therapeutic areas. Management now speaks as an operator of a multi-segment platform, not a niche SCIG device maker. The narrative centers on execution at scale, international leadership, and the potential for structural market expansion via oncology and SID opportunities.

Final Takeaway

KORU Medical Systems (KRMD) is in a growth acceleration phase, focusing on expanding global SCIG adoption, launching into oncology infusion, and diversifying its pharma-collaboration pipeline. While margin compression and pipeline delays pose near-term noise, strong execution, self-funded growth, and disciplined cost control provide a compelling setup for sustained 20%+ top-line growth. Execution on oncology commercialization, European PFS conversions, and 65% margin trajectory will be critical for valuation expansion.

Verdict: BUY, with potential upside from underestimated oncology and international catalysts.