KORU Medical Systems, Inc. (NASDAQ: KRMD) – Q2 2025 Earnings

KORU Medical Systems, Inc. (NASDAQ: KRMD) – Q2 2025 Earnings

Earnings Release Date: Aug. 6, 2025

Stock Price: $3.28

Market Cap: $151.5 million

Q2 2025 sales of $10.2 million vs $8.4 million in the prior year

Q2 2025 EPS of ($0.00) vs ($0.02) in the prior year

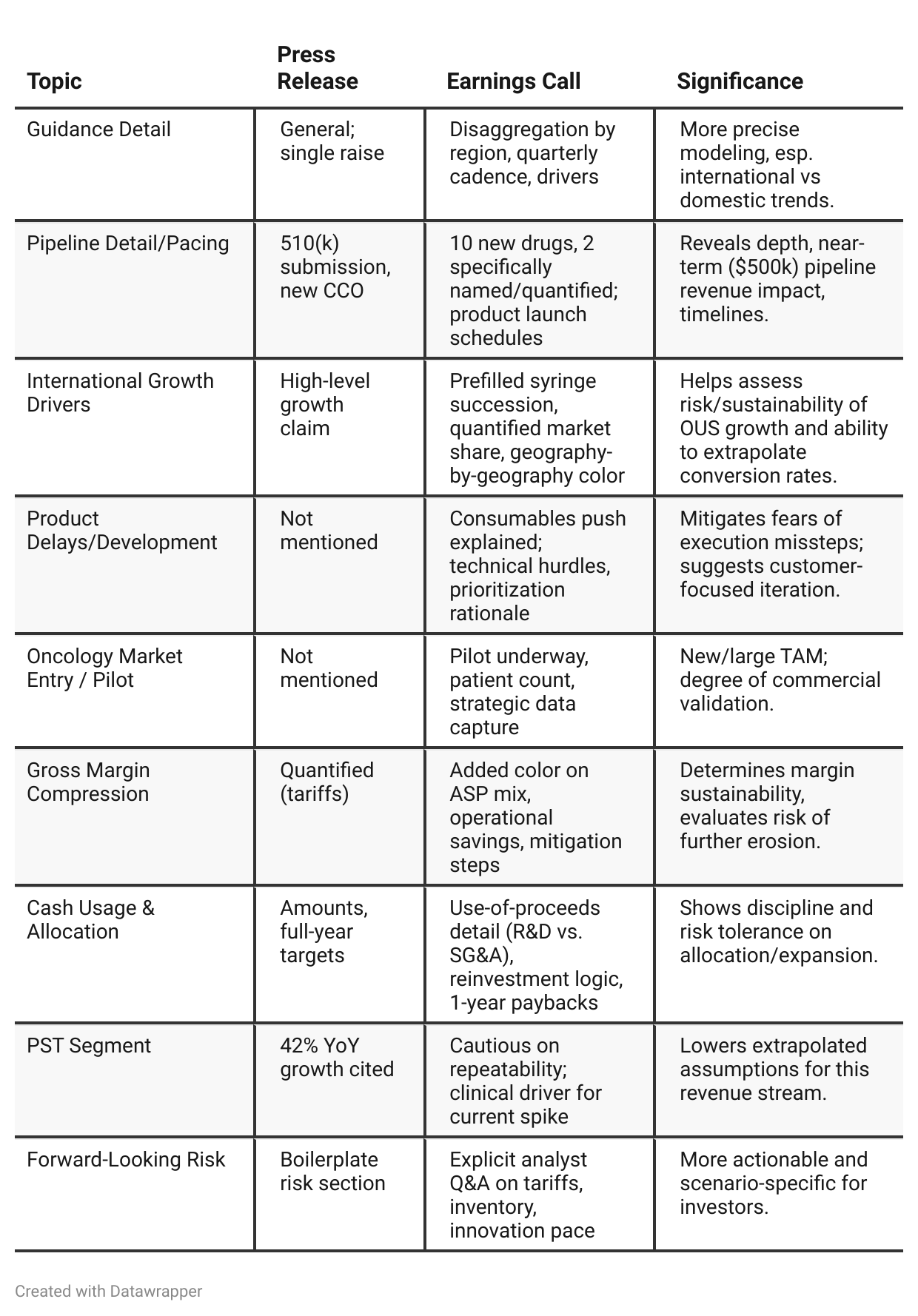

Press Release vs Call Transcript Comparison

Pipeline Transparency: The call transcript provides a much clearer window on near-term pipeline contributions (by drug and geography), versus vague “expansion” in the press release.

Segment Granularity: The press release aggregates domestic/international, while the call breaks down the mechanics of growth in each (patient starts, share gains, market conversions), as well as headwinds.

Execution Evidence: Management discusses learning from customer feedback, not rushing product launches, and prioritizing developments strategically—indicative of discipline and a healthily cautious approach.

Competitive Dynamics: The European conversion is still early-stage; the call makes clear that wins happen on a market-by-market basis and require time, despite headline growth rates.

Cash Flow Management: Management’s answers suggest continued focus on sustainability, not just one-off cost discipline post-infrastructure investment. Investors should care about this as the balance between growth and cash preservation will impact valuation and dilution risk.

Risks to Model: PST revenue is lumpy, near-term US revenue is subject to distributor swings, and gross margin relies on continued scale (future price/mix risks).

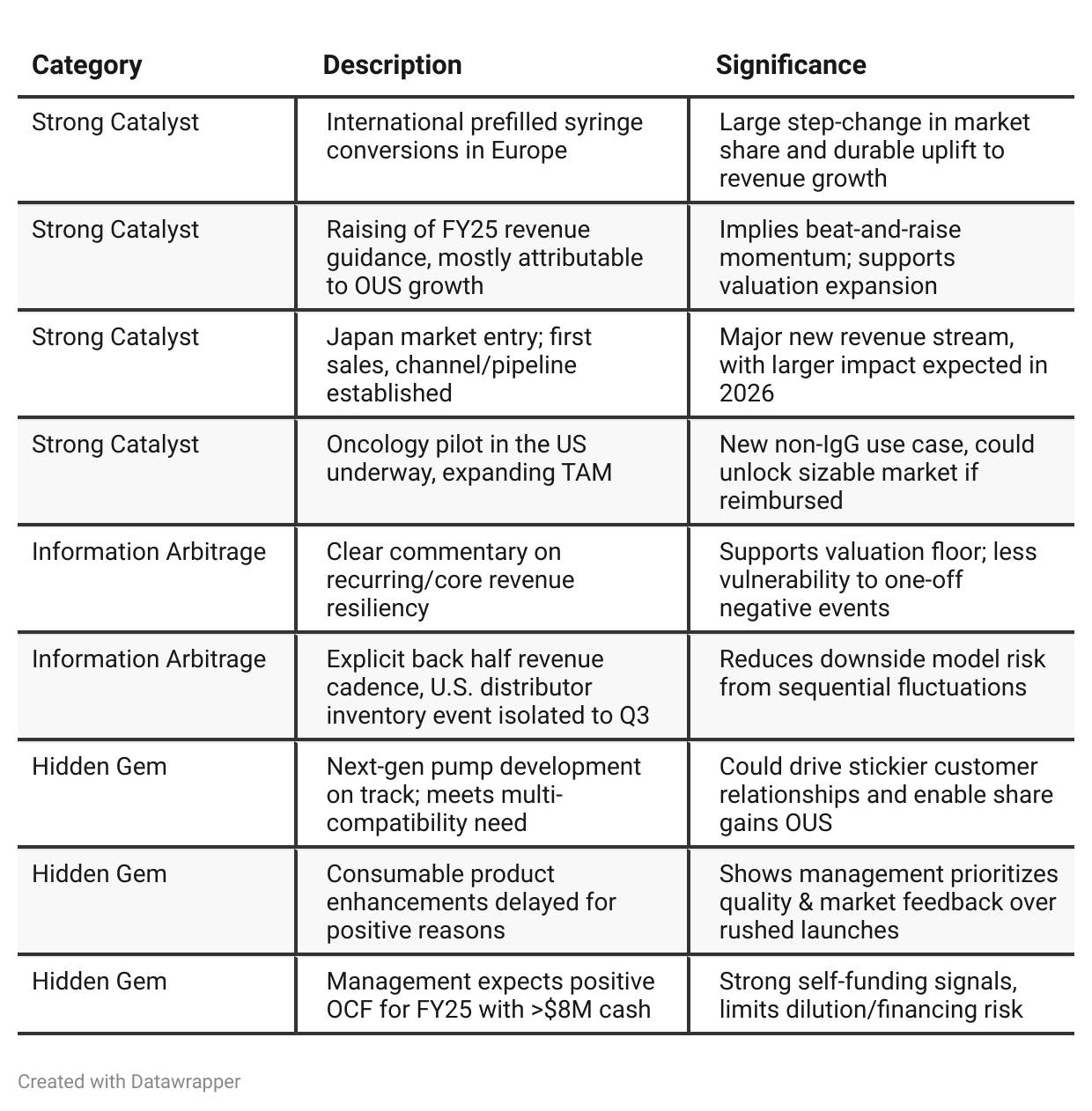

Positive Insights

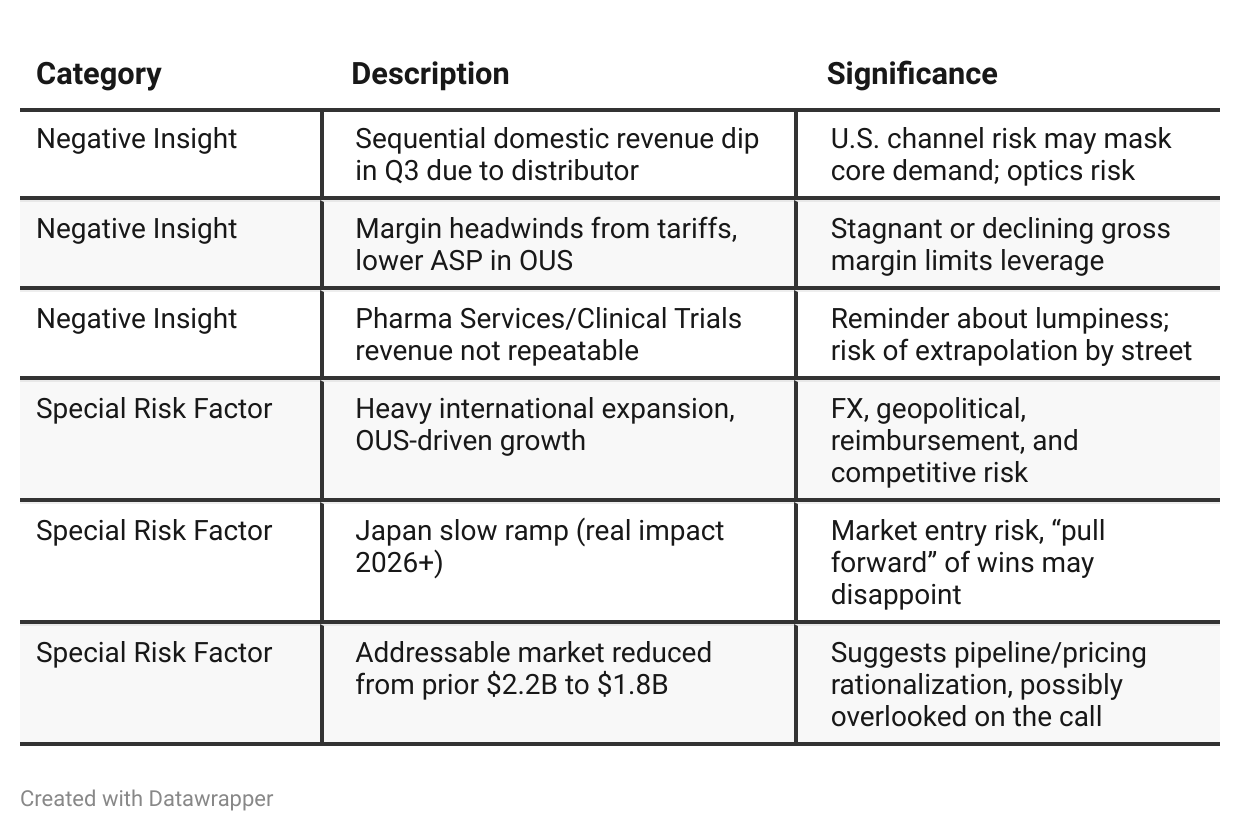

Negative Insights

Tariff Risk

Tariffs are cited as a 90bps annual gross margin headwind (~2% effect per order).

Most impact comes via a major third-party contract manufacturer; company has done a granular bill-of-materials review to isolate impacts.

Mitigation actions: Operational efficiency programs, vendor rebates, scaling efficiencies as sales grow. Ongoing work to control and offset costs.

Forward impact: Guidance maintains gross margin in the low 60% range (61–63%), suggesting management confidence.

Competitive risk: No direct mention of being at a disadvantage to peers, but ongoing tariff risk is a factor in the margin outlook and international competitiveness.

Innovation impact: No indication that tariffs are slowing R&D or product innovation; company is prioritizing high-ROI product launches and learning from customer feedback.

Outlook: Tariffs are manageable under current strategy, but persistent monitoring is advised as policy, supply chain, or volume dynamics may change.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: KORU Medical exudes optimism as a scale-up, building confidence in a robust and predictable recurring revenue core, rapid international penetration, and an evolving product pipeline. Management focuses on diversification—both through traditional pharma partnerships and self-initiated label pursuits—and signals operational discipline as a foundation for margin and cash flow improvement. The company sets the stage for a major year, highlighting key markets (Japan, prefilled syringe wins in Europe), new drugs, and a culture responsive to both partnerships and customer needs.Q2 2025: The company’s narrative matures from ambitious aspiration to tangible, milestone-driven momentum. Surpassing $10M in quarterly sales is celebrated as a watershed, while the raised guidance is backed by explicit, data-driven OUS successes. Management’s tone is even more confident, with detailed breakdowns on why, where, and how growth is happening—especially clarifying the transitory nature of US distributor inventory impacts and the durability of international market gains. New developments—advancement in the oncology pilot, confirmed initial sales in Japan, and pipeline execution (with deliberate product iteration and customer-centric thinking)—emphasize disciplined, sustainable progress. The company positions itself not just as a lucky beneficiary of market tailwinds, but as a savvy, execution-focused leader adapting to opportunities and risks in real-time.

Year-over-year comparison

Q2 2024: KORU is building momentum as an emerging global player in subcutaneous drug delivery, emphasizing a targeted strategy: broadening international reach (notably, Japan entry), expanding the core recurring SCIg patient base, and developing novel therapy partnerships. The company is positively evolving its operational structure and focusing on cash flow discipline and execution to achieve longer-term “Vision 2026.”

Q2 2025: The narrative has matured from foundation-building to scaling with confidence. KORU celebrates a revenue milestone, raises guidance thanks to durable international/OUS growth (most notably via prefilled syringe conversion), and provides granular transparency about regionally and timing-driven revenue and margin drivers. They are executing against a broadened product/drug pipeline, leveraging customer feedback for product refinement, and demonstrating operational leverage. The company positions itself as a disciplined, execution-focused innovator in a strong macro and market environment, with a much clearer line-of-sight to sustained, profitable growth.

Final Takeaway

KORU Medical Systems is in a high-growth phase, propelled by international expansion (especially prefilled syringe adoption and entry into Japan), pipeline innovation, and positive cash generation. While new products and geographies offer clear upside catalysts, sustaining margins amid tariff and ASP headwinds will be crucial. Investors should focus on management’s execution around OUS expansion, new product clearances, and the ability to maintain gross margins despite tariff and FX pressure. Verdict: Buy with an eye on margin and channel risks; the story offers multi-year upside if execution continues as guided.