Kimball Electronics, Inc. (NASDAQ: KE) – Q1 2026 Earnings

Kimball Electronics, Inc. (NASDAQ: KE) – Q1 2026 Earnings

Earnings Release Date: Nov. 05, 2025

Stock Price: $28.79

Market Cap: $708.2 million

Q1 2026 sales of $365.6 million vs $374.3 million in the prior year

Q1 2026 EPS of $0.40 vs $0.12 in the prior year

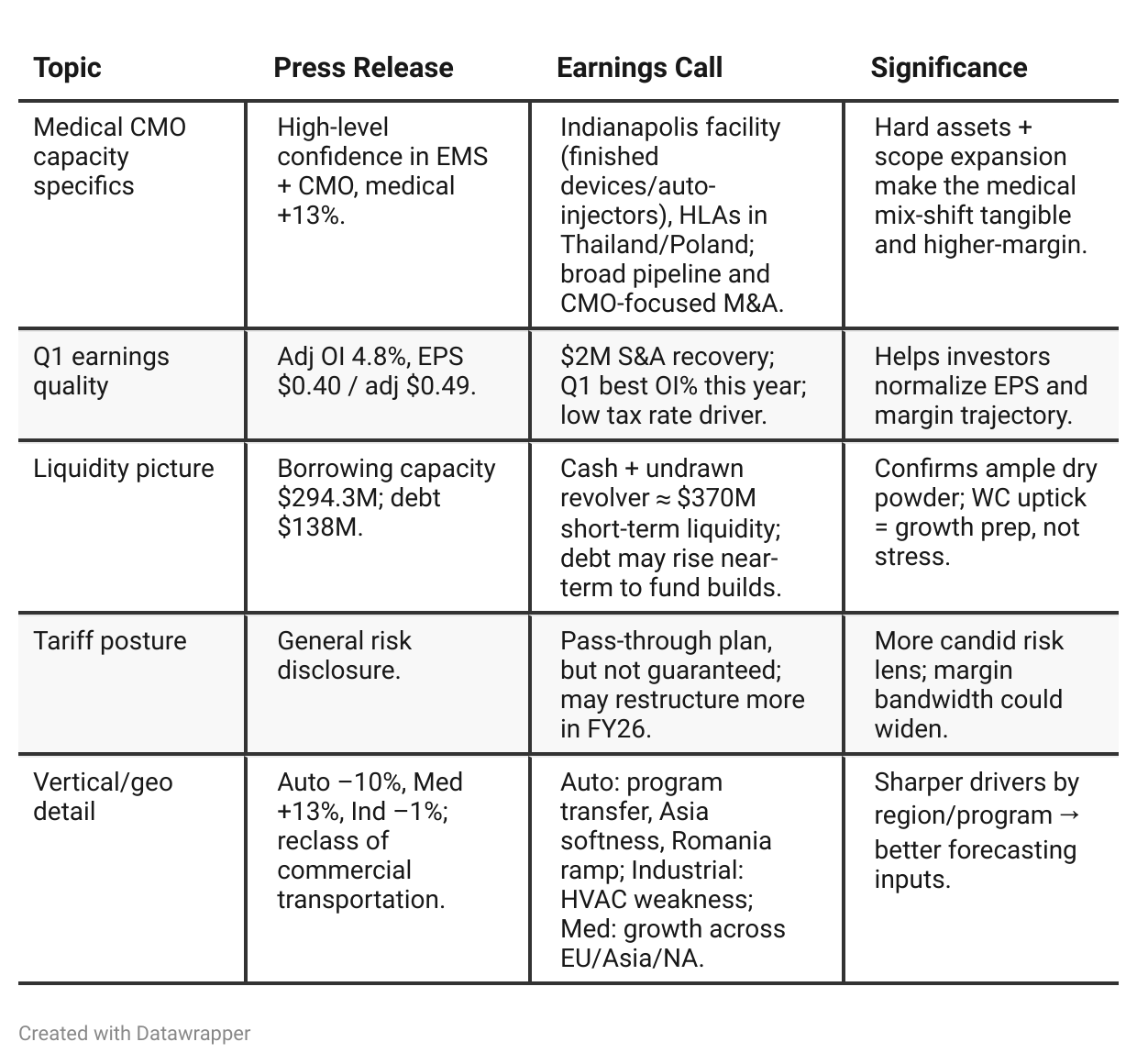

Press Release vs Call Transcript Comparison

Capital allocation tone: PR shows buybacks and deleveraging; call stresses disciplined M&A (won’t issue equity; will keep balance sheet strong), hinting bias to tuck-ins that lift EBITDA in medical CMO.

FY27 setup: PR points to “return to profitable topline growth next year”; call repeatedly frames FY27 re-acceleration (and no deterioration in FY27 EBITDA).

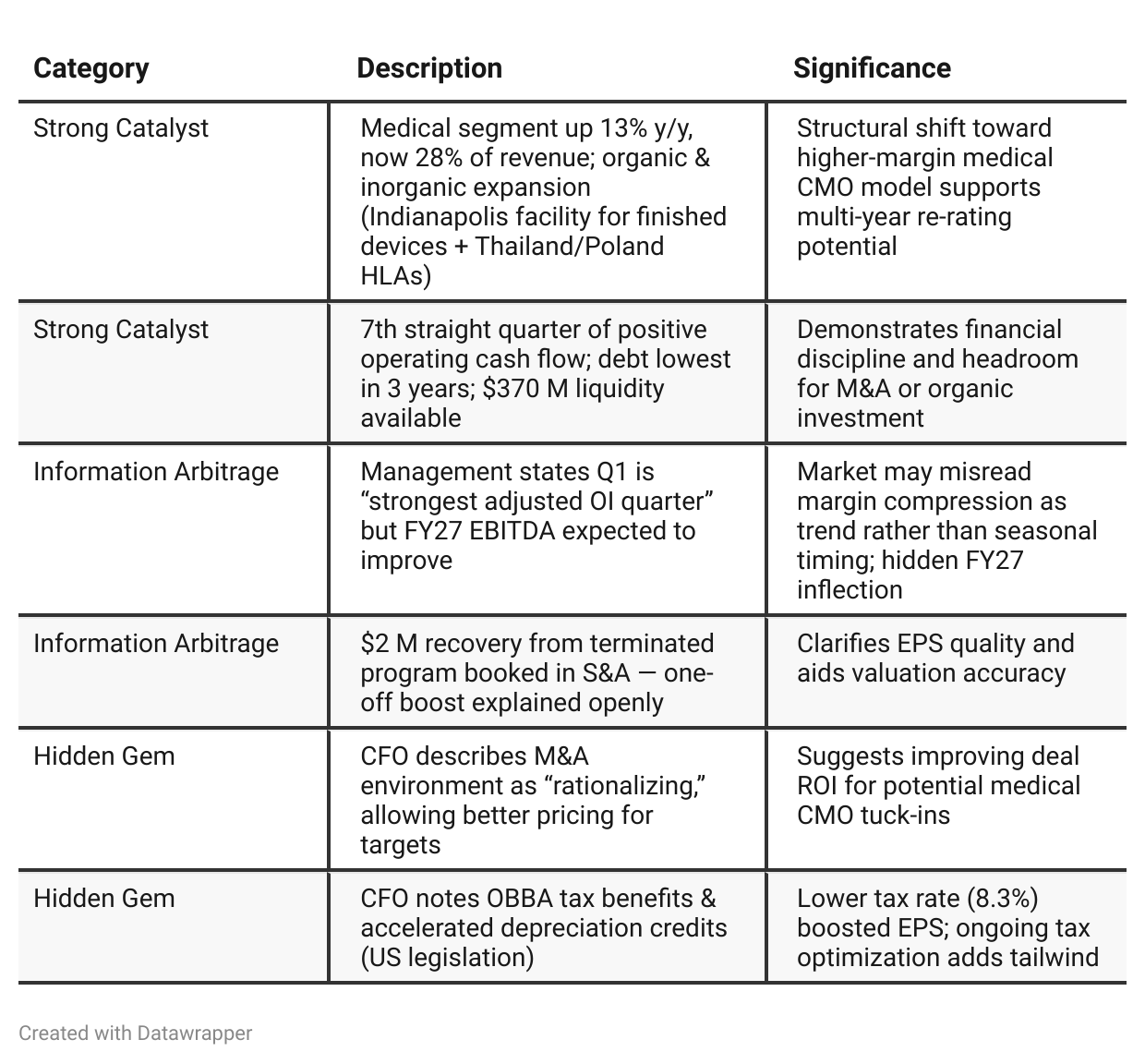

Positive Insights

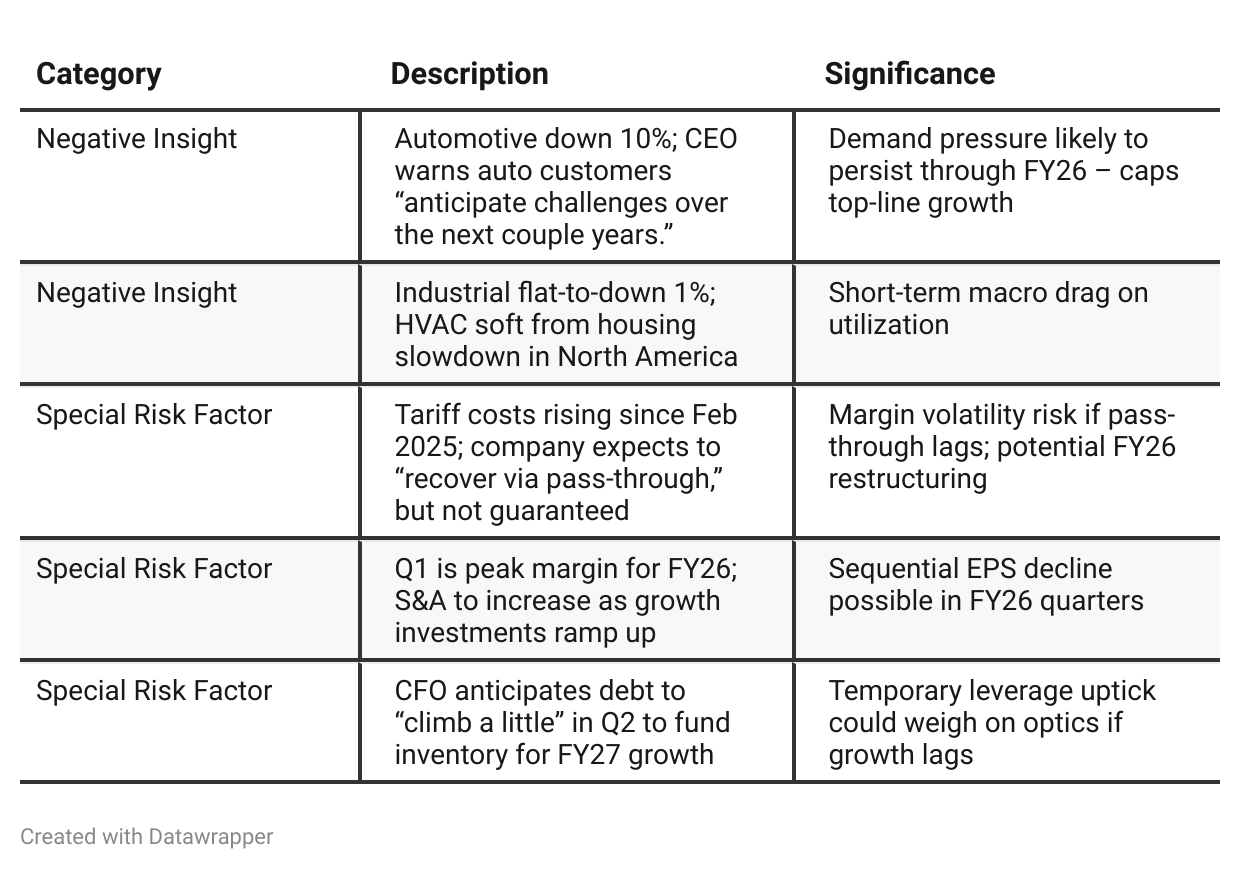

Negative Insights

Tariff Risk

Management explicitly addressed the U.S. tariff policy changes effective February 2025 and their impact:

Tariffs are “evolving rapidly,” affecting consumer demand and input costs.

Company expects to recover tariff costs via customer pass-throughs, but acknowledged partial recovery risk.

Plans to incur additional restructuring costs in FY26 to offset tariff pressures.

Active dialogue with manufacturing partners and lawmakers to mitigate impact.

Impact Summary: Tariffs may moderately weigh on FY26 margins, but the company’s multi-region footprint and pricing discipline reduce long-term exposure. Management’s candor on this topic builds credibility — they are proactively managing rather than downplaying the issue.

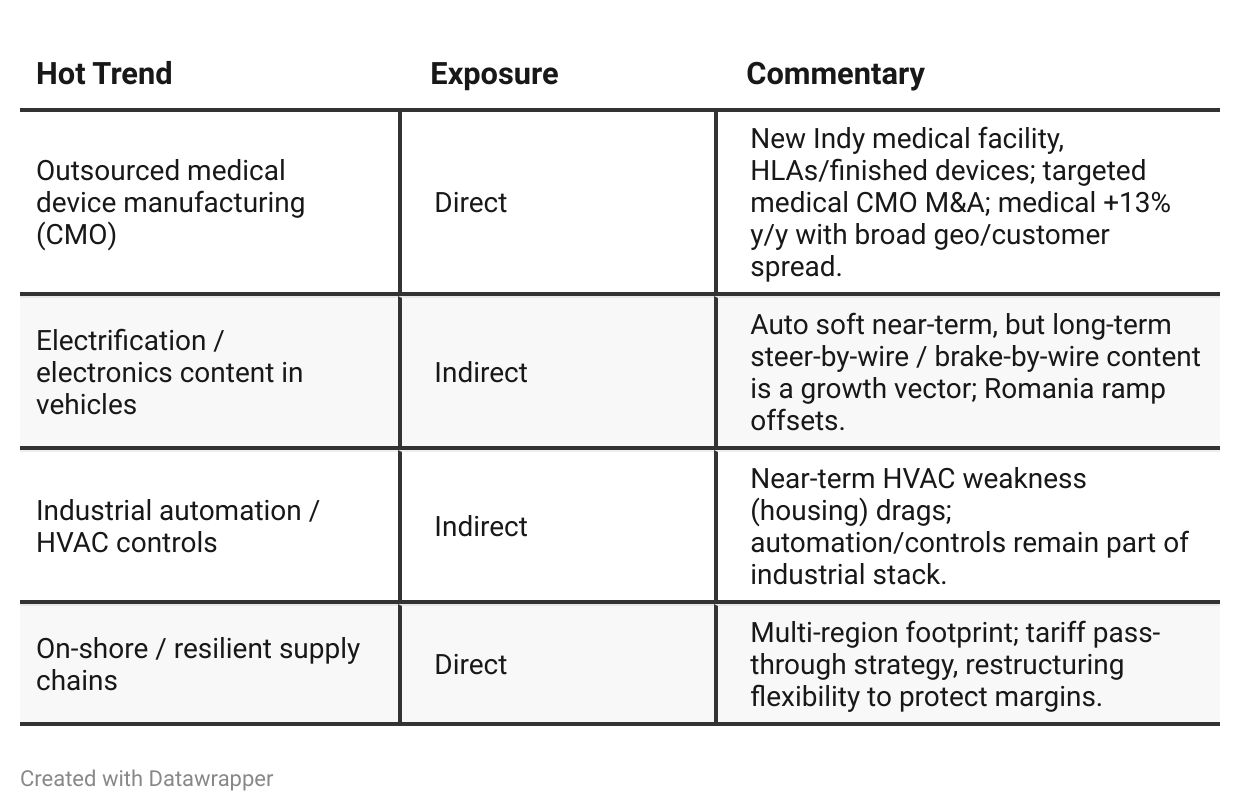

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q4 FY2025:KE “cleans the base” — restructures cost, exits weak pieces, secures record cash generation, and plants the medical CMO flag (Indy facility, HLA/finished device capability). FY26 is a transition, FY27 the re-acceleration.

Q1 FY2026:

KE “loads the spring” — confirms medical +13% and 28% mix, sets Q1 as peak OI% with planned S&A investment, warns tariff pass-through risk and housing softness, and explicitly ties a near-term WC build to FY27 ramps. Guidance reiterated; FY27 EBITDA expected to improve.

Year-over-year comparison

Q1 FY2025 Call Narrative:

Kimball Electronics was stabilizing its foundation — cutting costs, reducing debt, and digesting restructuring. Medical was emerging as the bright spot, but management remained cautious about macro softness and tariff complexity. The tone was one of recovery and operational repair.

Q1 FY2026 Call Narrative:

The story matures into a measured growth cycle. Management now speaks confidently about medical CMO traction (+13%), global diversification, and early revenue lift from new facilities. They frame FY26 as the setup year and FY27 as the acceleration year. Risks are more explicit (tariffs, S&A growth), but transparency and operational control instill credibility. The tone has shifted from defensive to constructive optimism — a pivot from repair to scale.

Final Takeaway

Kimball Electronics (KE) is in a transition phase, shifting from a low-margin EMS operator to a higher-value medical contract manufacturer. FY26 is a bridge year marked by strategic investment and tariff costs, but strong cash generation, a clean balance sheet, and growing medical visibility set up FY27 as a return-to-growth story. Execution on medical ramp, tariff pass-through, and M&A discipline will define valuation trajectory.

Verdict: BUY — with potential upside driven by margin expansion and medical CMO multiple re-rating in FY27.