Kimball Electronics (NASDAQ: KE) – Q4 2025 Earnings

Kimball Electronics (NASDAQ: KE) – Q4 2025 Earnings

Earnings Release Date: Aug. 13, 2025

Stock Price: $20.97

Market Cap: $514.9 million

Q4 2025 sales of $380.5 million vs $430.2 million in the prior year

Q4 2025 adjusted EPS of $0.34 vs $0.38 in the prior year

Full year sales of $1.5 billion vs $1.7 billion in the prior year

Full year EPS of $1.12 vs $1.64 in the prior year

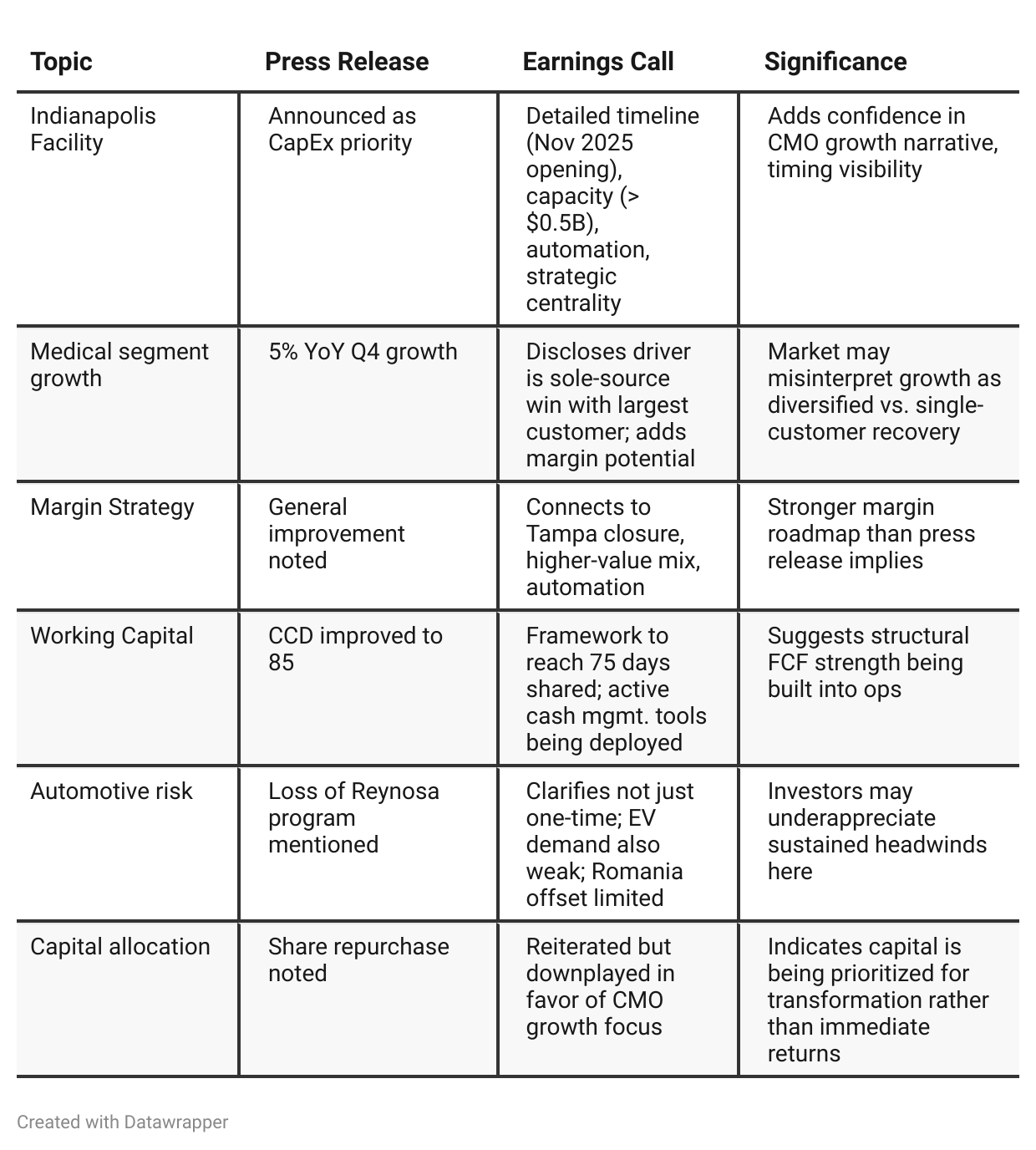

Press Release vs Call Transcript Comparison

While the press release presents a clean financial summary and confirms Kimball’s transformation trajectory, the earnings call delivers the real substance for investors: a clearer view into medical revenue concentration, margin leverage, and capital deployment strategy.

The transition to a medical CMO model is deeper and more urgent than the press release conveys, supported by strategic hires, automation, and a landmark customer win. However, the automotive headwinds and FY26 revenue contraction temper near-term enthusiasm. The divergence between the documents highlights the importance of the call for understanding quality of growth—not just its appearance.

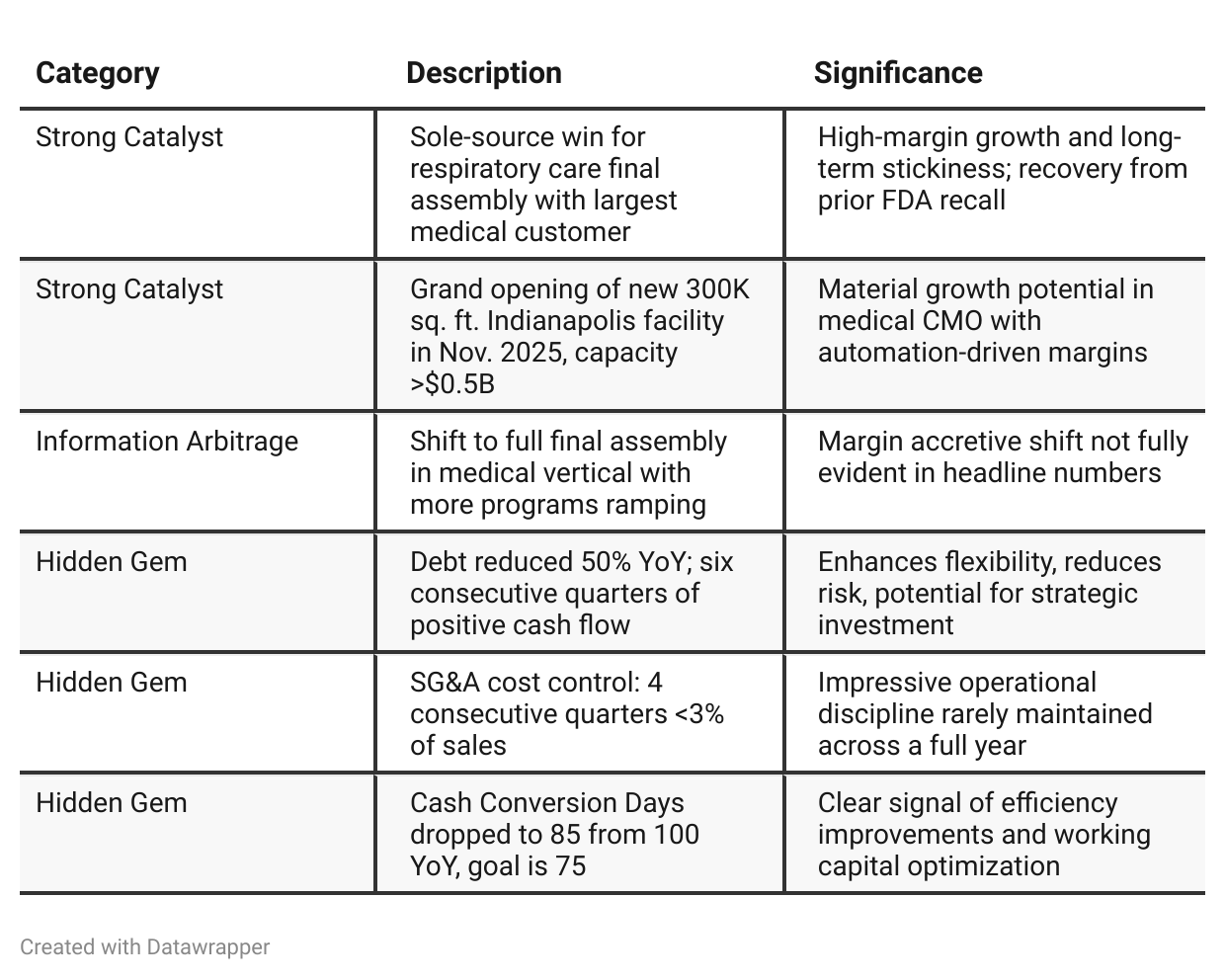

Positive Insights

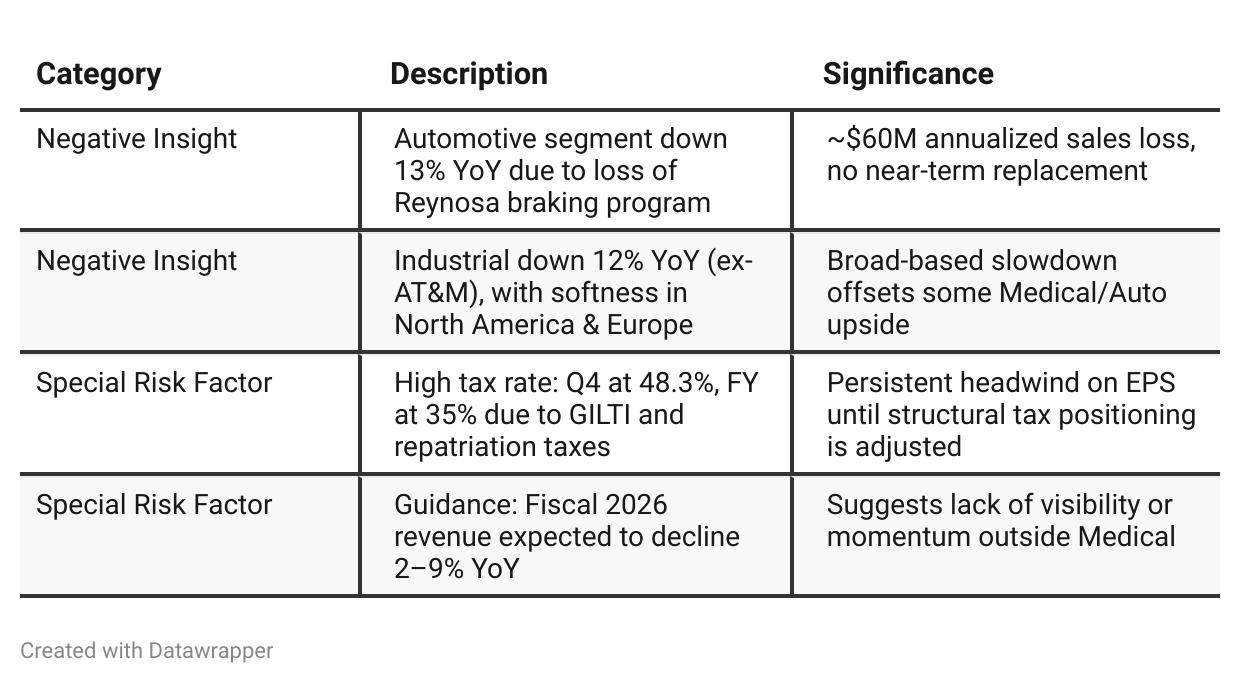

Negative Insights

Tariff Risk

Tariffs were discussed briefly. Management indicated:

Minimal direct exposure: KE is not typically the importer of record, shielding it from many direct tariff impacts.

Pass-through structure: Tariffs are passed through to customers, limiting margin impact.

Global footprint leveraged: Customers are given options to shift production across KE’s international facilities depending on tariff environment.

Proactive flexibility: KE qualifies alternative supply sources and adjusts sourcing dynamically.

Conclusion: Tariffs currently pose a low direct threat due to structure and global footprint, though KE remains watchful and flexible.

Previous Earnings Call

Quarter-over-quarter comparison

Kimball Electronics transitioned from stabilization to strategic reorientation. In Q3, the story was about weathering headwinds, managing cost and liquidity, and laying groundwork for medical growth.

By Q4, the company demonstrated traction: cash conversion improved materially, margins rose sequentially, and a high-profile sole-source win signaled execution in medical CMO. Management acknowledged that the company is in a “transition year” for FY26 but positioned that as a deliberate reset, not a retreat.

The message shifted from tactical survival to long-term scaling of a more profitable, focused business model.Year-over-year comparison

Kimball Electronics has shifted from a transitional, post-divestiture stabilization phase in Q4 2024 to a focused growth posture centered on medical contract manufacturing by Q4 2025.

In 2024, the company was digesting a challenging EMS environment, working through program-specific headwinds (notably an FDA recall and OEM brake program exit), and reorienting its cost base. By 2025, the tone turned confident—backed by record cash flow, materially reduced debt, and a clear capital allocation strategy toward medical vertical expansion.

The Indianapolis CMO facility and sole-source wins with Philips exemplify this shift from defensive margin protection to proactive growth building. Automotive remains under pressure, but Medical has become the centerpiece of Kimball's future.

Final Takeaway

Kimball Electronics is in a transition phase, focusing on expanding its high-margin Medical CMO platform while navigating Automotive and Industrial softness.

Despite near-term revenue headwinds, margin control, debt reduction, and strong cash flow underpin management’s confidence. Execution on the medical facility ramp, customer diversification, and margin leverage from increased utilization will be critical.

Verdict: Hold, with upside potential as FY27 growth visibility improves.