Intelligent Protection Management Corp. (NASDAQ: IPM) – Q3 2025 Earnings

Intelligent Protection Management Corp. (NASDAQ: IPM) – Q3 2025 Earnings

Press release and earnings call link

Earnings Release Date: Nov. 12, 2025

Stock Price: $1.97

Market Cap: $18.1 million

Q3 2025 sales of $6.2 million vs $5.9 million in the prior year

Q3 2025 EPS of ($0.05) vs ($0.09) in the prior year

Company: Intelligent Protection Management Corp. (NASDAQ: IPM)

Industry: Managed Technology Services — specializing in enterprise cybersecurity and cloud infrastructure.

Business Model: Provides managed IT services, private cloud hosting, data protection, and disaster recovery solutions. Revenue comes from managed IT, procurement, professional services, and subscriptions.

Customer Base: Primarily U.S. enterprise and commercial clients across legal, healthcare, and finance — highly regulated sectors that require certified, secure IT environments.

Market Position: Emerging player positioning itself as a “white-glove” cybersecurity and cloud provider, emphasizing personalized support and U.S.-based service teams.

Financial Trajectory: Following the January 2025 acquisition of Newtek Technology Solutions (NTS), IPM has seen rapid top-line growth (+9% sequentially in Q3) but remains operating at a loss as integration continues.

Strategic Focus: Integration of NTS, expanding cross-selling of ManyCam and new AI-powered offerings, enhancing cybersecurity capabilities, and pursuing bolt-on acquisitions to grow managed device count and recurring revenue.

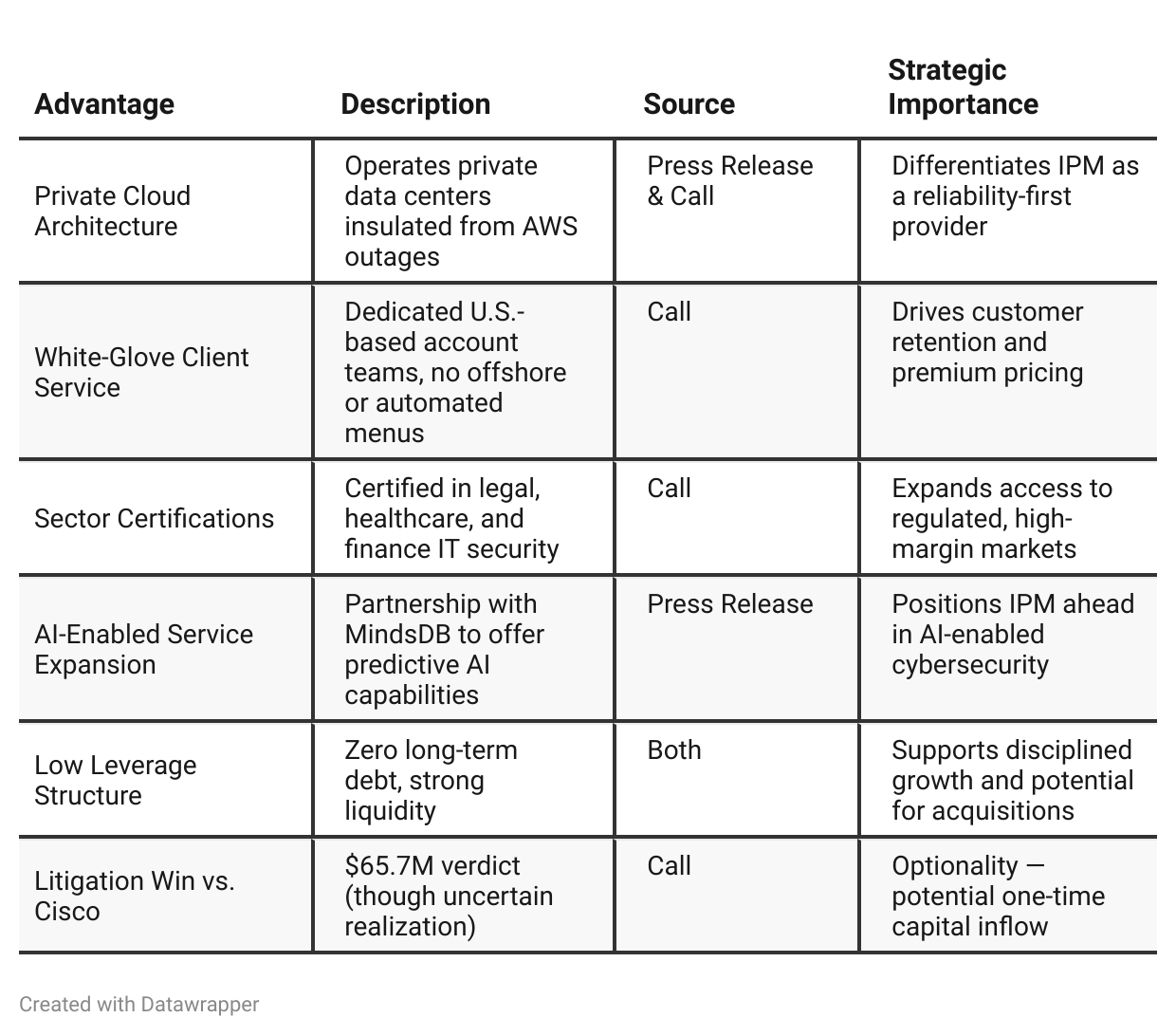

Competitive Advantage Insights

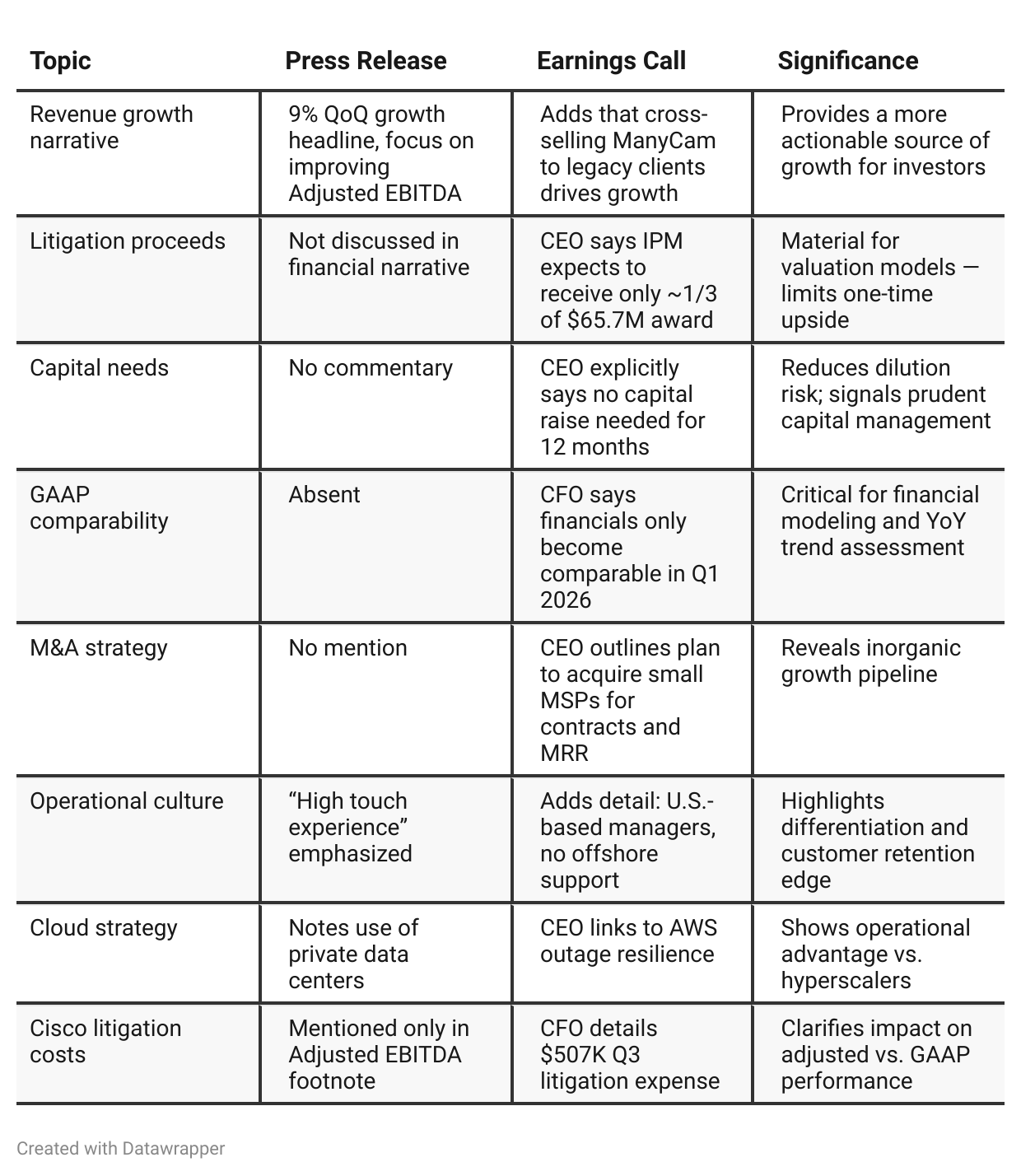

Press Release vs Call Transcript Comparison

The call is more strategic, focusing on culture, customer service differentiation, and integration efficiency.

The press release is more financial and promotional, built for headline investors and compliance, not insight.

The call’s Q&A section introduces the first acquisition roadmap — small-scale, accretive roll-ups to grow device count.

Deferred revenue ($3.5M) represents meaningful visibility into future quarters — but only mentioned numerically, not discussed strategically.

Management repeatedly stresses “white-glove” client support, implying premium pricing potential and stickier customers.

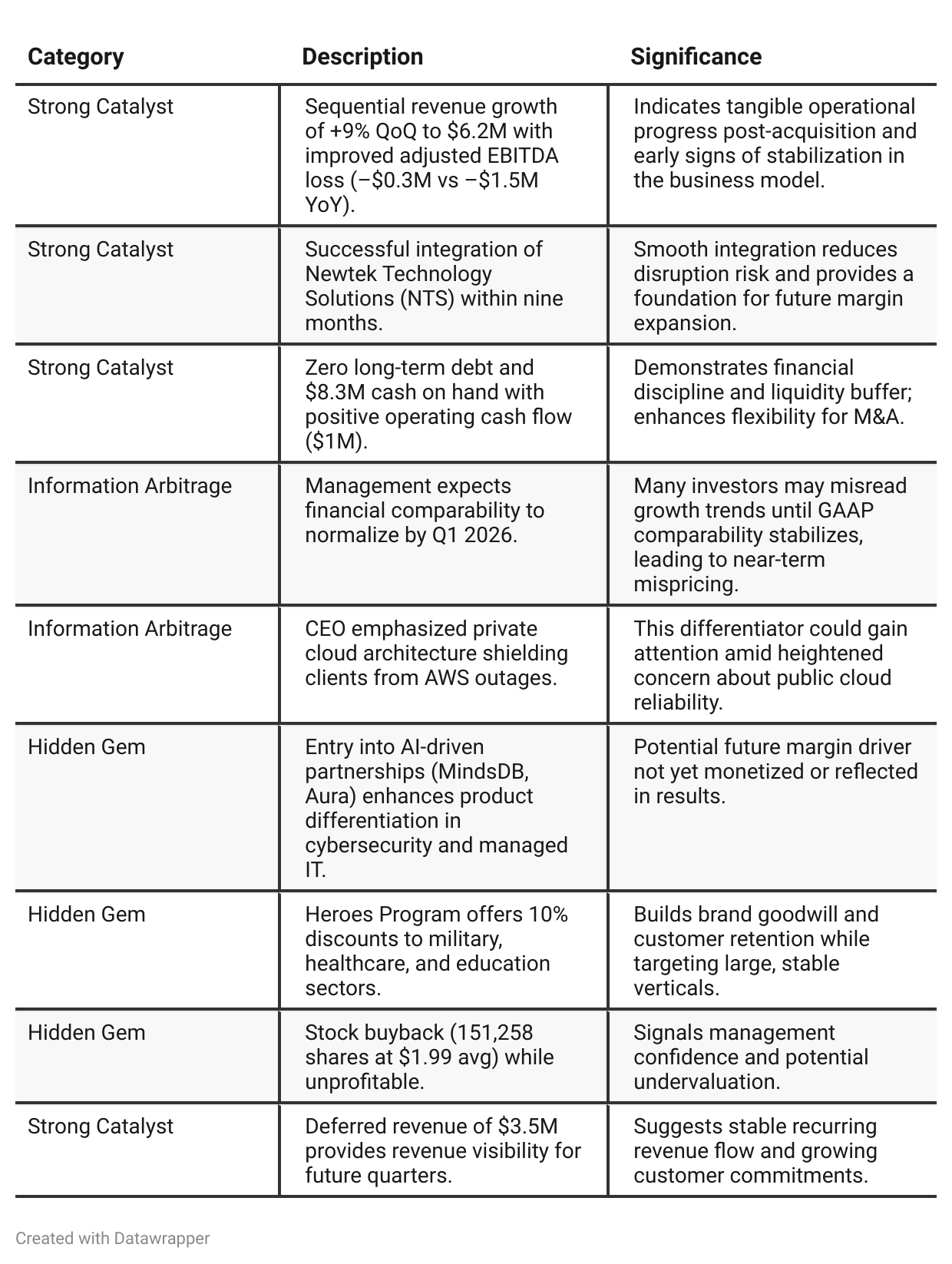

Positive Insights

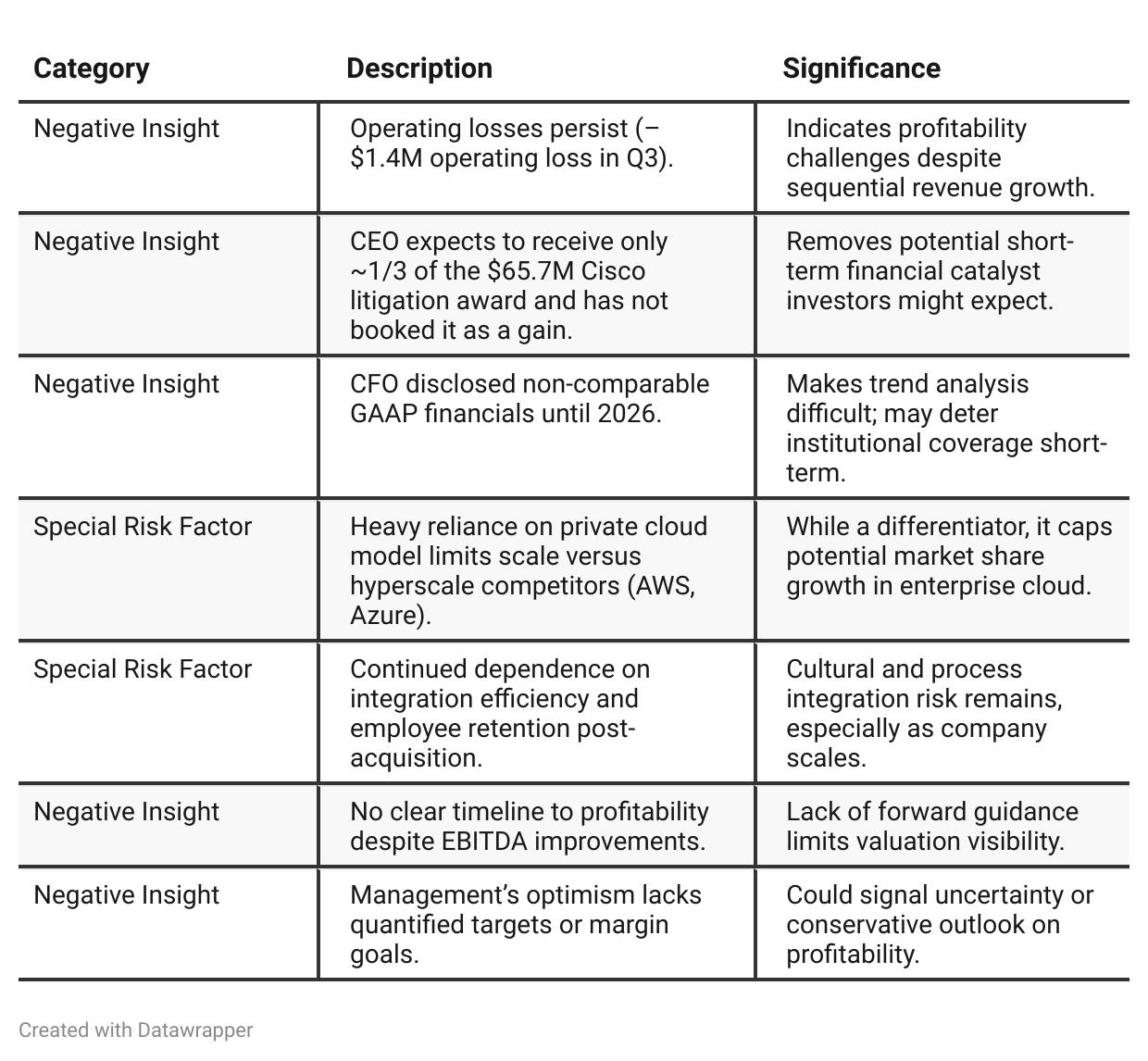

Negative Insights

Investor Underappreciation Signals

✅ Deferred Revenue Build — $3.5M deferred sales backlog represents locked-in service revenue for upcoming quarters, signaling visibility investors may underappreciate while focusing on current losses.

✅ Private Cloud Advantage — resilience during AWS outages gives IPM a credible differentiator that’s defensive in nature; investors may overlook this as “niche,” but enterprise clients value uptime guarantees highly.

✅ MindsDB AI Partnership — early-stage AI integration could evolve into a margin-accretive service layer over the core cybersecurity platform; the market likely undervalues this as “immaterial” until results surface.

✅ Stock Buyback During Loss Phase — management confidence signal while still in integration mode; suggests balance sheet discipline and belief in intrinsic undervaluation.

✅ No Capital Raise Planned — stability amid scaling reduces dilution risk and strengthens perception of financial self-sufficiency, especially rare for small-cap tech integrators post-acquisition.

Tariff Risk

No mention of U.S. tariffs or trade policy impacts in the transcript.

IPM’s business model — managed IT, private cloud hosting, and cybersecurity — has minimal direct exposure to tariff-driven costs since it’s service-heavy and not reliant on imported components. Indirect exposure could arise if tariffs increase costs for clients (hardware procurement), but management did not flag this risk.

Conclusion: Tariff exposure negligible at present.

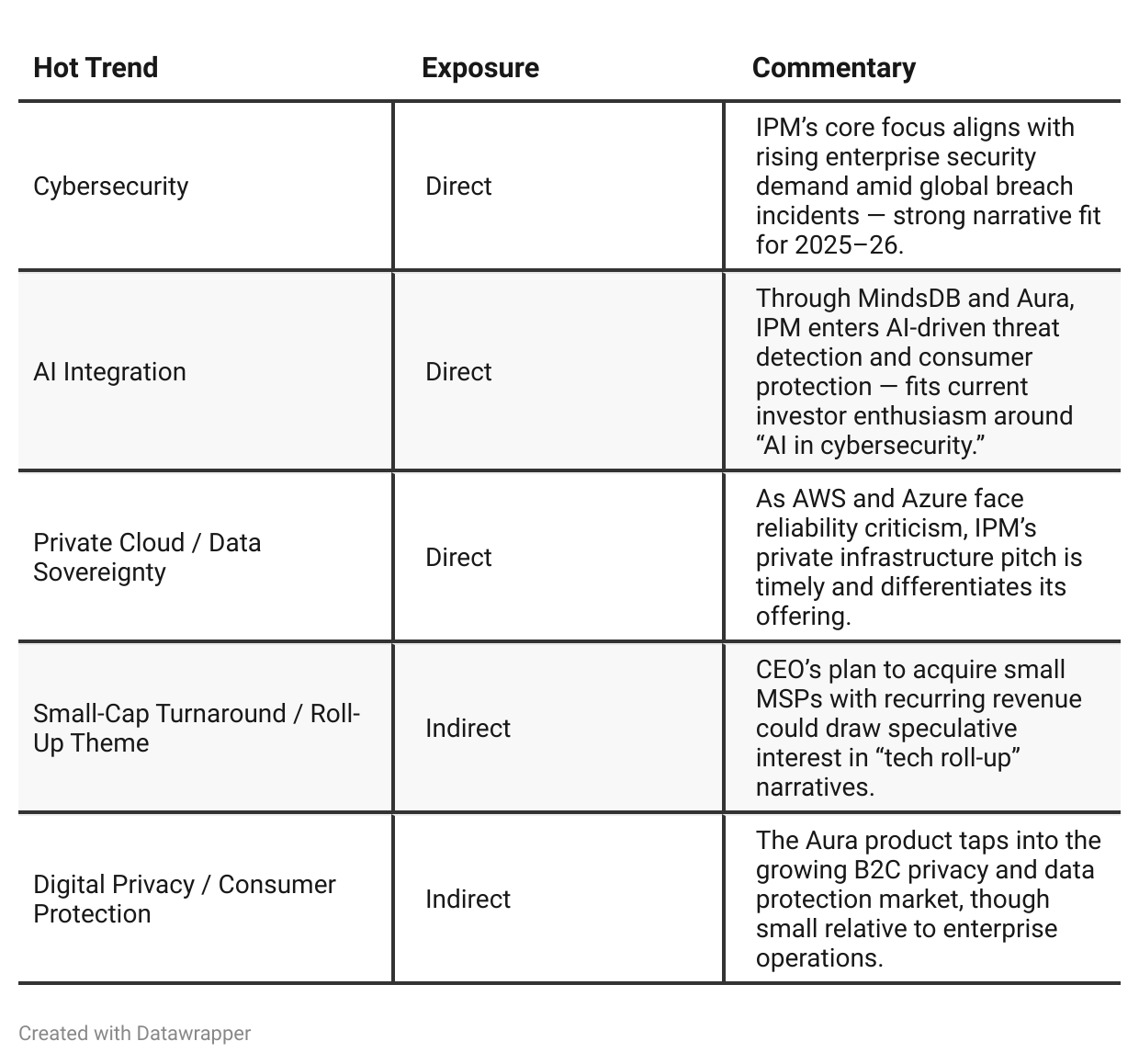

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Between Q2 and Q3 2025, Intelligent Protection Management Corp. (IPM) transitioned from an integration-focused narrative to an execution-driven one.In Q2, management’s tone was that of a newly transformed company — explaining its acquisition of NTS, laying operational groundwork, and signaling a cautious optimism about achieving adjusted EBITDA profitability by early 2026. The messaging emphasized structure, process, and foundation-building.

By Q3, the tone was distinctly more confident. The integration phase was framed as complete, and management’s language shifted toward efficiency, scalability, and market differentiation. IPM introduced tangible data points (9% sequential revenue growth, improved EBITDA, ongoing buybacks) and strategic expansions such as bolt-on acquisitions and AI-powered offerings.

The Q3 call also projected a more mature investor communication style — less about explaining the business, more about showcasing momentum. The narrative evolved from “we are building a platform” to “we are executing and expanding on it.”

Year-over-year comparison

—

Final Takeaway

Intelligent Protection Management Corp. is in a restructuring-to-growth phase, transitioning from acquisition integration toward stable recurring revenue. The company’s core strength lies in its private cloud reliability, AI partnerships, and zero-debt balance sheet. However, profitability and scale remain unproven, and the Cisco litigation outcome is a key swing factor.

Execution on cross-selling, margin improvement, and accretive acquisitions will determine whether IPM evolves from a small-cap turnaround into a scalable cybersecurity services player.

Verdict: HOLD — Moderate upside potential in 2026 if integration continues smoothly, but risk of volatility until GAAP comparability stabilizes.