Intelligent Protection Management Corp. (NASDAQ: IPM) – Q2 2025 Earnings

Intelligent Protection Management Corp. (NASDAQ: IPM) – Q2 2025 Earnings

Earnings Release Date: Aug. 12, 2025

Stock Price: $1.91

Market Cap: $7.6 million

Q2 2025 sales of $5.7 million vs $0.3 million in the prior year

Q2 2025 EPS of ($0.08) vs ($0.10) in the prior year

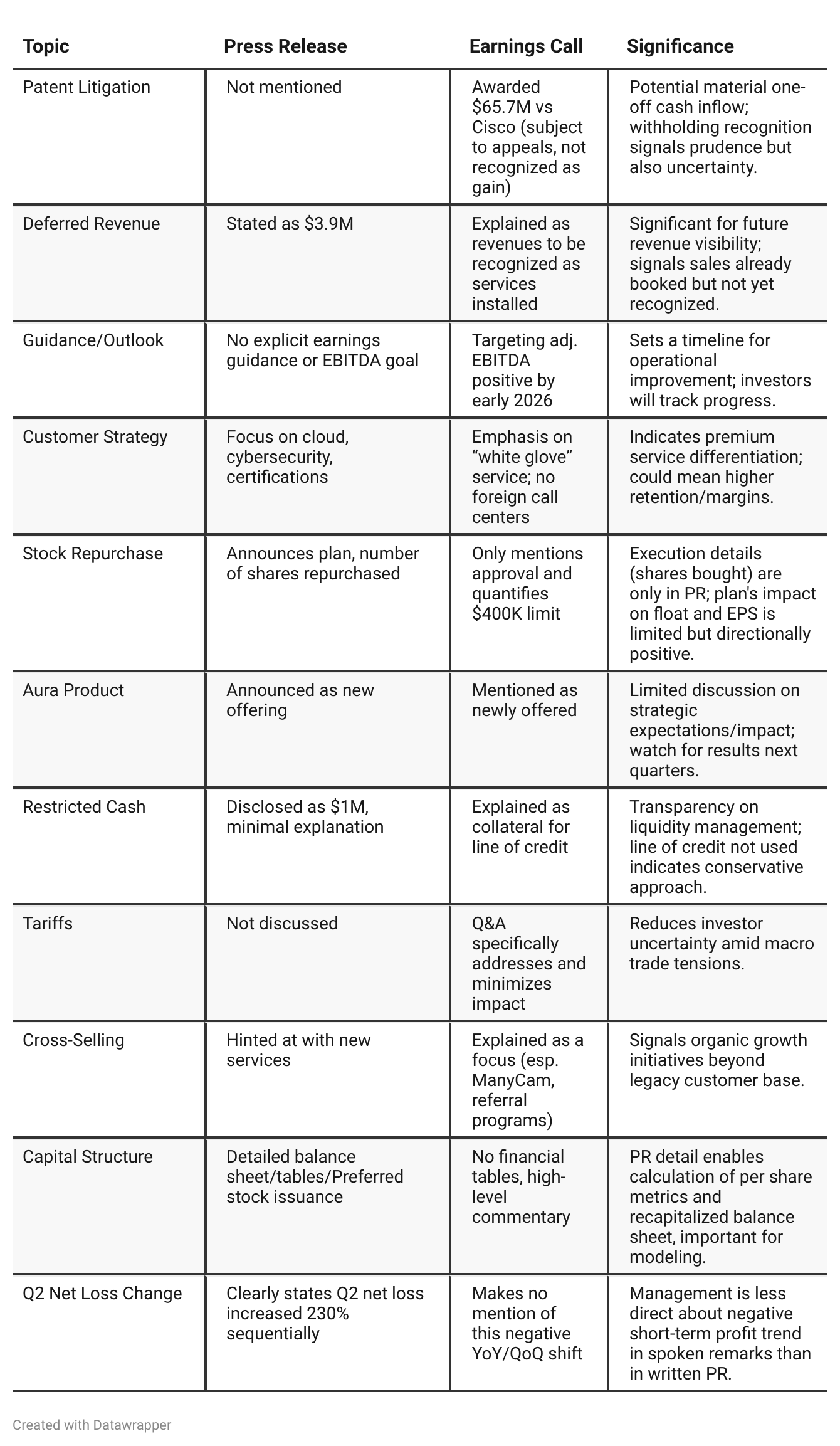

Press Release vs Call Transcript Comparison

Financials (PR is more granular): The press release provides full financial tables and more explicit period-to-period comps, crucial for analysts to model and benchmark future results. Call transcript offers context but not actual numbers beyond headline figures.

Investor Relations Transparency: The call includes a Q&A where management addresses investor-submitted questions, giving more color on liquidity (restricted cash), risk factors (tariffs), and growth strategies (referral/M&A), adding qualitative value not in the PR.

Acquisition Accounting: The call warns that historical comparisons are complicated by the NTS acquisition/divestiture, with true YoY comparability starting only in Q1 2026. This caution is flagged in passing in the PR.

Intangible Assets and Goodwill Surge: The PR’s balance sheet shows a significant increase in intangibles and goodwill post-acquisition, underscoring the shift to a tech/IP-rich company rather than pure service/hosting provider.

Cash Flow Positive from Ops, but Overall Cash Down: The PR shows positive op cash flow in 1H 2025, but investing outflows (NTS deal, capex) mean total cash is still down YTD—a pivotal detail for assessing actual burn/runway.

Stock Compensation and New Preferred Shares: Not directly addressed in the call, but relevant for dilution and shareholder analysis.

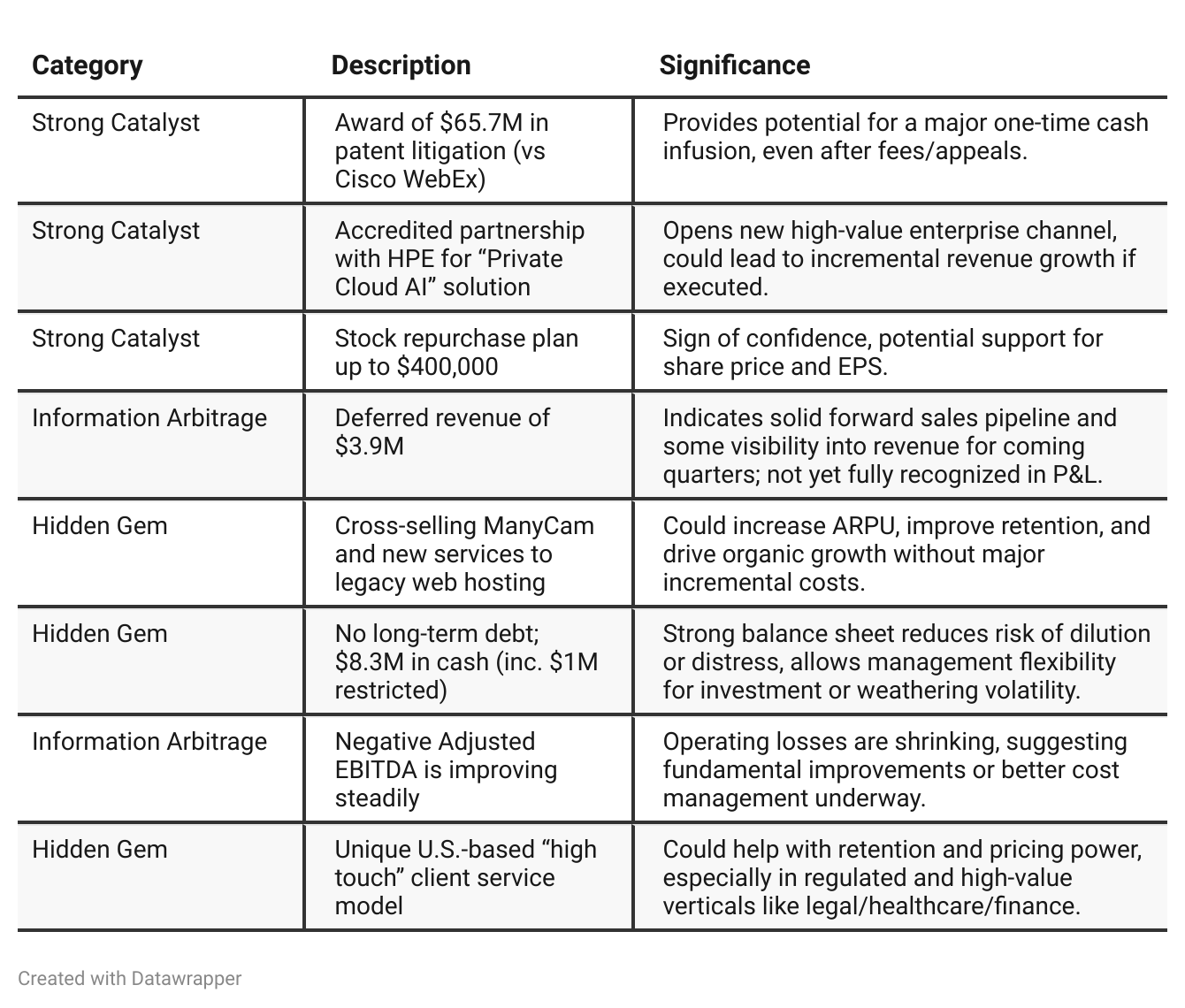

Positive Insights

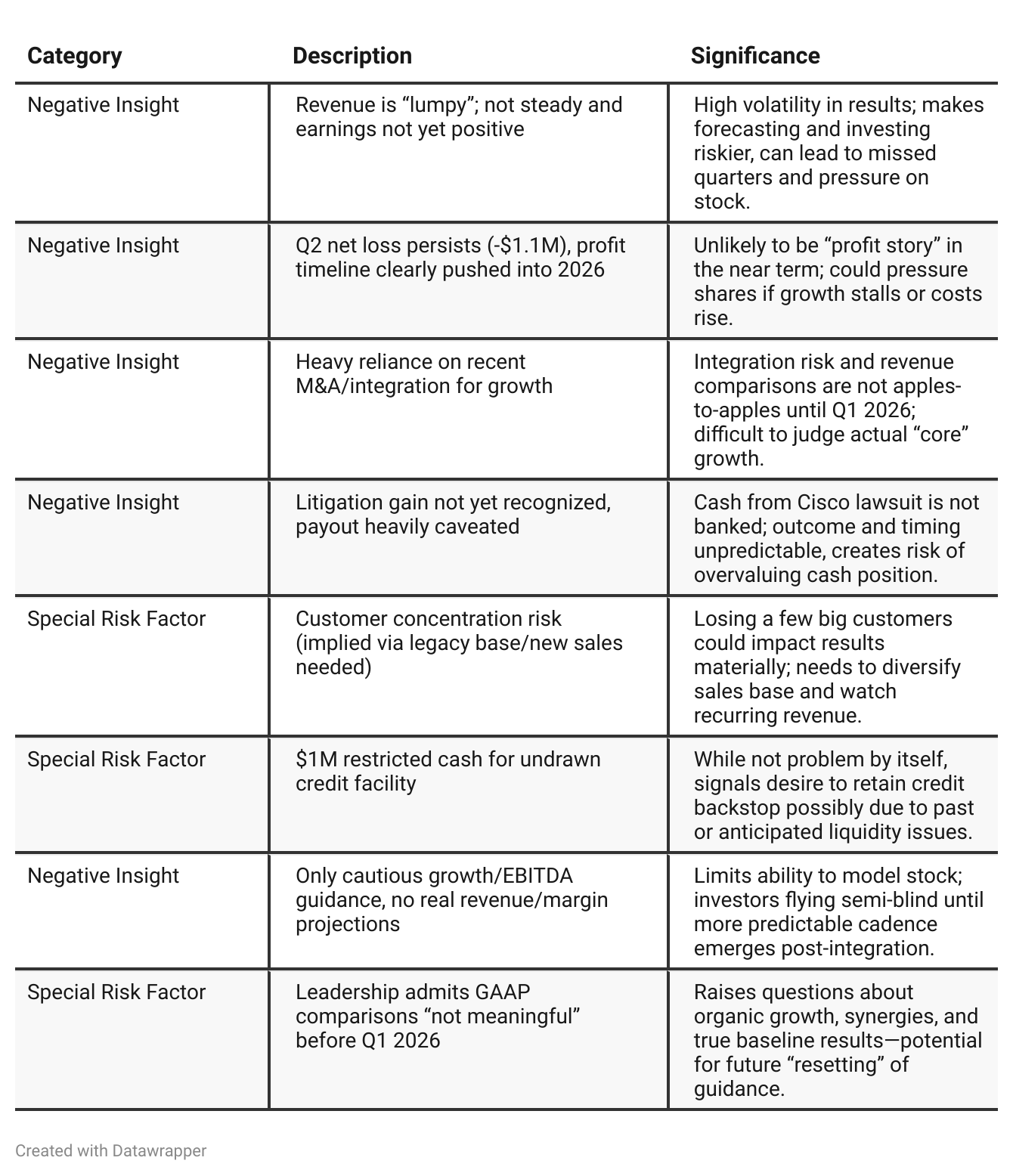

Negative Insights

Tariff Risk

Transcript Analysis:

Tariffs discussed during Q&A: Management states, “We’ve evaluated our customer base and the services we’re providing to them and do not anticipate that an increase in tariffs would have a material impact on our business in fiscal 2025.”

Actions: No supply chain changes, contract renegotiations, or price adjustments are mentioned. Company does not say it is shifting suppliers, offshoring, or actively hedging.

Forward-looking: Management remains vigilant—“We will continue to stay on top of the issue like others in the industry and reassess based on the changing landscape.” No projections of direct impact on costs, earnings, or growth are provided.

Market/competitive implication: No effects noted or forecasted for market share, competitive position, or innovation ability. IPM operates a services-heavy (rather than manufacturing) model, lowering direct tariff risk.

Summary: Tariffs are not currently expected to affect revenue, costs, or margins in FY25. No active countermeasures disclosed; monitoring situation. If trade environment worsens, this could change, but for now, tariffs are a non-event for IPM.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: IPM’s narrative is one of rebirth and repositioning: “We have just completed a major business pivot. Our foundation is in place. We’re excited, have a strong pipeline, and believe our unique cybersecurity/cloud solutions can win in a growing market. Here’s what we do now, and how we’ll get customers onboard and cross-sell.”Q2 2025: The narrative matures: “We’re executing the plan, gaining traction with key partnerships and new products, and already seeing the beginnings of growth and operational discipline. We are beginning to show results—deferred revenue is booked, our cost structure is improving, we’re putting cash to work for shareholders, and our model is distinctive (white-glove/U.S. focus). But we’re realistic: revenue is still lumpy, true comparability is a few quarters away, the legal windfall is not a lock, and we’re still a few quarters out from consistent profitability.”

Year-over-year comparison

Paltalk Q2 2024: A company at an inflection point, struggling with sliding legacy revenues, an inflation-sensitive consumer base, and weak operational performance. Management’s messaging is defensive, aiming to reassure investors with promises that the NTS acquisition, pending trial against Cisco, and product launches will rescue growth and transform the company. The story is one of hope pinned on near-term catalysts and a belief in turnaround through strategic moves.

IPM Q2 2025 (One Year Later): A transformed business that has pivoted decisively from its legacy to a more sophisticated, enterprise-facing, technology-managed services player. The company’s narrative is now built on execution, integration progress, growing partnerships, product innovation, and measured steps toward profitability. The tone is more realistic but also more authoritative—management openly discusses risks and caveats (integration “lumpiness,” delayed profitability, legal uncertainties) but also demonstrates real operational traction and strategic discipline.

Final Takeaway

Intelligent Protection Management Corp. is in a restructuring and repositioning phase, seeking to pivot to a higher-value, managed cybersecurity/cloud provider business post-acquisition. While sequential growth and strong cash/liquidity are positives, risks include ongoing losses, revenue lumpiness, and reliance on integration execution not yet fully proven. Key growth levers—legal award windfall, HPE partnership, and new products—must translate into real bottom-line improvement. Execution on cost controls, the transition to profitability, and early signs of success in referrals/cross-sell will be critical. Verdict: Hold, with moderate upside if business momentum accelerates or litigation cash is received, but risks remain if growth or profit goals slip.