Information Services Group, Inc. (NASDAQ: III) – Q3 2025 Earnings

Information Services Group, Inc. (NASDAQ: III) – Q3 2025 Earnings

Earnings Release Date: Nov. 03, 2025

Stock Price: $5.51

Market Cap: $265.9 million

Q3 2025 sales of $62.4 million vs $61.3 million in the prior year

Q3 2025 EPS of $0.06 vs $0.02 in the prior year

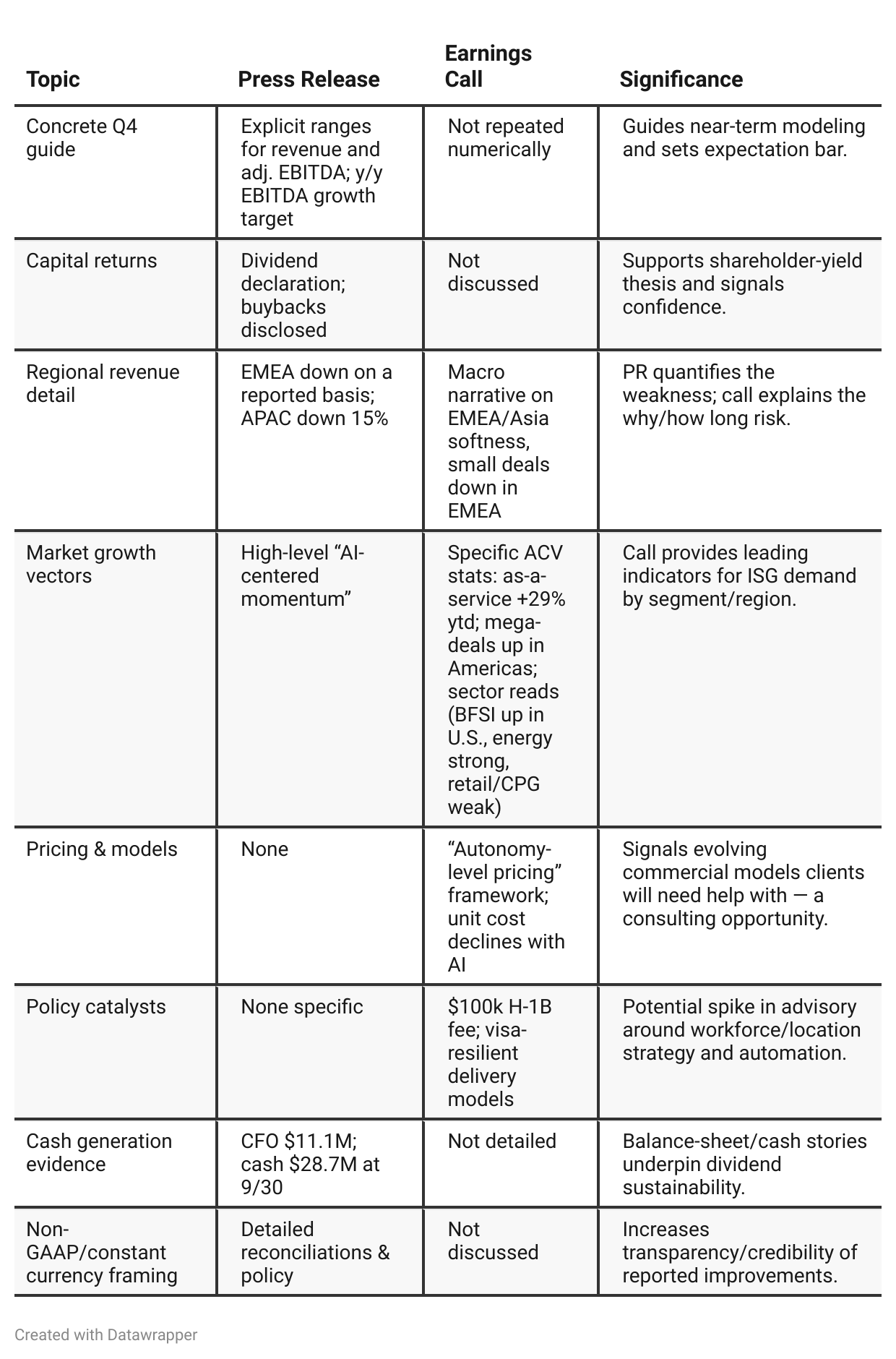

Press Release vs Call Transcript Comparison

Mix & margin: Adj. EBITDA margin up ~200 bps y/y signals favorable mix/efficiency; if AI-led advisory keeps scaling, this margin profile could persist.

Cash returns discipline: dividends + buybacks amidst positive CFO show room for continued shareholder returns if trends hold.

“Americas first” cycle: The call’s granular ACV reads match the PR’s revenue skew — model a continued U.S. carry with Europe/Asia lagging.

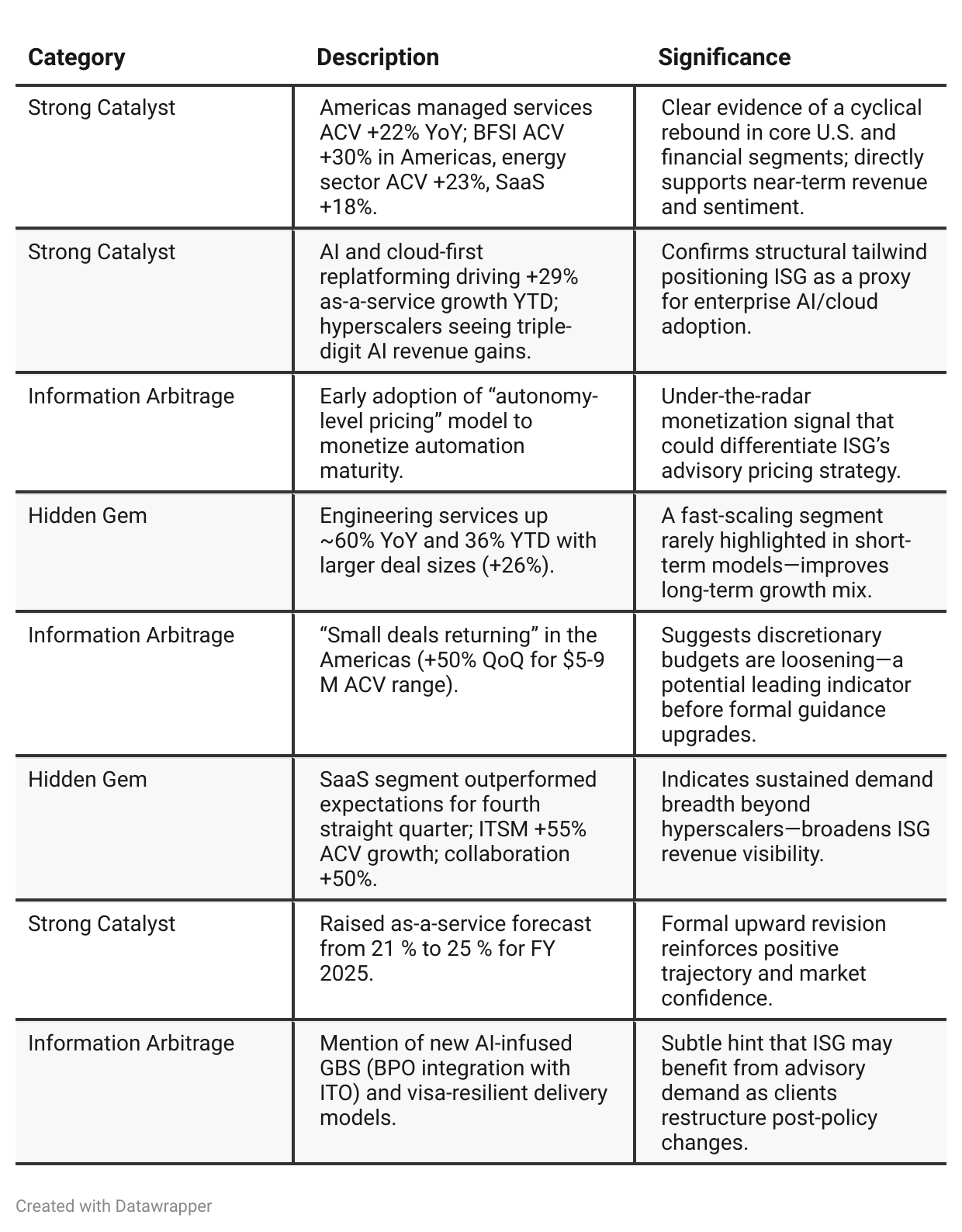

Positive Insights

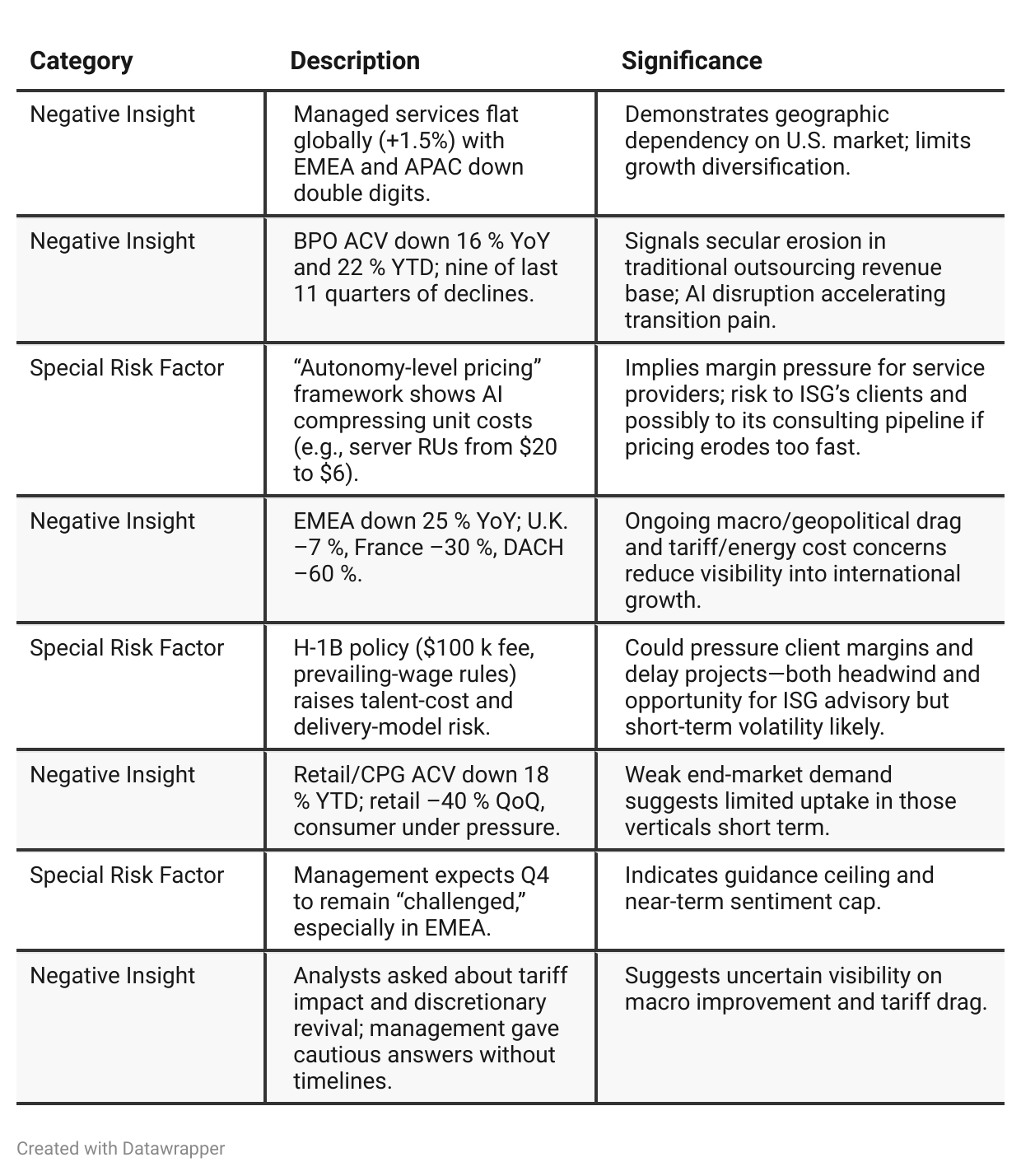

Negative Insights

Tariff Risk

Mentions: Tariffs are explicitly cited as a drag in EMEA (“energy costs, tariff concerns, and geopolitical tensions” hurting tech spending)

Impact: Retail and automotive sectors (“tariff hit sectors”) show the sharpest decline in ACV (–40% retail QoQ).

Mitigation: ISG expects clients to counter tariff pressures through cost optimization and supply-chain re-engineering advisory — which could boost ISG’s consulting demand.

Forward View: Management did not quantify tariff impact but expects continued uncertainty into Q4 and 2026; opportunity for AI-led efficiency projects may partially offset trade-related slowdowns.

Summary: Tariffs currently weigh on European and consumer verticals but create counter-cyclical demand for ISG’s cost-optimization consulting services.

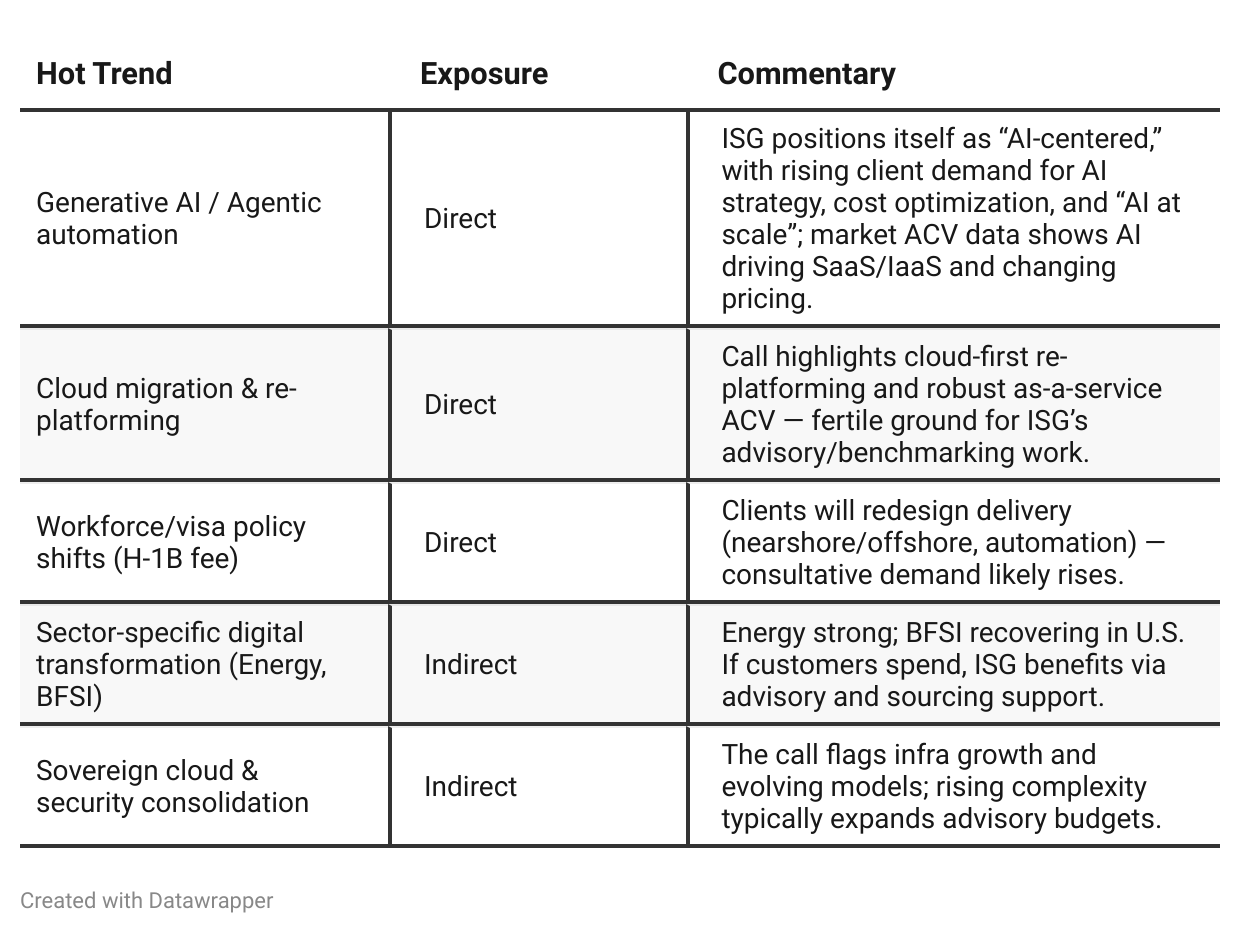

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

In Q2’25, ISG’s narrative centers on its own beat-and-raise style story—AI revenue scaling, cash generation, Americas strength, Italy tuck-in M&A, and a straightforward Q3 guide.In Q3’25, ISG widens the aperture: it codifies how AI/Cloud are reshaping demand, pricing, and delivery (small deals back in U.S.; BPO reset; “autonomy-level pricing”; H-1B rewriting workforce economics). The message shifts from “we’re executing” to “here’s the playbook for where the market is going”—with ISG positioned to advise through that change.

Year-over-year comparison

2024: ISG framed itself as a steady hand in turbulent markets—emphasizing resilience, disciplined cost control, and cautious optimism amid delayed client decisions and regional softness. AI was a coming opportunity, not yet a revenue engine.

2025: The company’s story matures into one of strategic leadership. ISG now speaks as the market’s architect, interpreting how AI, automation, and regulation reshape global services. Its messaging shifts from “we’re stable” to “we define the next pricing and delivery models.” Financial tone is confident but disciplined—growth concentrated in U.S. and as-a-service, offset by structural headwinds in EMEA and BPO.

Final Takeaway

ISG (NASDAQ: III) is in a growth reacceleration phase, driven by AI-enabled advisory services, cloud migration, and engineering expansion. While U.S. momentum and as-a-service growth support the bull case, persistent weakness in EMEA and pricing pressure from AI automation pose risks. Execution on AI-related consulting and margin discipline will be key.

Verdict: BUY, with potential upside if AI consulting pipeline translates into earnings expansion through 2026.