Information Services Group, Inc. (NASDAQ: III) – Q2 2025 Earnings

Information Services Group, Inc. (NASDAQ: III) – Q2 2025 Earnings

Earnings Release Date: Aug. 6, 2025

Stock Price: $4.24

Market Cap: $204.6 million

Q2 2025 sales of $61.6 million vs $64.3 million in the prior year

Q2 2025 EPS of $0.08 vs $0.07 in the prior year

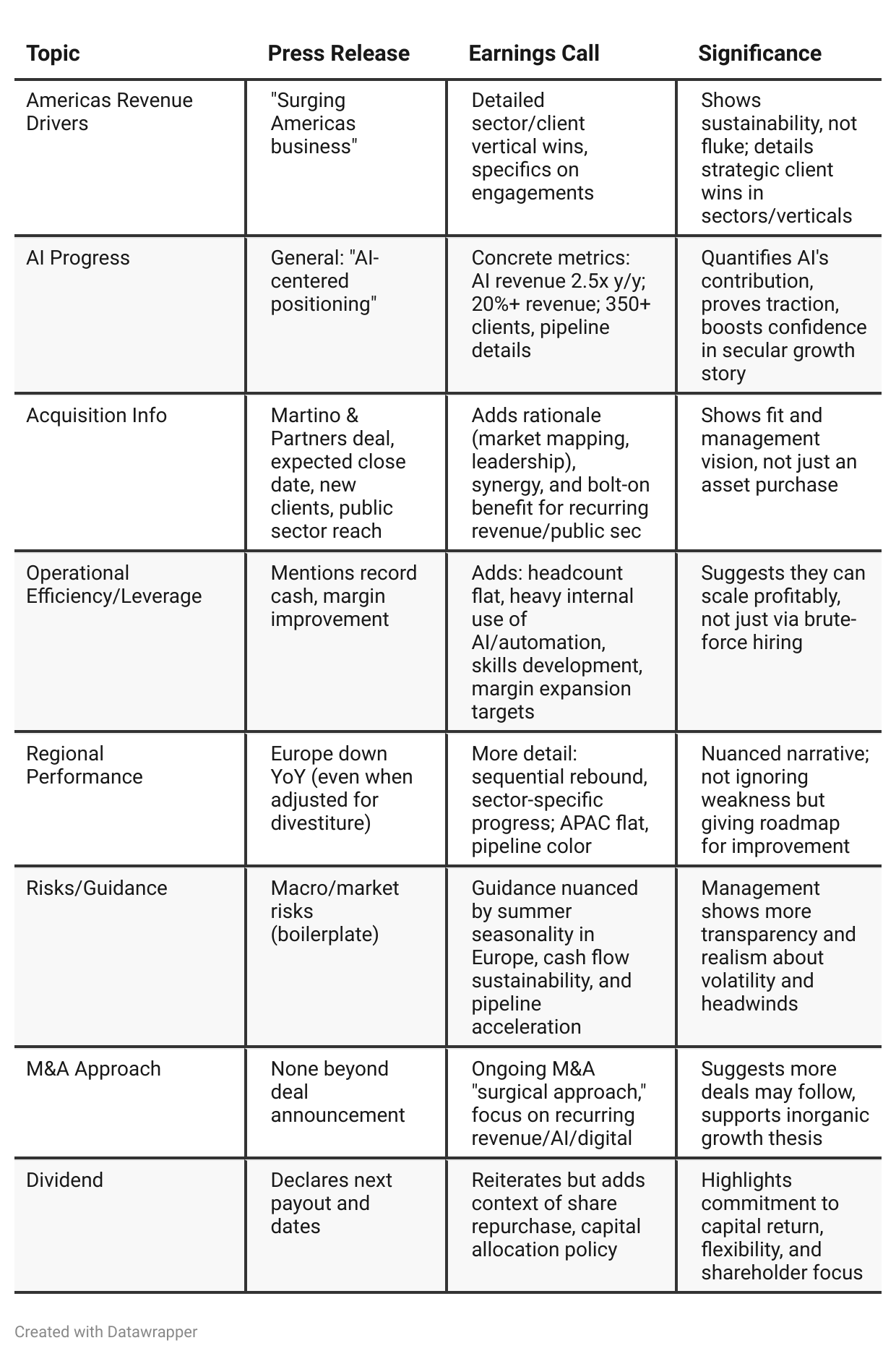

Press Release vs Call Transcript Comparison

AI as a Core Differentiator: Both documents frame ISG as an “AI-centered” firm, but the call makes clear they are quantifying and accelerating this shift—growing pipeline, infrastructure, and client base.

Capital Allocation Discipline: Clear commitment to dividends, buybacks, and M&A, but with disciplined, return-focused approach.

Share Count & Repurchases: Slight reduction in diluted shares; $11M remaining repo authorization may provide further EPS support.

Margin Expansion: Margin expansion due to improved mix, operating discipline, higher-value work, and internal automation; this is a notable theme for upside potential.

Management Candor: On the call, management is frank about both positives (AI pipeline, cash, sector wins) and negatives (cash timing, European uncertainty, utilization drift), which is positive for investor trust.

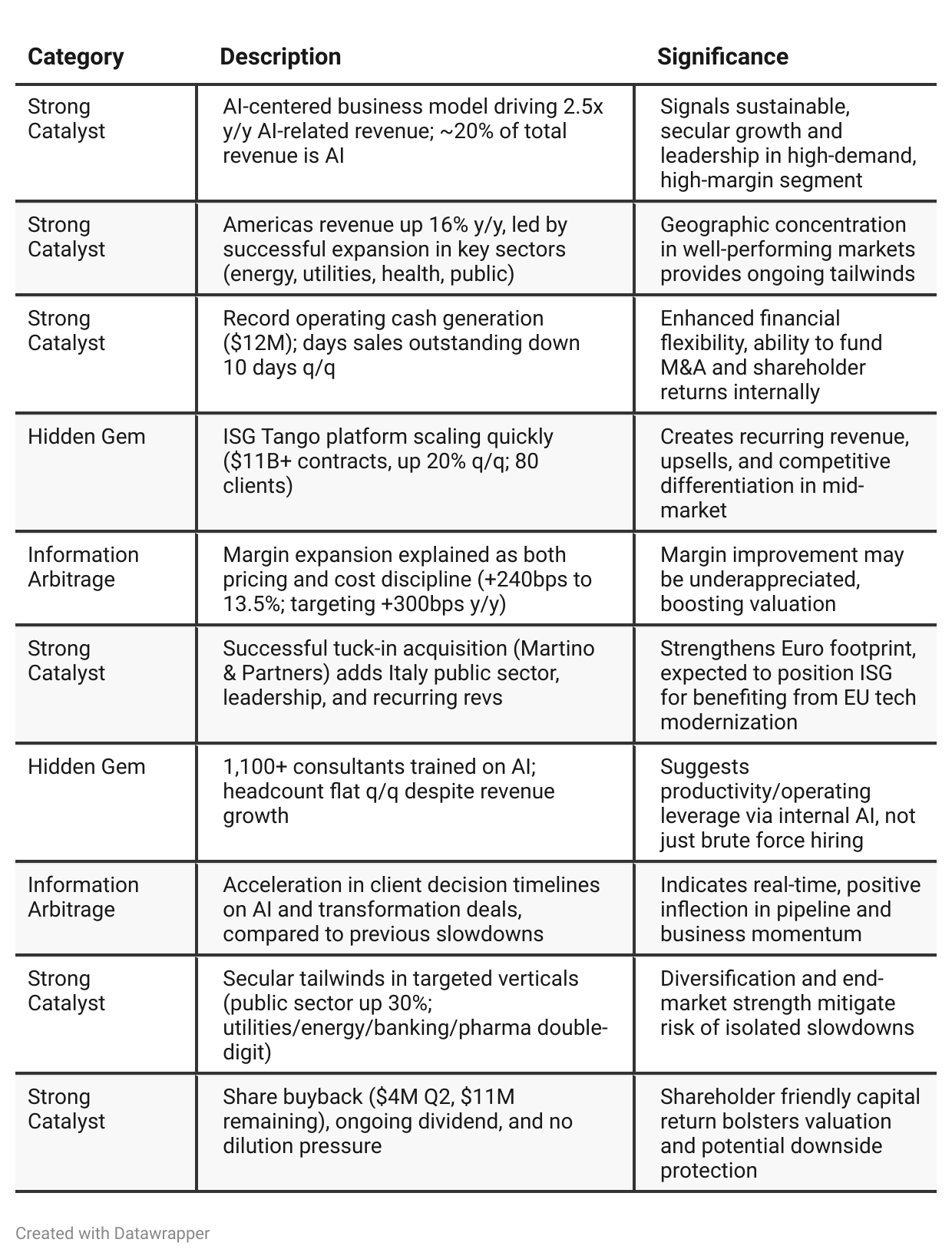

Positive Insights

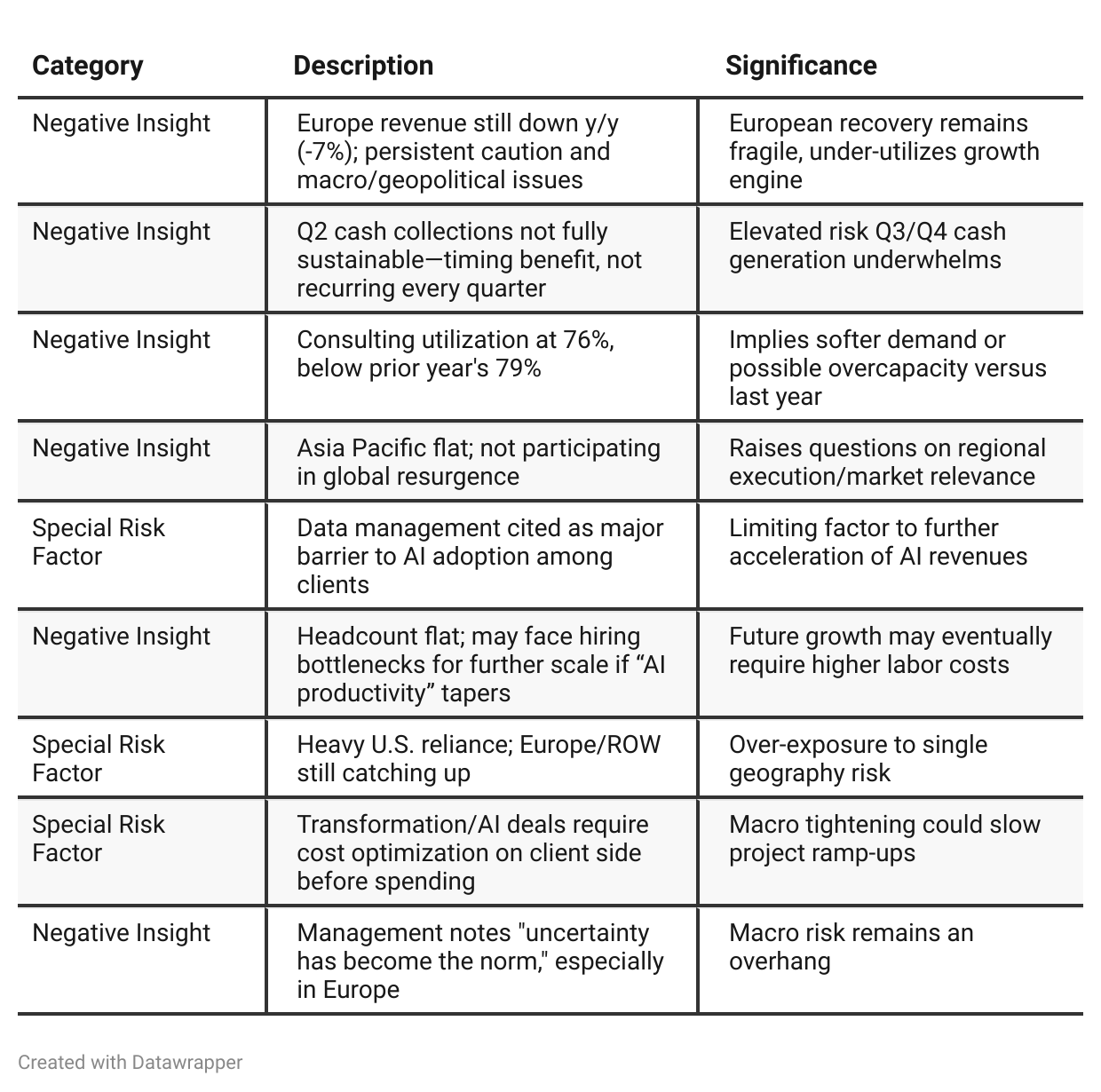

Negative Insights

Tariff Risk

Mentions & Tone:

Management acknowledges “tariff risks seem to be manageable,” and credits some pipeline acceleration to “a little more certainty around the tariffs” in the U.S.

Explicitly: “There’s at least a sizing of what those [tariffs] are and what kind of products… are being tariffed. And they are then responding and reacting and trying to either get ahead of it or to help mitigate some of that. And so we’re right in the middle of it.”

Tech-services spending outlook is “somewhat mixed,” but no indication that tariffs are causing major disruption to revenue or profitability at present.

Mitigation Actions:

ISG’s core exposure is to tech services/advisory rather than manufacturing—this lessens direct supply-chain risk from tariffs.

Clients are using ISG to optimize tech costs, which includes supply-chain adjustments due to tariffs (“uncertainty breeding stronger demand for technology-led cost and supply-chain optimization services, and that plays to our strengths”).

Impact on Market Share, Competitive Advantage, and Innovation:

ISG states that tariff-related uncertainty is actually driving increased demand for their services in supply chain and cost optimization. This suggests potential market share gains from clients needing more external expertise to navigate these macro complexities.

No evidence in the call that tariffs are hurting ISG’s competitive position; rather, ISG’s vendor-agnostic and advisory model may provide a competitive edge as companies seek objective partners to respond to trade disruptions.

ISG is not reporting any negative impact on its own innovation or ability to deliver AI/digital transformation projects as a result of tariffs.

Forward-Looking Statements and Projections:

Management expects tariff exposure to remain manageable and sees no current signs of profit or revenue impairment from trade policy. They do, however, frame the macro environment as "uncertain" and suggest they will monitor developments closely.

If trade tensions intensify or impact technology budgets and implementation schedules, the company may see a near-term slowdown, but so far, the net effect is neutral-to-positive for ISG’s advisory demand.

Sentiment Analysis

The overall sentiment for $III is bullish. Several comments highlight strong operating and financial metrics, such as robust ROE, EBIT and free cash flow growth, and suggest the stock is one of the best compounders. Notably, there are comparisons to life-changing returns, endorsements from prominent shareholders, and references to bullish analyst ratings and targets. While there are some neutral informational posts and unrelated tickers mixed in, the prevailing views from investors with opinions are positive and supportive of future upside.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

In Q1 2025, ISG’s management established a foundation of “momentum” and operational discipline, with a measured optimism balanced by caution around macro uncertainty—especially tariffs and European sentiment. The company emphasized margin expansion, AI client adoption, and solid growth in the Americas, but remained watchful about external risks and client hesitancy.By Q2 2025, ISG’s tone is more self-assured and outwardly aggressive. The narrative shifts from defensive stability to proactive opportunity capture: AI revenues and client counts are accelerating, new accounts and large-ticket wins are achieved faster, and operating leverage allows for record cash generation. The company positions itself as an agile, trusted advisor taking advantage of changing client priorities, especially as uncertainty itself is now catalyzing demand for their services. Strategic M&A is introduced as a new growth engine, and Europe’s sequential improvements are finally materializing, albeit cautiously. Management’s messaging projects an image of ISG not just weathering the macro storm, but thriving because of it, with more concrete milestones and a clear pathway toward value creation and further market share gains.

Year-over-year comparison

In Q2 2024, ISG was in a transition phase—navigating macro-driven caution, emphasizing product mix and cost controls, and working to leverage Tango and emerging AI capabilities to stabilize and later grow margins. Demand (especially for digital and recurring) was rising but hampered by slow decision cycles and heavy external headwinds, with leadership guided but guarded.

By Q2 2025, the tone and substance are more assertive and forward-looking: AI is no longer a prospect but a central, measurable engine of growth and margin. Record operational results provide a platform for confidence. The pipeline is now converting quickly, ISG Tango is a real force for mid-market expansion, and the strategy is broadened with targeted M&A to strengthen geographic and public sector reach. Europe is still watched closely, but rather than hoping for recovery, the company is actively planting seeds—both via deals and internal scaling.

The story is one of successful transformation: ISG has pivoted from defensive stabilization to proactive, AI-driven growth, with tangible progress, credible financial performance, and a more confident roadmap for capturing emerging sector and technology trends.

Final Takeaway

Information Services Group, Inc. is in a growth phase, leveraging a robust pivot toward AI-powered consulting and recurring revenue. Strong balance sheet, margin expansion, operational leverage, and a diversified vertical/client base position the firm well for durable outperformance. Europe recovery remains a key watch item, but pipeline momentum and disciplined capital allocation are positives. Execution on AI, mid-market platforms, and expansion in Europe will be critical. Verdict: BUY, with moderate volatility but substantial long-term potential if execution continues.