The Eastern Company (NASDAQ: EML) – Q3 2025 Earnings

The Eastern Company (NASDAQ: EML) – Q3 2025 Earnings

Press release and earnings call link

Earnings Release Date: Nov. 04, 2025

Stock Price: $21.27

Market Cap: $129.2 million

Q3 2025 sales of $55.3 million vs $71.3 million in the prior year

Q3 2025 EPS of $0.10 vs $0.75 in the prior year

Overview. The Eastern Company (“Eastern”) designs and manufactures engineered components and systems for commercial transportation, logistics (e.g., returnable transport packaging), and other industrial end markets from facilities in the U.S., Canada, Mexico, Taiwan, and China.

Revenue drivers (what they sell). Key lines are truck mirror assemblies, latches/handles/locks (used across Class 8 trucks and specialty vehicles), and returnable transport packaging tied to automotive model launch cycles.

Main customers / end markets. Heavy-duty trucks (Class 8 = the heaviest road trucks), North American auto OEMs (including the “Big 3”), and government/specialty vehicles (e.g., USPS program via Oshkosh).

Market positioning. A diversified niche supplier of engineered solutions with long-standing OEM relationships; not a category volume leader, but positioned as a specialized component partner that can flex across cycles.

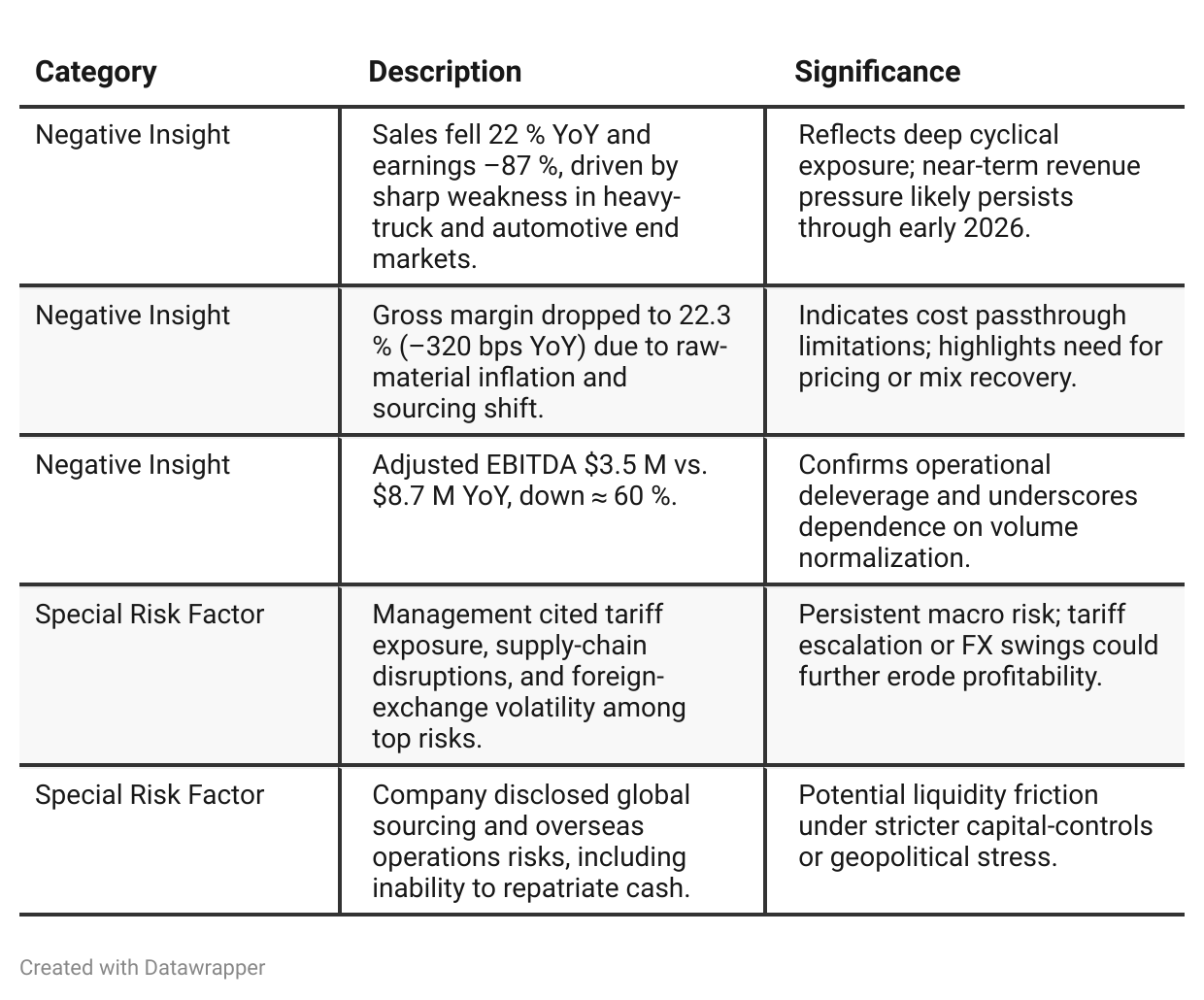

Recent financial trajectory. Q3’25 net sales fell 22% YoY to $55.3M; gross margin compressed to 22.3% (from 25.5%); EPS from continuing ops was $0.10; Adjusted EBITDA was $3.5M. Nine-month revenue declined 7% to $191.4M.

Near-term themes / strategy. Cost resets and footprint changes, balance-sheet flex (new $100M revolver), targeted share repurchases (~118k shares), and customer diversification while awaiting an eventual truck and auto model-launch rebound. Management also flagged USPS program momentum and a cautious 2026 cadence (soft 1H; improvement later).

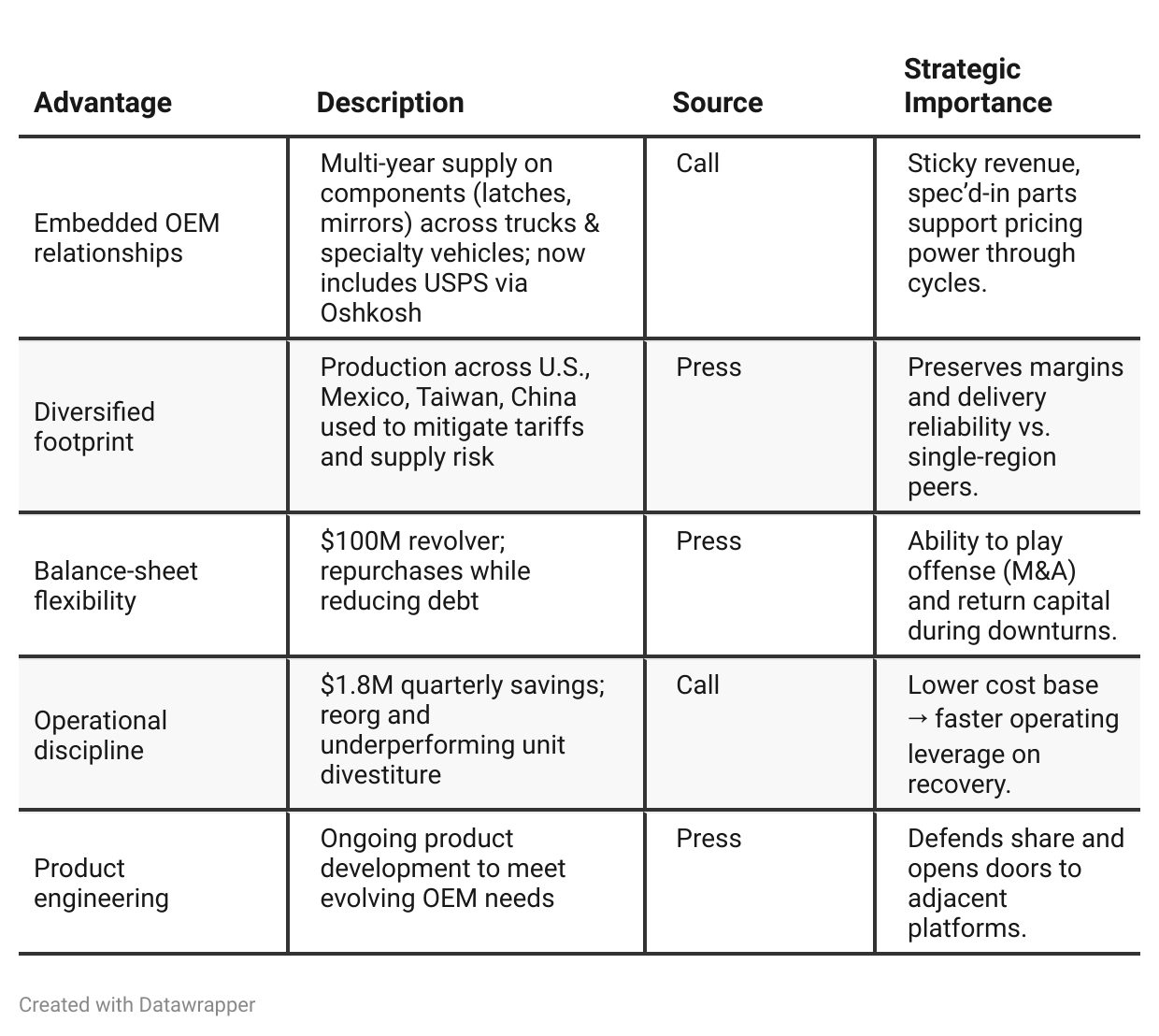

Competitive Advantage Insights

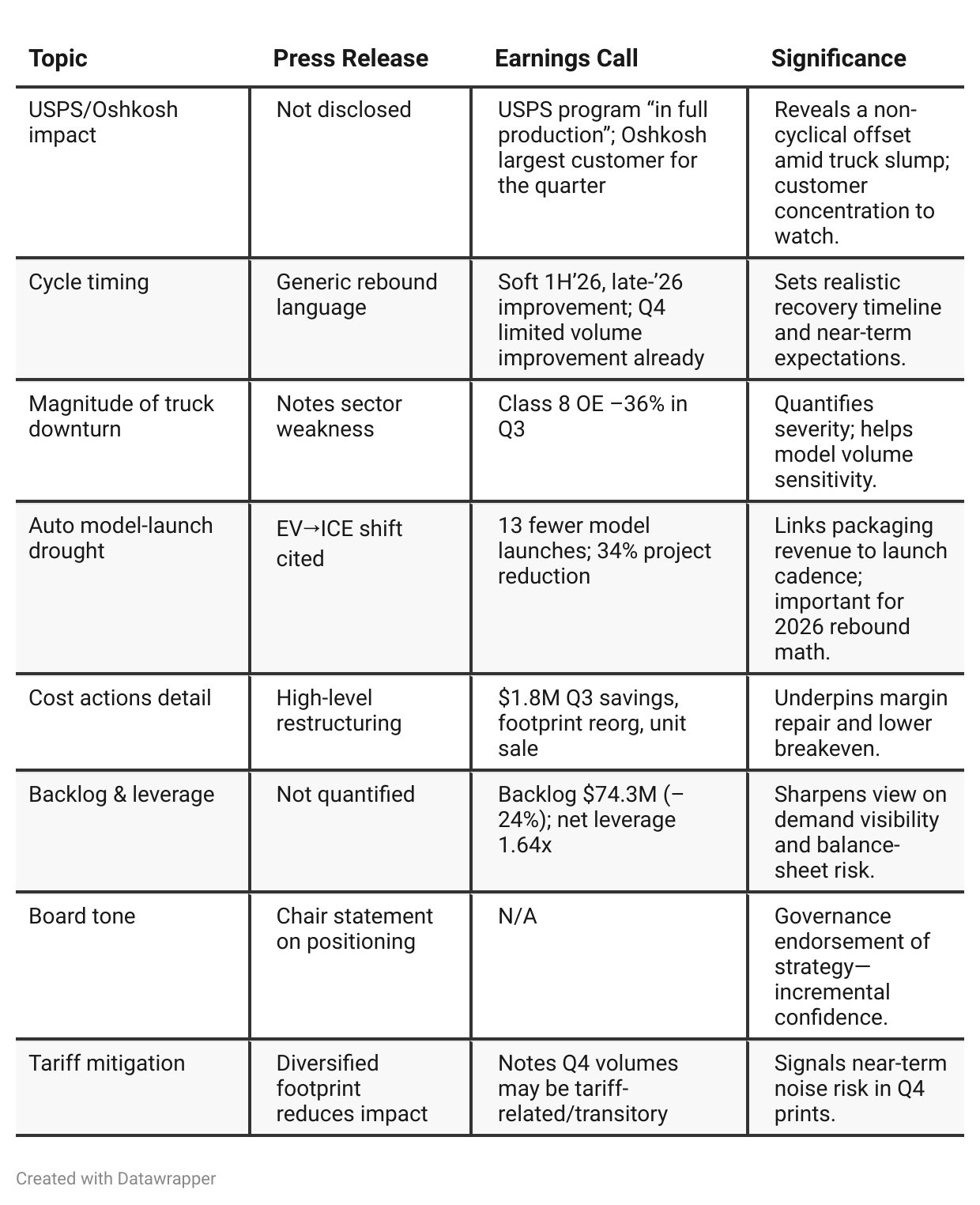

Press Release vs Call Transcript Comparison

Margin path: Both sources cite mix/volume pressure, but the call’s specifics (mirror sourcing transition; volume normalization → margin normalization) support a reversion case once volumes rebound—useful for modeling EBITDA/GM recovery without needing pricing heroics.

Capital allocation: The press release highlights repurchases and debt paydown; the call adds a flexible revolver and conservative leverage, implying M&A optionality when valuations are attractive.

Demand indicators: The call’s backlog split and auto launch commentary are leading indicators that aren’t obvious in the release—these sharpen timing for when packaging and latches could turn.

Positive Insights

Negative Insights

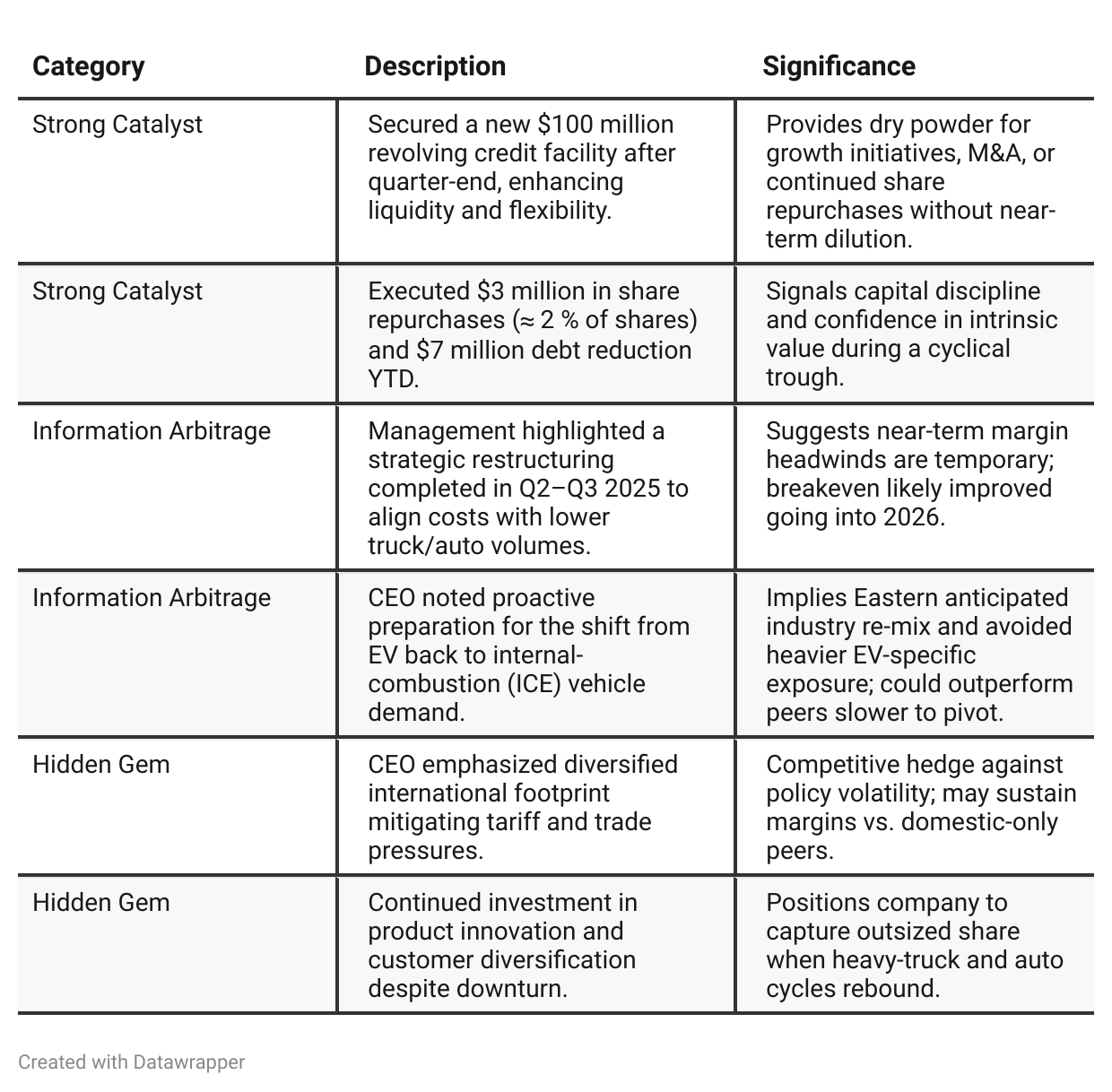

Investor Underappreciation Signals

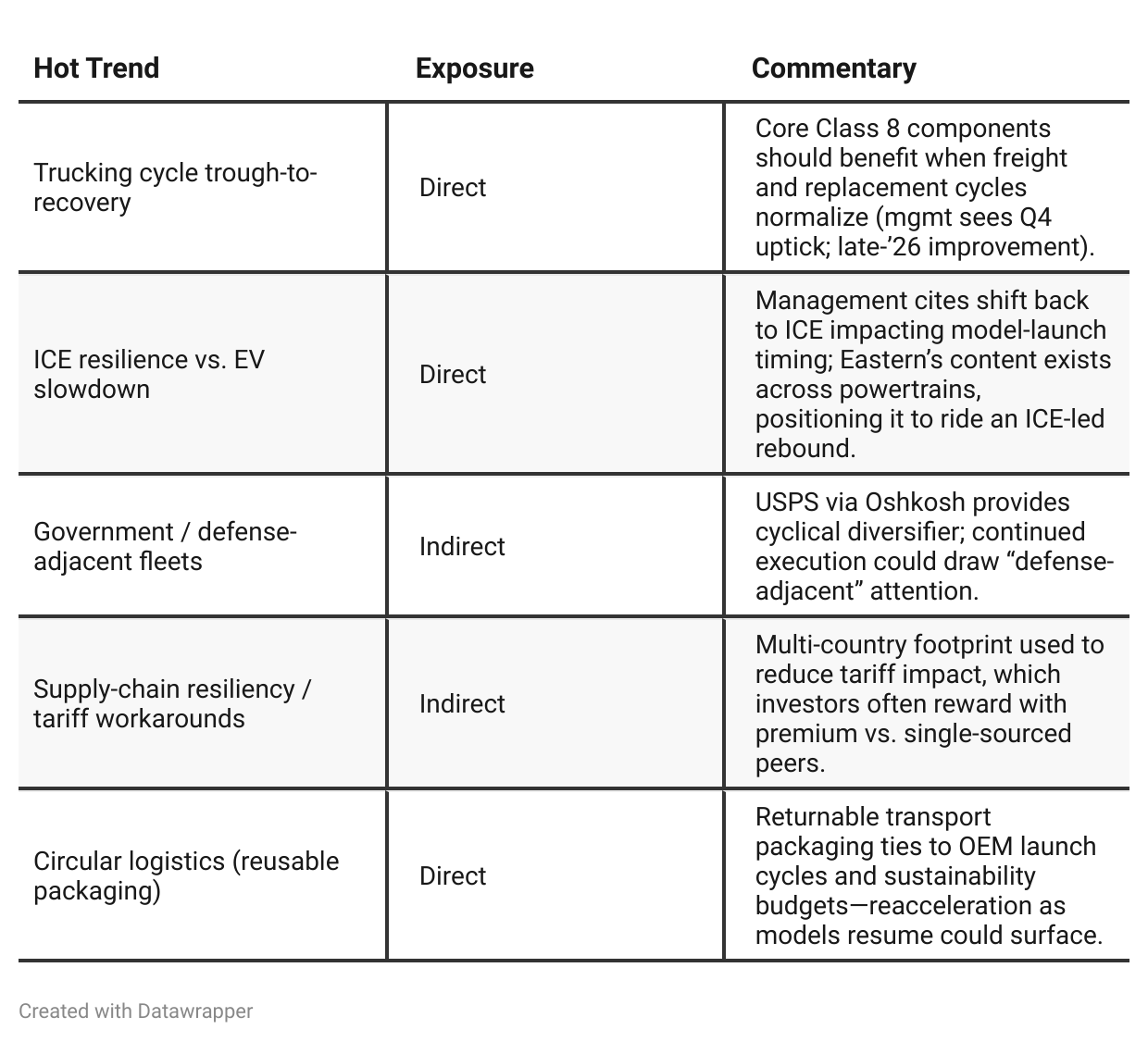

✅ USPS Vehicle Contract Ramping — The Oshkosh USPS vehicle program has ramped into full production and became Eberhard’s largest customer this quarter. Investors may be underestimating its durability and earnings impact into FY26 because management avoided quantifying revenue, but the full-year run-rate suggests meaningful incremental volume stability against cyclical end-market weakness.

✅ Automotive Model Launch Rebound — Management confirmed a “historical low” in new model launches this year but noted backlog growth and increasing program activity heading into 2026. This setup for a multi-quarter recovery is likely being overlooked due to current automotive softness, yet early backlog inflection indicates a near-term lift in returnable packaging and latch demand.

✅ Margin Rebound Setup — The gross margin hit was driven by one-time volume and sourcing transitions, not structural deterioration. With volumes normalizing and restructuring complete, gross margins are set to revert toward historical levels — a potential catalyst that consensus models may not fully reflect.

✅ Operational Restructuring Payoff — The company completed workforce and footprint realignment, yielding $1.8M in quarterly savings. Investors likely view this as defensive, but the leaner cost base positions Eastern for high incremental margins once volumes recover, creating significant earnings leverage.

✅ $100M Revolving Credit Facility — The new facility provides headroom for M&A and growth investments beyond sustaining operations. Given the conservative balance sheet and ongoing debt reduction, the market may be missing how this liquidity enables opportunistic bolt-ons that could accelerate scale and diversification.

✅ Shift Back to Internal Combustion Platforms — Eastern anticipated the pivot from EVs back to internal combustion vehicles and restructured accordingly. Investors still focused on EV slowdown may not appreciate that this pivot reduces project volatility and could accelerate platform awards as OEMs retool ICE lineups.

✅ Improving Q4 Volume Signals — Management cited “marginal improvements” in Q4 Class 8 truck volumes and early signs of demand recovery. With the truck replacement cycle aging and freight conditions stabilizing, near-term upside could emerge faster than implied by consensus forecasts anchored to trough conditions.

Tariff Risk

The company explicitly acknowledged that “leveraging our diversified international footprint, we have been successful in reducing the impact of tariffs and trade-related pressures”.

However, under its risk-factors section, Eastern warns that future increases in U.S. trade tariffs could affect raw-material costs, availability, and overall cost structure. The main mitigation strategy is supply-chain diversification across the U.S., Mexico, Taiwan, and China. No specific quantitative tariff impact or margin sensitivity was disclosed.

Investor takeaway: Tariff exposure remains a manageable but persistent macro risk. Continued global diversification and proactive sourcing provide partial insulation, but sharp tariff escalation could still pressure margins and cash flow in upcoming periods.

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2’25 call → Q3’25 update:

The story evolves from “we’re executing a playbook to control what we can” (cost takeout, footprint changes, USPS ramp, disciplined buybacks, and readiness for M&A) to “we’ve proven the playbook and fortified the balance sheet to outlast a deeper trough” (heavier admission of demand softness, precise P&L impacts, and a new $100m revolver). The overarching arc is cyclical pain now, optionality and operating leverage later—with the latest update deliberately strengthening the liquidity message and reiterating diversification/innovation as the bridge to recovery.Year-over-year comparison

Between Q3 2024 and Q3 2025, The Eastern Company’s narrative evolves from renewal to resilience:

In Q3 2024, Eastern spoke from a position of operational improvement and leadership transition — celebrating margin gains, divesting a non-core unit, and welcoming a new CEO with ambitions for accelerated growth. One year later, in Q3 2025, that same CEO speaks from the trough of the cycle: sales and profits have contracted sharply, yet the messaging is pragmatic and controlled. The company highlights liquidity strength, disciplined restructuring, and strategic diversification as bridges to recovery. The tone shifts from optimism about expansion to confidence in survival and readiness to capitalize when demand returns.

Final Takeaway

The Eastern Company is in a stabilization phase, focusing on cost realignment, liquidity strengthening, and customer diversification. While the downturn in heavy-truck and auto end-markets has sharply hit revenue and margins, management has executed proactive restructuring, debt reduction, and a new credit facility to weather the cycle. Near-term fundamentals remain weak, but long-term positioning is improving.

Verdict: HOLD, with potential upside if 2026 brings truck/auto recovery and restructuring savings flow-through.