The Eastern Company (NASDAQ: EML) – Q2 2025 Earnings

The Eastern Company (NASDAQ: EML) – Q2 2025 Earnings

Earnings Release Date: Aug. 5, 2025

Stock Price: $22.33

Market Cap: $136.5 million

Q2 2025 sales of $70.2 million vs $72.6 million in the prior year

Q2 2025 EPS of $0.33 vs $0.65 in the prior year

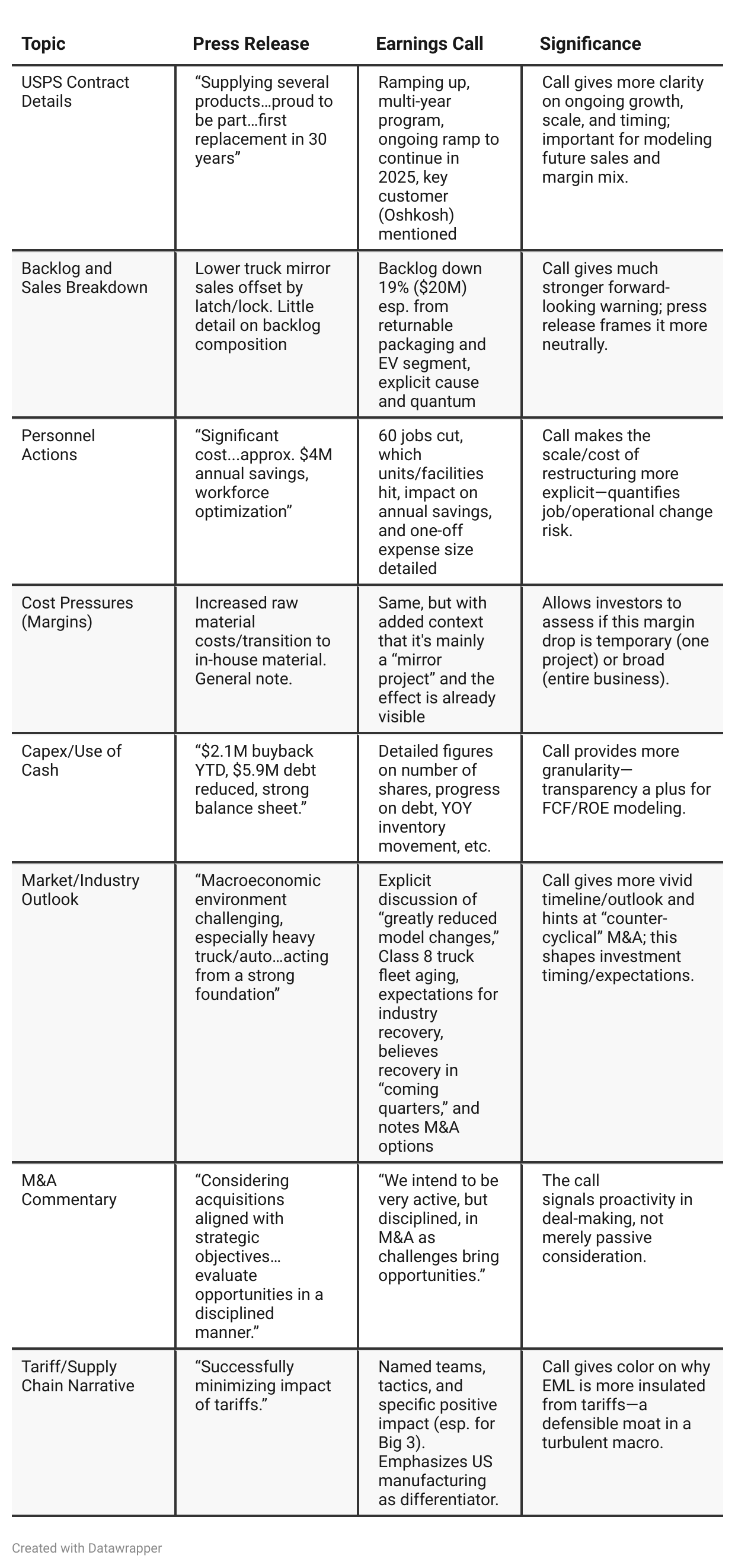

Press Release vs Call Transcript Comparison

Transparency Level: The call is more candid about the future being tough (backlog, industry headwinds), whereas the press release is more polished and positive.

Adjusted Metrics: The press release references non-GAAP numbers but the call walks listeners through what the normalization is and how restructuring affects profit—crucial for modeling true run-rate profit.

Leadership/Strategy Refresh: Only in call do we really hear about a “new leadership team in place” and “strategic refresh”—signals culture change that could precede new initiatives or M&A philosophy.

Investor Focus: Both documents aim to reassure investors with cost controls, strong cash flow, and buybacks, but the call is more direct in managing expectations for a slow near-term and an acquisition-led growth future.

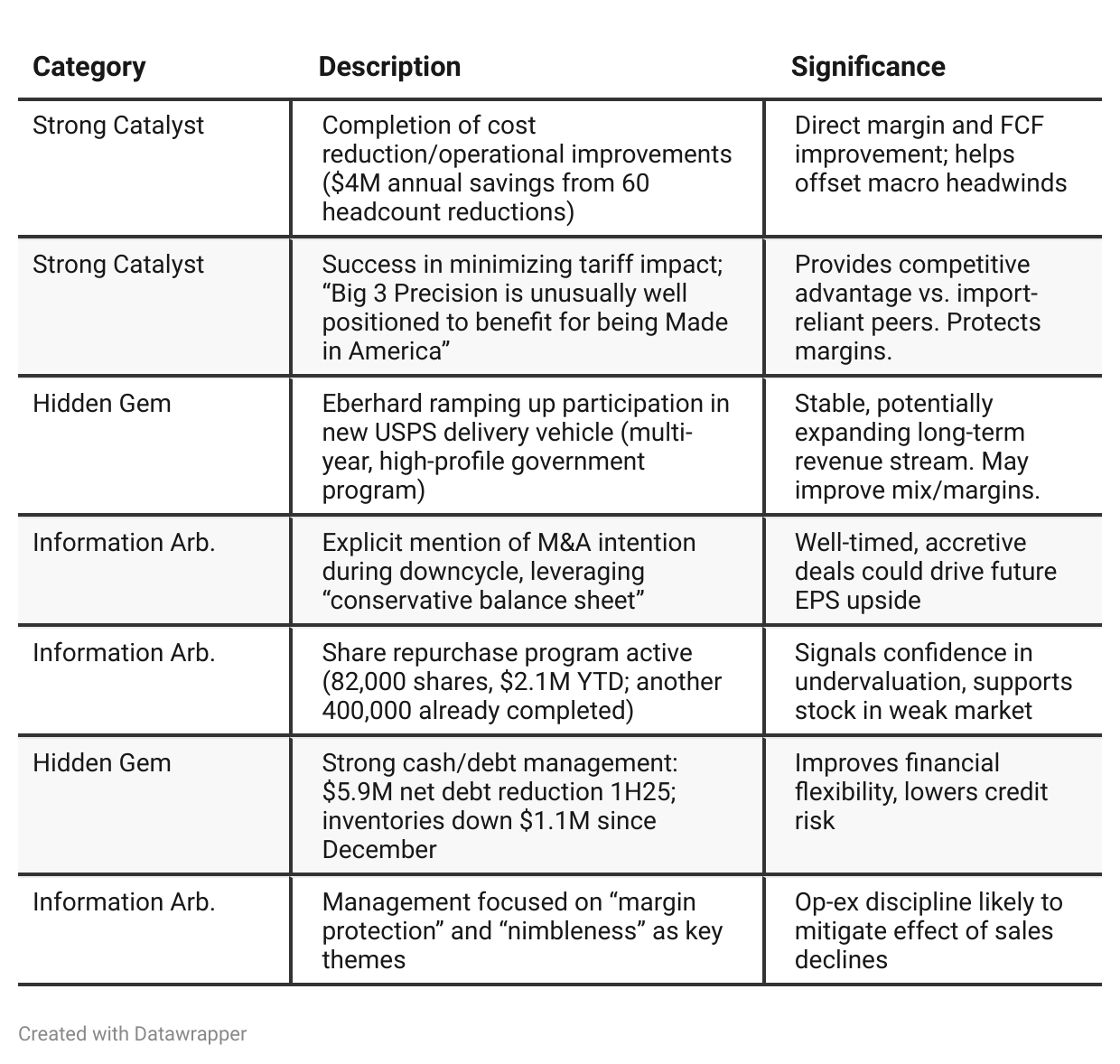

Positive Insights

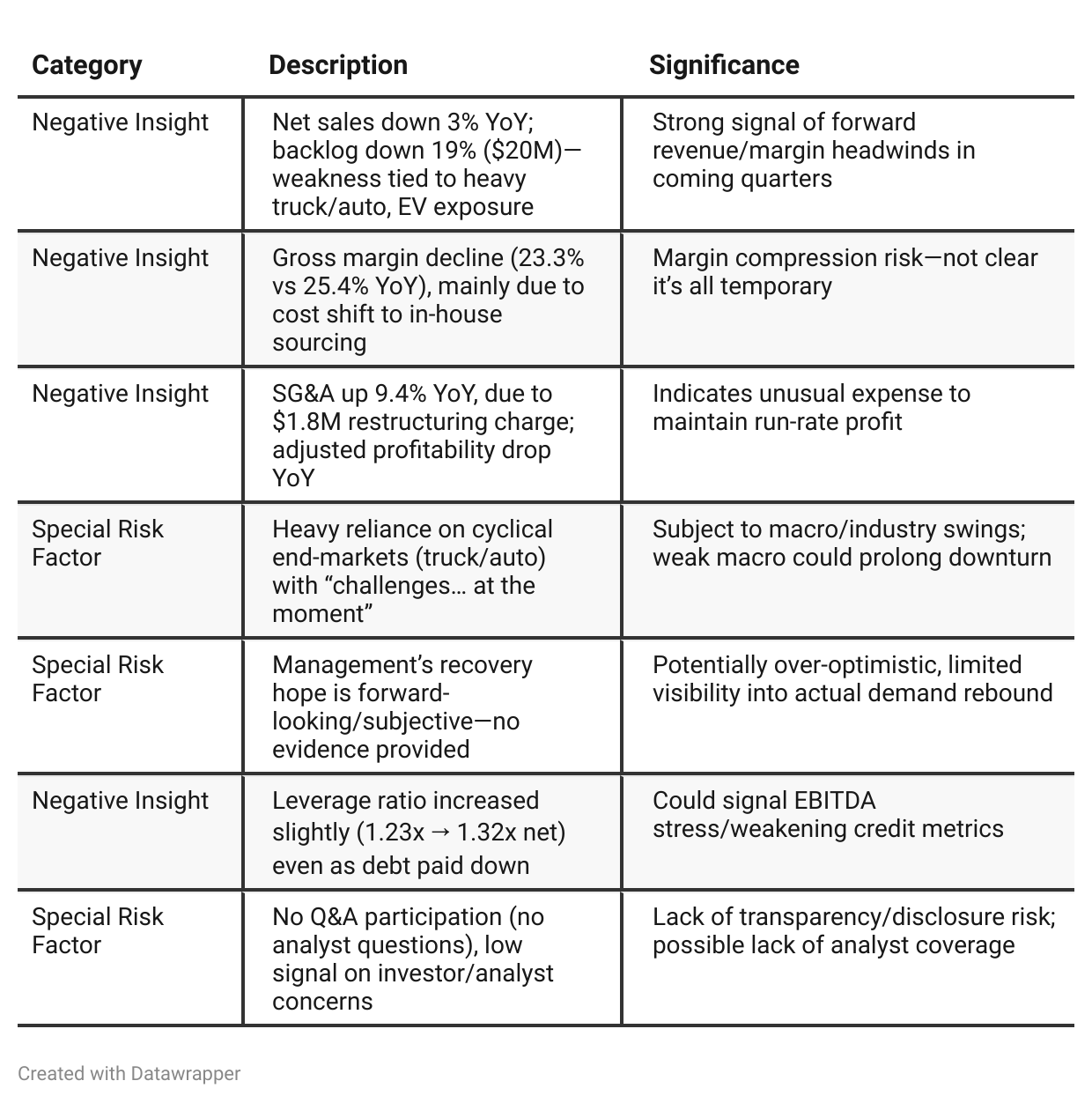

Negative Insights

Tariff Risk

Tariff exposure was directly addressed on the call—management stated that teams have “virtually neutralized” the tariff impact on the P&L, and that Big 3 Precision’s U.S. manufacturing footprint gives it a “Made in America” advantage. This not only mitigates input cost risks but could also support market share gains if foreign competitors remain tariff-disadvantaged. The company appears to be adjusting its supply chain proactively and prioritizing domestic operations to maintain cost and pricing advantages. There were no specific forward-looking negatives noted on tariff risks, and management’s confident tone suggests these have been “handled” for now—an underappreciated defensive asset versus peers. Investors should continue to monitor for any new tariff actions, trade policy changes, or evidence that mitigation strategies are losing effectiveness.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: The Eastern Company entered the year in transformation mode—completing major structural moves, strengthening its leadership, and positioning its balance sheet and operations for both resilience and future growth. Management was vocal about relentless execution, cost control, and the ability to “jump on” demand if and when markets recovered. While cautious given macro/industry softness and tariffs, leadership sounded optimistic about the company’s competitive moat ("Made in America") and refreshed M&A ambitions.Q2 2025: By the next quarter, the tone shifted a bit more defensive and pragmatic. Market headwinds have deepened, with significant revenue and backlog declines, further margin erosion, and sharper cost actions. However, Eastern no longer just promises transformation—it reports its completion (cost cuts, site closures, streamlining). Rather than projecting near-term growth, management focuses on margin protection and maintaining strategic flexibility. The company highlights the major USPS program as a key long-term driver and stresses readiness to make the most of industry distress through disciplined M&A. The narrative moves from active transformation for future opportunity to defensive execution and positioning for an eventual market rebound.

Year-over-year comparison

Q2 2024: Eastern was in a growth and transformation mode, leveraging agility to win new business and grow backlog. The messaging emphasized operational progress, flexibility, new customer wins, and margin expansion despite acknowledging some market headwinds.

Q2 2025: The story pivots to defense and survival as demand weakens. Management focuses on aggressive cost control, restructuring, and safeguarding the business against extended industry softness. Long-term optimism remains (especially regarding USPS and possible M&A), but short-term caution and execution discipline dominate the messaging. Growth levers are now framed as future opportunities to pursue once the market stabilizes rather than immediate catalysts.

Final Takeaway

The Eastern Company is in a restructuring and margin-protection phase, concentrating on cost efficiency, selective growth (USPS, M&A), and capital discipline amid significant sector demand headwinds. While management’s proactive expense control and cash focus are strong positives, the notable decline in backlog and top-line sales, coupled with dependency on cyclical markets, mean that near-term earnings risk remains. Execution on cost savings, effective margin management, and timing of end-market recovery will be critical in determining the next leg for the stock. Verdict: Hold, with the view that visibility on demand or real new contract ramp (esp. USPS) could justify a future upgrade; risk is further topline/GM deterioration or failed demand recovery.