Donnelley Financial Solutions, Inc. (NYSE: DFIN) – Q3 2025 Earnings

Donnelley Financial Solutions, Inc. (NYSE: DFIN) – Q3 2025 Earnings

Earnings Release Date: Oct. 29, 2025

Stock Price: $51.70

Market Cap: $1442.4 million

Q3 2025 sales of $175.3 million vs $179.5 million in the prior year

Q3 2025 EPS of -$1.49 vs $0.29 in the prior year

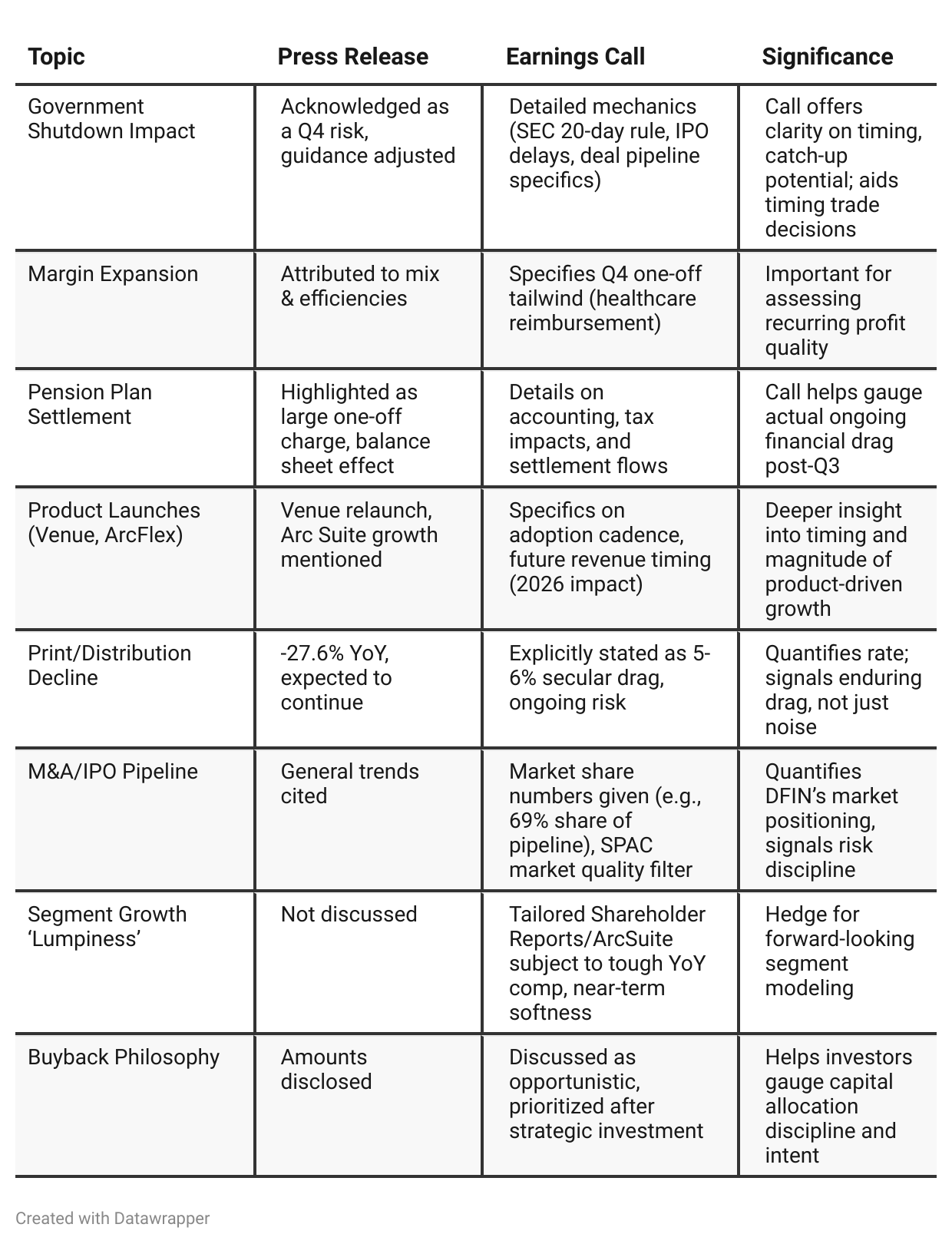

Press Release vs Call Transcript Comparison

Transparency & Guidance: The call adds important color/context to reported numbers, especially nuances in margin quality, capital deployment, and macro event risk.

Execution Discipline: DFIN’s filtering of low-quality SPACs (call only) suggests management is prioritizing long-term client value and sustainable ARR over near-term revenue “at any cost.”

Leverage: Leverage remains low (0.6x net), offering considerable flexibility, even after pension settlement and buybacks.

Pension Settlement: While optically painful (GAAP loss), the settlement improves flexibility and reduces future volatility—important for cash flow modeling.

Cash Burn/Working Capital: Slide in cash is a yellow flag, but manageable given overall liquidity/backstop.

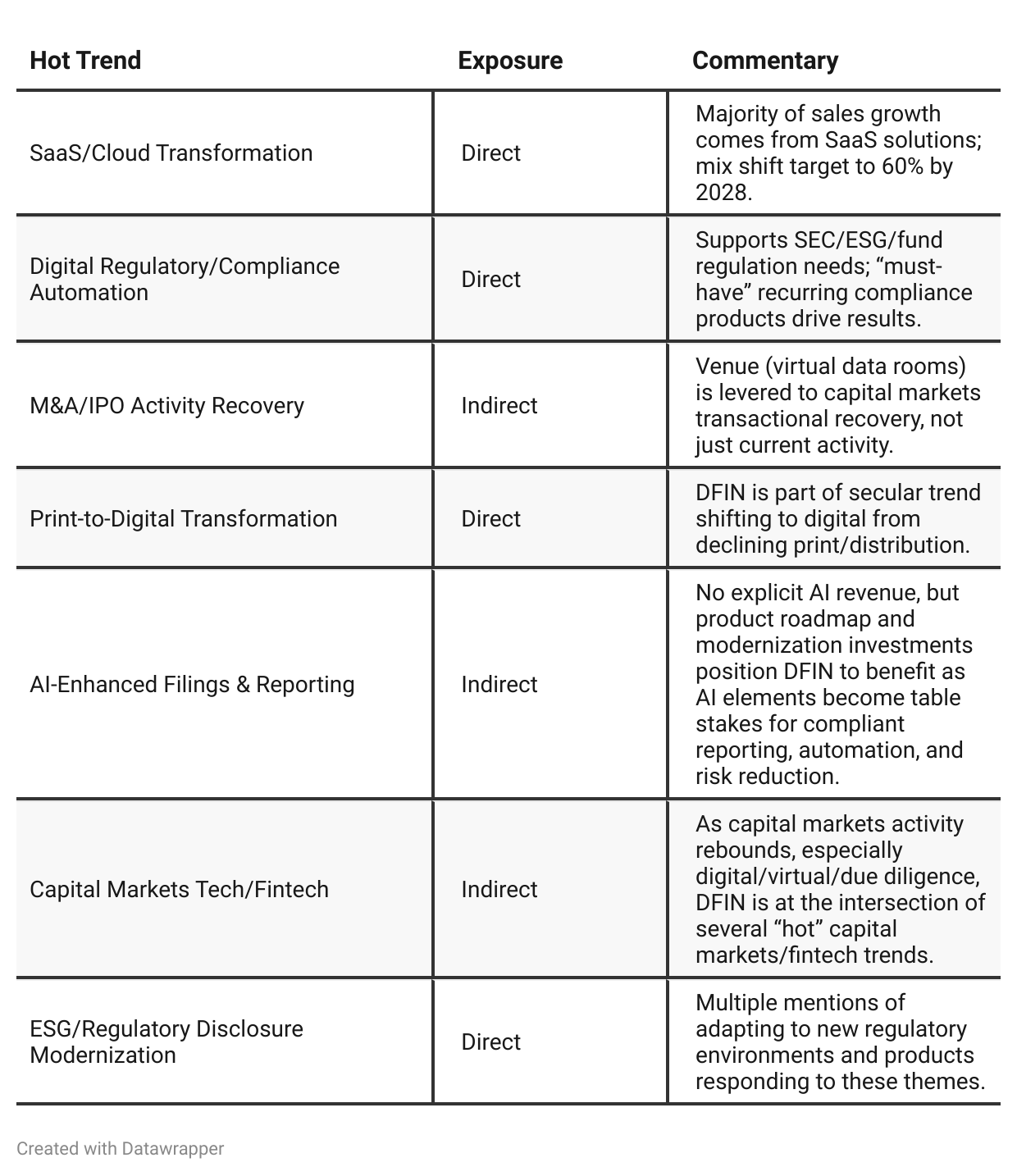

Hot Trend Leverage: DFIN’s exposure to regulatory/SaaS/AI/M&A automation themes is increasingly evident, with the secular decline in print being actively managed.

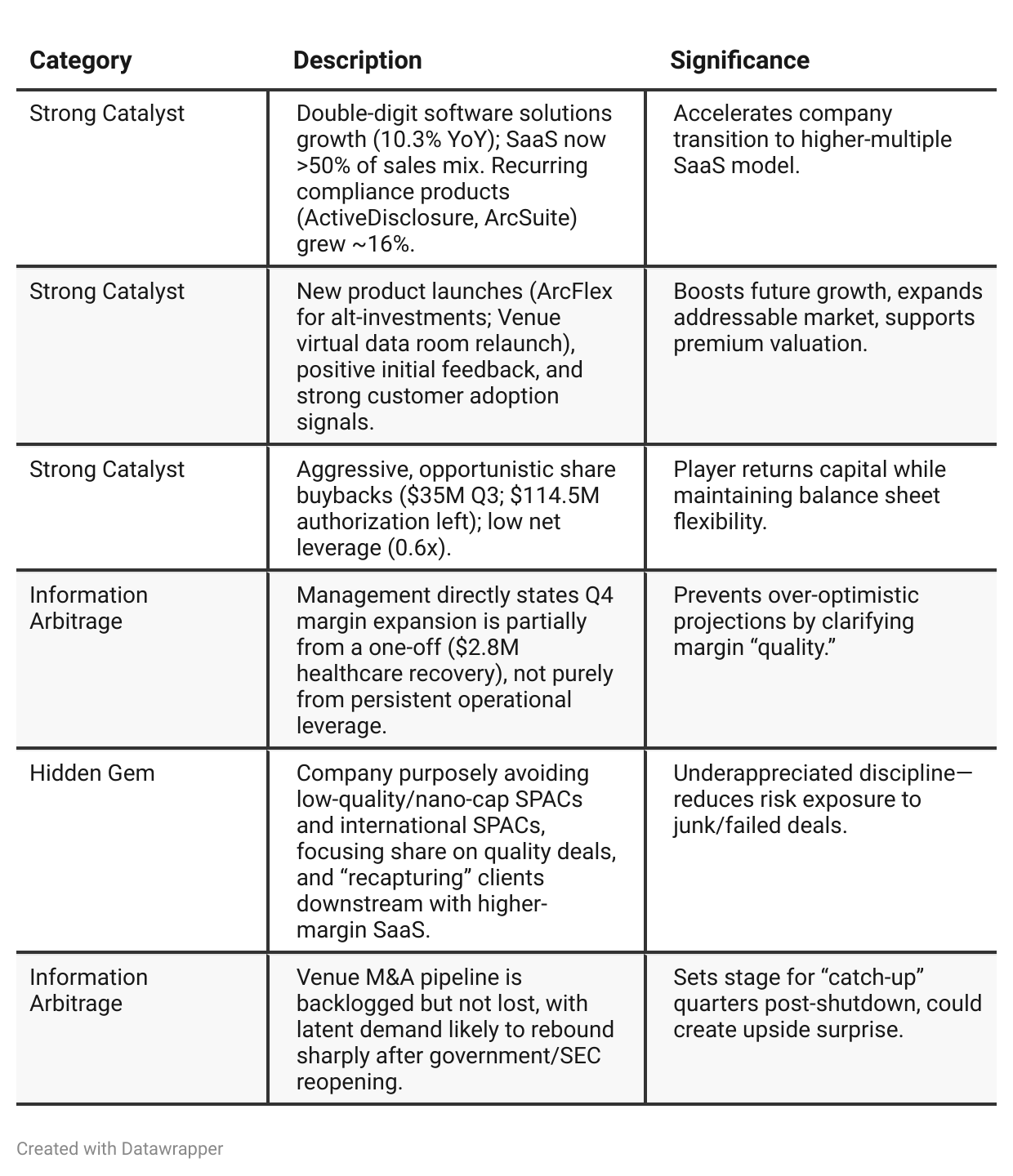

Positive Insights

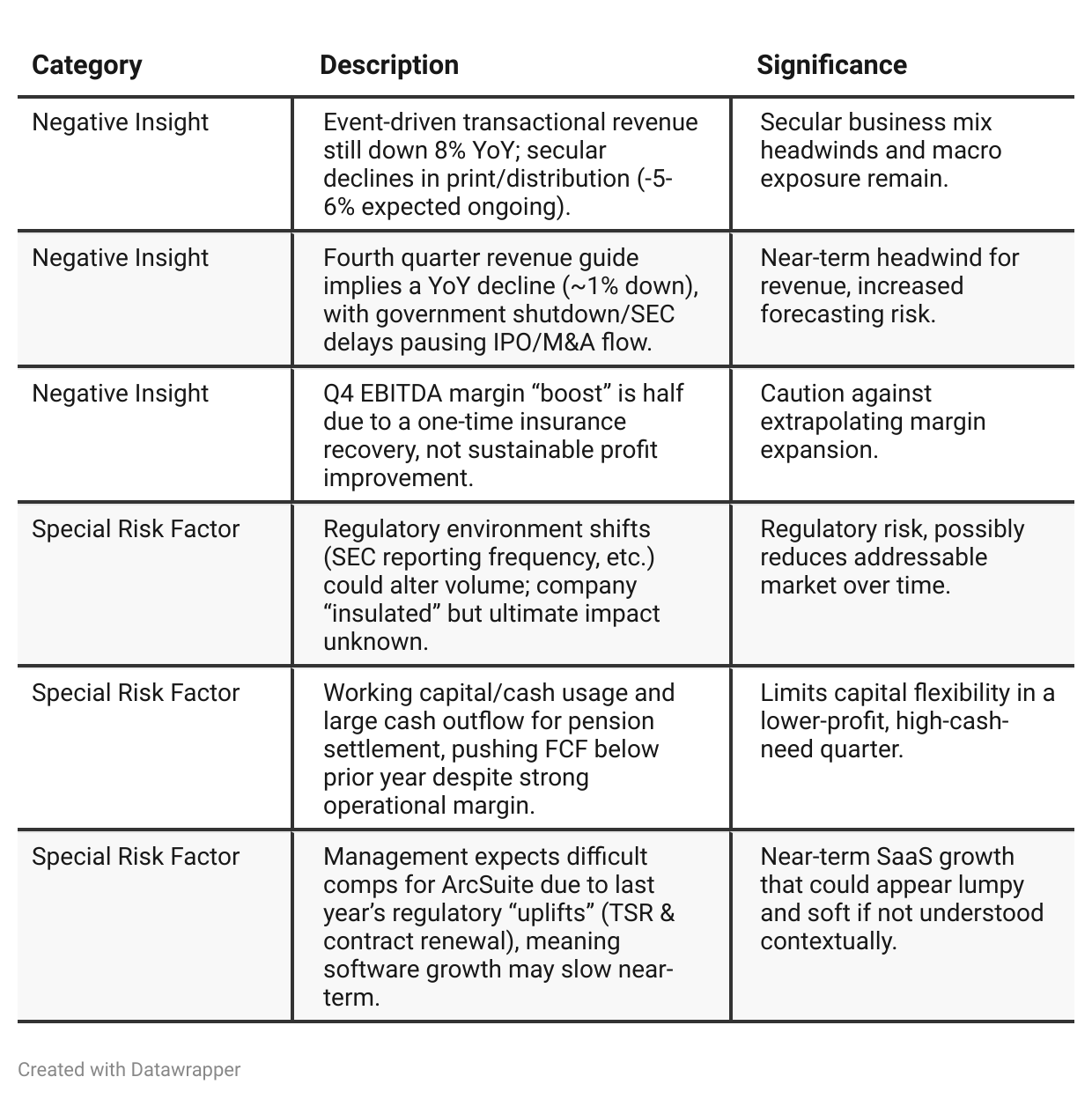

Negative Insights

Tariff Risk

No references to U.S. tariffs or trade policy were found in the transcript. There was no discussion of exposure to supply chain disruption, cost inflation, market share shifts, or pricing strategy changes related to tariffs. No mitigating actions, forward-looking projections, or any impact from global trade policy were mentioned by management or analysts. There is no evidence that tariffs are currently a material factor for DFIN’s business model or outlook.

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025: DFIN’s narrative was one of resilient adaptation and steady transformation. Despite a gloomy market start, improving activity and strong execution on margin, cash flow, and SaaS growth set a positive tone. Management stressed structural shifts, process execution, and a gradual but consistent move towards a higher-margin, software-based model, using FCF for disciplined buybacks and strategic flexibility. External factors were a headwind but improving.Q3 2025: The story shifted from gradual improvement to “strategic execution amidst uncontrollable turbulence.” While DFIN’s strategy (SaaS transformation, selective capital deployment, high-quality deal focus) is unchanged and steadily progressing—now augmented by product launches and customer wins—unforeseen macro obstacles (the prolonged SEC/government shutdown) have paused revenue recognition and dampened near-term outlook. Management is more explicit about guidance caution, transparent about non-operating margin boosts, and laser-focused on being ready to capitalize on a deal rebound once the policy bottleneck clears.

Year-over-year comparison

Q3 2024: DFIN’s message was “we’re leading the regulatory transformation and executing our SaaS transition,” riding strong growth in recurring software revenue, new product wins, and customer adoption even as legacy events and capital market ops were subdued. Management projected confidence that operating leverage, innovation, and disciplined capital allocation would deliver steady progress and prepare DFIN for an eventual market rebound.

Q3 2025: The narrative matures to: “our SaaS transition and innovation remain intact, but external realities—namely the SEC shutdown—have forced revenue and deal activity into a temporary pause.” Management is still confident, but is now emphasizing transparency, readiness for a sharp rebound, and patience. The conversation shifts from pursuit of incremental improvement to deliberate navigation of macro turbulence, with even more attention on recurring revenue and anticipating pent-up pipeline demand. New launches and operational improvements continue, but near-term growth is now limited more by forces beyond DFIN’s control than internal execution.

Final Takeaway

Donnelley Financial Solutions (DFIN) is in a strategic SaaS-led transformation phase, steadily shifting away from legacy print/services and deepening its recurring revenue base. Top-line growth and margin expansion are driven by subscription software, innovation, and new products, but the government shutdown has paused much of their deal-driven growth and delayed key revenue streams. Management is disciplined in capital deployment, opportunistic on buybacks, and prudent on quality, but risks remain from macro shocks and regulatory shifts. Verdict: HOLD, with tactical upside contingent on post-shutdown deal rebound and continuing SaaS execution. Investors should watch for confirmation that deal volumes normalize and margin expansion is sustained absent non-recurring boosts.