Donnelley Financial Solutions, Inc. (NYSE: DFIN) – Q2 2025 Earnings

Donnelley Financial Solutions, Inc. (NYSE: DFIN) – Q2 2025 Earnings

Earnings Release Date: Jul. 31, 2025

Stock Price: $63.86

Market Cap: $1768.9 million

Q2 2025 sales of $218.1 million vs $242.7 million in the prior year

Q2 2025 EPS of $1.49 vs $1.66 in the prior year

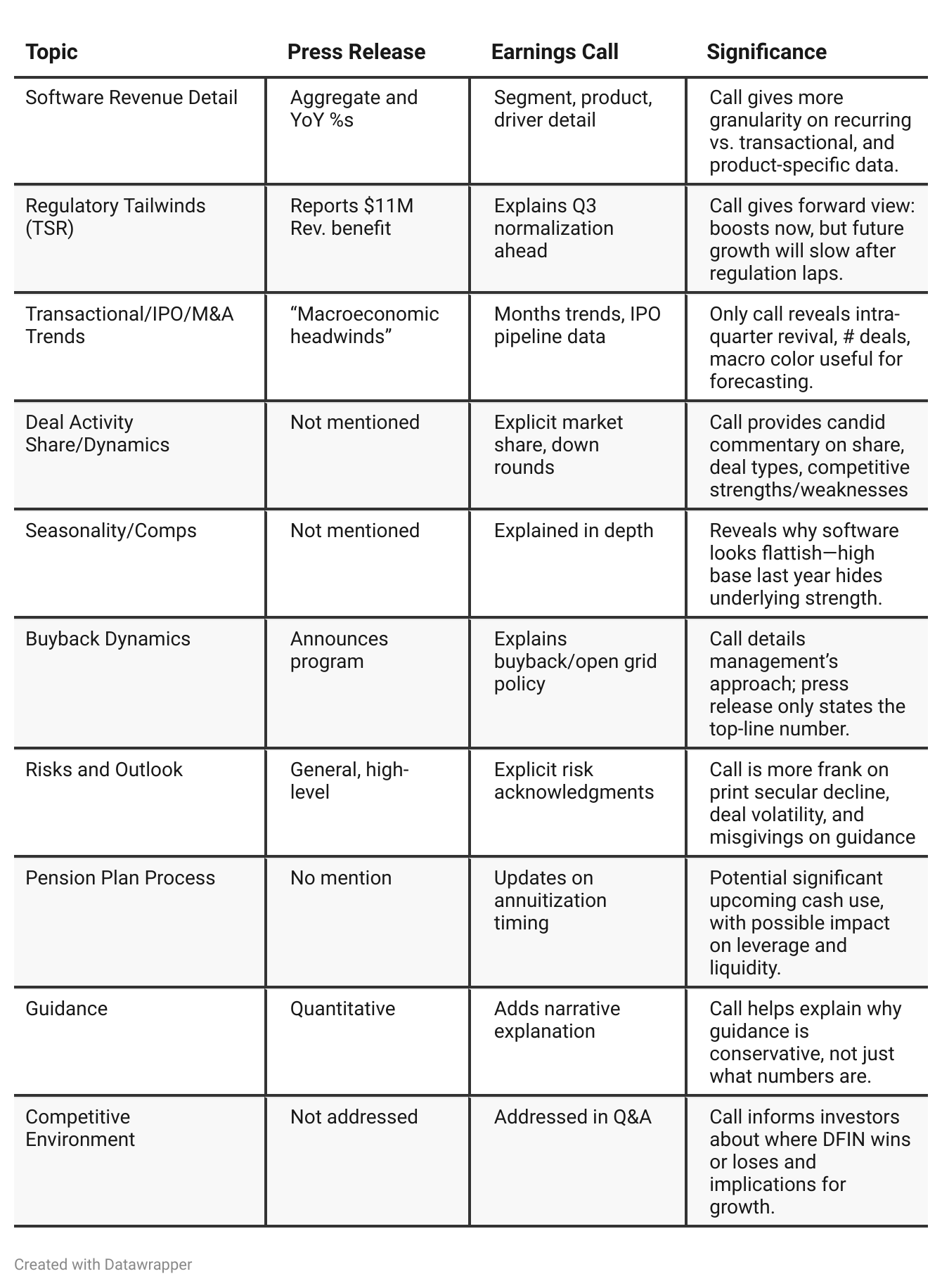

Press Release vs Call Transcript Comparison

Transformation is on Track: Both documents reinforce the seriousness and progress of the shift to software and recurring revenues.

Margins Holding Up: Despite sales declines, strong cost controls and mix shift keep EBITDA margins among company highs.

Balance Sheet is Healthy: Cash flow, low leverage, and capital return remain robust, supporting financial flexibility.

Q3 Caution Warranted: Both documents note “ongoing headwinds” into Q3; not just a company issue, but sector and market factor.

Print Revenue Will Continue Falling: Multiple explicit warnings that this is a secular—not cyclical—decline.

TSR was a One-Off Spike: Investors should not annualize Q1-Q3 Arc Suite/TSR growth rates.

Buyback Opportunity is Valuation Sensitive: Management’s “valued grid” approach suggests they are careful stewards, but could also mean less downside support if stock price rebounds too far, too fast.

Deal Activity Still Uncertain: Some green shoots, but management not counting on a rapid boom; visibility is lowest in this (cyclical) segment.

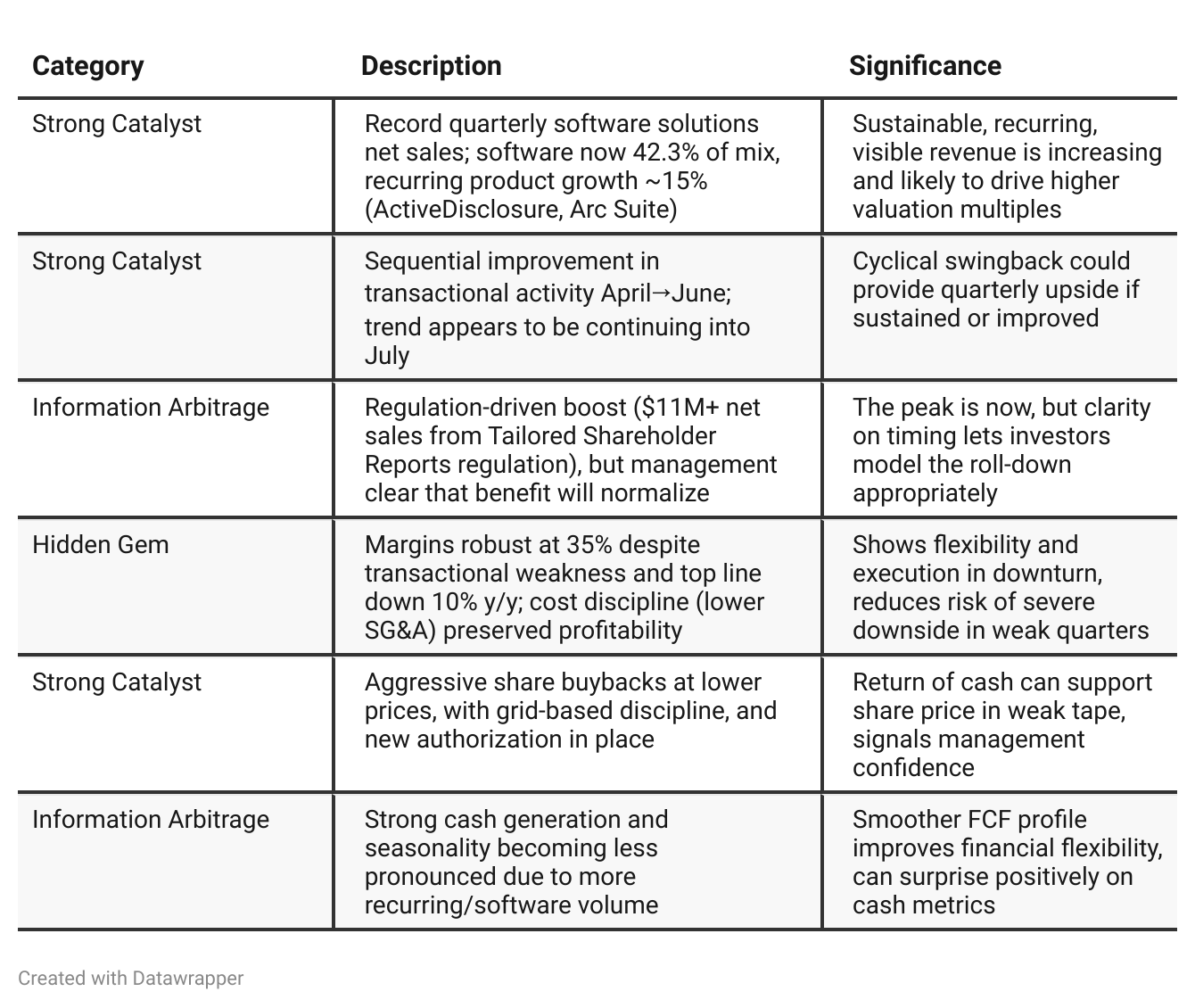

Positive Insights

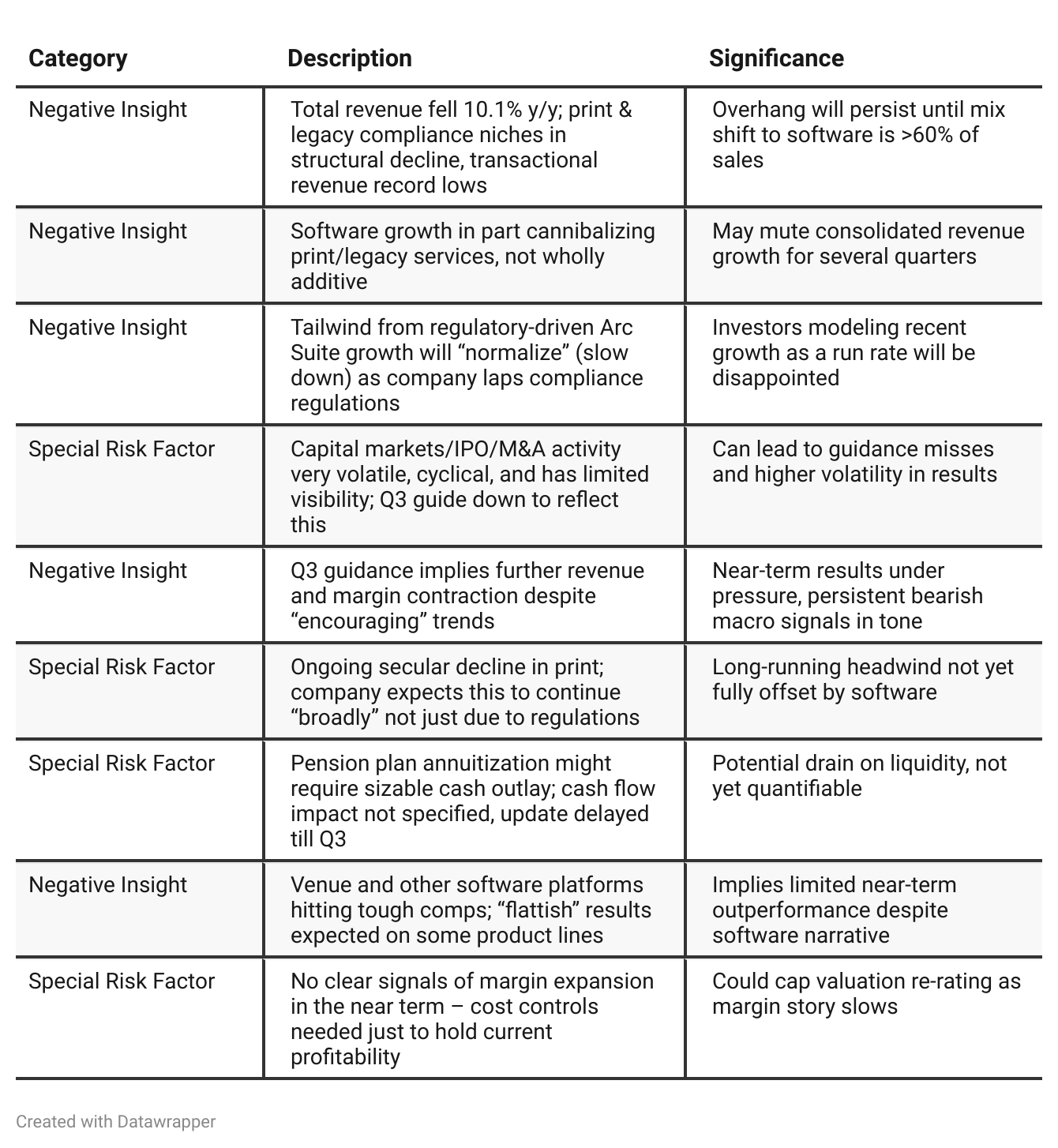

Negative Insights

Tariff Risk

Tariffs were explicitly mentioned as causing a “significant short-term impact” on transactional offerings (i.e., IPO, capital market deal volume) in the quarter. This was followed by a sequential improvement as the quarter progressed, suggesting recovery from the immediate shock.

No evidence of supply chain issues, cost inflation, or margin squeeze tied directly to tariffs—impacts appear on the demand side (i.e., deal flow sensitive to macro/trade headlines).

Management is not flagging any operational or supply chain adjustments in response to tariffs.

Trade “headline risks” and “policy shifts” are cited as ongoing uncertainties for transactional volumes, in line with their commentary on macro/market unpredictability.

No forward guidance or mitigation strategies articulated beyond acknowledgment of risk and monitoring market response.

Sentiment Analysis

The overall sentiment toward $DFIN is neutral. While there are a few positive notes such as praise for company analysis, mention of customer wins, and excitement about IPO activity (which could benefit DFIN), there are also notable concerns about disappointing quarterly results, margins, customer retention metrics (GRR), and a cautious Q3 outlook despite improving market conditions. Enthusiasm over buybacks is tempered by worries about operational performance. The balance of bullish and bearish viewpoints results in an overall neutral sentiment.

Previous Earnings Call

Quarter-over-quarter comparison

In Q1 2025, DFIN exuded confidence as its software transformation and cost control strategies yielded record margins and positive mix shift progress. The management emphasized aggressive buybacks at low prices, strong recurring revenue momentum, and felt protected from macro risks thanks to its business model. Regulatory change (TSR) was framed as a major driver of software revenue growth.By Q2 2025, management’s tone became more cautious. While the narrative remains one of successful transformation—with software solutions increasingly dominant—the call clearly acknowledges macro headwinds: steep sequential and YoY declines in transactional and print revenue, the normalization/decline of regulatory tailwinds as they lap the initial TSR surge, and uncertainty from tariffs and trade. Guidance is reset lower for both revenue and margin, and management frames the next phase as one of stabilization, margin defense, and prudent capital deployment, rather than outperformance. Investors are repeatedly cautioned that legacy headwinds and market volatility are not abating quickly, and that modeling high growth from recent regulatory wins would be unrealistic going forward.

Year-over-year comparison

In Q2 2024, DFIN told a confident story of accelerating software growth, record margins, market share wins, and transformation-driven momentum, powered by both regulatory catalysts and strong operational execution. While legacy print was acknowledged as declining, it was more than offset by new business, and management suggested that DFIN was entering a new phase of sustainable, structural growth.

By Q2 2025, the company’s tone and messaging have notably shifted. Management emphasizes the resilience of the model and the company’s ability to withstand ongoing, sharper headwinds: pronounced transactional and print declines, waning windfall from regulatory change, and external risks like tariffs and muted capital market activity. Current focus is on margin preservation, prudent capital deployment, and defensive strategies rather than expansion. Growth is now driven mainly by smaller, steadier improvements in software lines, but without the tailwinds that made the prior year's narrative so bullish. DFIN’s message has evolved from confident outperformance to one of pragmatic adaptation.

Final Takeaway

Donnelley Financial Solutions (DFIN) is in a late-stage transformation phase, pivoting towards a recurring software-driven business model while managing the secular decline of its print and transactional revenue base. Short-term upside is limited by regulatory growth normalizing, continued print headwinds, and volatile transactional demand. Disciplined execution, margin defense, and capital return strategy are all positives, but evidence of sustainable topline growth is needed before a more constructive view is warranted. Expect execution on cash flow, margin stability, and new software wins (post-regulation) to be critical for future performance. Verdict: HOLD, with balanced risk/reward, awaiting a clear inflection in underlying revenue or transactional environment.