DATA Communications Management Corp. (OTCQX: DCMDF/DCM.TO) – Q3 2025 Earnings

DATA Communications Management Corp. (OTCQX: DCMDF/DCM.TO) – Q3 2025 Earnings

Press release and earnings call link

Earnings Release Date: Nov. 11, 2025 (all figures in Canadian dollars)

Stock Price: $0.91

Market Cap: $50.2 million

Q3 2025 sales of $79.8 million vs $69.8 million in the prior year

Q3 2025 EPS of $0.12 vs ($0.09) in the prior year

Overview:

DCM (TSX: DCM / OTCQX: DCMDF) is a Canadian print and digital communications company that helps large enterprises and public agencies manage complex marketing workflows, regulatory communications, and customer engagement.

Revenue Drivers:

Core revenue stems from print-based marketing and business communications, transactional mail, large-format and label printing, packaging, and—more recently—digital workflow and AI-enabled software platforms such as ContentCloud.ai and CCM 360 (customer communication management).

Customer Base:

Serves ~2,500 clients, including 70 of Canada’s 100 largest corporations, plus major government and financial institutions.

Market Positioning:

The market leader in integrated print-digital communications in Canada, evolving from a mature print consolidator to a tech-enabled hybrid player.

Financial Trajectory:

Revenue down 3.1 % YoY to $105 M, yet profitability stable (Adj. EBITDA margin 11.7 %), SG&A reduced by ~15 %. The company generates solid free cash flow and is reducing net debt (down to $80.6 M).

Strategic Focus (2025):

Accelerate digital transition via AI-powered platforms

Pursue disciplined M&A (esp. labels, large-format, packaging)

Maintain capital returns (dividend + share buyback) while deleveraging

Drive operational efficiency and margin expansion

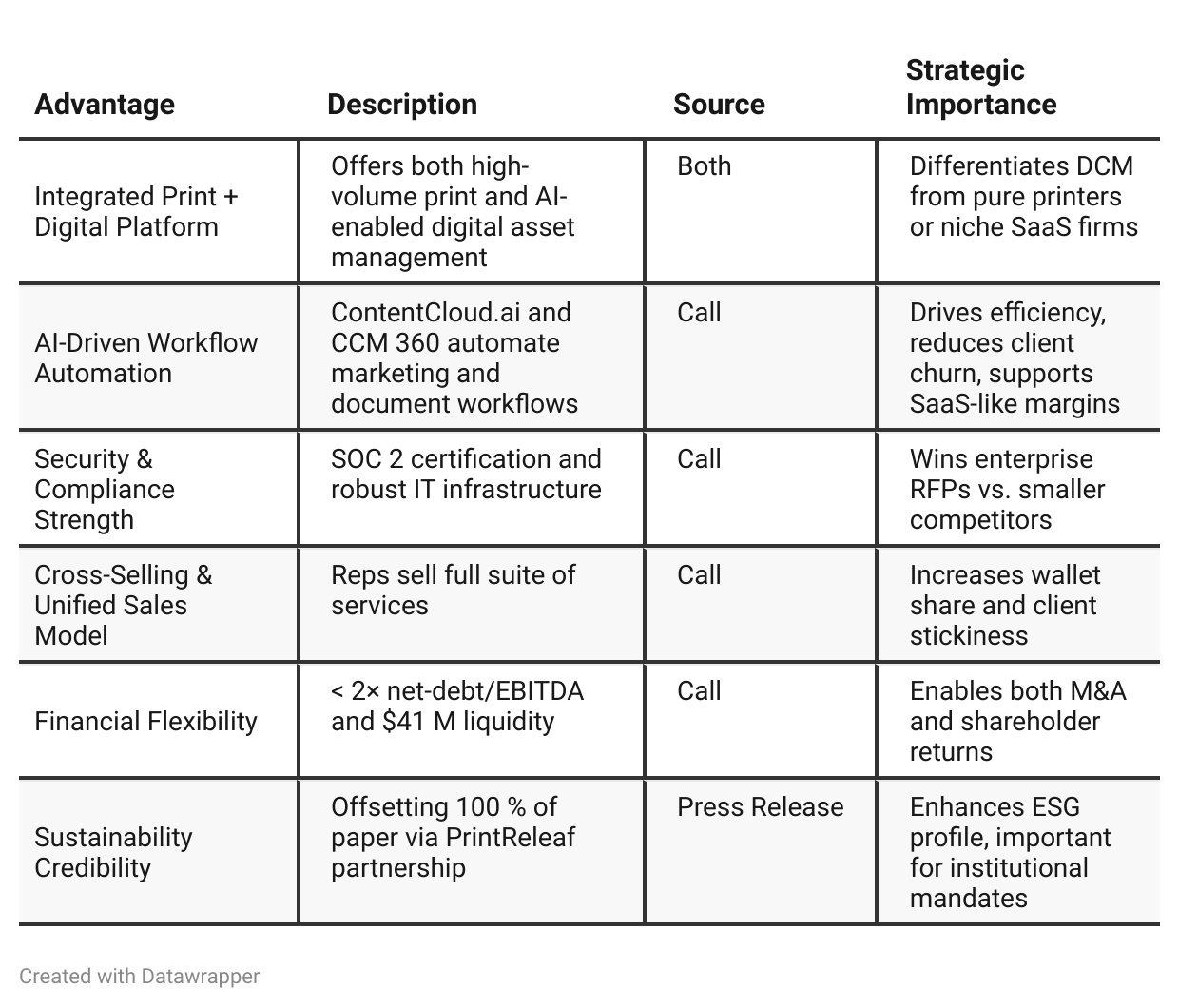

Competitive Advantage Insights

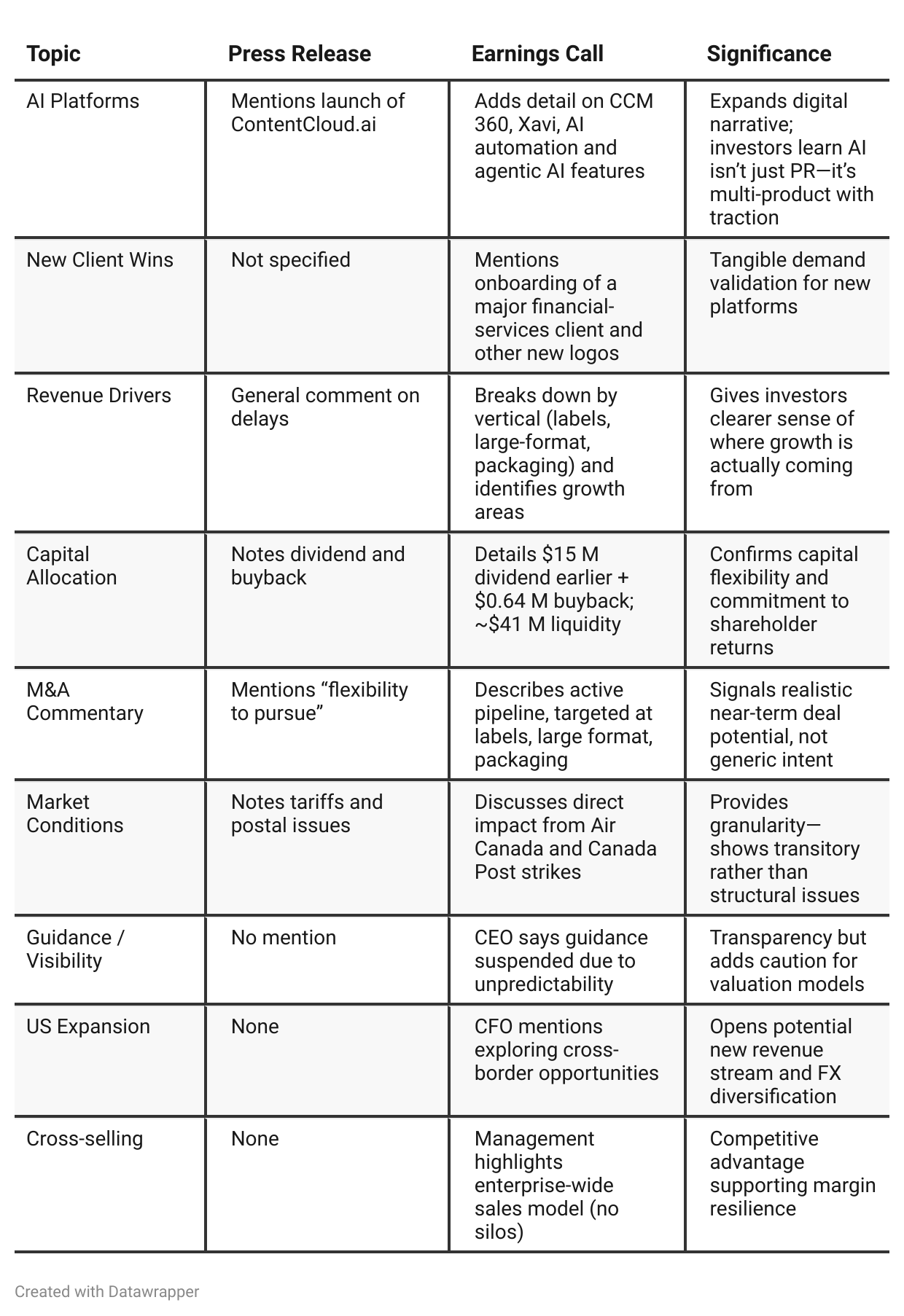

Press Release vs Call Transcript Comparison

The call showcases operational agility: SG&A down 15 %, R&D stable → management can flex cost base without hurting innovation.

Analyst Q&A revealed security compliance (SOC 2) as a competitive differentiator, supporting wins vs. smaller competitors.

DCM emphasized SaaS-like recurring revenues in tech-enabled services (subscription and license models) that will scale gradually.

Tone shift: the press release reads defensive (“navigating uncertainty”), whereas the call projects controlled optimism (“all in on growth”).

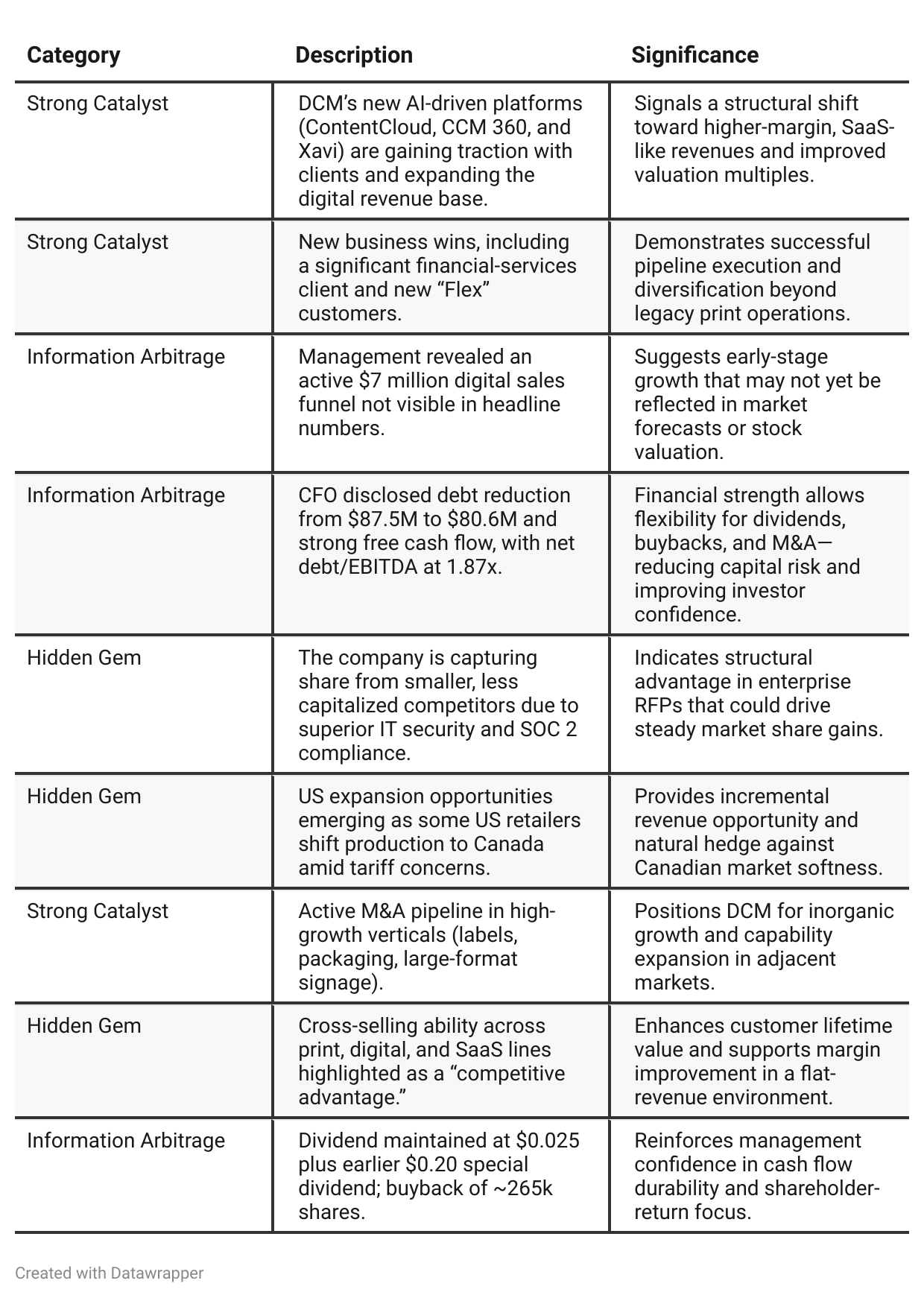

Positive Insights

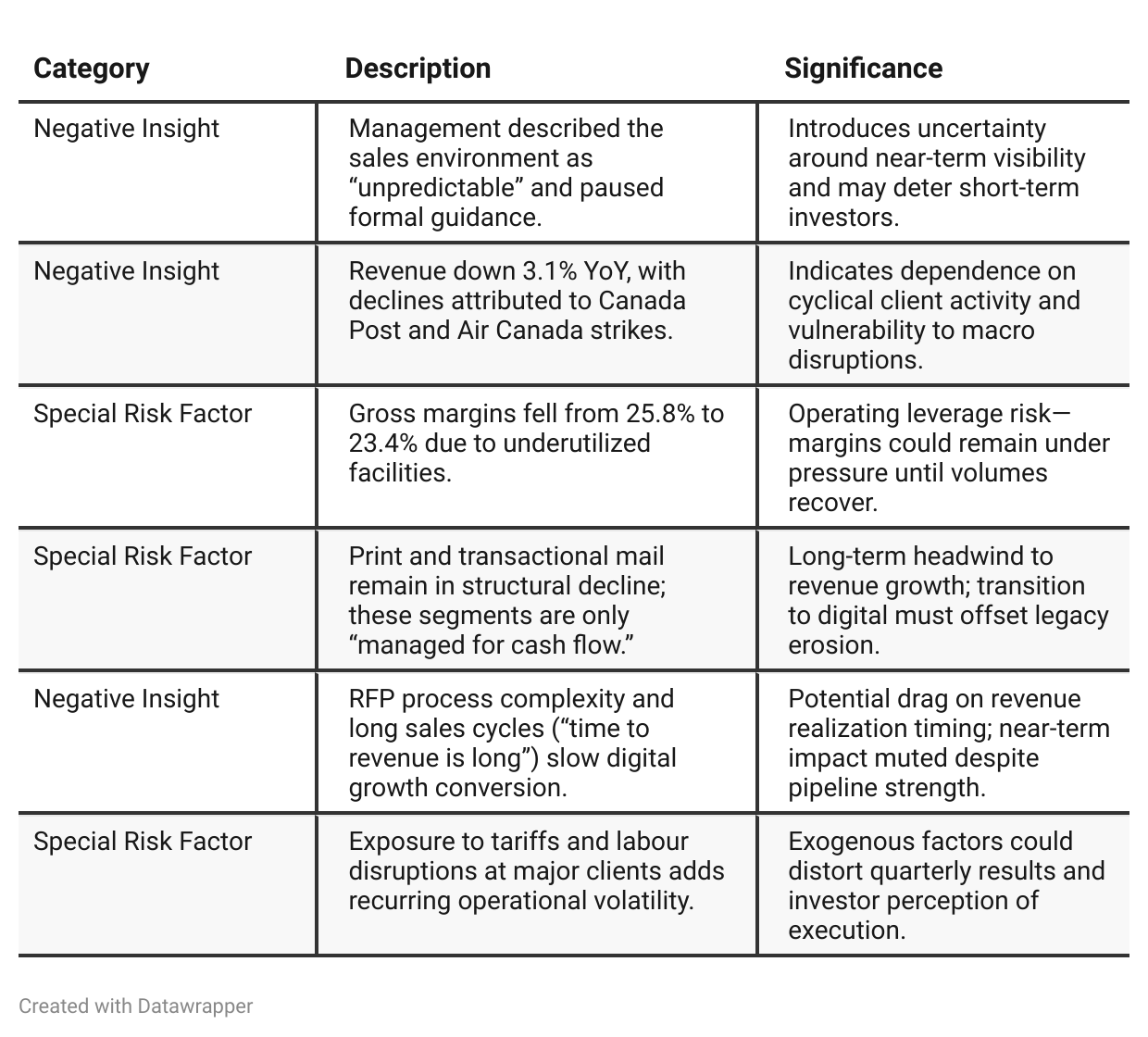

Negative Insights

Investor Underappreciation Signals

✅ AI Platform Depth — Beyond ContentCloud.ai, DCM now markets a full suite (ContentCloud, CCM 360, Xavi) with live clients and $7 M funnel. Investors may still price DCM as a print company, but these recurring digital revenues can re-rate valuation once growth proves durable.

✅ Operating Leverage Recovery — Gross margin compression is mainly from under-utilized plants due to strikes; when volumes return, fixed-cost absorption could lift EBITDA sharply, a lever the market may not model in.

✅ M&A Optionality — Management confirmed active, accretive deal flow in labels and packaging. With < 2× net-debt/EBITDA, DCM has dry powder. Investors might underestimate near-term deal probability given robust pipeline comments.

✅ Cross-Selling Engine — Unified salesforce sells across print + digital lines, raising wallet share. Investors may overlook this structural margin enhancer because it’s embedded in SG&A improvements rather than explicit segment disclosure.

✅ U.S. Tariff Arbitrage — Canadian-based servicing of U.S. retailers shifting production north due to tariff fears opens incremental share gains that aren’t yet in consensus expectations.

Tariff Risk

Tariffs were directly mentioned as a factor reducing business confidence and driving U.S. retailers to shift production into Canada—a double-edged sword.

Impact: Tariff uncertainty is currently dampening client marketing spend.

Mitigation: DCM benefits indirectly as some U.S. firms localize Canadian operations, creating incremental demand for DCM’s services.

Forward View: If tariffs persist or escalate, domestic demand may partially offset losses from cross-border exposure.

Net Effect: Neutral-to-slightly positive; tariffs act as both a short-term drag and a long-term localization catalyst.

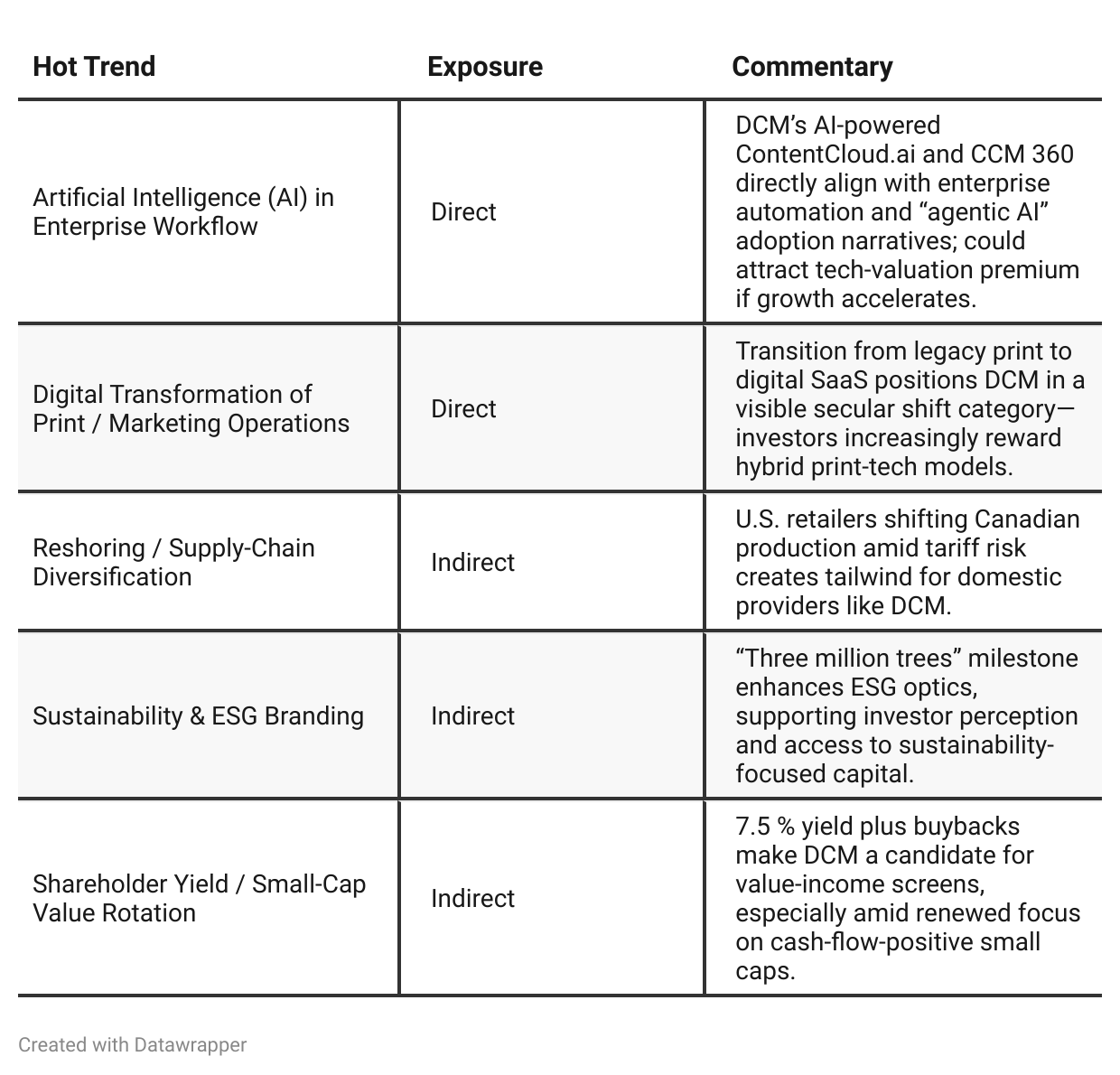

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Earlier Call (Q2 2025)

DCM’s narrative was one of resilience under duress. Management spent much of the call emphasizing stability amid macro disruptions (tariffs, postal strikes, cautious clients). The focus was defensive — protecting EBITDA margins, preserving clients, and maintaining cash flow while laying the groundwork for digital expansion.Latest Call (Q3 2025)

By Q3, the story evolves into confidence and digital traction. The tone shifts to controlled execution — AI-enabled products are no longer aspirational but monetizing. Management is actively buying back shares, reducing leverage, and maintaining dividends, signaling internal confidence.Year-over-year comparison

—

Final Takeaway

DATA Communications Management Corp. is in a transformation phase, moving from print-heavy operations to a digitally driven, AI-enabled platform. Key growth drivers include new enterprise wins, AI-enabled products, and accretive M&A opportunities. While revenue visibility is limited due to macro headwinds and client caution, cost discipline and strong cash flow support dividends and share repurchases.

Verdict: BUY, with medium-term upside as digital traction converts to sustainable top-line growth. Short-term volatility possible due to market uncertainty and legacy segment drag.