DATA Communications Management Corp (OTCQX: DCMDF) – Q2 2025 Earnings

DATA Communications Management Corp (OTCQX: DCMDF) – Q2 2025 Earnings

Earnings Release Date: Aug. 6, 2025

Stock Price: $1.09

Market Cap: $60.2 million

Q2 2025 sales of $113.8 million vs $125.8 million in the prior year

Q2 2025 EPS of $0.07 vs $0.07 in the prior year

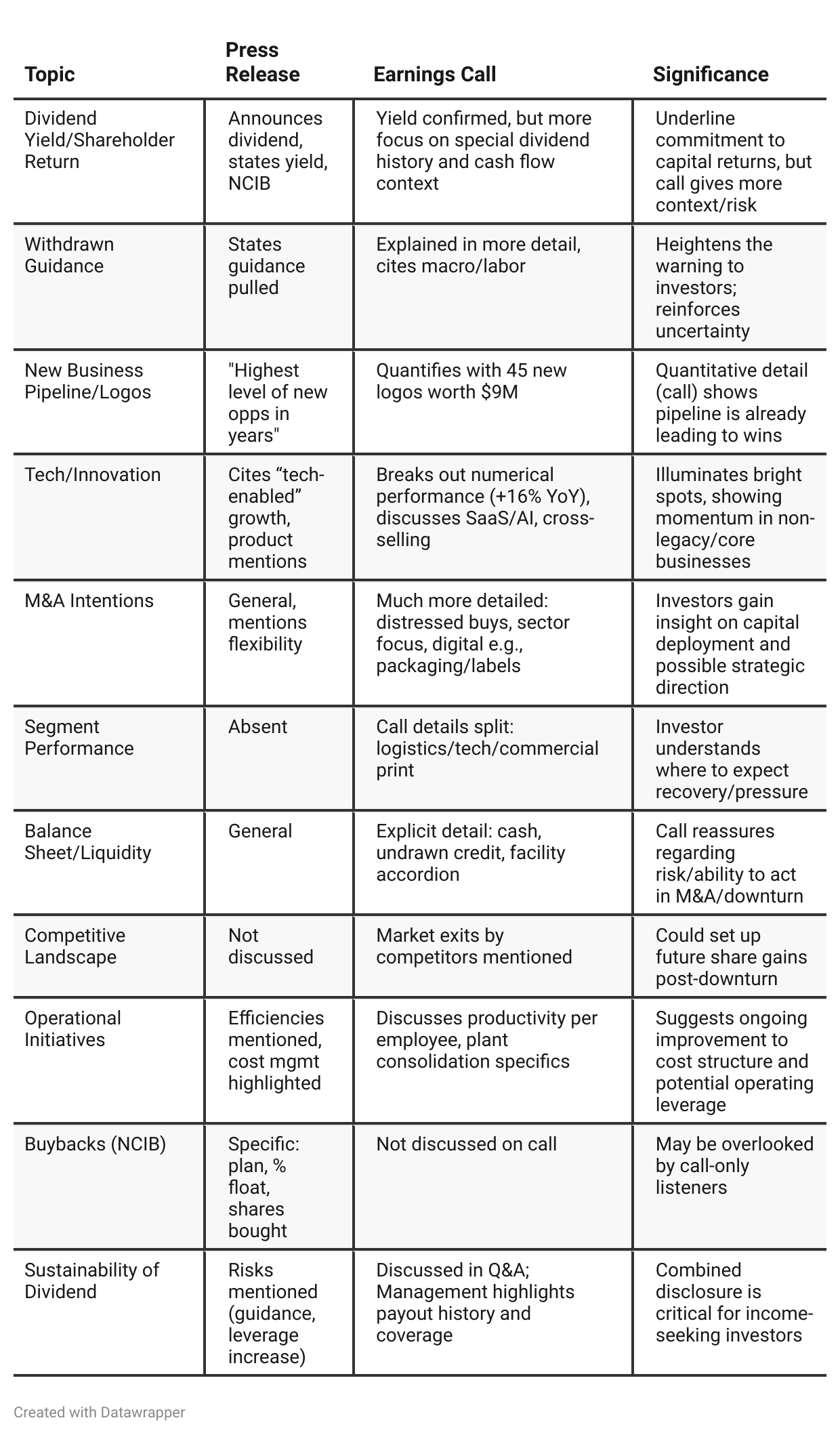

Press Release vs Call Transcript Comparison

Earnings Call gives much more operational/sub-segment color than the press release, crucial for modeling and scenario planning.

Call Delivers Confidence Tone: CEOs emphasize “no material client losses,” “all in on growth,” and upcoming “operating leverage” — tone more optimistic and forward-looking versus more cautious release.

Cost and Productivity improvements (detailed in call) may set DCM up for a better rebound when end-markets stabilize.

Tech and digital progress specifics are call-only — important for investors seeking a secular growth angle.

Risks around tariffs, labor, and client order irregularity run through both, but call Q&A provides much clearer, more actionable context (e.g., procurement responses, impact segmentation).

Leverage and dividend policy — both frame high payout as doable because of free cash flow, but admit future risks if headwinds extend, which is a nuanced but critical point for yield-focused investors.

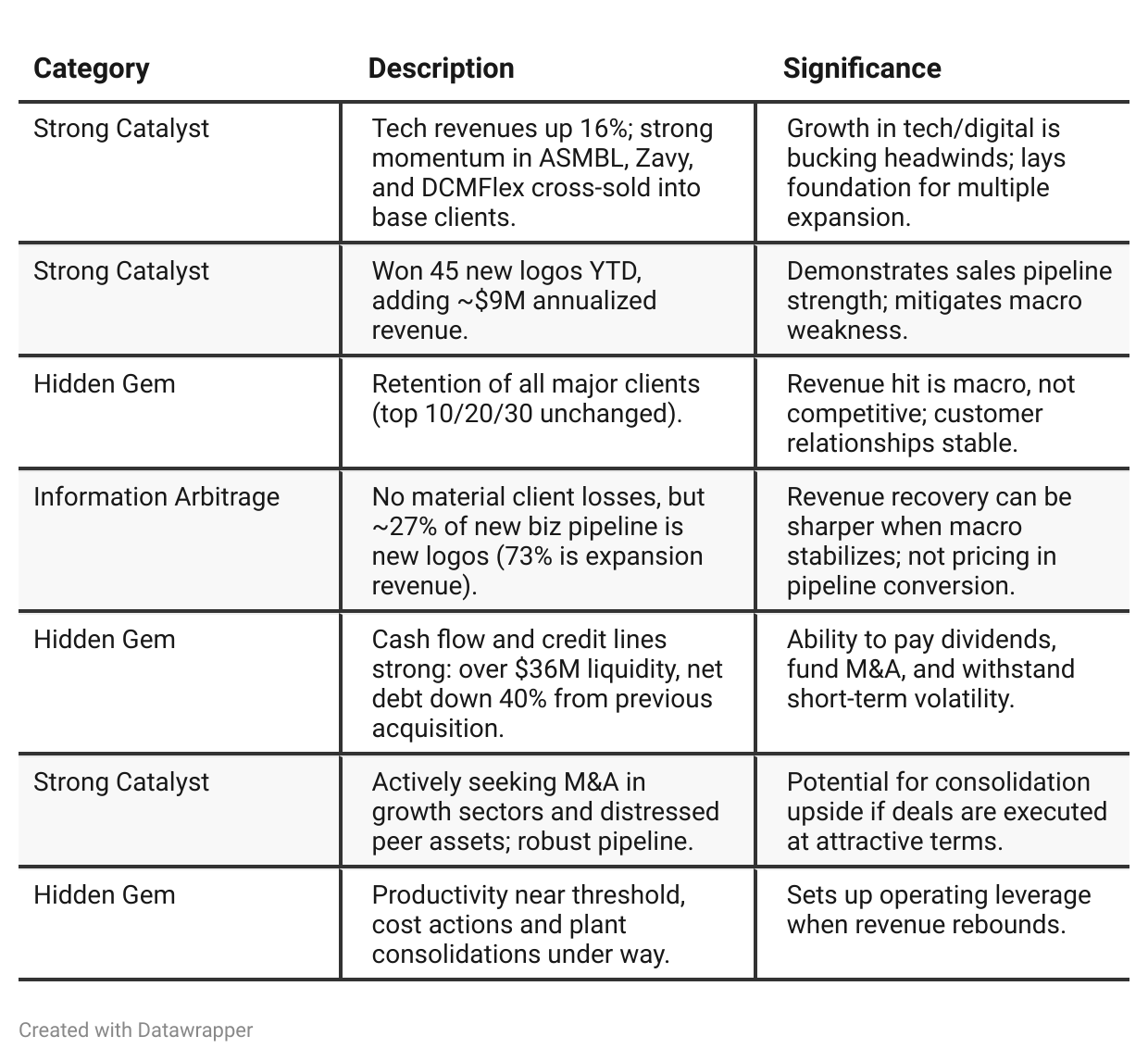

Positive Insights

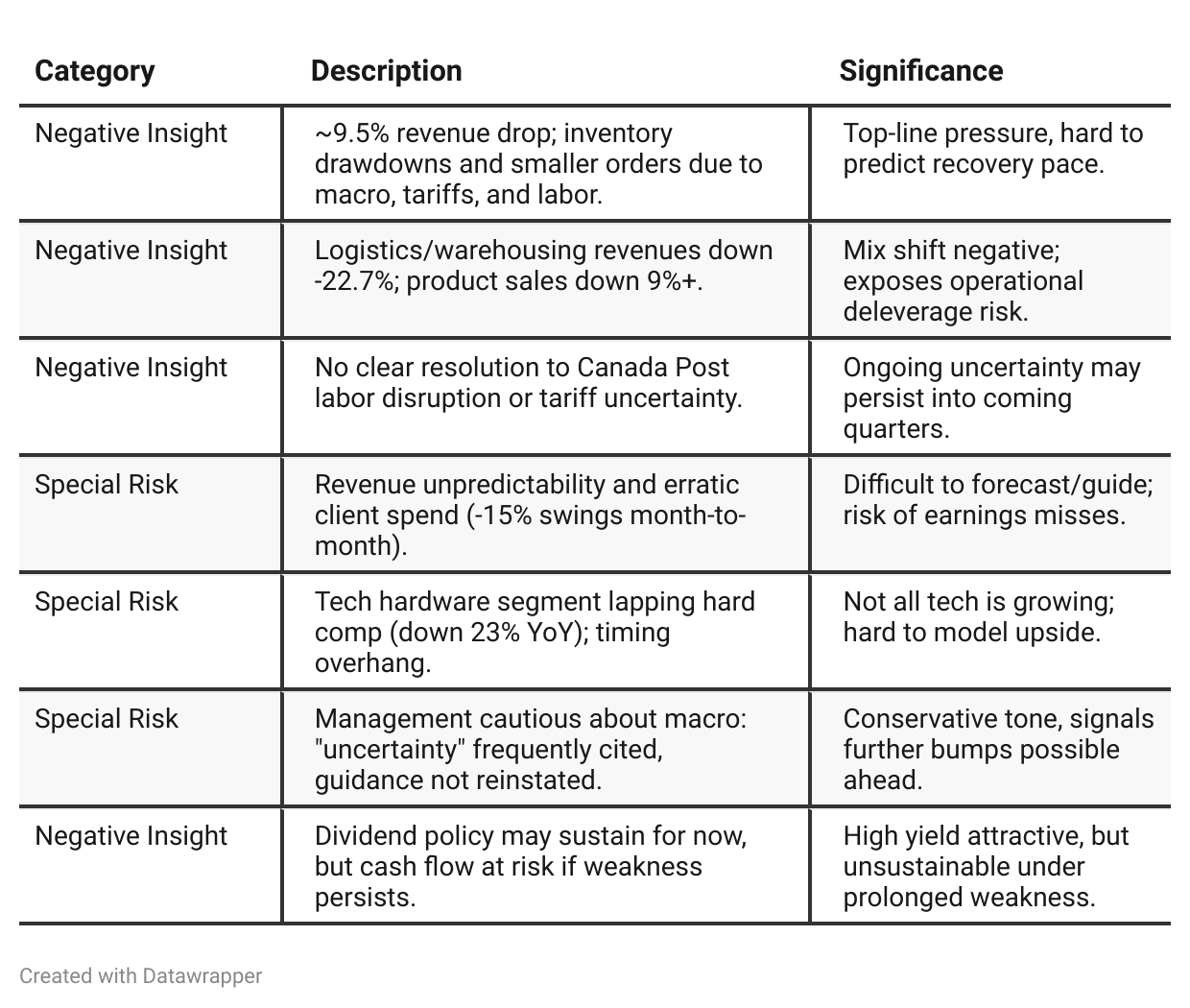

Negative Insights

Tariff Risk

Discussion of U.S. tariffs: Management stated tariffs and tariff-related uncertainty have negatively affected business confidence, resulting in delayed orders and smaller order sizes. The "bad" side is ongoing unpredictability; the "good" is that it forced DCM to diversify paper sourcing globally.

Risk Mitigation Actions: DCM has already diversified its supply chain away from the U.S., finding competitive alternative sources internationally, reducing dependence on U.S. paper for the commercial print business. This mitigates some cost and supply chain risks and may provide pricing advantages versus less-prepared peers.

Market Share Impact: Management indicates some struggling peers have exited, possibly enabling DCM to pick up market share, especially if tariffs persist or escalate.

Forward-Looking Statements: Paper remains under CUSMA for now ("still covered for now"), but management emphasizes continued monitoring and flexibility. No quantitative guidance given on future impact, but management is proactive.

Conclusion: Tariff uncertainty remains a significant risk, but DCM’s proactive sourcing is a relative advantage. Investors should watch for further escalation, any cost shocks, or competitive disruptions in the supply chain.

Sentiment Analysis

The overall sentiment is neutral. While there is acknowledgement of stable earnings and a notable dividend yield, concern is also expressed about the company’s pace of debt reduction. No strong positive or negative emotion dominates, leading to a balanced view among investors.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q1 2025: DCMDF emerges from a period of integration and restructuring, with management expressing optimism about stable margins, strong cash flow, and a mounting business pipeline. There’s a confident focus on turning the page toward organic growth with “all in on growth” messaging, capitalizing on tech expansion and defending profitability. Macro threats are noted, but seen as manageable obstacles—not barriers.Q2 2025: The narrative becomes more cautious and operationally defensive. Revenue shortfalls are attributed to broad-based macro headwinds, and management’s tone reflects pragmatic patience—recognizing that the business environment is more difficult than anticipated. The focus shifts from immediate growth to resilience: retaining all key clients, controlling costs, maintaining liquidity, and preparing for medium-term opportunity (including possible market share gains through M&A or competitor exits). Strategic themes remain, but timelines are now more conditional on external recovery.

Year-over-year comparison

—

Final Takeaway

DATA Communications Management Corp. is in a stabilization phase—weathering market volatility with strict cost control, strong liquidity, and a growing tech-enabled pipeline. While technology momentum and customer retention are positives, persistent macro headwinds, revenue unpredictability, and external risks (tariffs, labor) limit near-term upside. Execution on pipeline conversion, M&A, and cost leverage will be critical. Verdict: Hold, with a bias to upgrade on clearer signs of stabilization or growth.