Data I/O Corporation (NASDAQ: DAIO) – Q3 2025 Earnings

Data I/O Corporation (NASDAQ: DAIO) – Q3 2025 Earnings

Earnings Release Date: Oct. 30, 2025

Stock Price: $3.11

Market Cap: $28.9 million

Q3 2025 sales of $5.4 million vs $5.4 million in the prior year

Q3 2025 EPS of ($0.15) vs ($0.03) in the prior year

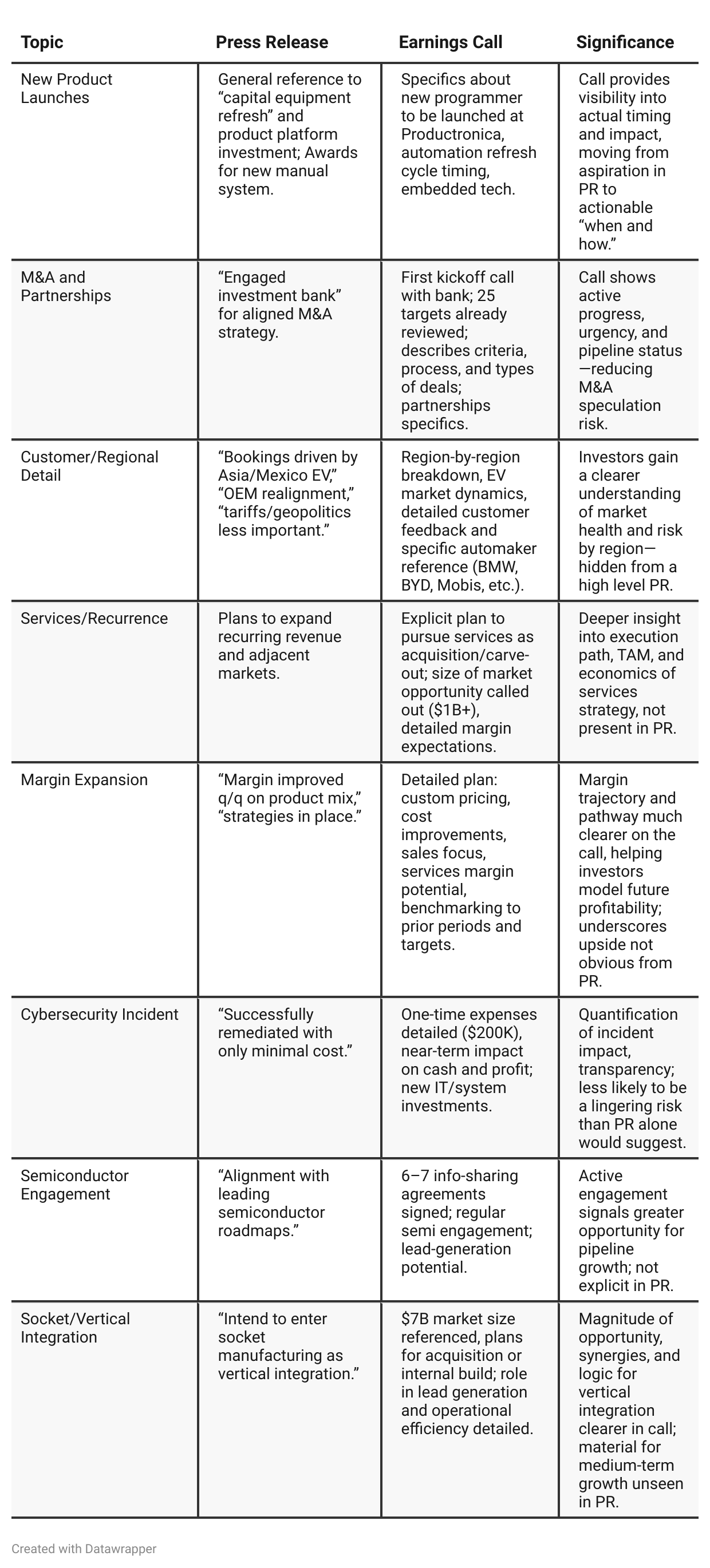

Press Release vs Call Transcript Comparison

The earnings call paints a much sharper picture of near-term regional headwinds in Europe and sector concentration risk (auto exposure >75% of bookings).

Press release frames “cyber remediated, growth progressing,” but the call details meaningful ongoing cost controls, margin improvement plans, and the mix of CapEx vs. recurring/services lines.

DAIO’s management is candid about the lumpy/slow CapEx cycle and is prioritizing actions to offset it—a positive for institutional investors used to smoothing/visibility.

The call provides rare specificity about pipeline timing (Productronica launch, services!) and a bias toward executing M&A/services before embedded/sockets as revenue levers.

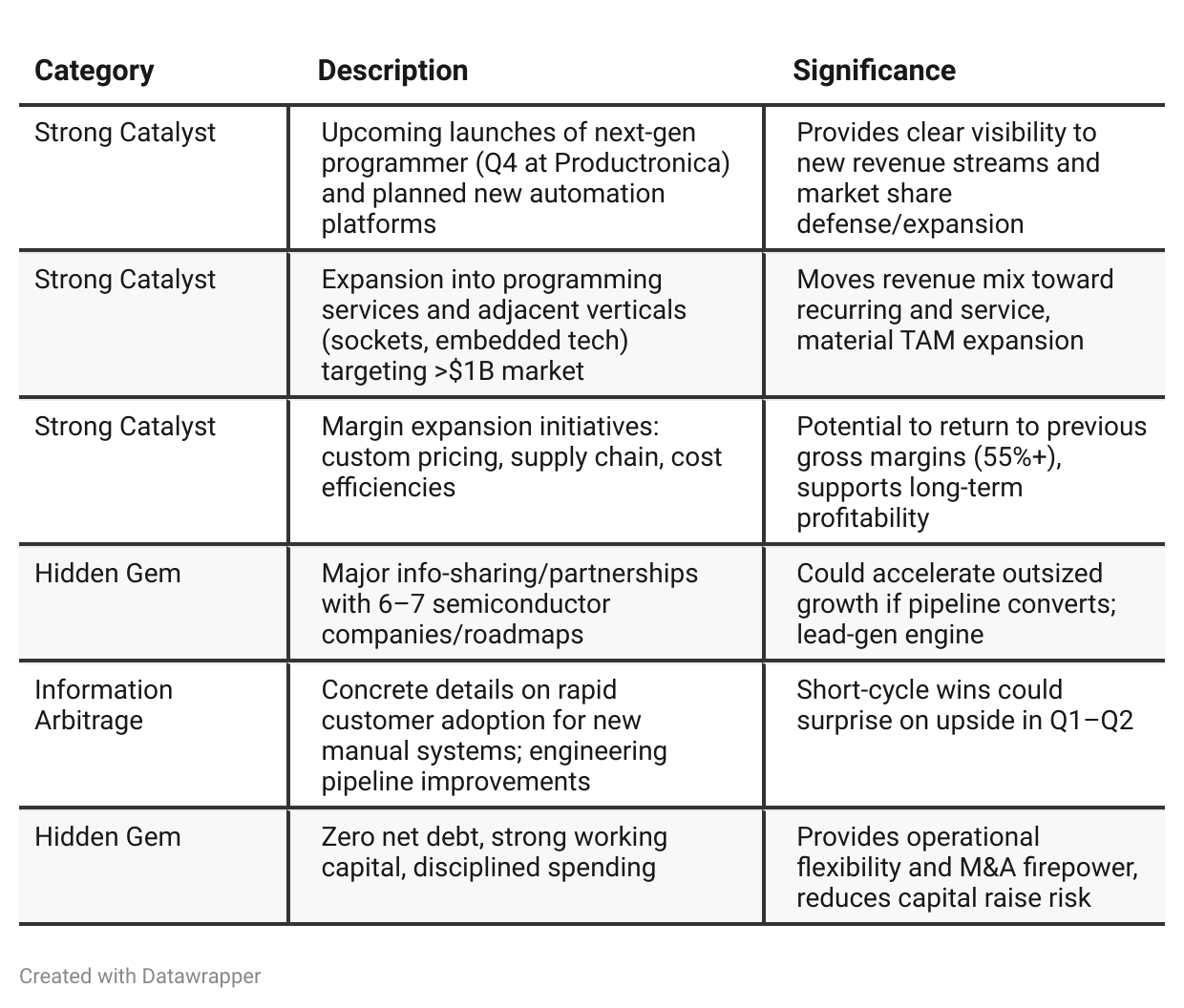

Positive Insights

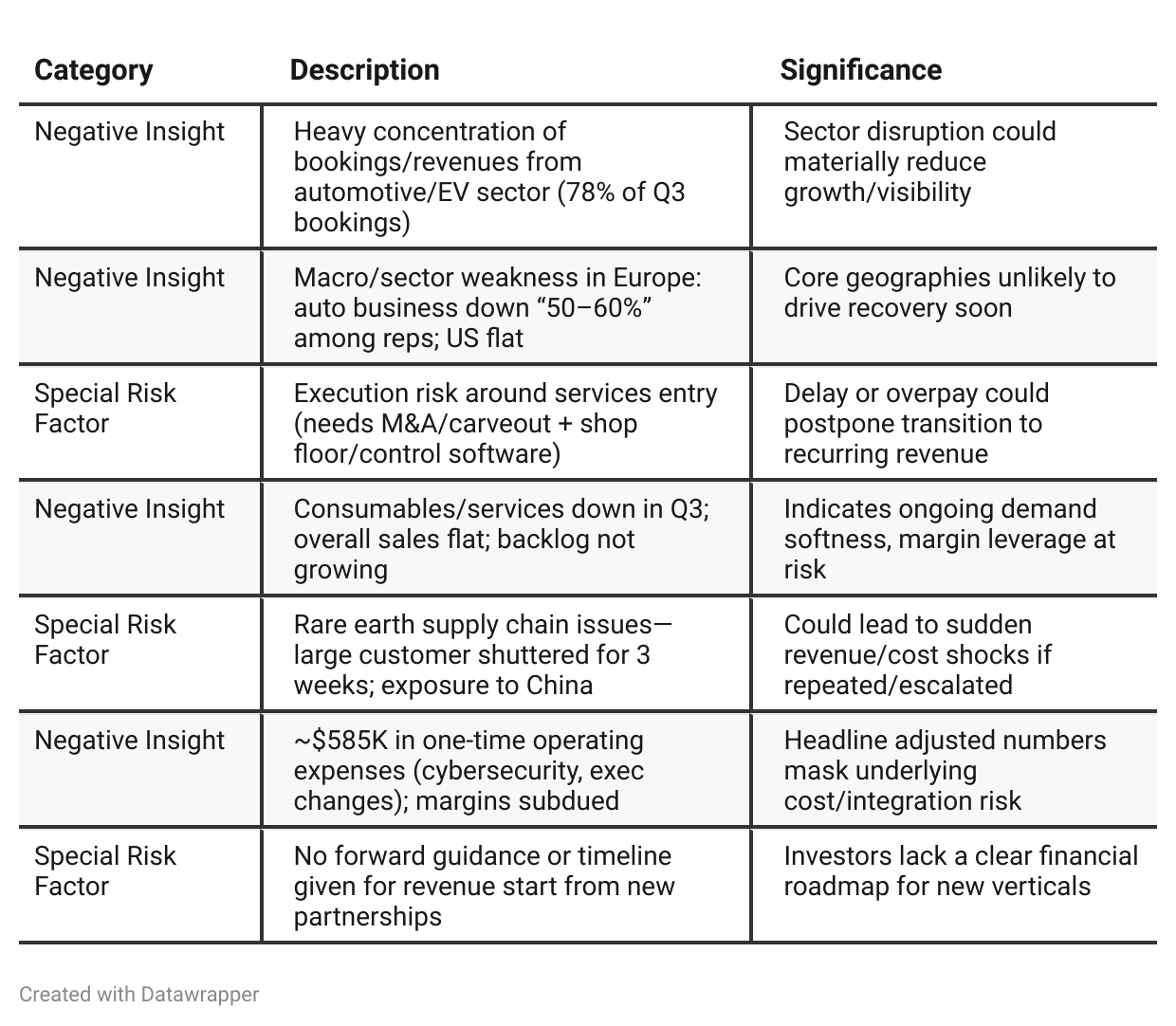

Negative Insights

Tariff Risk

Tariff/Trade Policy Analysis: Tariffs and global trade friction remain an ongoing but now “tertiary” risk for Data I/O, according to management. Key takeaways include:

Direct impacts: Products/services impacted by global trade/tariffs (previous gating factor, still causing caution especially in Europe).

Mitigation actions: Supply chain planning, local (Asia/Mexico) bookings, direct engagement with global OEMs, margin defense through proactive pricing.

Indirect exposure: Rare earth supply chain disruption—a large automotive customer shuttered production for three weeks. Management views such issues as potentially sudden and impactful, dependent on international negotiation outcomes (e.g., China/Europe rare earth control).

Forward-looking: Management hopes for progress/relief in global trade but warns that the landscape remains volatile. No quantification of impact or projected P&L effects—but supply chain adjustments and customer localization are ongoing.

Conclusion on Tariffs: Data I/O has reduced vulnerability to trade/tariff shocks versus prior periods but remains exposed via supply chain and customer base in automotive/EV. Future trade or supply shocks could quickly impact bookings, revenue timing, and cost structure, making ongoing monitoring essential.

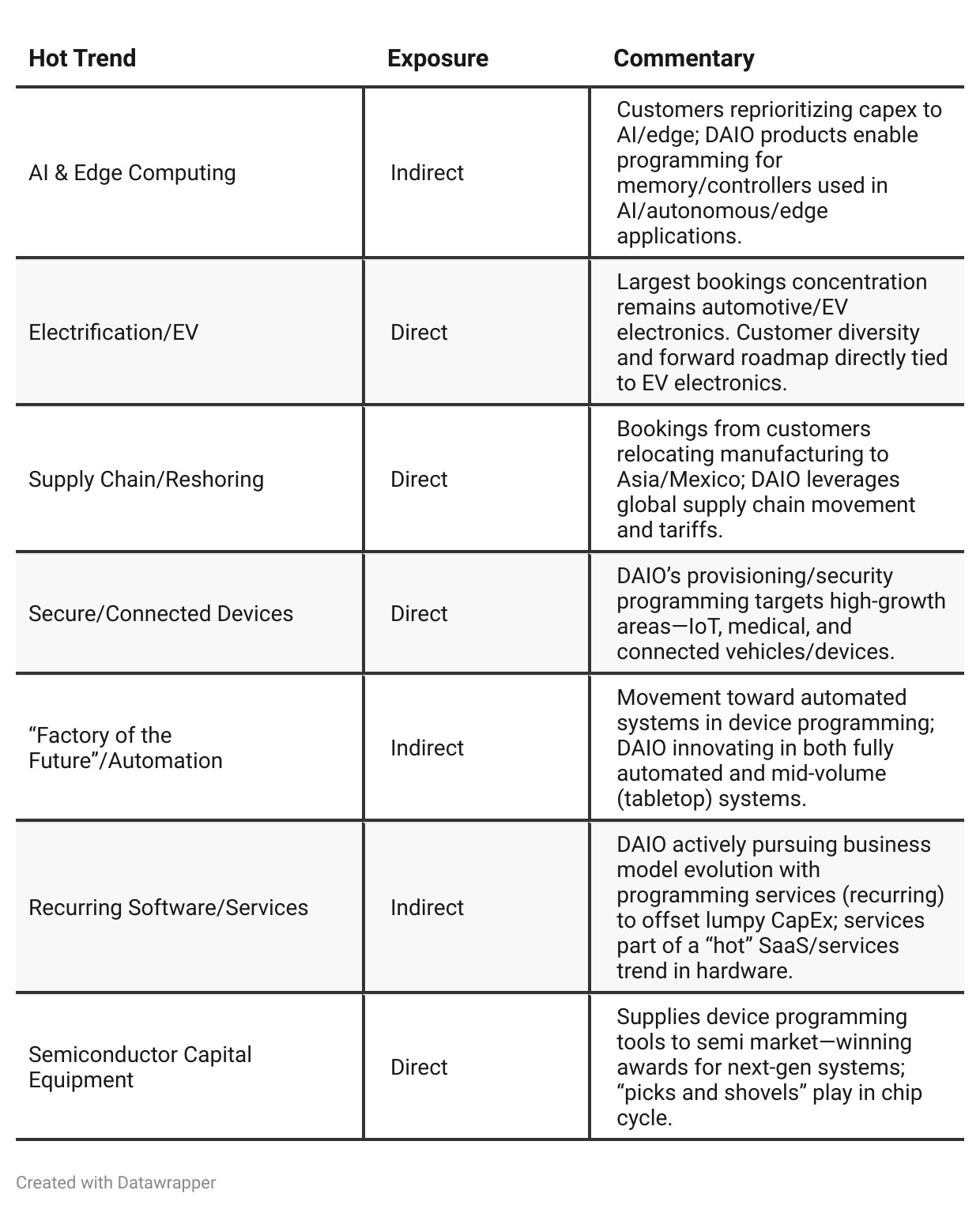

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025 Narrative: Data I/O was in recovery mode: battling mix, margin, and supply chain challenges, rolling out leadership and operational changes, and aggressively trying to fix technical and process gaps that hurt performance. The tone was earnest—focused on survival, operational hygiene, and restoring customer confidence, particularly around UFS yields. Optimism was rooted in upcoming product launches and the sense that “better days are coming,” but with evident caution about ongoing macro and industry headwinds.Q3 2025 Narrative: A year into the CEO’s tenure, Data I/O is shifting from remediation to transformation. The company has reignited its product pipeline, with awards and customer validation fueling confidence. Management is taking bold steps toward sector expansion—with ambitions in programming services, embedded solutions, and vertical integration. Strategic partnerships, M&A, and new revenue models (recurring and service-based) are no longer future aspirations, but imminent activities. Margin expansion and market diversification remain top priorities, but the messaging is now about building the next foundation, leveraging existing strengths, and positioning the company for breakout growth as macro clouds clear and technology transitions (AI, high-density flash) reset the competitive landscape.

Year-over-year comparison

Q3 2024:

Data I/O is under new leadership, focused on stabilizing its core business as auto market softness and macro headwinds impact sales. The new CEO is evaluating operational strengths and weaknesses and laying the foundation for future diversification, with immediate successes in cost controls and balance sheet management offsetting near-term revenue challenges. The tone is prudent and methodical; the goal is to prepare for a more transformative phase.

Q3 2025:

A year later, Data I/O has moved decisively into growth mode. The company has refreshed its product portfolio, won industry recognition, and is launching initiatives aimed at capturing far larger, more recurring, and more diversified revenue streams through services, partnerships, and targeted acquisitions. While sector headwinds continue, the team expresses strong confidence, pointing to milestone achievements, robust customer engagement, and a clear strategic roadmap for sustainable growth and market leadership.

Final Takeaway

Data I/O (DAIO) is in a restructuring and transition phase, seeking to diversify its revenue base with new products, recurring services, and vertical integration. While the company’s strong cash position and margin initiatives are positives, near-term growth remains highly exposed to volatility in the automotive/EV and European markets. New business lines present substantial opportunity but also execution risk, and tangible financial impact remains to be seen. Verdict: Hold. Execution on services entry, new product adoption, and geographic diversification will determine the upside.