Data I/O Corporation (NASDAQ: DAIO) – Q2 2025 Earnings

Data I/O Corporation (NASDAQ: DAIO) – Q2 2025 Earnings

Earnings Release Date: Jul. 24, 2025

Stock Price: $3.24

Market Cap: $30.1 million

Q2 2025 sales of $5.95 million vs $5.06 million in the prior year

Q2 2025 EPS of -$0.08 vs -$0.09 in the prior year

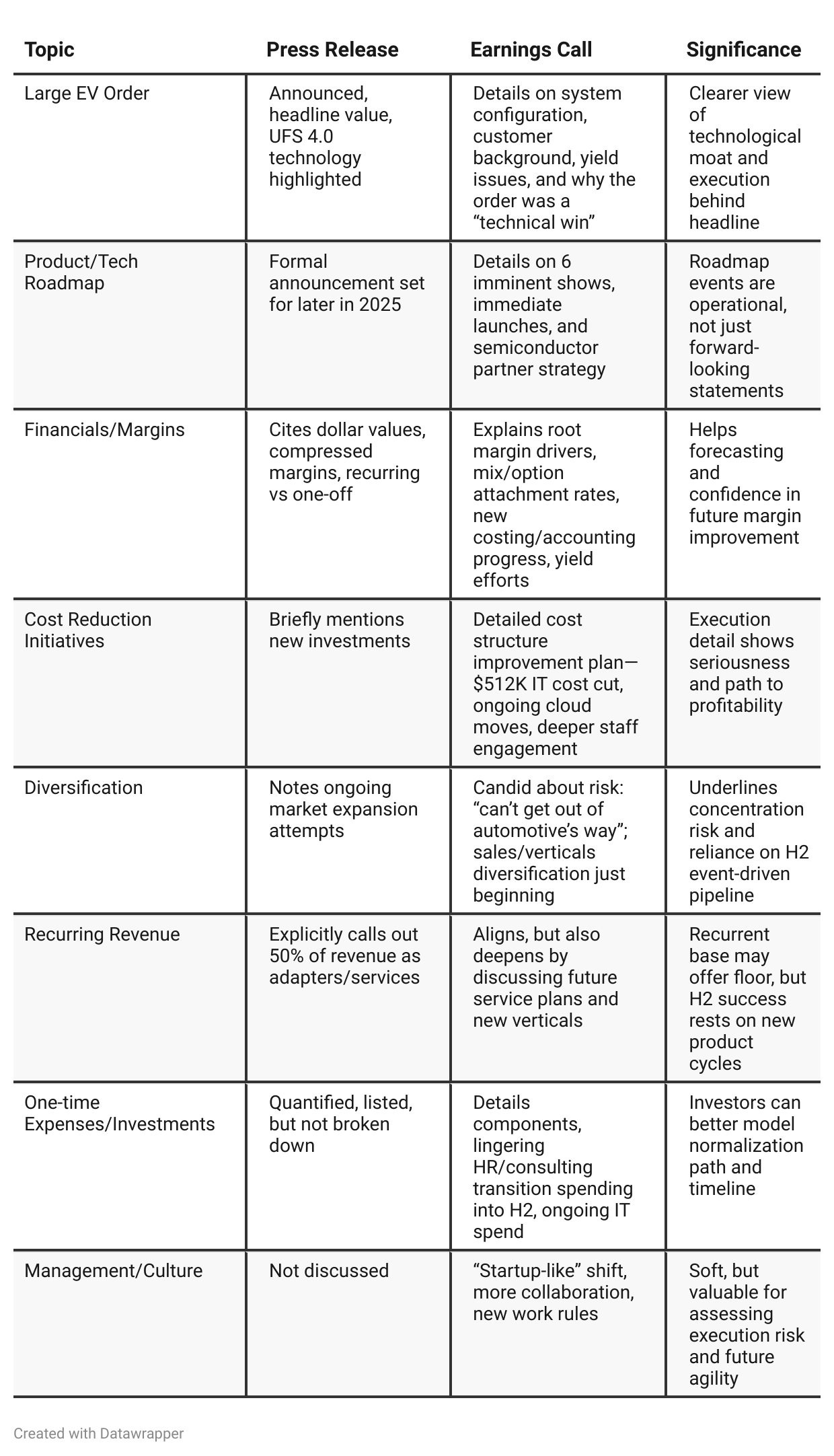

Press Release vs Call Transcript Comparison

Execution Risk/Growth Signal: Management’s candidness about the “hard” first half, resource focus, and product iteration timeline is a positive for tracking execution—but means H2/H1 can surprise in both directions.

Balance Sheet Health: Zero debt and stable net working capital provide a runway to absorb planned investments and unexpected transition costs.

Visibility on H2: Numerous product launches/events and “pent-up” customer orders hint at possible improvement, but also mean H2 will be make-or-break for sentiment.

New cost accounting/cost structure transparency: If successful, these initiatives may unlock future margin expansion and valuation re-rating potential if growth returns.

Service DNA: Emphasis on field service, new Salesforce Service Cloud adoption, and direct customer touchpoints suggest that higher-margin, sticky aftermarket/service revenue could rise over time.

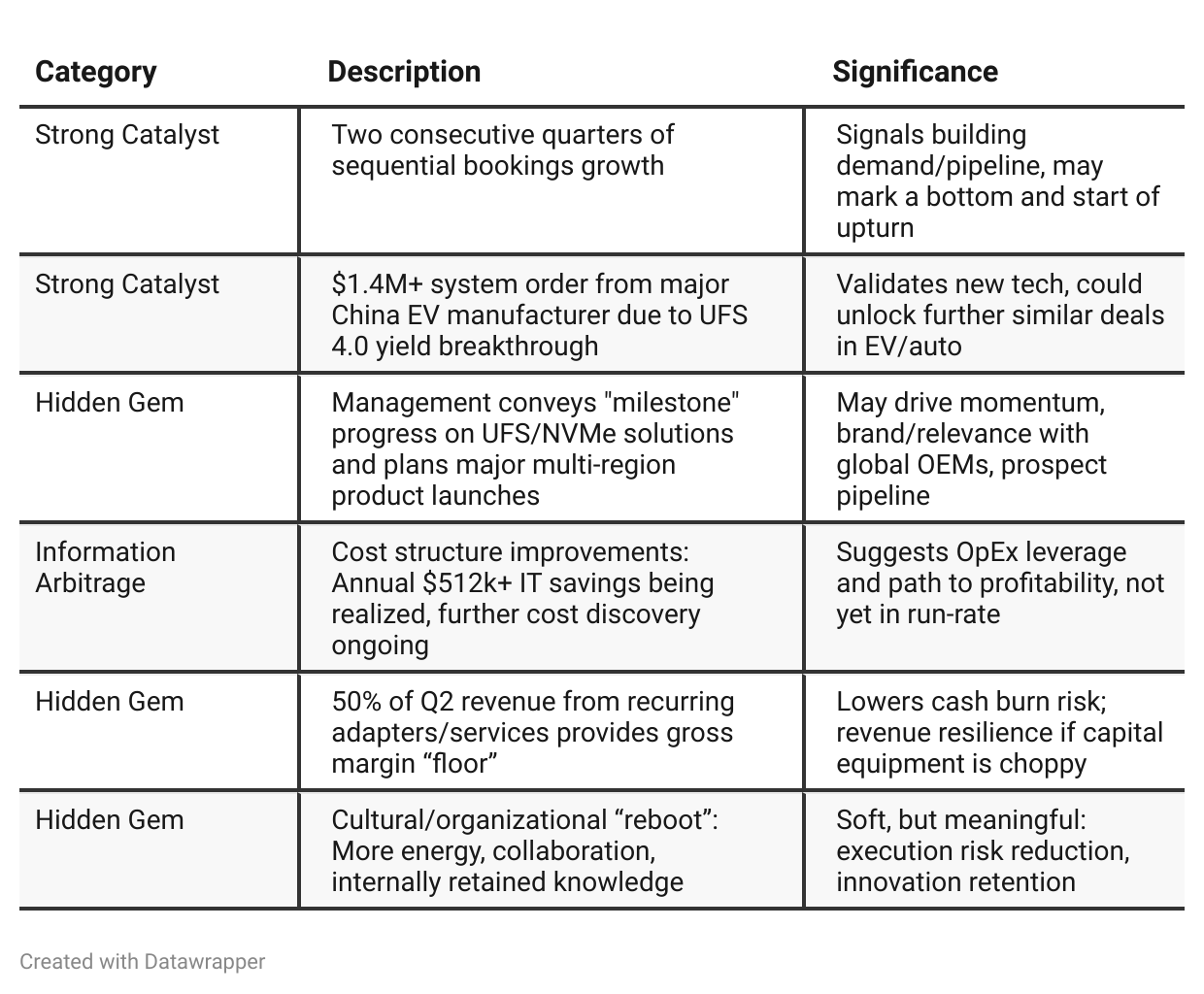

Positive Insights

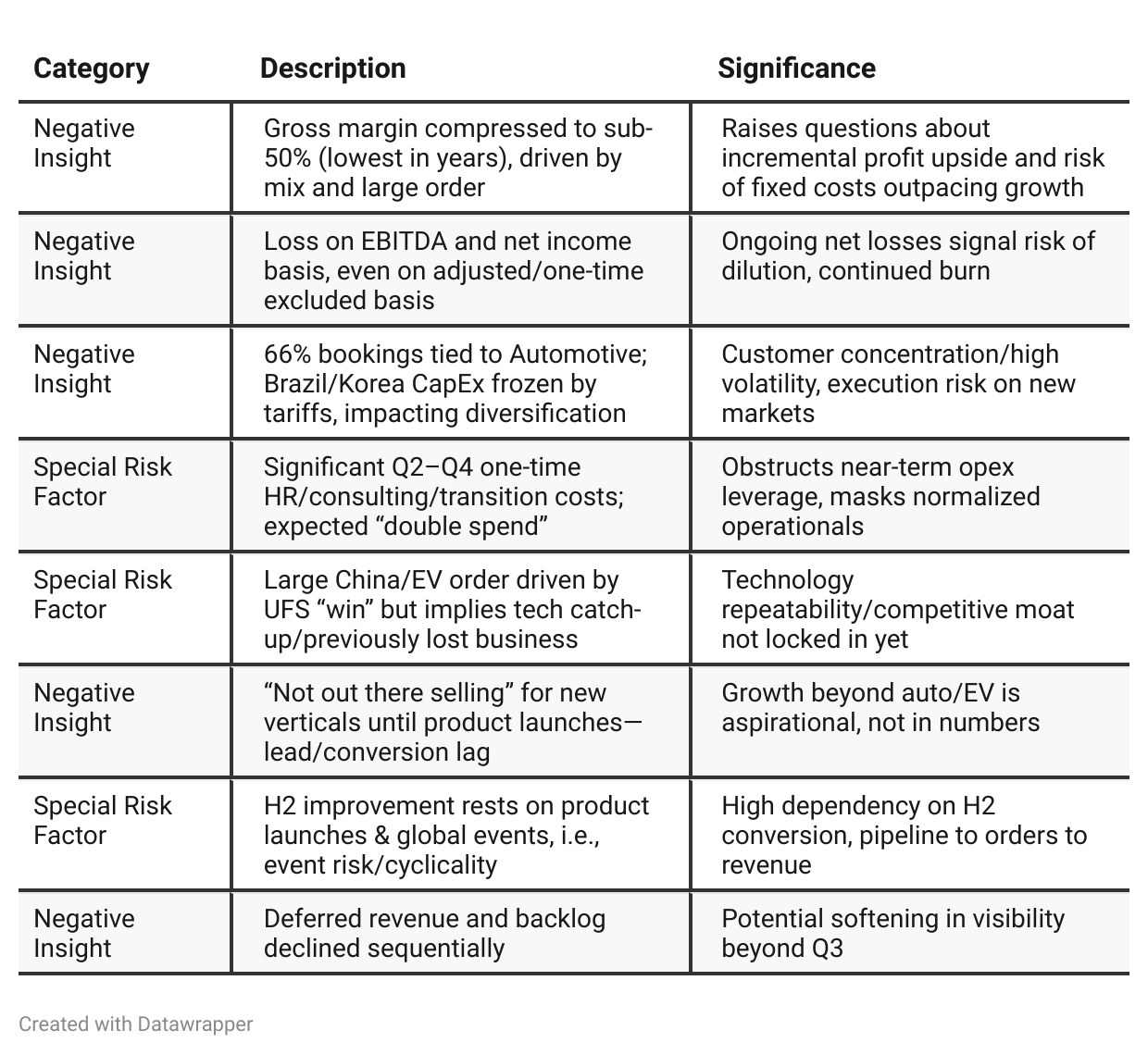

Negative Insights

Tariff Risk

In H1 2025, CapEx in Korea and other global accounts was frozen or reduced due to tariff/trade issues—this directly impacted top-line bookings and revenue, highlighting the revenue risk of unpredictable international policy.

Tariff/part sourcing pressures pushed management to diversify both manufacturing and supply origin; some share shifted to China for execution, but also to mitigate US/China/EU friction.

CEO and CFO both stress that ongoing and anticipated tariff escalation led to early/ongoing supply chain planning, product sourcing shifts, and direct actions to avoid new input costs (e.g., aluminum sourcing).

Certain smaller cost pressures from tariffs have only started to appear (e.g., input costs on aluminum in some machine parts), but are limited in effect; actively being rerouted.

Recurring comment: Europe and the Americas were under CapEx restraint owing to persistent unresolved international trade negotiations.

On competitive advantage: CEO expresses that fixing yield issues on UFS 3.1/4.0 is a technical edge not easily matched, but is candid that pent-up demand in several regions depends on tariff visibility and global agreement.

Sentiment Analysis

The overall sentiment is neutral. While some comments reflect concern about a potential weak quarter and recall management’s description of “scary” months for bookings, the actual results were better than the lowest expectations—sequential revenue held up, and the quarter was not considered a disaster. The sentiment is balanced, with neither strong bullish optimism nor clear bearish negativity dominating the conversation.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: Data I/O was at the start of a possible turnaround, celebrating a rebound quarter while acknowledging the uncertainty ahead. Management was cautiously optimistic: leading indicators (trade show metrics, recurring revenue, strategic dialogues with semis) suggested green shoots, but tariffs, CapEx push-outs (especially in Asia), and auto concentration all loomed large. Strategic investments in product and platform were under development, with visibility that new wins could unfold in H2, and ongoing cost discipline calibrated to enable these bets.Q2 2025: With another quarter completed, the company progressed from theoretical to at least partial execution: bookings continued to improve, a key technical milestone was achieved (delivering a large EV order), and management made transparent operational changes (cloud IT, cost savings, consultant/HR transitions). However, a split narrative emerges: there is clear momentum (“collaboration,” culture, new orders), but also blunt honesty about the persistent reliance on automotive, the challenging product mix leading to sharp margin compression, and risk that hoped-for new verticals/events/product launches must now deliver in the second half. The team is energized and better organized, but Q2 remains “a hard quarter” by the CEO’s own admission, with only June providing relief after a tough spring. H2 is now the pivot point for the investment story.

Year-over-year comparison

Q2 2024: Data I/O is in “wait-and-see” mode, hurt by an abrupt auto sector pause in the Americas. Management is defensive—leaning on cash, expense control, and recurring revenue to weather volatility, and positioning tactically for a cyclical bounce and ongoing diversification.

Q2 2025: The company has pivoted from defense to proactive change and execution. Booking momentum and a technical platform breakthrough (UFS yield fix) give credibility to growth ambitions, and organizational energy is notably higher. Still, real risks remain: auto exposure persists, margin improvement is a work in progress, hefty transformation costs mask profit progress, and the hoped-for H2 event-driven conversion is crucial. The story is now “smart bets and transparent execution” rather than just survival and optimism. Success in H2 is not guaranteed, but management has raised the bar on both transparency and accountability.

Final Takeaway

Data I/O is in a product transformation and operational improvement phase, pushing core platform innovation (UFS/NVMe) and restructuring its cost base. While sequential bookings growth and technical wins are positive, execution risk remains high given customer concentration, compressed margins, and reliance on a strong event-driven H2 inflection. Investors should focus on non-automotive order conversion, margin recovery as new programs ramp, and evidence that cost savings are sustainable and translate to profits. Verdict: HOLD—upside if new platforms convert to incremental, higher-margin sales; downside if cash burn persists or launches fizzle.