CuriosityStream Inc. (NASDAQ: CURI) – Q3 2025 Earnings

CuriosityStream Inc. (NASDAQ: CURI) – Q3 2025 Earnings

Press release and earnings call link

Earnings Release Date: Nov. 12, 2025

Stock Price: $3.75

Market Cap: $215.0 million

Q3 2025 sales of $16.0 million vs $17.8 million in the prior year

Q3 2025 EPS of ($0.02) vs ($0.08) in the prior year

Overview:

CuriosityStream (NASDAQ: CURI) is a global factual media company offering documentary and non-fiction programming across streaming (SVOD), ad-supported (FAST/AVOD), and licensing channels. It differentiates itself by curating and producing science, history, and technology content—often marketed as “the Netflix for knowledge.”

Revenue Drivers:

Subscriptions (retail + wholesale): Direct-to-consumer and partner-distributed streaming.

Licensing: Selling access to its video/audio library for AI model training and traditional media use.

Advertising: Monetization through FAST channels and sponsorships.

Customer Base / End Markets:

Consumers worldwide (B2C subscribers).

AI model developers and hyperscalers (B2B data licensing).

Global broadcasters, streamers, and pay-TV partners.

Market Positioning:

Emerging niche leader in factual entertainment and AI data licensing. The company is repositioning from a traditional streaming model to a data-rich content licensor at the intersection of media and artificial intelligence.

Financial Trajectory:

Turnaround phase — revenue grew 46% YoY to $18.4 M with three consecutive quarters of positive EBITDA and record free cash flow. Net losses persist due to high stock-based compensation (SBC), but underlying cash profitability improved sharply.

Strategic Focus:

Expanding AI licensing as the fastest-growing revenue engine.

Maintaining cost discipline and positive cash flow.

Preparing for 2026 subscription relaunch with premium tiers and new packaging.

Continuing dividend payments funded by operating cash flow.

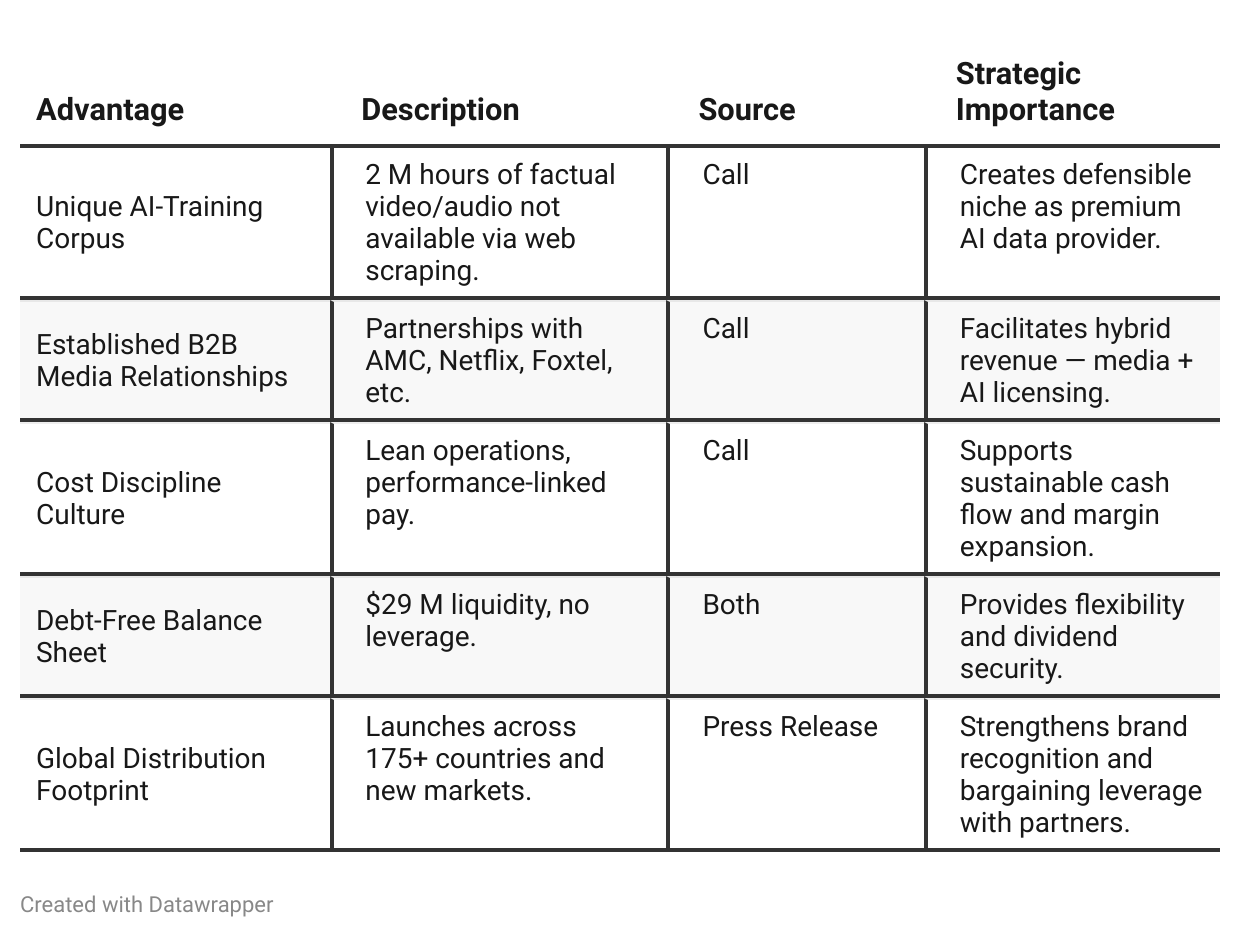

Competitive Advantage Insights

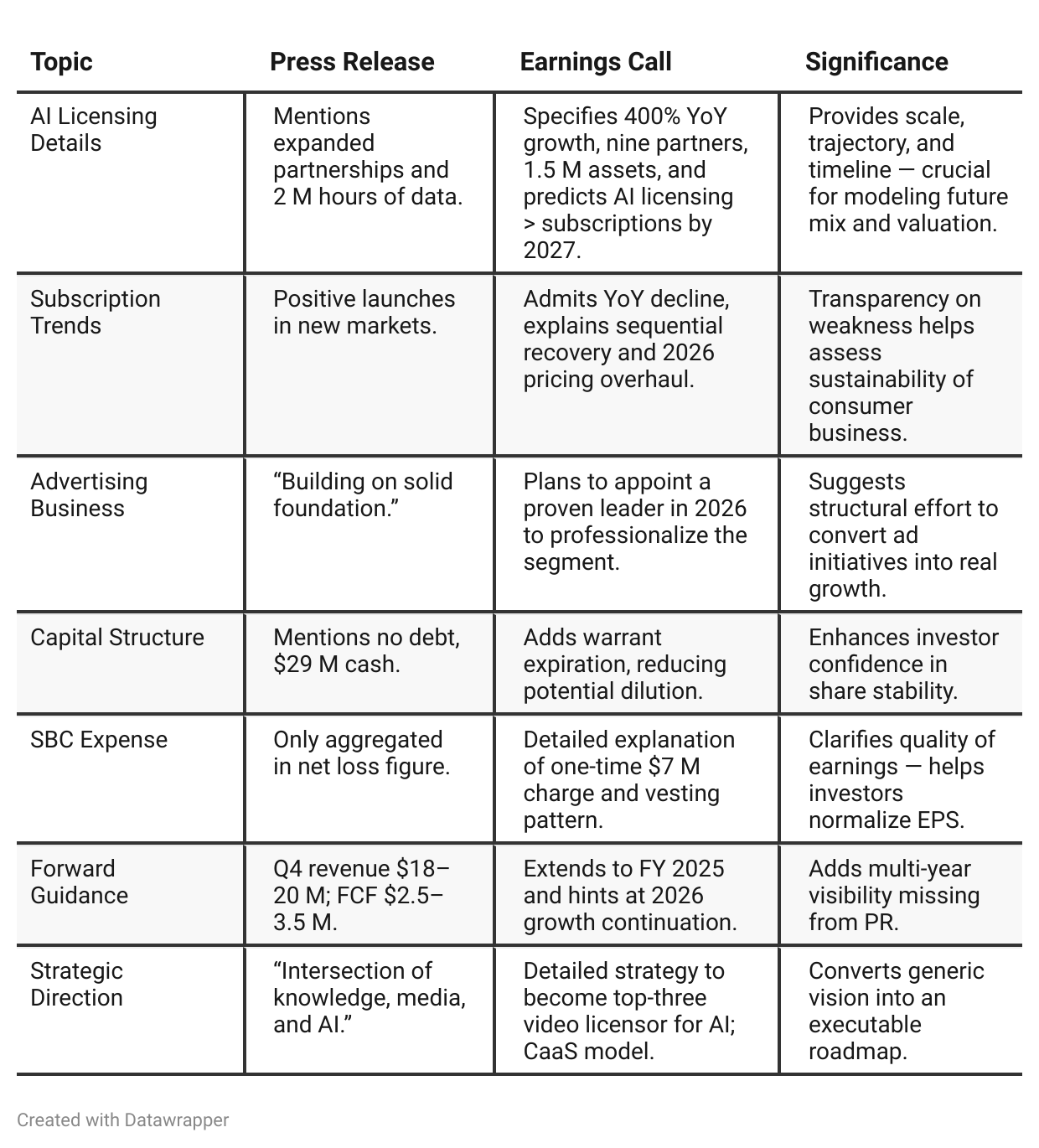

Press Release vs Call Transcript Comparison

Narrative Shift: The press release still markets CuriosityStream as a content company; the call repositions it as an AI data-licensing infrastructure play.

Operational Discipline: Management repeatedly emphasized cost rationalization and performance-linked pay — important given small-cap investor skepticism about media firms.

Cash Culture: Management highlighted that dividends are and will be covered by operating cash flow — a strong message to income investors.

Investor Communication: The call explicitly sought to pre-empt concerns about “lumpiness” and capital efficiency, showing improved IR sophistication.

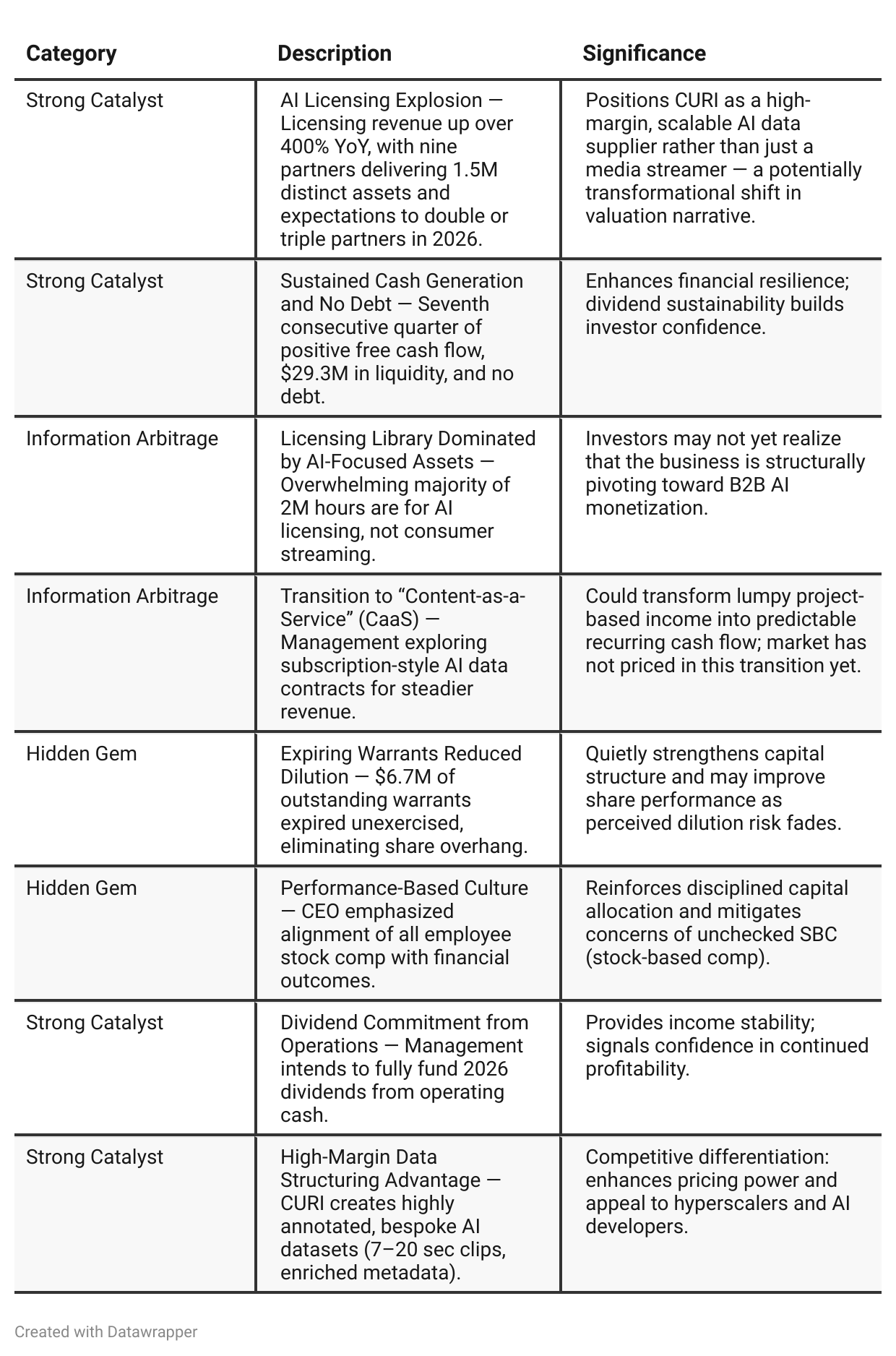

Positive Insights

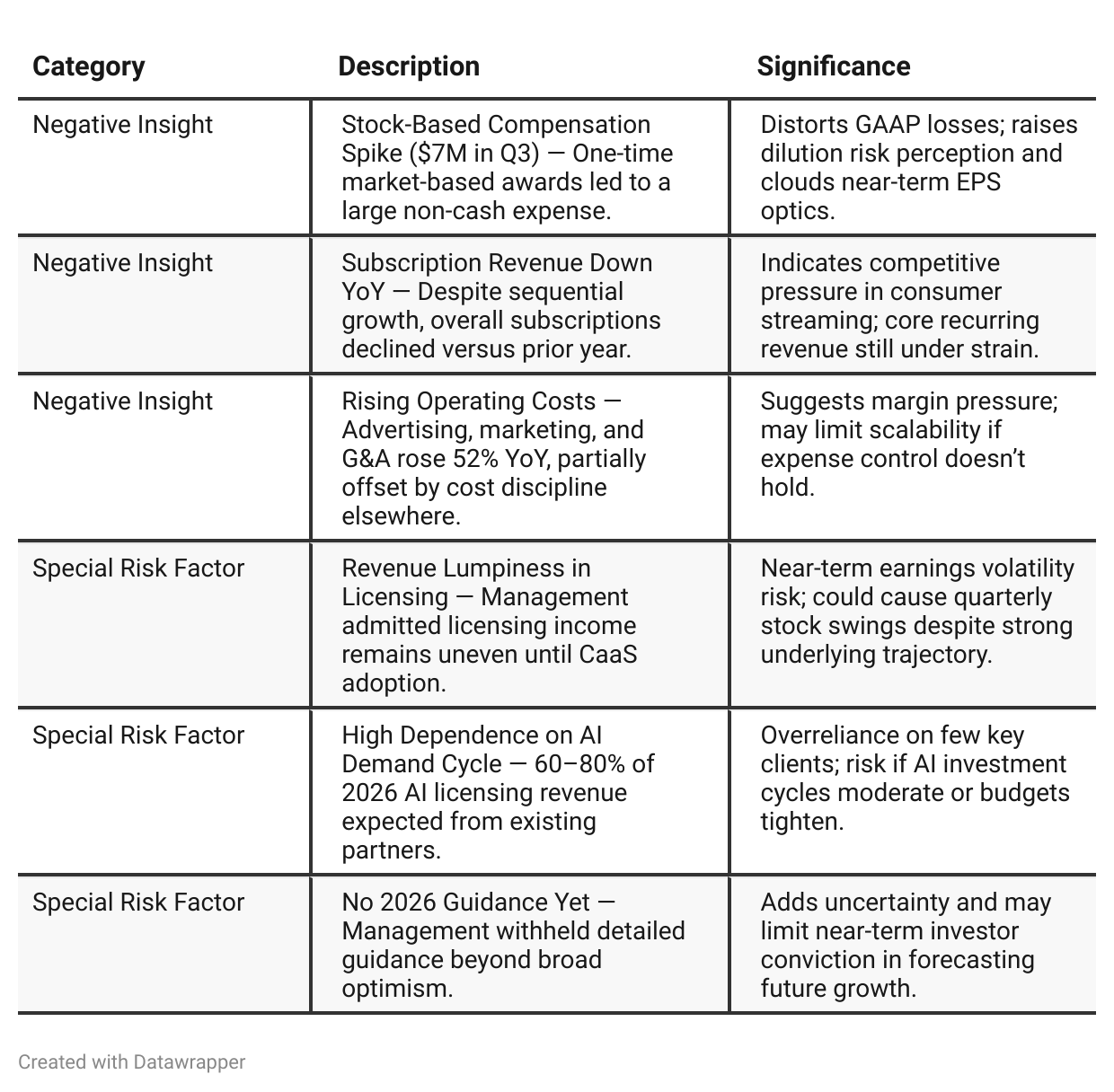

Negative Insights

Investor Underappreciation Signals

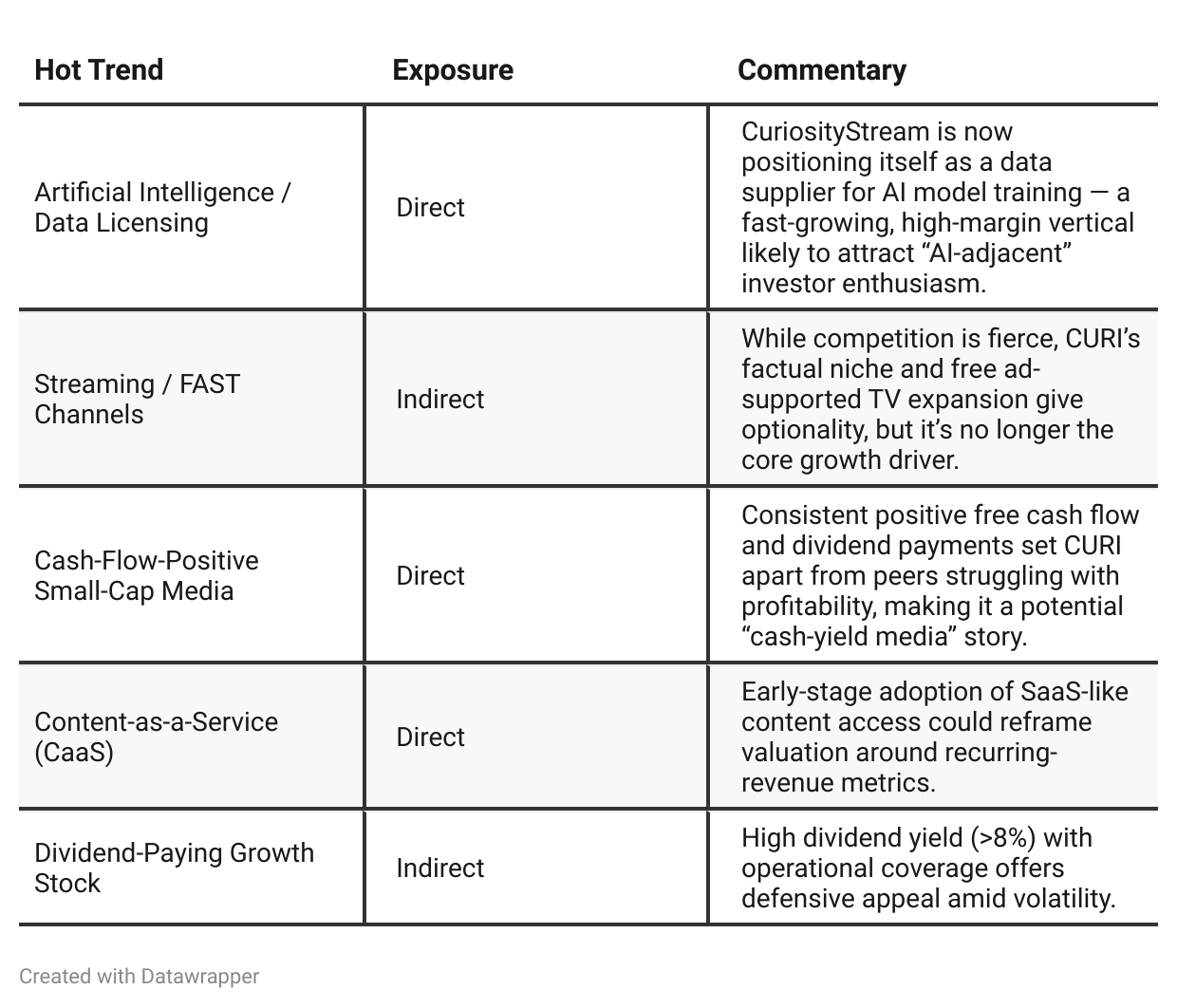

✅ AI Licensing Flywheel — Licensing revenue grew >400% YoY with nine hyperscaler partners, and management expects it to exceed subscriptions by 2027. Investors may underappreciate that this transforms CURI into a high-margin B2B data licensor rather than a streaming service, potentially deserving tech-style multiples.

✅ Content-as-a-Service Model — Management’s move to SaaS-like multi-term AI data access contracts could smooth earnings and increase predictability. Investors might overlook its recurrence potential until disclosed contract structures appear in filings.

✅ Warrant Expiration Cleanup — $6.7 M in warrants expired unexercised, removing dilution risk. The market may miss this de-risking event, which can support a rerating once liquidity overhang concerns fade.

✅ Operational Dividend Coverage — Dividends to be funded entirely from cash flow in 2026. With many small-cap media firms cutting dividends, this operational coverage is a sign of true cash generation the market may not fully price in.

✅ SBC-Distorted GAAP Loss — Adjusted EBITDA positive for three straight quarters; underlying profitability masked by temporary SBC. Once normalized, margins could surprise to the upside.

Tariff Risk

There were no mentions of U.S. tariffs or trade policy impacts in the earnings call. CuriosityStream operates in the digital media and data-licensing sectors, so its supply chain exposure is minimal. Its main cost structure involves content creation and digital distribution, not manufacturing or imports.

Conclusion: Tariff exposure is negligible; no related mitigation measures or risks were discussed.

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Between Q2 2025 and Q3 2025, CuriosityStream’s narrative evolved from bold conceptual transformation to measurable operational momentum.In Q2, CEO Clint Stinchcomb positioned the company as a pioneer redefining media through AI licensing, passionately defending the longevity and scalability of that model. The message centered on vision, potential, and intellectual leadership in a fast-moving field.

By Q3, the tone shifted toward proof of execution — management detailed recurring partnerships, doubled library size, strong cash flow, and cultural discipline. The narrative now blends technological ambition with financial credibility, positioning CuriosityStream as an AI data licensor with steady cash returns and dividend reliability.

Year-over-year comparison

Between Q3 2024 and Q3 2025, CuriosityStream’s story evolved from a streaming turnaround to an AI data-licensing transformation.

In Q3 2024, the company was proving it could survive and generate cash. Management emphasized efficiency, rationalization, and modest licensing wins. The messaging was careful, pragmatic, and defensive — focused on credibility after years of volatility.

By Q3 2025, that narrative flipped. CuriosityStream positioned itself as a profitable, dividend-paying AI data licensor operating at the crossroads of media and technology. The tone was ambitious but grounded, highlighting operational maturity, recurring revenue, and leadership in a new category — “video licensing for AI training.”

Final Takeaway

CuriosityStream (CURI) is in a growth-to-transformation phase, pivoting from pure-streaming to AI-driven content licensing. While profitability is obscured by one-time SBC, underlying free cash flow strength and a debt-free balance sheet underpin a sustainable dividend and credible growth path.

Execution on AI licensing expansion, CaaS adoption, and subscription stabilization will determine whether CURI graduates from niche media to a recognized AI infrastructure play.

Verdict: BUY, with strong upside potential as the market digests the pivot and sees recurring AI licensing revenue materialize.