CuriosityStream Inc. (NASDAQ: CURI) – Q2 2025 Earnings

CuriosityStream Inc. (NASDAQ: CURI) – Q2 2025 Earnings

Earnings Release Date: Aug. 5, 2025

Stock Price: $4.93

Market Cap: $282.7 million

Q2 2025 sales of $19.0 million vs $12.4 million in the prior year

Q2 2025 EPS of $0.01 vs ($0.04) in the prior year

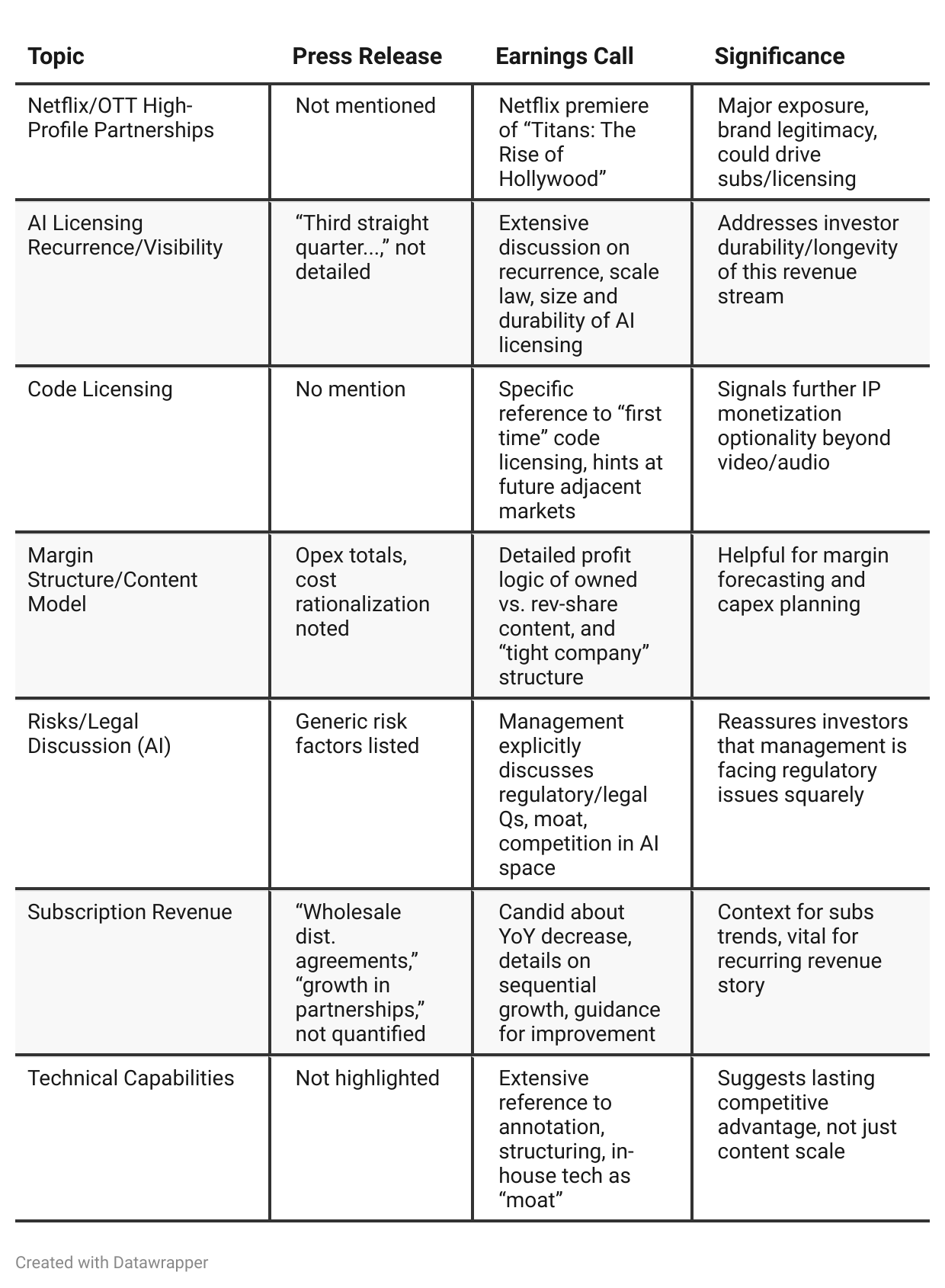

Press Release vs Call Transcript Comparison

Capital Return: Dividend yield at 6.5% (call), and payout of both ordinary and special dividends (release), differentiates CURI from most peers—positive for income investors, but limits reinvestment in growth.

Liquidity & Balance Sheet: $30.7M cash/securities, no debt—provides downside protection and operational flexibility.

Guidance Integrity: Both documents reiterate full-year and Q3 guidance, but only the call explains underlying assumptions, notably that licensing is outpacing subscriptions.

Management Tone: The call is more candid, strategic, and confident about the future—especially around AI licensing’s longevity and CURI’s unique position. The press release is upbeat but less nuanced.

Potential M&A: Hints that company may consider outright content/library purchases as an “ongoing” strategy (call), not described in release—potential capex spike or expanded asset base.

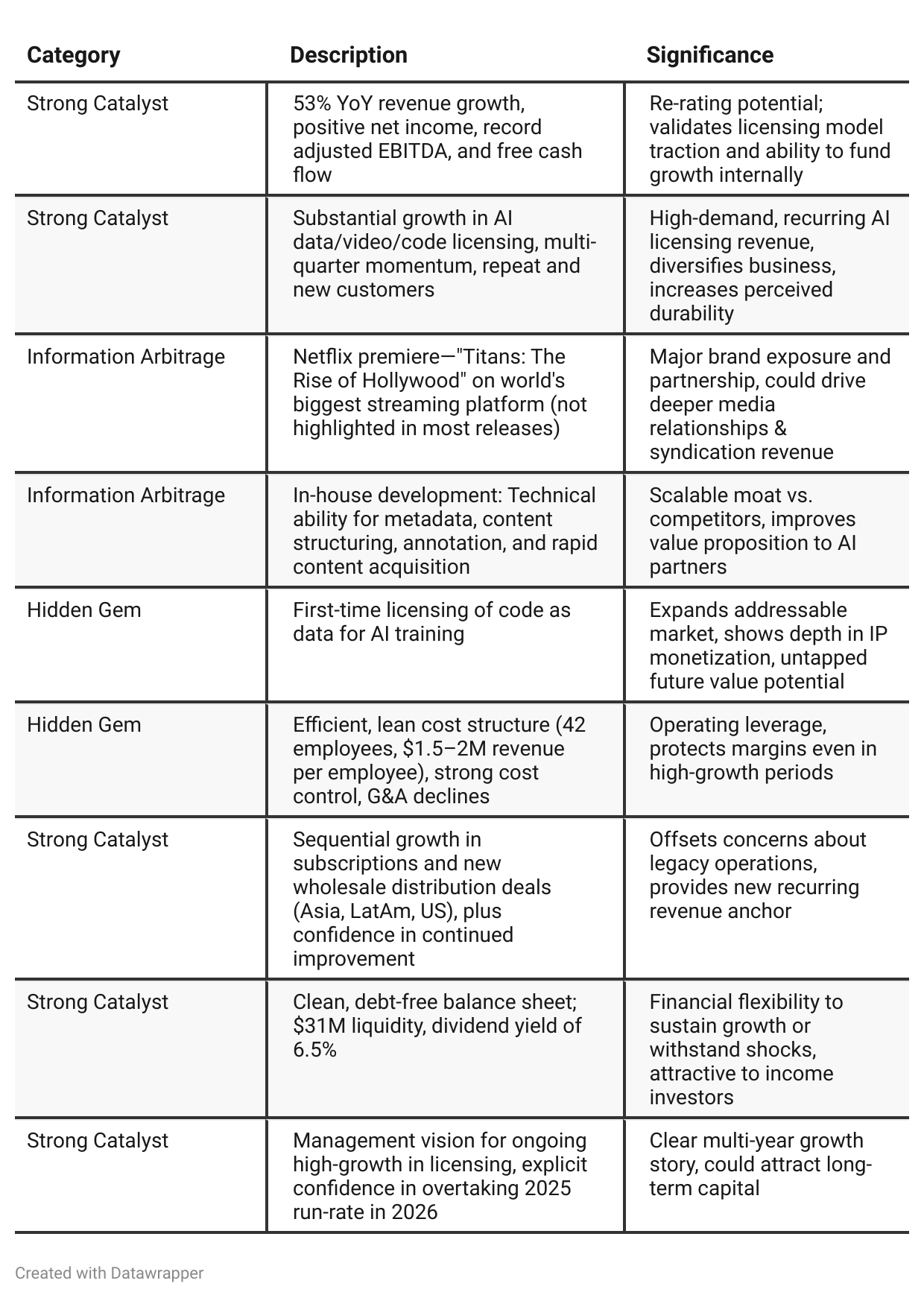

Positive Insights

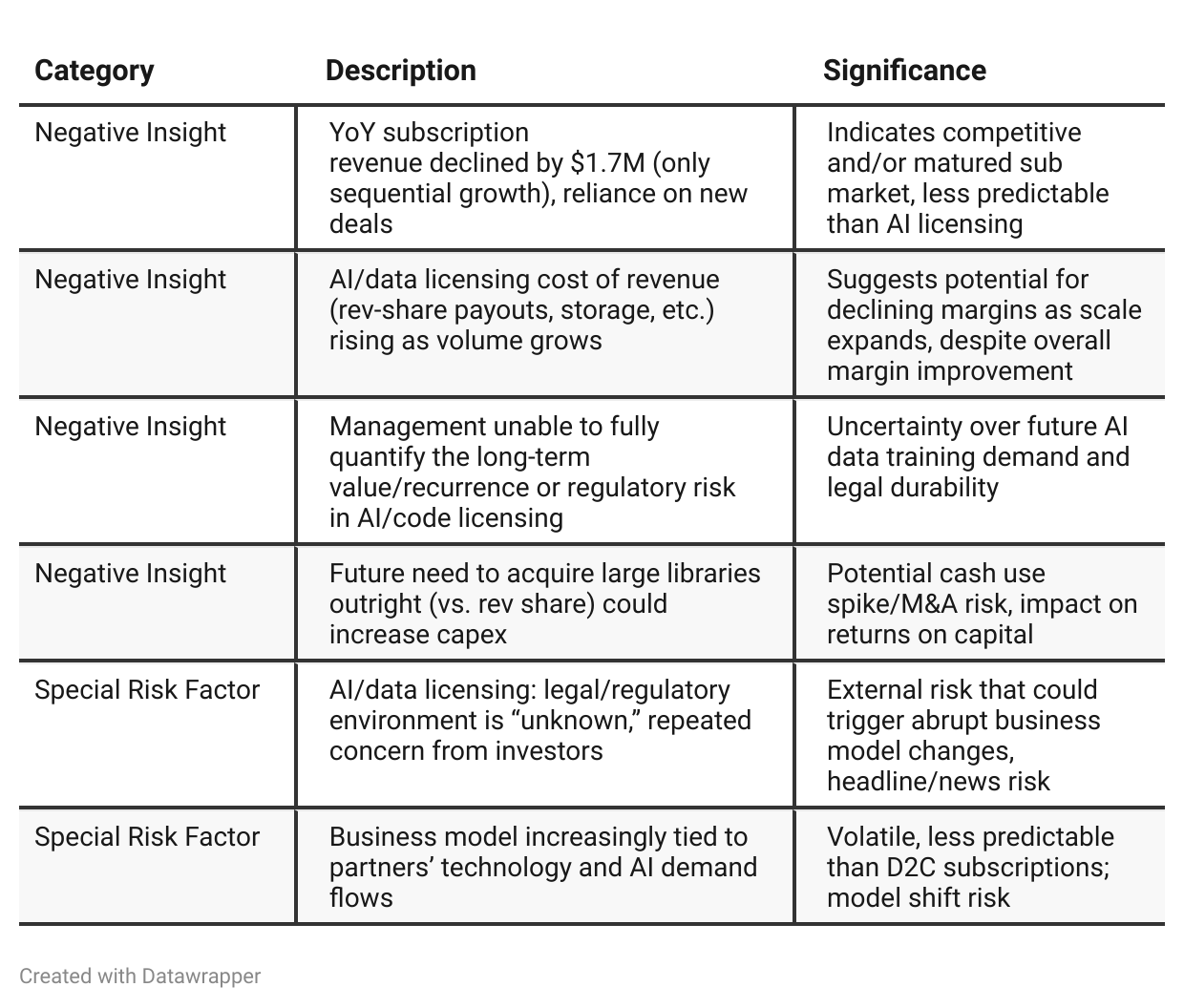

Negative Insights

Tariff Risk

Transcript Mentions:

There is no direct mention of tariffs, U.S. trade policy, or related supply chain impacts in the Q2 2025 earnings call transcript.

Assessment:

CuriosityStream’s business model is centered around digital content licensing, streaming, and selling intellectual property/assets for AI training, which offers a natural insulation from conventional tariffs that typically affect physical goods or component supply chains.

While the company is expanding into international markets (Asia, Latin America, Europe), there is no indication that foreign content licensing, distribution, or streaming operations are currently constrained by tariffs or protectionist policy.

Potential Indirect Risks:

Geo-political/data localization regulation: As the company deals in content and data, changes in international data privacy laws, digital/content tariffs, or new cross-border IP restrictions could in the future represent similar challenges to conventional tariffs—even if not discussed here.

International Expansion: If tensions rise between the U.S. and certain countries, regulatory complexities rather than tariffs may affect CuriosityStream's deals or repatriation of international revenue.

Mitigation:

The transcript provides confidence that CURI’s focus on “ethically sourced, rights-cleared” content and strong global partnerships may help mitigate future regulatory risks—even as no explicit mention is made of mitigation strategies for tariff scenarios.

Forward-Looking:

Investors should monitor for any future statements regarding international content distribution, global expansion impacts, or new legal hurdles that could stem from global trade policy shifts affecting digital media or data flows.

Sentiment Analysis

The overall sentiment toward CuriosityStream ($CURI) is bullish. Investors express optimism about the company's recent earnings performance, dividend yield, and growth in data licensing, highlighting its recovery potential, valuation appeal, and technical strength. Despite some mentions of profit-taking or short-term disappointment after a gap-up, these are outweighed by consistent comments emphasizing buying, holding, and upward expectations, as well as anticipation of positive guidance or further price appreciation.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: CuriosityStream’s narrative centered on achievement of long-sought financial sustainability. Management proudly highlighted their transition from cash-burning to consistently cash-generative, punctuated by positive net income and free cash flow, dividend initiation, and sharp cost discipline. Growth was tied to surging content/data licensing to tech and media, while keeping the subscription business stable and optimizing for marketing efficiency. There was careful optimism but an undercurrent of caution regarding future “lumpiness” and a need to prove that AI/data licensing is repeatable, not just a one-off.Q2 2025: The company’s tone and outlook shift decisively toward bold, long-term positioning. Management frames CuriosityStream as not just stable but transformative—a likely industry leader in AI/data content licensing. The Q2 call is both more ambitious and more granular: it introduces competitive differentiators such as technical metadata capabilities, emphasizes repeat and expanding AI licensing, and displays confidence through increased and special dividends. Risks are acknowledged (especially legal/regulatory AI issues), but CURI shows much greater swagger in discussing its “moat,” new revenue opportunities (including code licensing), and ability to ride—and shape—a technological paradigm shift. The message is no longer about just survival and stability, but about stepping onto a much bigger growth stage in the industry.

Year-over-year comparison

In Q2 2024, CuriosityStream was still in the late stages of operational turnaround: steadfastly focused on cost control, repeatable cash generation, and proving it could be a sustainably profitable, dividend-paying business. Growth was welcome but cautious; licensing and partnership deals were variable, and any enthusiasm was tempered by the need to maintain stability. Management wanted the market to know that CURI had roots, discipline, and resilience, with early optionality in exploring data/AI monetization.

By Q2 2025, the narrative leaps forward with confidence, boldness, and ambition. Management now sees CuriosityStream not just as a survivor or solid operator but as an innovator and industry leader—particularly in the booming field of AI-driven content/data licensing. New lines of recurring revenue, technical innovations in metadata and IP structuring, and high-profile partnerships (like Netflix) underpin a vision of CURI as an “outlier” uniquely ready to thrive as the media and technology landscape transforms. Candid about risks, management is more eager to talk about scalable moats, industry dominance, and a future where CuriosityStream is a key input provider to the AI revolution, rather than just a content library for streaming platforms.

Final Takeaway

CuriosityStream is in a high-growth, transition phase, rapidly scaling its AI/data licensing business while maintaining robust cash flow and capital returns. The company’s proprietary content library, in-house tech capabilities, and expanding global reach give it a defensible advantage. While positive momentum in AI-related revenues and efficient cost controls support a bullish view, investors should watch for regulatory/legal risks and the evolving success of subscription and nascent ad streams. Execution on licensing renewal, margin discipline, and legal risk management will be crucial.

Verdict: Buy, with strong upside if AI demand persists and subscription recovery materializes—regulatory clarity and competitor moves are key watch items.