Core Molding Technologies, Inc. (NYSE: CMT) – Q3 2025 Earnings

Core Molding Technologies, Inc. (NYSE: CMT) – Q3 2025 Earnings

Earnings Release Date: Nov. 04, 2025

Stock Price: $18.34

Market Cap: $158.1 million

Q3 2025 sales of $58.4 million vs $73.0 million in the prior year

Q3 2025 EPS of $0.22 vs $0.36 in the prior year

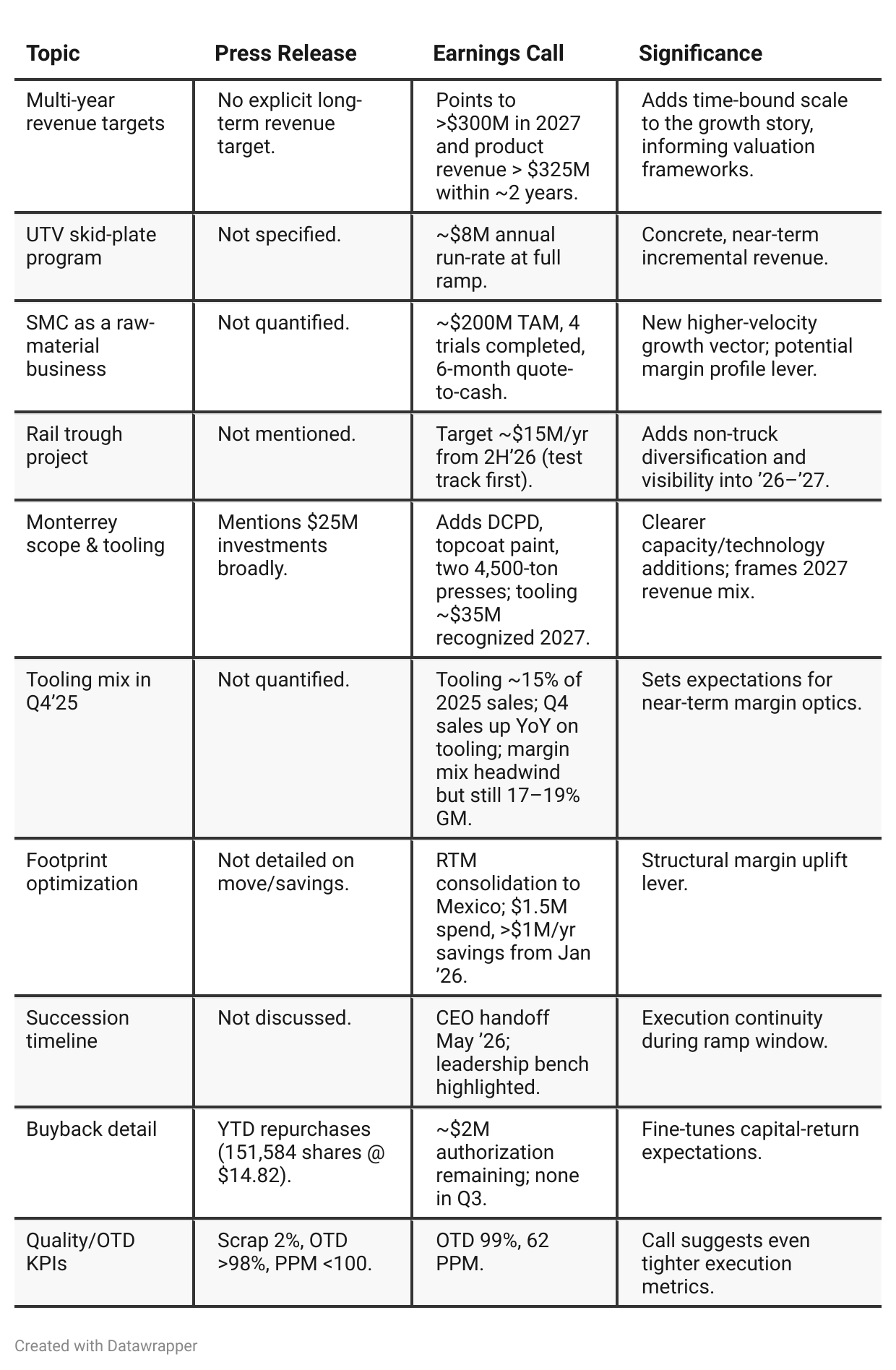

Press Release vs Call Transcript Comparison

Mix optics vs. core health: Tooling surge boosts Q4 sales but dilutes gross margin; management still anchors 17–19% GM, implying underlying operations remain strong.

Balance sheet = offensive option: Liquidity $92.4M and debt <1x TTM Adj. EBITDA supports ongoing capex and possible selective buybacks.

Cycle hedge: Diversification (power sports recovery, building products, industrial/utilities + rail) lessens reliance on truck timing.

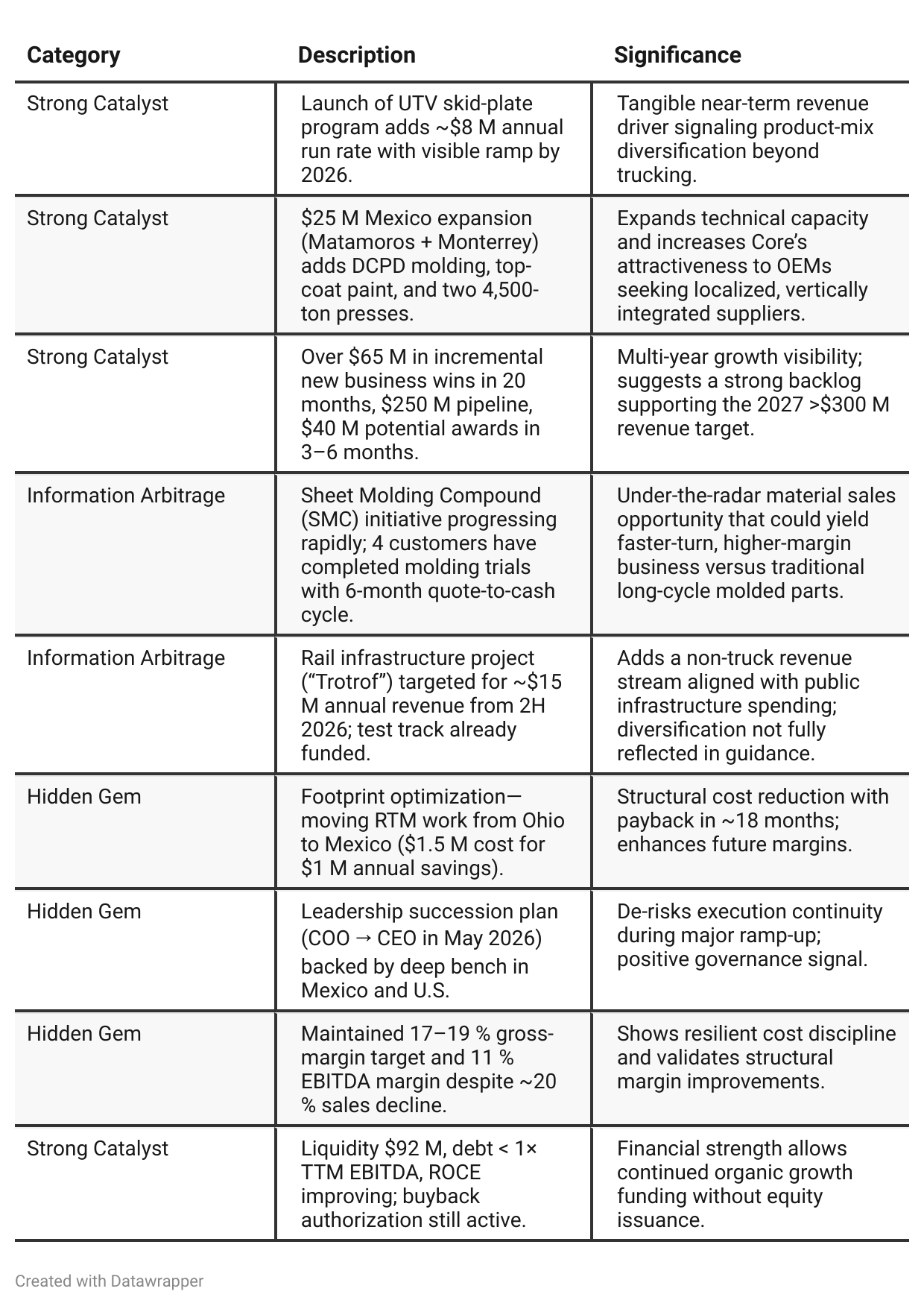

Positive Insights

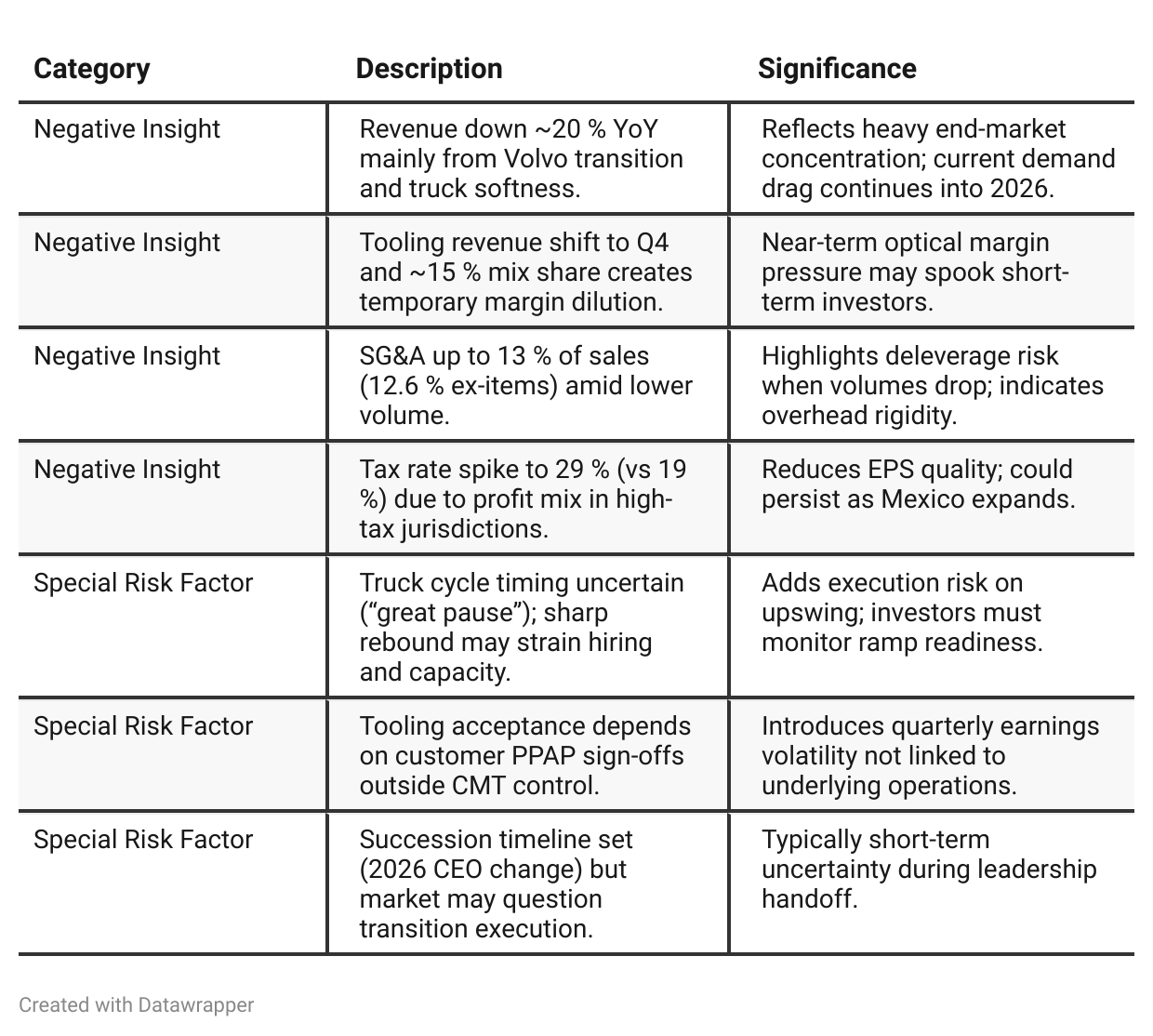

Negative Insights

Tariff Risk

Tariffs were addressed directly in both management remarks and Q&A:

Exposure: Products are USMCA-compliant (operations in U.S., Mexico, and Canada) and currently exempt from tariffs.

Risk Mechanism: Biggest concern is demand softness from customers if tariffs persist or expand to truck OEMs.

Mitigation: (1) Dual geographic operations allow shifting production if tariffs change. (2) Contracts include raw-material adjusters to pass through cost increases.

Forward View: Monitoring policy uncertainty into 2026; no direct financial impact yet.

Assessment: Low direct tariff risk currently; management appears proactive in pricing and logistics structure.

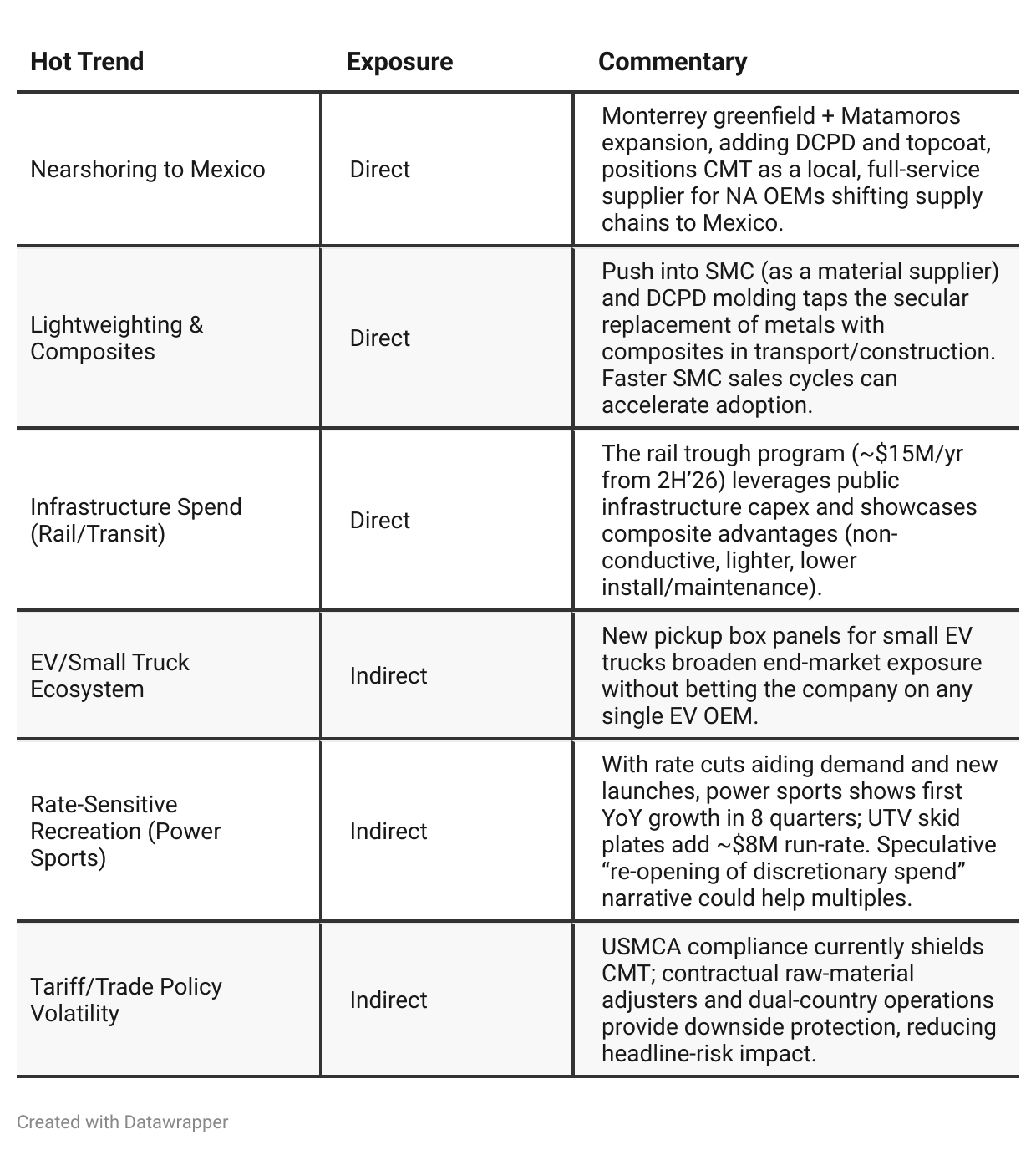

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

From Q2’25’s “we’ve won a lot and are building capacity” to Q3’25’s “we’re converting wins into live programs, sharpening the sales engine, and managing mix/timing.” The narrative advances from strategic ambition (wins, capex, SMC TAM) to operational specificity (UTV live, SMC trials, rail test track, tooling timing), while keeping the >$300M revenue target intact and acknowledging near-term volatility from tooling and truck demand.Year-over-year comparison

Q3 2024 → “Transformation Complete, Growth Phase Begins.”

CMT framed itself as emerging from a four-year turnaround with operational stability, improved margins, and an ambitious “Invest for Growth” strategy. Messaging centered on internal capability, culture, and pipeline potential rather than immediate financial acceleration.Q3 2025 → “Execution and Conversion.”

The focus shifted from what they planned to how they are delivering: concrete launches (UTV skid plates), live customer trials (SMC), defined expansion milestones (Mexico), and specific profit improvement actions (footprint shift, cost savings). Management’s language is less visionary, more metric-anchored. Tariffs and truck-cycle caution temper the optimism, yet the >$300 M 2027 revenue target stays central.

Final Takeaway

Core Molding Technologies (CMT) is in a growth and diversification phase, expanding capabilities through near-shoring and new composite processes. While truck demand remains weak short-term, structural investments in SMC materials, rail projects, and power-sports programs build multi-year visibility. Tariff risks are manageable and liquidity strong. Execution on tooling timing and program launches will determine how quickly earnings expand.

Verdict: BUY, with potential upside as 2026 volume recovers and margin leverage kicks in.