Core Molding Technologies, Inc. (NYSE: CMT) – Q2 2025 Earnings

Core Molding Technologies, Inc. (NYSE: CMT) – Q2 2025 Earnings

Earnings Release Date: Aug. 5, 2025

Stock Price: $16.79

Market Cap: $144.7 million

Q2 2025 sales of $79.2 million vs $88.7 million in the prior year

Q2 2025 EPS of $0.47 vs $0.73 in the prior year

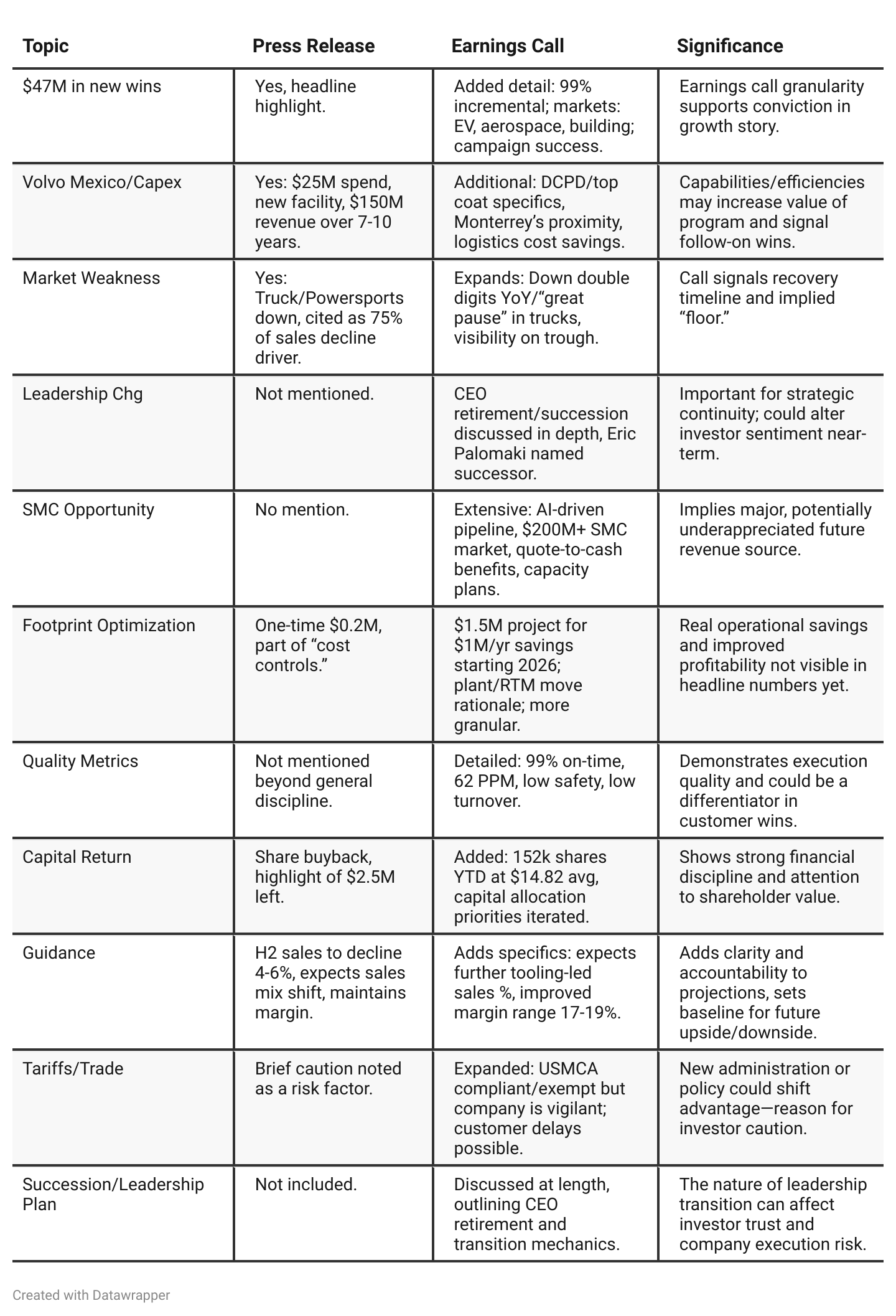

Press Release vs Call Transcript Comparison

Call Is the “Alpha Source”: Much of the upside detail—aggressive SMC pipeline, AI-led sales opportunities, manufacturing/capex granularity, and succession plan—appears only in the earnings call.

Press Release Is “Safe,” Call Has “Risk/Reward”: The PR supports base-case investment. The call, for an attentive investor, surfaces both greater risk (market/leadership) and the higher reward (SMC/expansion/efficiencies).

Margin Management, Not Growth Yet Drives Story: Near-term numbers are protected by cost and mix management—not truly organic volume growth. Forward potential hinges on conversion of new business pipeline and industry rebound.

Leadership Transition Needs Watching: The call’s detailed succession plan clearly lays groundwork for continuity, but leadership transitions retain inherent risk for execution drift or cultural change.

Capital Structure and Buyback: Strong liquidity and prudent leverage (<1x EBITDA) provide flexibility and signal balance sheet safety for growth or downturn.

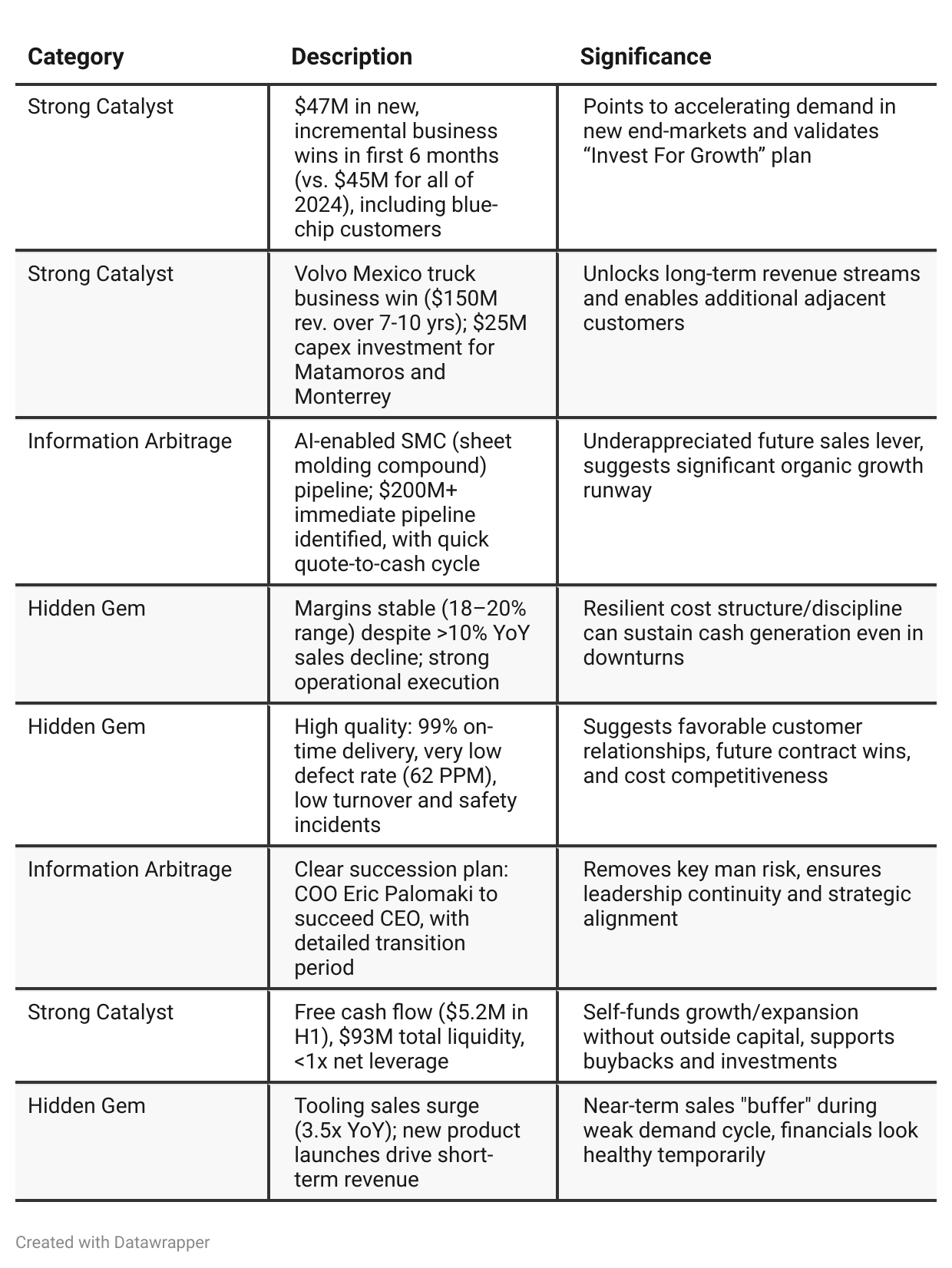

Positive Insights

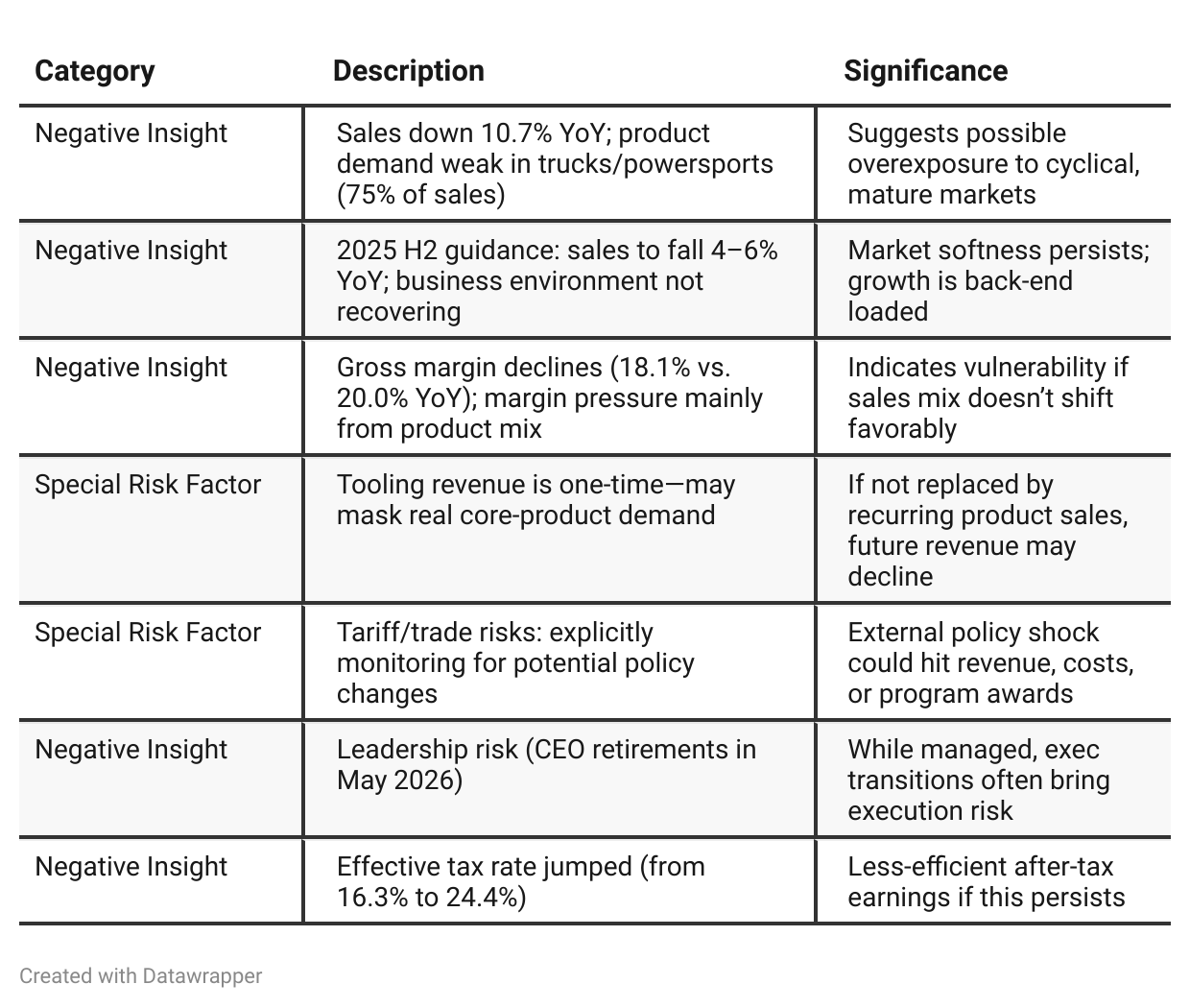

Negative Insights

Tariff Risk

Transcript Mentions: "our products in both Canada and Mexico are USMCA compliant and are currently exempt from tariffs. However, we will continue to closely monitor how changes in trade policies affect our customers and their end markets."

Contextual Details: Management acknowledges potential risk from future changes in U.S. trade policy and tariffs, and there are hints that tariff uncertainties are causing delays "in the market, both in demand and in the awarding of new programs."

Mitigation Activities: No specific supply chain shifts or contract renegotiations are described; company positions itself as “vigilant” and is actively monitoring potential policy changes, but does not provide explicit mitigation strategies such as shifting production, renegotiating contracts, or altering pricing at this time.

The effect of tariffs is currently neutral due to USMCA compliance, but future changes could introduce downside risk through delayed customer awards, shifts in demand, or cost impacts. Investors should track management commentary in future calls, SEC filings, and government trade policy updates for any escalation or mitigation plans. No impact on market share or innovation capacity was directly mentioned in this call, but vigilance is warranted as Core Molding remains exposed to U.S. and North American trade policy shifts.

Sentiment Analysis

The overall sentiment towards the stock is bullish. Multiple investors express optimism about the company's technical setup, anticipate continued price appreciation, and reference breakout patterns and specific price targets that are significantly higher than current levels. The consistent use of positive language, targets, and technical signals reflects strong confidence in further upward movement for the stock.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q1 2025: Core Molding Technologies entered 2025 highlighting its turnaround, operational discipline, and readiness to invest for growth. Despite soft end-market demand, particularly in trucks and powersports, management remained confident in its ability to maintain margins and cash flow through cost control. The pipeline was described as robust, but decision-making and order timing from customers was cited as a key challenge. Investments in SMC production and facility upgrades were mapped out, with a playbook focused on being ready to capture growth as market conditions improve. M&A and organic sales expansion were both in consideration, but nothing transformative had landed yet.Q2 2025: By Q2, the company’s story had shifted from “preparation and waiting” to “execution and momentum.” Major new contracts—most notably the Volvo Mexico win and a rapid build in incremental business—validated the investment-for-growth strategy and marked a tangible step forward. Capex and expansion plans accelerated, with more detailed linkage to captured revenue opportunities as well as expanded product/market offerings. Sentiment was more explicitly upbeat and forward-looking, with AI-enabled revenue opportunities materializing and cost structure improvements being quantified. The company also began communicating about its leadership succession plan, aiming for stability and continuity into its next chapter. Management acknowledged macroeconomic hurdles but now foregrounded contract wins and growth levers as offsetting these challenges.

Year-over-year comparison

Q2 2024: Core Molding Technologies was in a transitional phase, having completed much of the heavy lifting on operational transformation and now shifting focus to sales and marketing execution to unlock future growth. The company was proud of its quality/service wins, but patient: the pipeline was strong, sales cycles long, and end-market demand soft, especially in trucks. Efforts were underway to hire and structure for scalable, diversified, vertical-led growth—but substantial improvement was promised for the future, not yet in hand.

Q2 2025: The company’s narrative has shifted to tangible results and external validation. Investments in people, processes, and capability have paid off, reflected in record new business (with most wins incremental), major blue-chip contracts, and expansion into new markets and technologies. While macro softness persists, Core Molding points directly to closed deals and detailed capex for growth. There’s confidence in both management succession and operational execution, as well as a clear vision of scaling up annual revenue despite slow legacy end-markets. The strategy is the same—but now delivers actionable growth and deeper competitive advantages.

Final Takeaway

Core Molding Technologies, Inc. is in a transition phase, aiming to pivot from legacy markets to diversified, higher-growth verticals through organic growth, AI-enabled lead generation, and a major program with Volvo. While impressive new business wins, margin stability, and financial discipline lay a solid foundation, weak legacy end-markets, reliance on one-time tooling revenue, and the upcoming CEO transition present tangible risks. Execution on the SMC pipeline, realization of new customer wins, and macro recovery are critical for future performance. Verdict: Hold, with moderate upside potential if key initiatives deliver and demand stabilizes. Monitor pipeline conversion, margin trends, and leadership handoff.