Celestica Inc. (NYSE: CLS) – Q3 2025 Earnings

Celestica Inc. (NYSE: CLS) – Q3 2025 Earnings

Earnings Release Date: Oct. 27, 2025

Stock Price: $296.6

Market Cap: $34111.3 million

Q3 2025 sales of $3.19 billion vs $2.50 billion in the prior year

Q3 2025 EPS of $2.31 vs $0.75 in the prior year

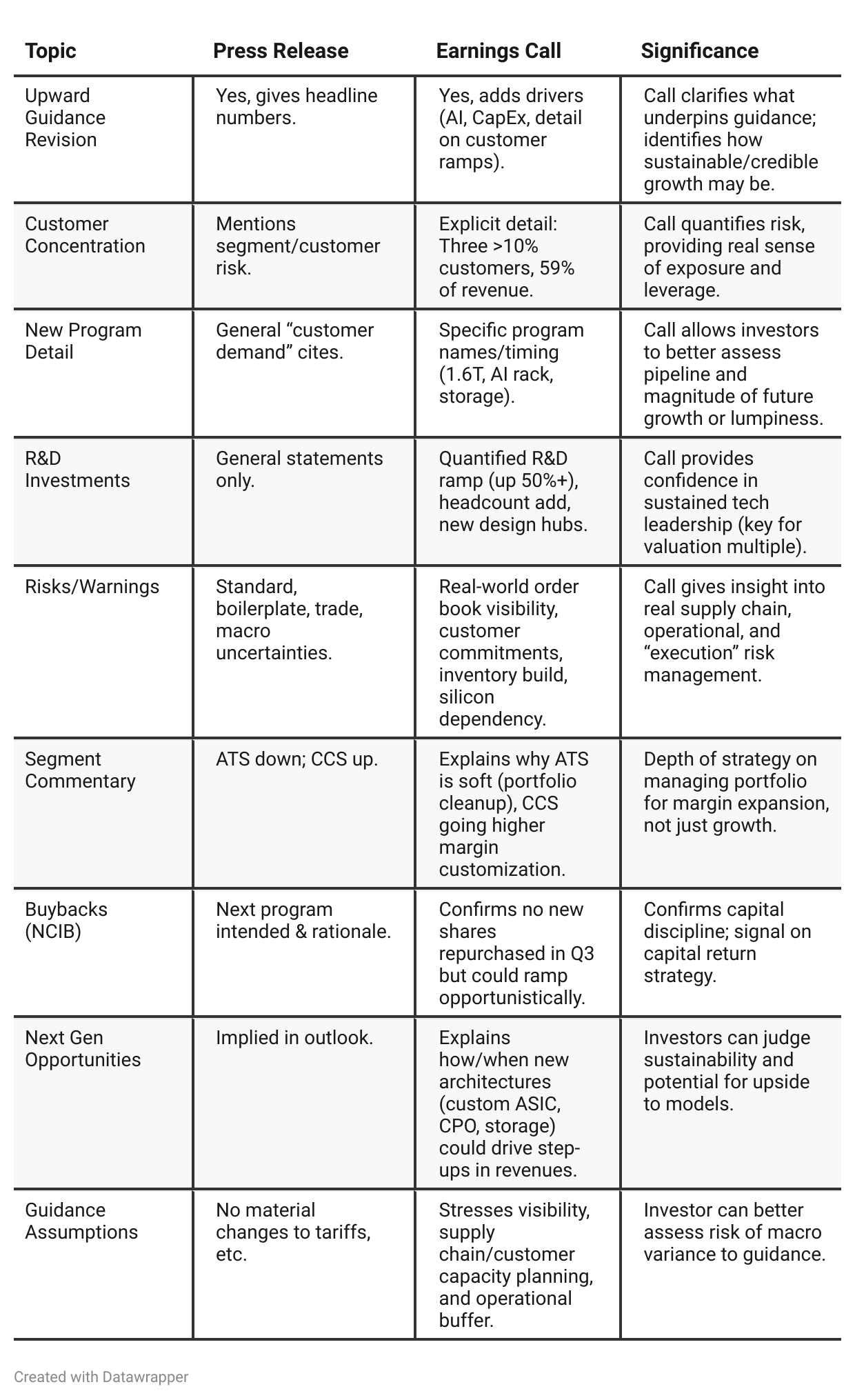

Press Release vs Call Transcript Comparison

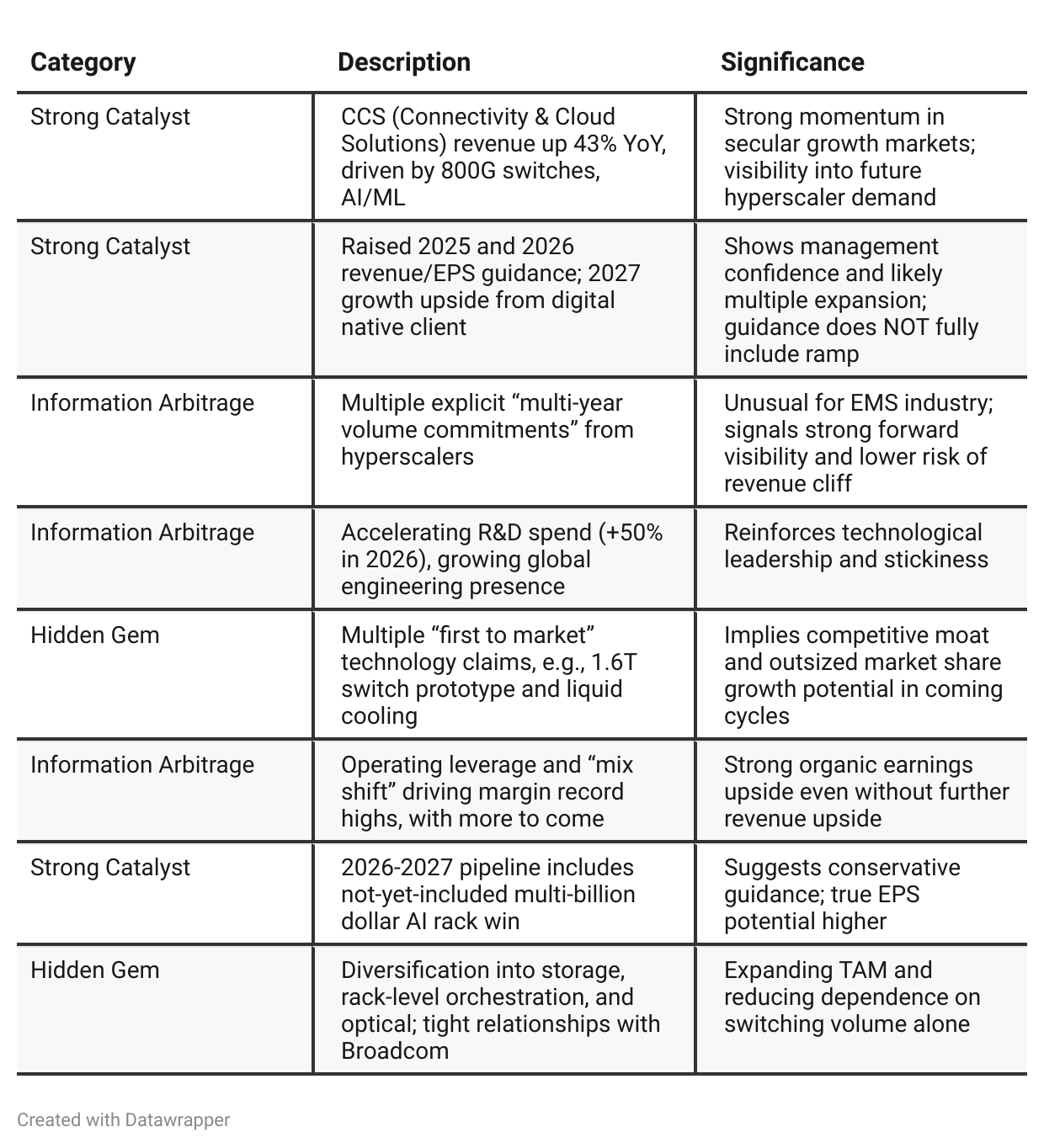

Operating Leverage: The call highlights that much of the margin gain is from mix shift and operating leverage—not just cost cuts—which is positive, but notes that certain service/program lines (e.g., complex rack integration) can be dilutive.

Strategic Positioning: Call details strong incumbency in scale-up/-out networking, with stated intention to cross-sell into broader enterprise, moving beyond exclusive dependency on hyperscalers.

Technology Barriers: Describes why rapid switch cycles (400G→800G→1.6T→3.2T) are a structural advantage for Celestica (barrier to entry, first-mover, sticky customer position).

Sustainability of Growth: Call interviews and Q&A strongly support multi-year visibility (through 2027), but stress that not all upside is captured in present guidance (digital native AI racks ramping not fully reflected yet).

Balance Sheet: Very strong cash flow, low leverage, substantial available revolver—financial flexibility for buybacks, select M&A, capex as opportunities dictate.

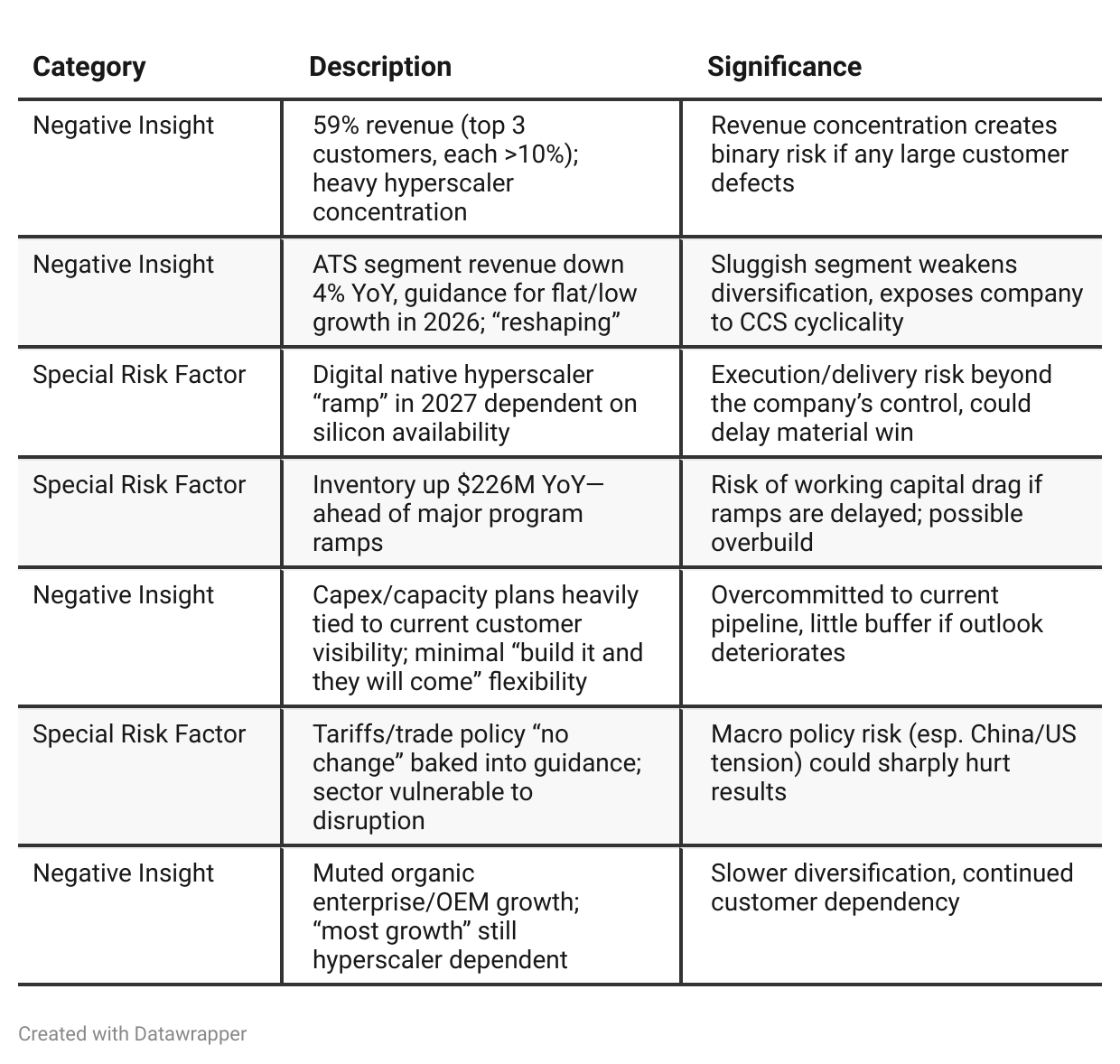

Positive Insights

Negative Insights

Tariff Risk

Guidance Sensitivity: All financial guidance explicitly assumes no material changes to current tariff or trade restrictions. Any new tariffs could negatively impact results.

Mitigation: Celestica claims most tariff costs are passed through to customers and is investing in manufacturing capacity in both the U.S. and Asia to provide supply flexibility.

Exposure: Some customers (especially in ATS/semiconductor) are delaying investments pending tariff clarity, highlighting the broader risk to demand.

Bottom Line: Tariffs are not currently impacting results, but significant new trade actions or escalation could pressure margins, slow projects, and force a downward revision of guidance. Investors should watch for signs of policy changes and supply chain movement in future updates.

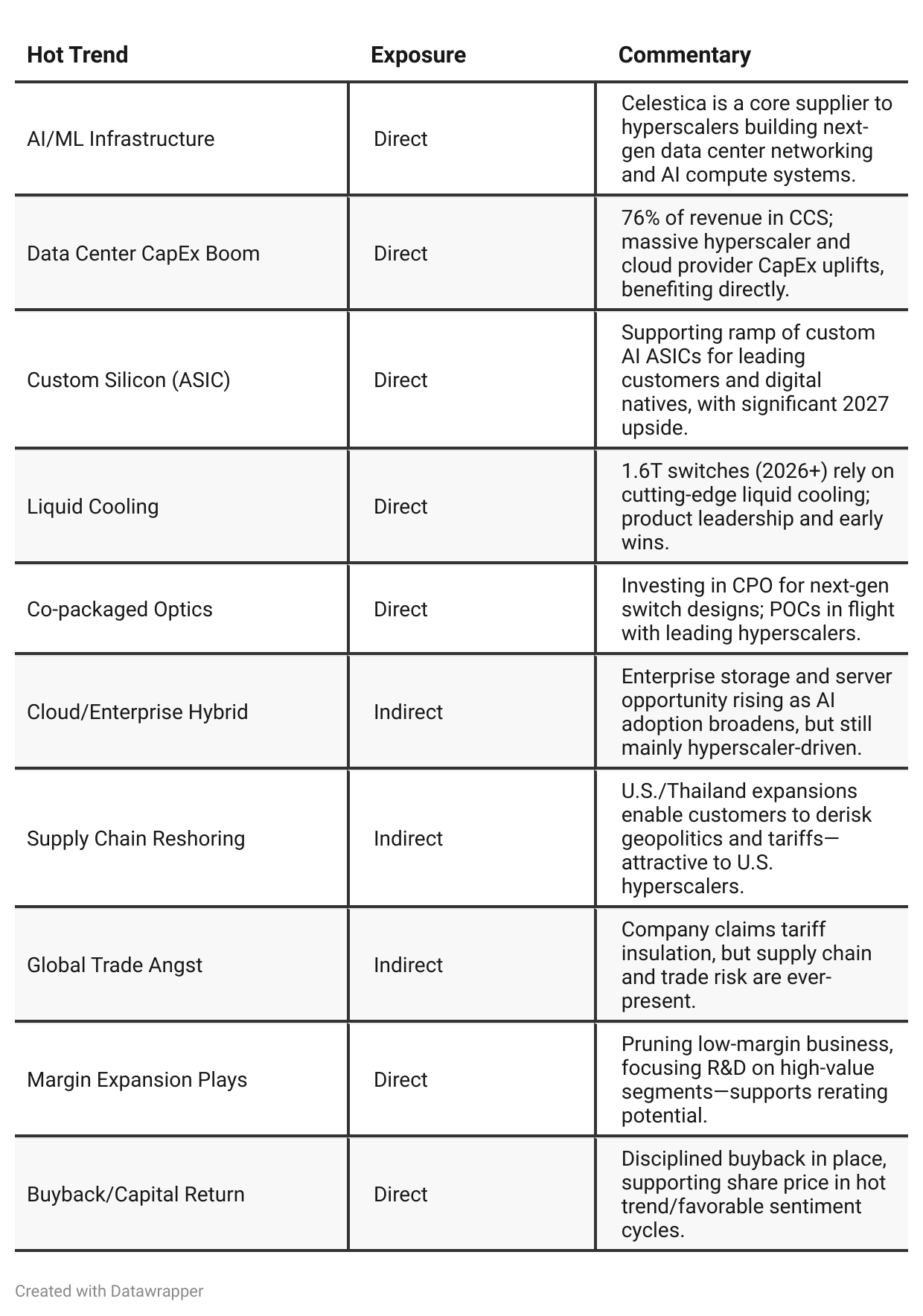

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025: Celestica is executing well in a high-growth environment, leveraging hyperscaler demand and networking transitions (400G→800G). The tone is one of cautious success—upwardly revised guidance is based on strong backlog and execution, yet tempered by external risks (macro, tariffs, supply chain). The story is centered around growth, operational resilience, and expanding customer/program breadth, with a “high-confidence” but not exuberant outlook.Q3 2025: The narrative becomes transformative and future-centric. Confidence grows, with the company positioning itself not just as a top-tier supplier, but as an emerging global technology platform leader in AI/datacenter infrastructure. Management shifts messaging to emphasize innovation (R&D, hiring, system-level solutions, liquid cooling, scale-up networking), deepening competitive moat, and multi-year, high-visibility opportunities—especially from new AI rack-scale programs and custom ASIC platforms. While margin and growth momentum continue, the tone becomes one of urgency (“accelerating change”), vision, and the validation of a long-term strategic pivot—albeit with even clearer articulation of concentration and execution risks and macro uncertainties.

Year-over-year comparison

Q3 2024: Celestica is beating peers on growth and margin; strong demand for networking switches and custom compute platforms with hyperscalers. Careful management of operating leverage, capital allocation, and legacy portfolio (especially in ATS/industrial) is driving record results. The future looks bright, but near-term bumps (“technology transitions”) are acknowledged, and the company is building out capabilities to capture more of the AI hardware stack.

Q3 2025: With those capabilities now developed and validated through major customer program wins, Celestica is in “hyper-growth” mode—investing massively in R&D, expanding global capacity, and pursuing ever more complex and lucrative AI infrastructure projects (rack-scale, liquid cooling, software-enabled offerings). The company is not just managing industry cycles, it is increasingly shaping them: moving into leadership roles in emerging standards (scale-up Ethernet, custom ASICs), and deepening entrenched relationships with the world’s most demanding customers. Financial guidance and confidence have been dramatically raised, and the narrative is now about sustaining multi-year compounded growth, asserting technology leadership, and being the “go-to” partner for cutting-edge data center deployments.

Final Takeaway

Celestica is executing extremely well on explosive AI/data center trends, with unique multi-year customer commitments and margin expansion levers. Its ability to balance aggressive growth with operational discipline stands out, but outsized dependence on a few hyperscalers and vulnerability to global trade policy are real risks. Success now hinges on execution and the macro/trade environment holding steady. BUY with the proviso that investors closely monitor signs of trade, customer, or supply chain disruption for any change in trajectory.