Celestica Inc. (NYSE: CLS) – Q2 2025 Earnings

Celestica Inc. (NYSE: CLS) – Q2 2025 Earnings

Earnings Release Date: Jul. 28, 2025

Stock Price: $170.22

Market Cap: $19592.3 million

Q2 2025 sales of $2.89 billion vs $2.39 billion in the prior year

Q2 2025 EPS of $1.82 vs $0.80 in the prior year

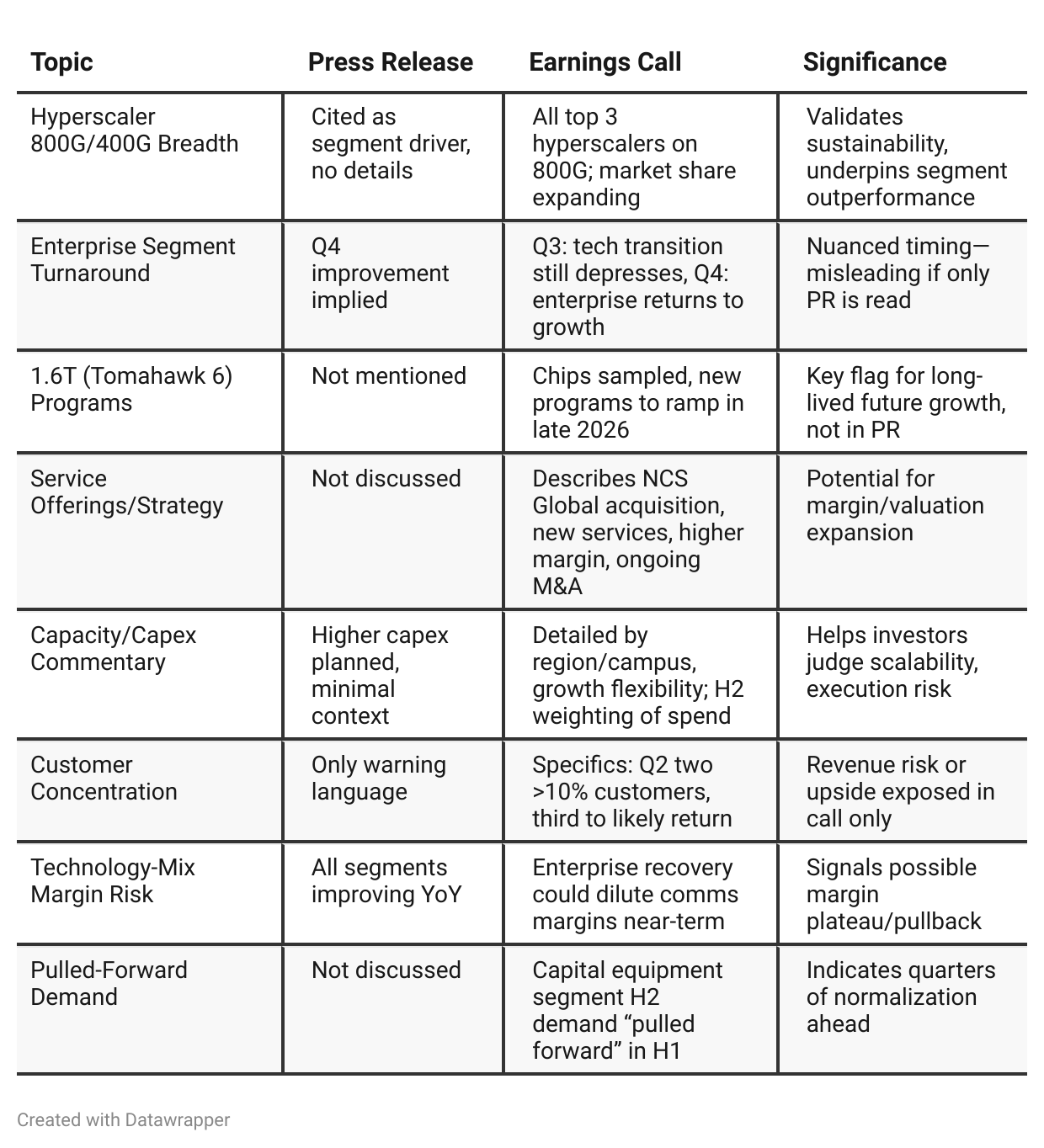

Press Release vs Call Transcript Comparison

Numbers Alone Are Not Strategy: The press release makes the quarter look like a broad-based blowout; only the call reveals tech/demand “puts and takes” and underlying transition risks.

Growth Drivers Are Narrow and Cyclical: Growth is extremely skewed to a handful of large hyperscalers and tech transitions (400/800G/1.6T), with lots of volatility and dependency.

Operational Flexibility Is a Strength—But Also a Risk: Company stresses its ability to scale quickly and “fill buildings,” but this could leave excess capex if demand softens. The call mentions 12-month lead times for facility expansion, a crucial input for modeling future returns and cash consumption.

Margin Expansion May Plateau: While new record margins are noted, call Q&A suggests that further upside is increasingly dependent on higher-value-add (services, next-gen programs), with some normalization as the business mix shifts.

Services Could Support a Higher Multiple: Reference in the call to services (and higher margins thereof) signals a potential business model evolution that could drive a rerating—call listeners know to flag this long before numbers show up.

Timing of Next Guidance Critical: Management defers longer-term (2026) visibility to the next call, implying some uncertainty/potential downside about how durable this demand really is.

No Big Surprises in Financials, but Risks in Mix and Macro: Both release and call show strong cash flow, limited gross debt, and ongoing share repurchases, but also rising inventory and capex—could amplify swings if a hyperscaler delays/cancels orders.

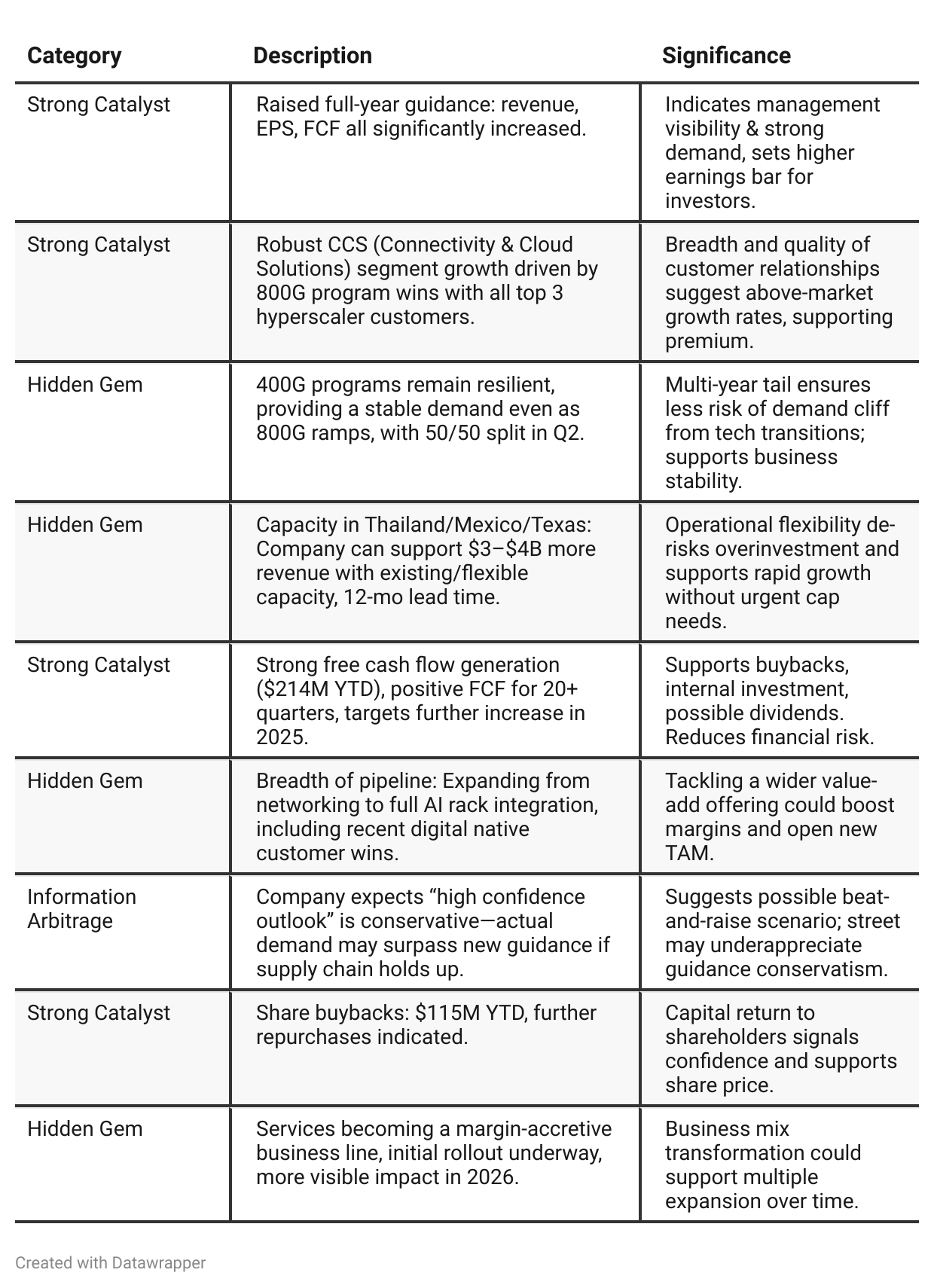

Positive Insights

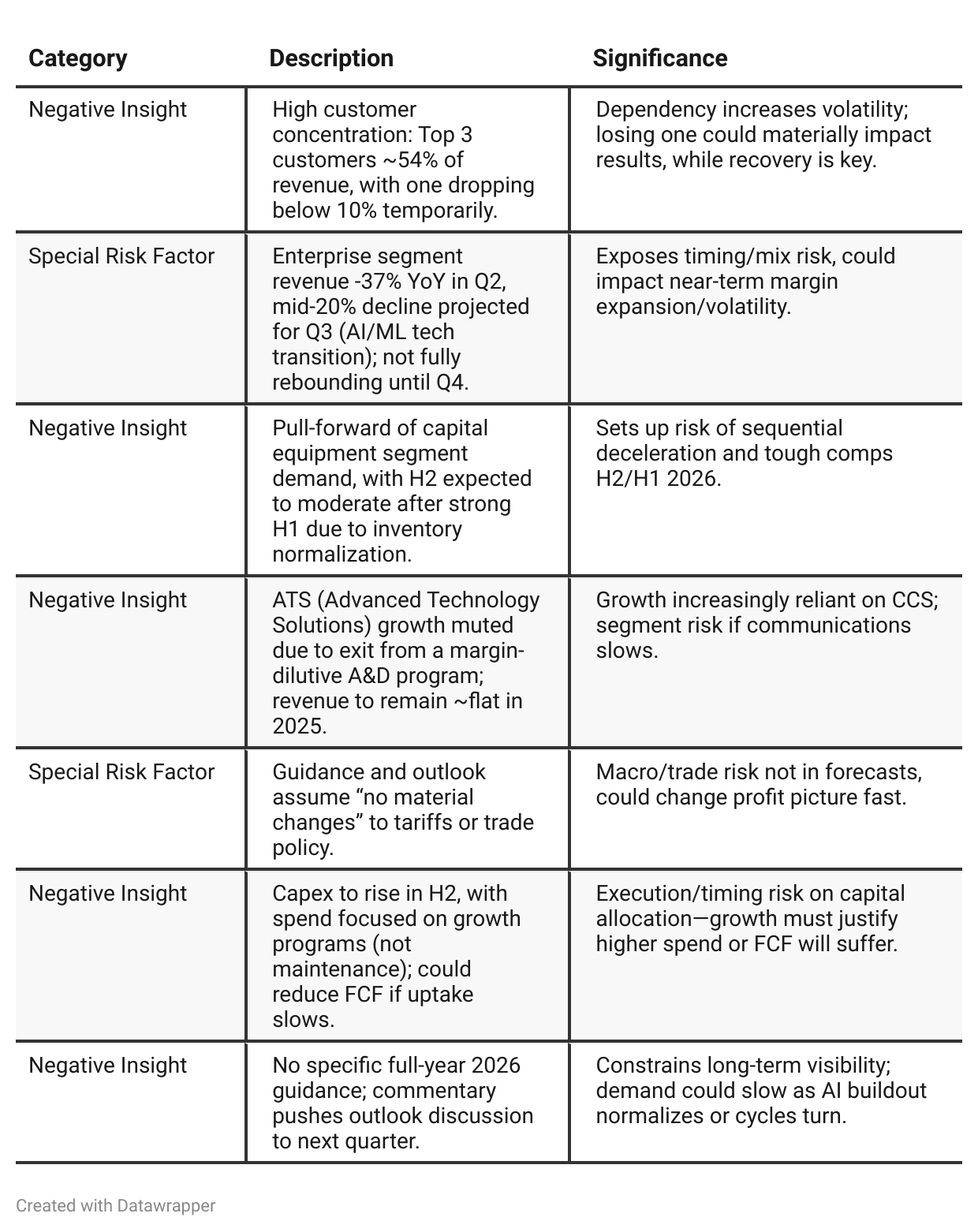

Negative Insights

Tariff Risk

Current Impact: Tariffs had minimal effect in Q2 due to exemptions and pauses; most costs are passed through to customers.

Guidance Assumption: 2025 outlook assumes no major tariff or trade policy changes—any shift could affect revenue and profitability.

Risk Management: Celestica mitigates risk with a flexible, global supply chain and strong customer contracts.

Caution: If tariffs increase or policies change suddenly, margins and forecasts could be at risk. Investors should watch for updates on trade policy.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: Celestica entered 2025 on a note of caution, having built strong momentum but facing a complex macro and trade environment. The company positioned itself as resilient—buoyed by secular demand for AI and hyperscaler capacity, but careful to frame all guidance as risk-adjusted and “high confidence.” They cited flexibility, preparedness for further tariff volatility, and capacity to quickly pivot manufacturing as critical differentiators. The message: “We’re strong, but the world is unpredictable—here’s how we’re protecting the downside.”Q2 2025: Confidence has clearly built quarter-over-quarter. The “resilient” company is now foregrounding execution and market leadership—exceeding guidance, boosting annual targets across the board, and emphasizing operational excellence. Management’s tone is more assertive, less qualified. They discuss the transition toward new technologies (800G/1.6T) as having crossed key milestones, with customer adoption widespread and design win breadth growing. Risk language—while present—is significantly dialed down. The message: “Our strategy is working—we’re not just managing risk, we’re driving growth and taking share.”

Year-over-year comparison

Q2 2024 (July): Celestica enjoyed strong momentum, driven by broad AI and data center buildouts, but while celebrating growth, was balancing optimism with caution around cyclic industrial softness and questions about the durability of the AI cycle. Management focused on operational flexibility, delivering on new technology ramps, and mitigating overinvestment risk through customer and program diversification.

Q2 2025 (July): Celestica’s narrative has turned decidedly more confident. The company is not just riding the AI wave, but explicitly winning the technology transition—delivering record results, raising expectations, and securing a leadership position among hyperscaler customers. Execution is measured by share-of-wallet and breadth of design wins, not just revenue growth. Customer and product mix changes are now positioned as sources of margin enhancement and future growth, with most risks recast as “if macro or trade policy shifts.” The tone is performance-driven, forward-leaning, and less preoccupied with cyclical or macro uncertainties.

Final Takeaway

Celestica is in a late-stage growth phase, leveraging AI/hyperscaler buildouts and strong execution in networking hardware. The company’s raised guidance, robust free cash flow, and expanding customer base are positives, but risks remain in customer concentration, hyperscaler order cyclicality, and policy/trade headlines. Execution on ramping new technology (800G/1.6T), capturing service margin, and enterprise segment recovery will be critical for future outperformance. Verdict: Buy, with upside dependent on sustained AI/CCS investment and downside risk around customer dependency and macro stability.