CECO Environmental Corp. (NASDAQ: CECO) – Q3 2025 Earnings

CECO Environmental Corp. (NASDAQ: CECO) – Q3 2025 Earnings

Earnings Release Date: Oct. 28, 2025

Stock Price: $53.36

Market Cap: $1886.8 million

Q3 2025 sales of $197.6 million vs $135.5 million in the prior year

Q3 2025 EPS of $0.04 vs $0.06 in the prior year

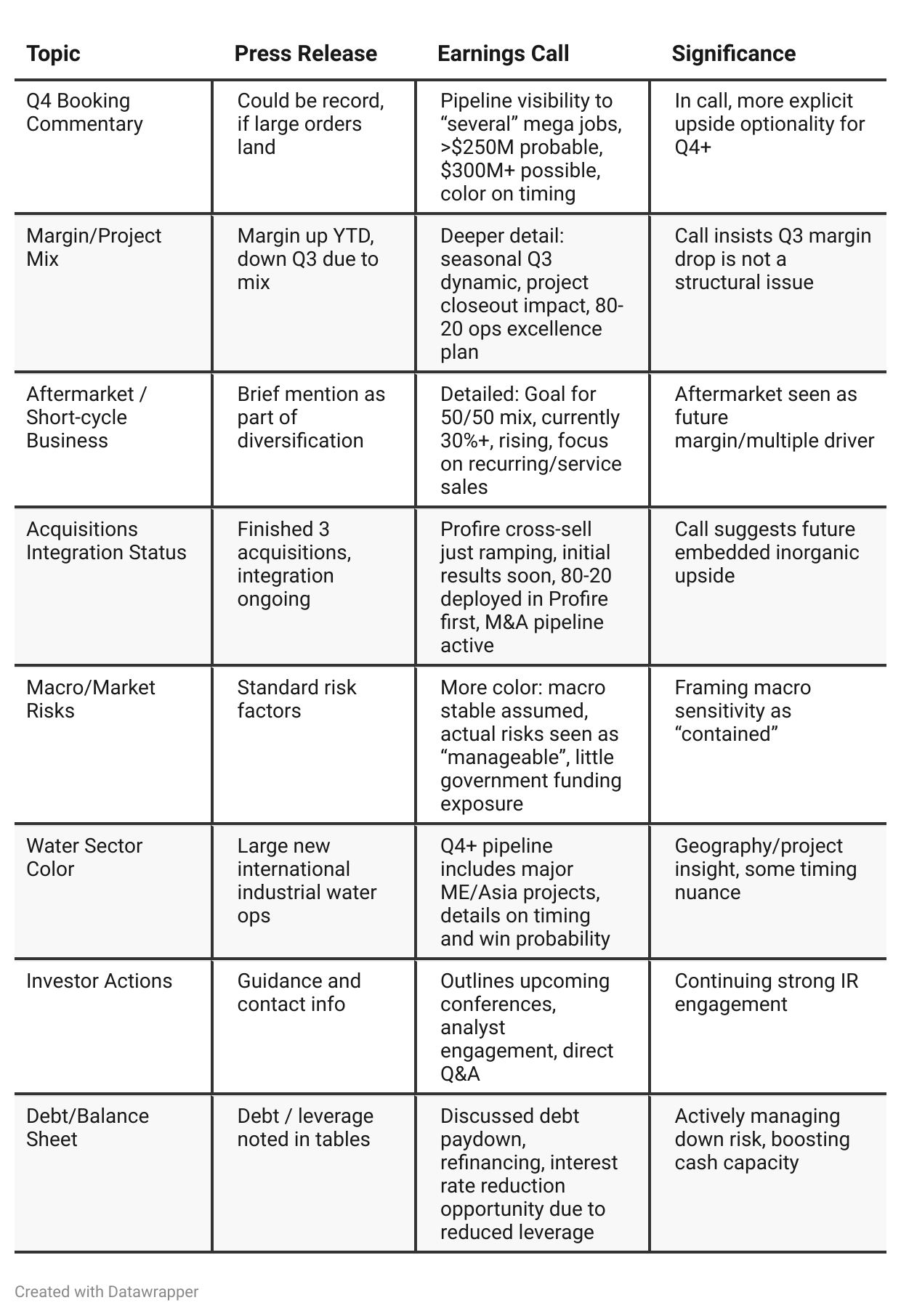

Press Release vs Call Transcript Comparison

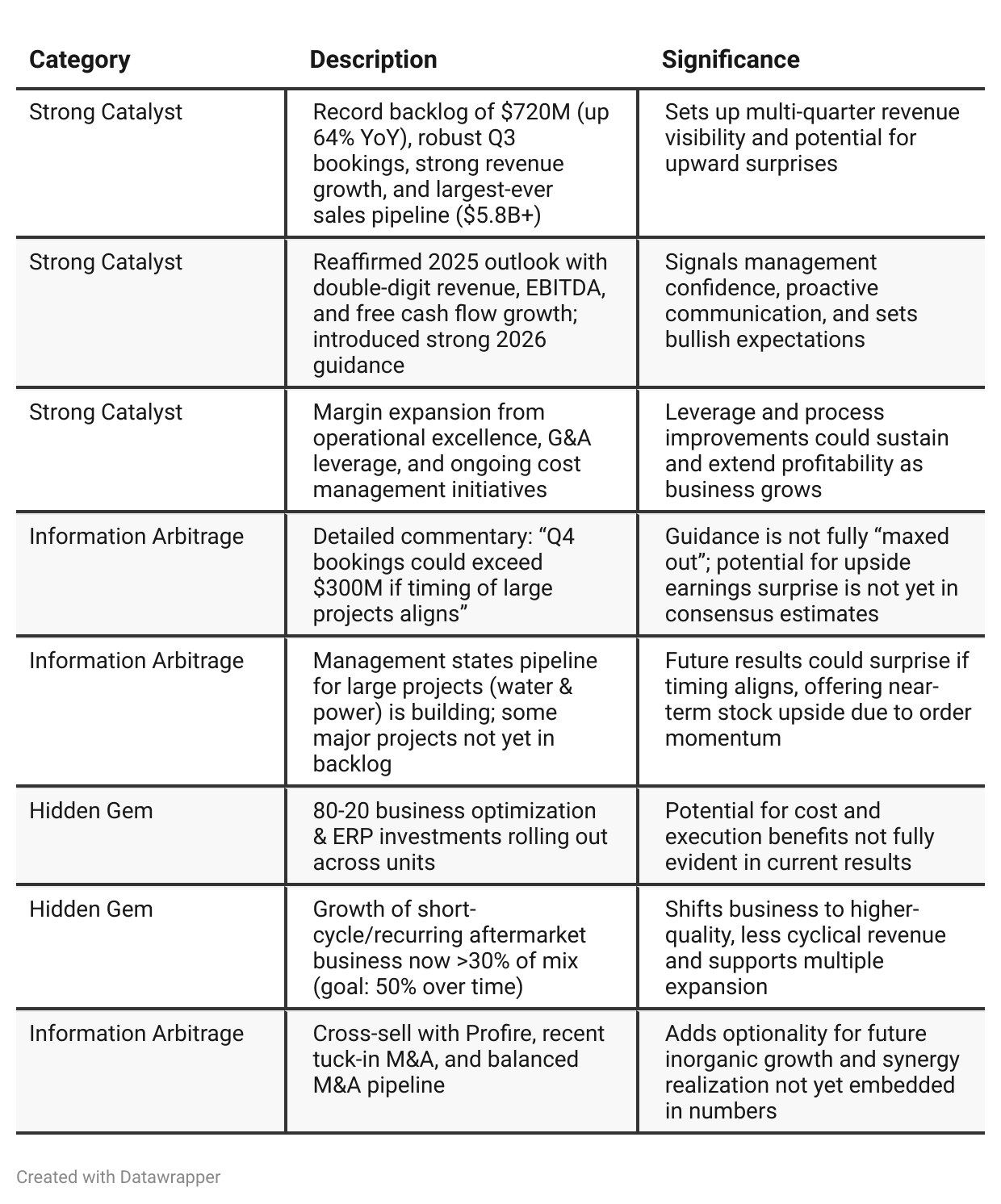

Management’s Q&A reveals strong confidence in outlook, but also repeatedly stresses the inherent lumpiness and “timing” risk with large projects. This helps set expectations—unexpected order timing can swing quarter-to-quarter results.

Ongoing strategic shift toward more aftermarket/recurring revenue reflected in short-cycle growth and targeted mix change; expect more investor focus on this going forward.

Commentary on macro resilience (not consumer-driven, insulated from typical recession headwinds) could support a “resilient” narrative for institutional capital and higher multiples.

Q3 margin issues were proactively explained with numerical attribution (30-50bps on one project) and seasonality context. Shows management transparency.

Cross-selling and integration of Profire, and undisclosed M&A pipeline, is a stated but not-yet-realized upside lever.

Explicit recognition that EBITDA Margins can grow even if gross margins dip, due to cost control and SG&A leverage—important for value investors.

Positive Insights

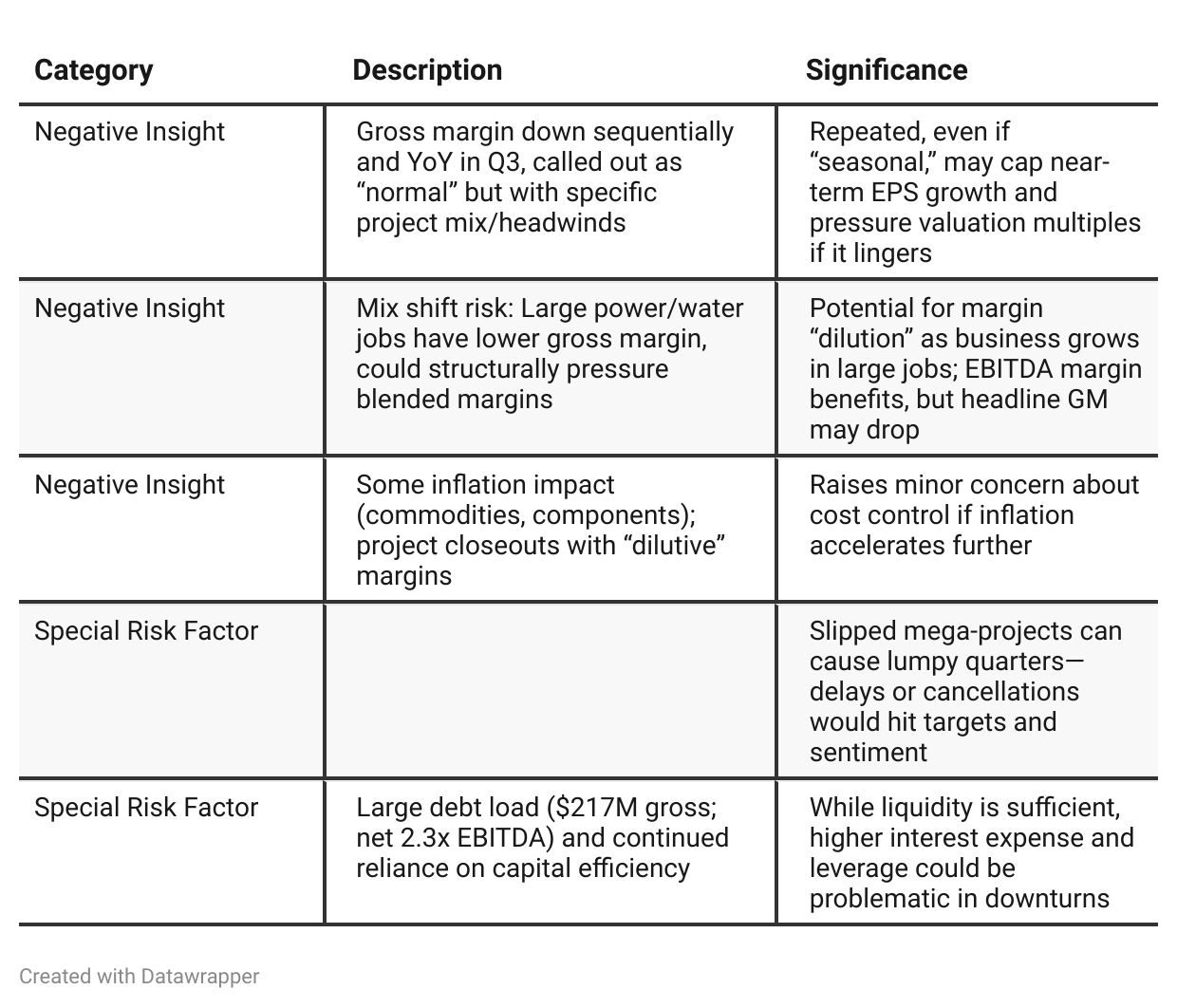

Negative Insights

Tariff Risk

Transcript Mentions:

Management explicitly mentions they “continue to monitor tariffs and the impact on inflation.”

Tariffs and input price inflation on select commodities/components are included in cost models; supply chain adaptations are already in place (mitigating actions like adjusted designs, alternate sourcing).

Tariffs, interest rates, and the US government shutdown are not materially impacting current results. Tariffs are a “headline risk” but not currently affecting big projects in guidance.

No major concern voiced; management describes tariff-related risk as manageable with strong scenario planning.

Mitigation Actions:

Constant supply chain and supplier communication to optimize project pricing and margin levels.

Supply chain described as “stable,” and the company is proactive in scenario planning to address any future tariff escalation.

No mention of shifting production location or renegotiating pricing yet—company is monitoring, not yet reacting materially.

Market Impact:

Company’s global exposure reduces sensitivity to US policy swings; much of the future backlog (especially large industrial water projects) is in regions not subject to the highest trade/tariff risk.

No impact reported on market share or competitive positioning directly due to tariffs.

Conclusion on Tariff Risks:

CECO is aware and watchful, but tariffs are not a material driver (headwind or tailwind) at this stage due to geographic diversity and strong supply chain management.

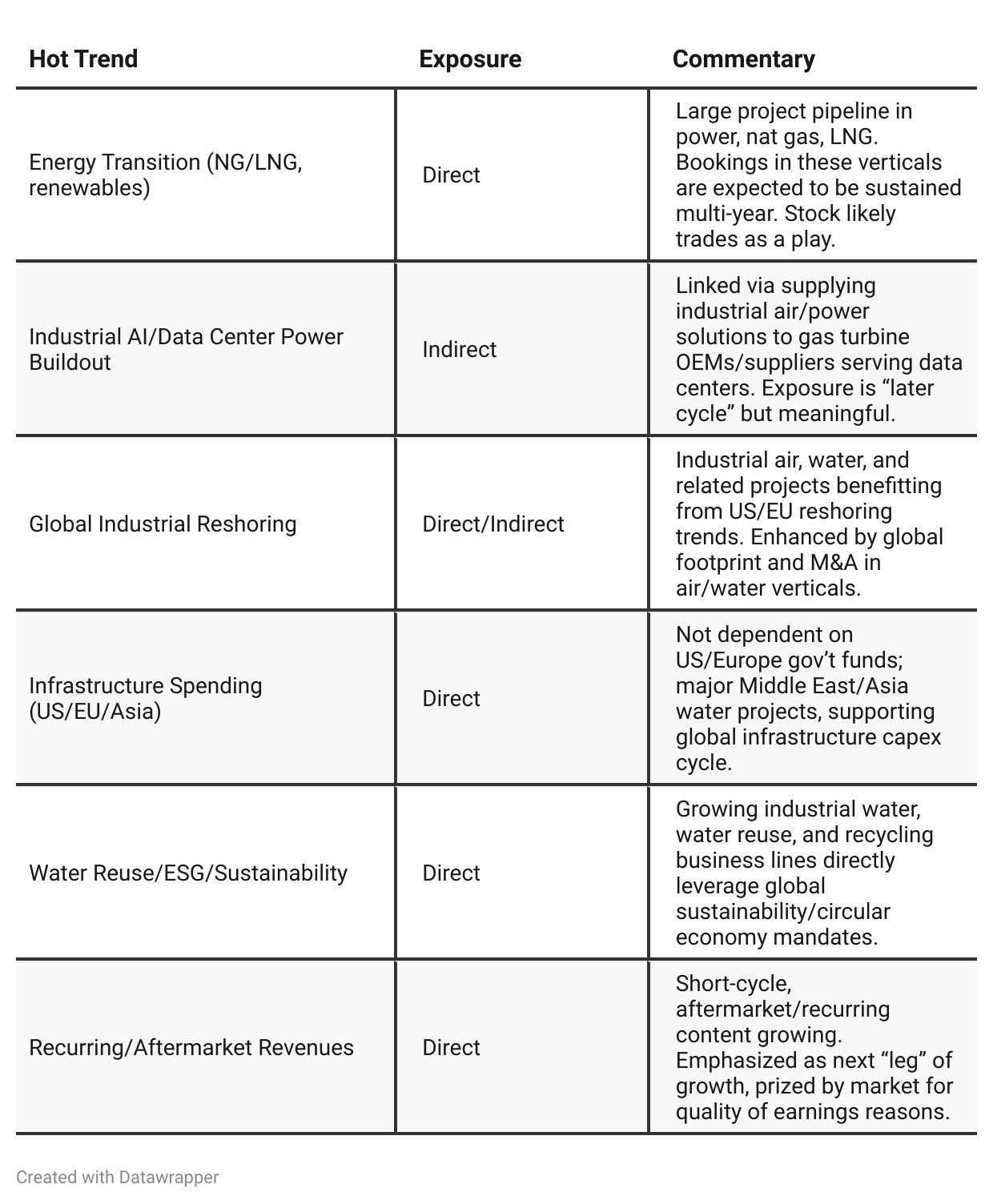

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025: CECO Environmental is riding the crest of a multi-year transformation, delivering record results across revenue, backlog, and orders, powered by disciplined execution, strategic acquisitions, and a broadened market/message that spans power generation, semiconductors, industrial water, and gas infrastructure. Operational excellence and aggressive investment have fueled a new growth phase, moving CECO firmly away from its former status as a low-growth industrial. The company raises guidance, celebrates strong project execution, and expresses confidence in multi-year demand themes and its ability to continue scaling.Q3 2025: Having already exceeded last year’s record sales with a quarter still to go, CECO’s narrative turns from “breakout” to “sustained high performance and readiness for the next plateau.” There’s a measured confidence: the company reaffirms ambitious 2025 targets and—newly—provides early, bullish 2026 guidance. The message also matures: CECO candidly addresses project mix, seasonality, and operational headwinds while pointing to sophisticated responses (like process optimization and the 80-20 program). The outlook is less about proving CECO’s right to grow, and more about managing scale, optimizing capital/liquidity, balancing project size/mix, and preparing for a billion dollar plus revenue run-rate—backed by a robust international and short-cycle business. Scenario planning and risk monitoring are more visible, as is a commitment to “repeatable growth” and outperformance irrespective of short-term macro blips.

Year-over-year comparison

Q3 2024: CECO Environmental was navigating growing pains—record bookings and backlog, but revenue recognition delays due to customer timing. The focus was on overcoming these short-term hiccups, closing and integrating transformational acquisitions, and laying the foundation for an outsized 2025. Management framed setbacks as timing issues, not loss of demand, and emphasized a multi-year transformation toward scale and margin improvement.

Q3 2025: The company has moved from aspiring to sustainable high performance. Record Q3 financials validate years of investment and transformation. Management’s narrative matures: their position as a market leader is secure, their pipeline and backlog give rare visibility, and their guidance process is more transparent, disciplined, and confident. Rather than focusing on repairing or explaining, they now talk about scaling, industrial discipline, operating complexity, and sustaining double-digit growth as a global platform. M&A is presented as optional, not a requirement to meet guidance. Margins and growth are backed up by a robust pipeline and capacity expansion. Macro risks are acknowledged but not central.

Final Takeaway

CECO Environmental is in a strong growth phase, leveraging record backlog, robust sales pipeline, and repeatable double-digit top and bottom line growth. The move toward more recurring revenue and operational efficiency should improve earnings quality and valuation over time. While large-project “lumpiness,” margin mix headwinds, and execution risks exist, the current set-up is compelling. Investors should focus on Q4 booking momentum, margin mix trends, and realization of project pipeline into actual revenue. Verdict: BUY. Upside potential if several mega-projects land and recurring/high-quality earnings continue to rise.