CECO Environmental Corp. (NASDAQ: CECO) – Q2 2025 Earnings

CECO Environmental Corp. (NASDAQ: CECO) – Q2 2025 Earnings

Earnings Release Date: Jul. 29, 2025

Stock Price: $34.71

Market Cap: $1224.7 million

Q2 2025 sales of $185.4 million vs $137.1 million in the prior year

Q2 2025 EPS of $0.24 vs $0.18 in the prior year

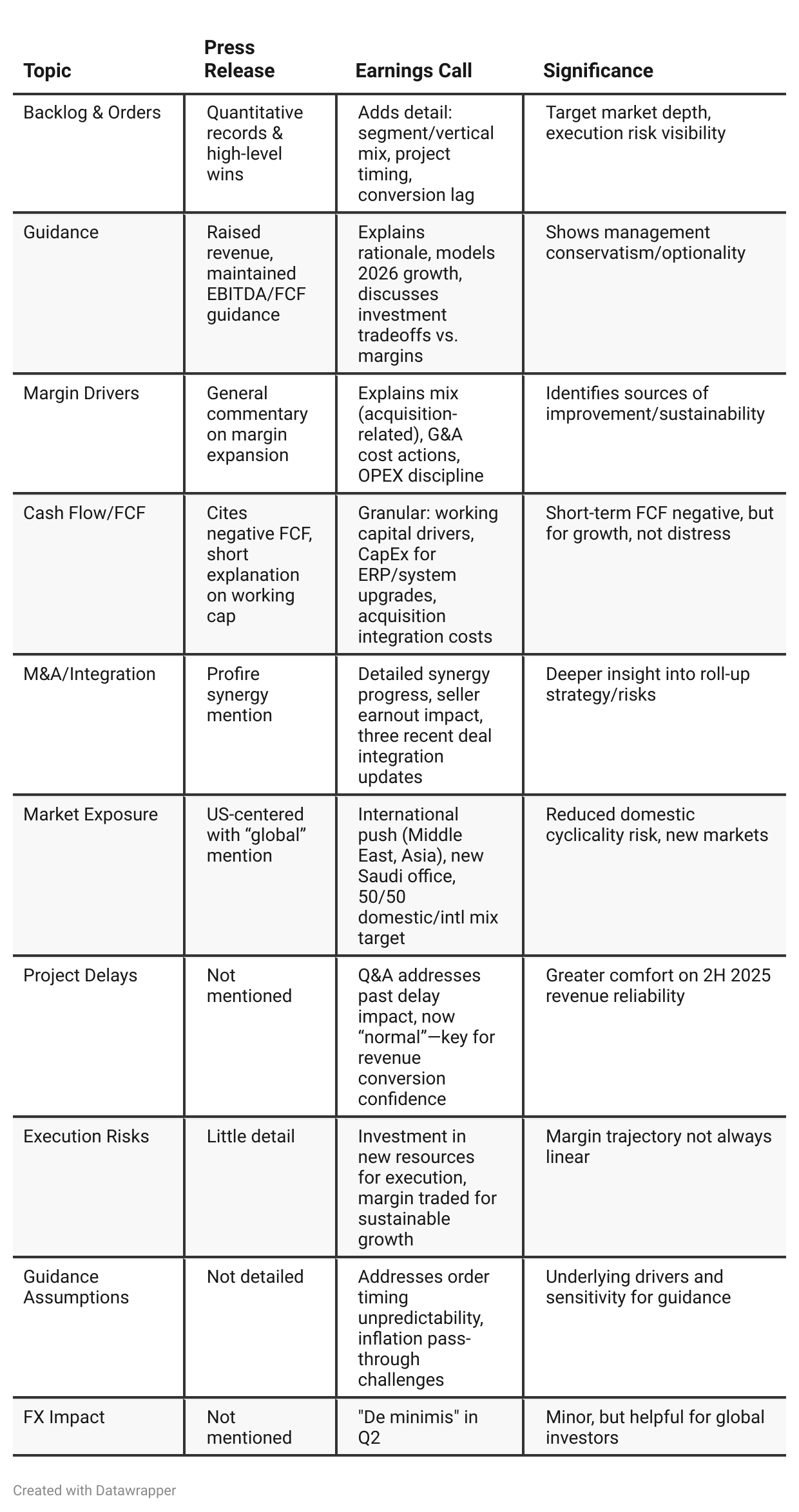

Press Release vs Call Transcript Comparison

Valuation Implication: PR signals momentum and guidance raise, but the EC provides clarity on why the business may trade at a premium—visibility into 2026, active M&A, diversified growth, and proven execution on past synergies.

Growth vs. Margin: Strategic reinvestment means FCF or EBITDA margins may lag, but topline and market share expansion are priorities. This could lead to a higher multiple if topline and backlog growth are sustained.

Execution & Risk Appetite: Management shows willingness to incur higher costs and leverage for access to new markets and order wins, but is also conscious of “cost levers” if the growth cycle cools.

Communication Consistency: Both PR and call signal bullishness, but only the call explains management decision-making, risk management, and the non-linear nature of margin improvement.

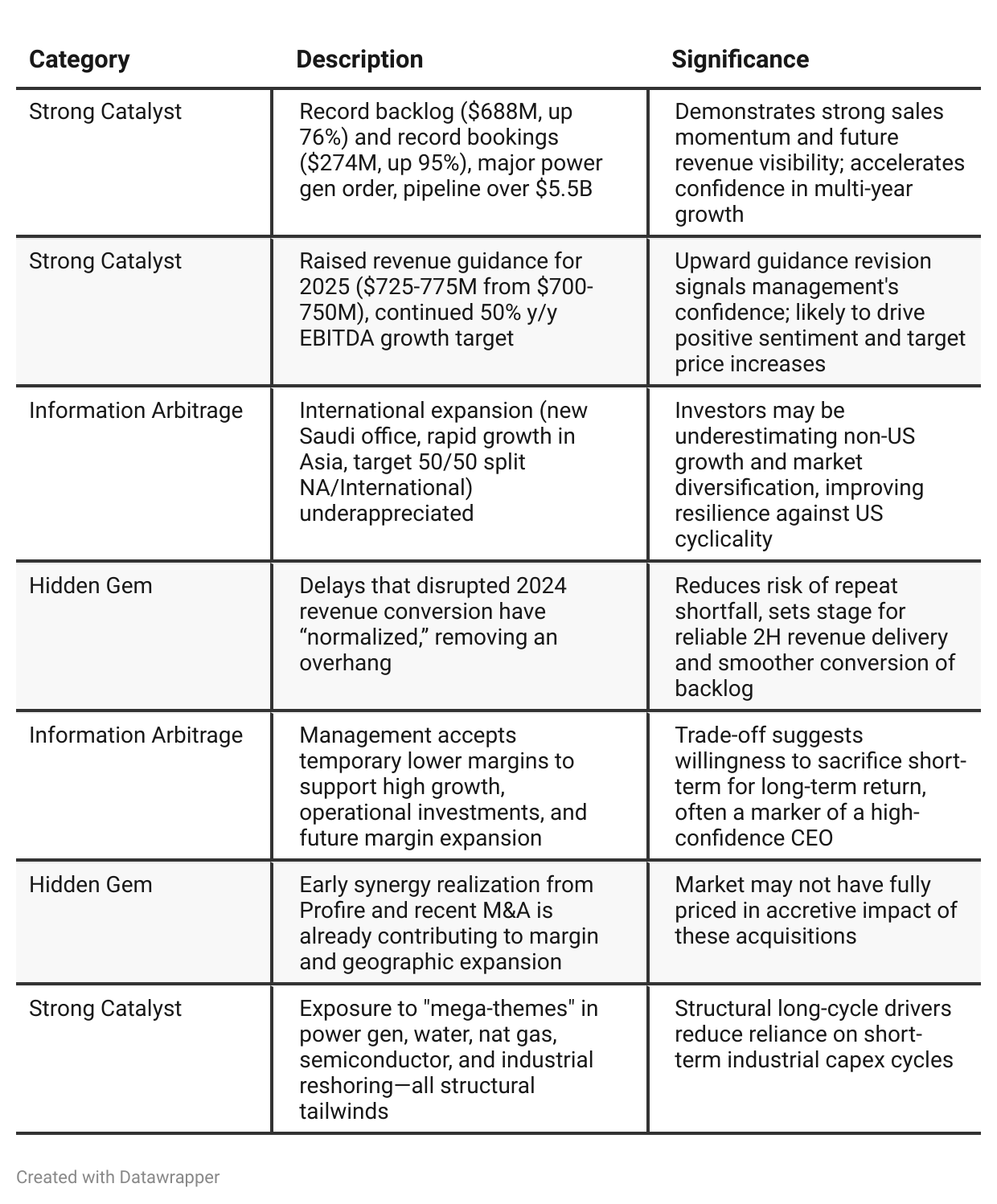

Positive Insights

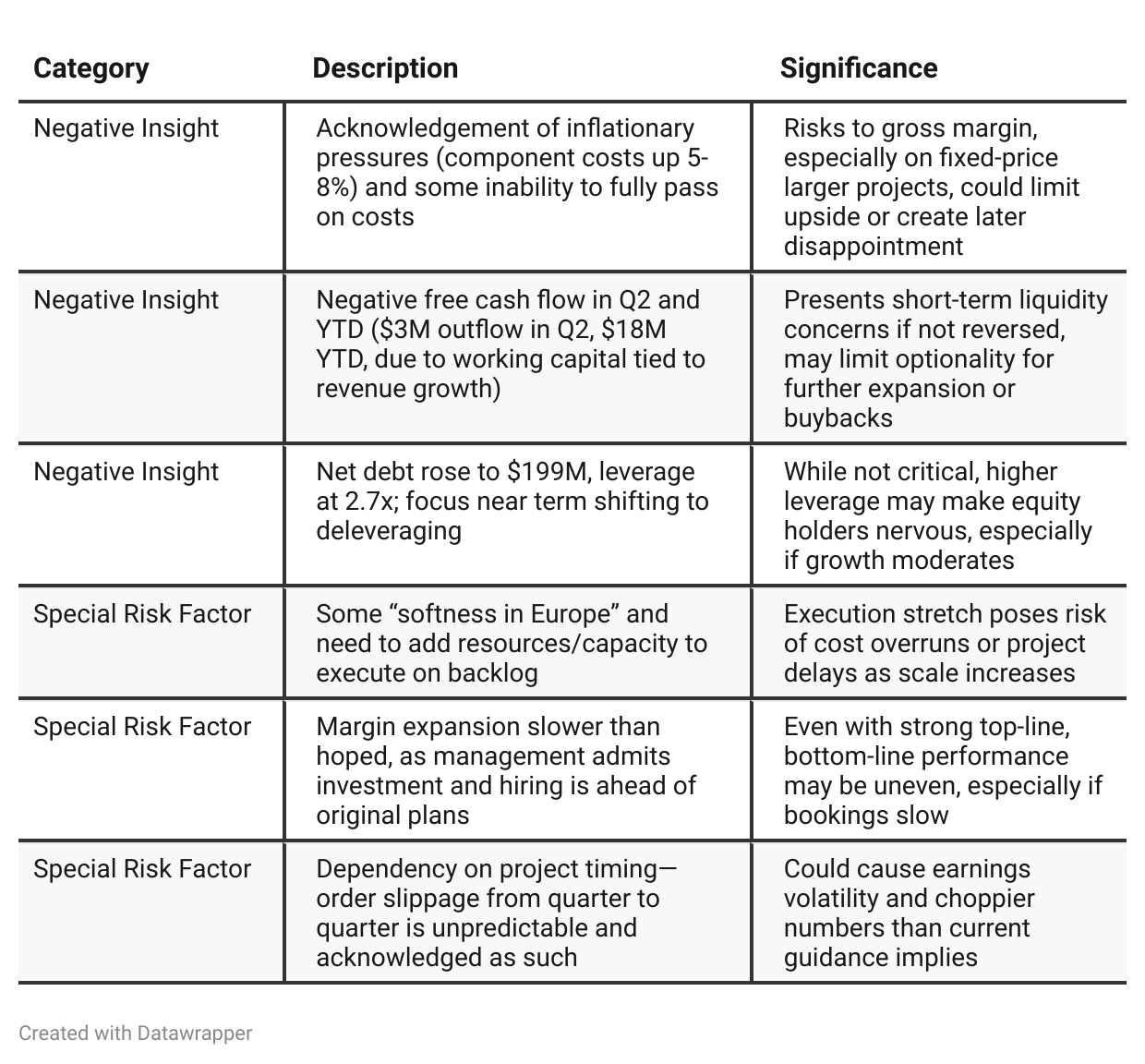

Negative Insights

Tariff Risk

Mentions of U.S. tariffs and trade policies:

Management (Todd Gleason) confirmed their view on tariff impacts is “unchanged” from prior quarters and remains closely monitored.

Tariffs and inflation: Company is seeing input cost increases (5-8% on components), attributing some to broader industrial price pressure, which includes tariff effects.

Pricing power: For large/fixed contracts, they're able to pass on most costs, but not all—so certain cost inflation (tariff-driven or otherwise) will pressure margins.

Mitigation: Focus on sourcing/productivity offset, cost actions, and advance modeling of expected inflation in guidance; increased geographical/vertical diversification also helps hedge tariff-specific exposure.

Mitigation Actions:

Contracts: For fixed-price contracts, CECO generally tries to match fixed pricing with their supply chain, reducing mismatch risk. However, they can't pre-buy or lock in all component prices, so some residual exposure exists.

Pricing: There is some ability to raise prices for customers, but the company acknowledges this is harder on large or long-duration contracts.

Productivity Initiatives: Management stresses ongoing efforts to offset inflation and tariff headwinds through operational productivity gains and cost actions.

Geographic Diversification: Growing international exposure (e.g., the new Saudi office, Asia expansion) is a subtle hedge, reducing dependency on US-centric policy and tariff environments.

Market Share/Innovation:

There is no sign that tariffs are causing CECO to lose market share or fall behind competitively. On the contrary, their international push and product diversity suggest they are adapting well.

Forward-Looking Statements:

Management states their forward inflationary and cost guidance already factors in expected tariff impacts for 2H 2025, and their outlook is “fundamentally unchanged.”

No quantitative estimate of future tariff impact or explicit directional forecast, but clear awareness and proactive modeling.

Sentiment Analysis

The overall sentiment toward CECO is bullish. Investors express enthusiasm about the company’s performance, its record backlog, raised revenue guidance, and share price momentum following strong earnings. Multiple comments emphasize expectations for continued growth, particularly in the power generation market, and a belief that the stock will continue to trend higher. Occasional mentions of chart patterns or waiting for pullbacks are present, but the predominant tone is positive and focused on upward potential, with few mentions of bearish scenarios. This strong positivity supports a bullish classification.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

In Q1 2025, CECO told a story of sturdy, resilient growth in the face of significant external uncertainty—navigating global tariffs, inflation, and integration of new acquisitions with cautious optimism. The company highlighted its defensive strengths (diverse portfolio, contractual protections against tariffs, flexible cost structure), while making the case that secular growth drivers and a swelling sales pipeline underpin their outlook. Much of the Q1 message is about prudent management and dealing with “noise” while keeping guidance steady.By Q2 2025, the tone and narrative have shifted markedly towards ambition and offense. CECO is coming off a record-breaking quarter, raising revenue and backlog guidance, and openly discussing the early innings of multi-year, double-digit growth. Project execution risks from late 2024 have been resolved, and management describes a more normalized and confident conversion of backlog to revenue. The story pivots to international expansion, mega-theme demand (data centers, AI, water, global industrialization), and the company’s readiness (through resource ramp-up and operational changes) to scale rapidly. The concerns of Q1 now seem well managed, and the company’s narrative is increasingly about capturing upside and establishing long-term leadership.

Year-over-year comparison

Q2 2024 CECO presented as a company in strong operational shape, laser-focused on margin expansion and backlog conversion, but facing “lumpiness” in bookings due to customer-side delays and a longer order cycle for large projects. Management was cautiously optimistic, repeatedly referencing a robust sales pipeline and mega-themes as enduring drivers, yet messaging was somewhat tempered by macro and project timing uncertainty.

Q2 2025 The narrative evolves decisively from defensive confidence to offensive growth. CECO shifts the story to celebrating records in every key metric (bookings, backlog, revenue, margin), with resolved delays and a highly visible multi-year growth runway. International expansion is more prominent, and management is candid about trading some near-term margin for future positioning. The company’s messaging is firmly focused on scaling execution to meet overwhelming demand, supporting elevated guidance and long-term ambitions (hinting at a $1 billion+ revenue company).

Final Takeaway

CECO Environmental is in a high-growth phase, riding secular demand in power, water, industrial energy, and environmental solutions. Major backlog and bookings, expanding end markets, and new international reach set the stage for durable multi-year revenue growth. Risks around rising costs, working capital needs, leverage, and execution reflect an aggressive growth path but are so far managed with transparency and discipline. Conversion of backlog to free cash flow and maintenance of margin will be most critical. Verdict: Buy, with continued monitoring of execution and cash discipline.