Bel Fuse Inc. (NASDAQ: BELFA) – Q3 2025 Earnings

Bel Fuse Inc. (NASDAQ: BELFA) – Q3 2025 Earnings

Earnings Release Date: Oct. 29, 2025

Stock Price: $139.00

Market Cap: $293.9 million

Q3 2025 sales of $179.0 million vs $123.6 million in the prior year

Q3 2025 EPS of $1.77 vs $0.61 in the prior year

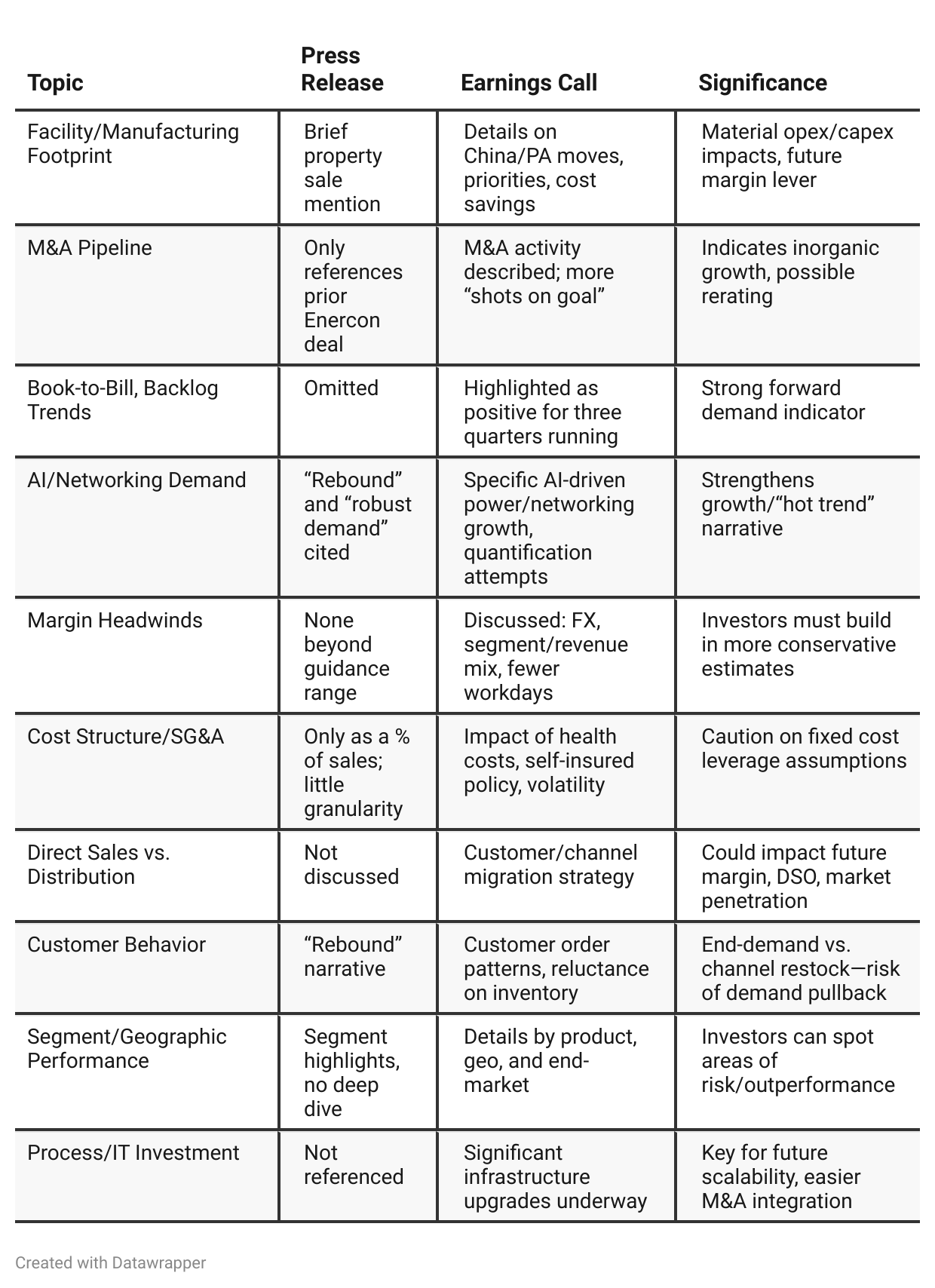

Press Release vs Call Transcript Comparison

Reported vs. Underlying Strength: While headline numbers are impressive, much of the margin expansion is attributed to volume leverage and restructuring—a dynamic that may not persist. Management says as much on the call.

Quality of Revenue: Power and Connectivity segments are the main growth engines, with partial AI tailwind, but Magnetics is rebounding at lower margins, dragging group margin if mix shifts.

Cash Flows and Leverage: Repaying debt rapidly, balance sheet flexibility for M&A, but capex and dividend outflows bear watching.

Valuation Multiples: New non-GAAP definitions potentially help paint a rosier operational picture for “growth/multiple expansion” investors, but require scrutiny.

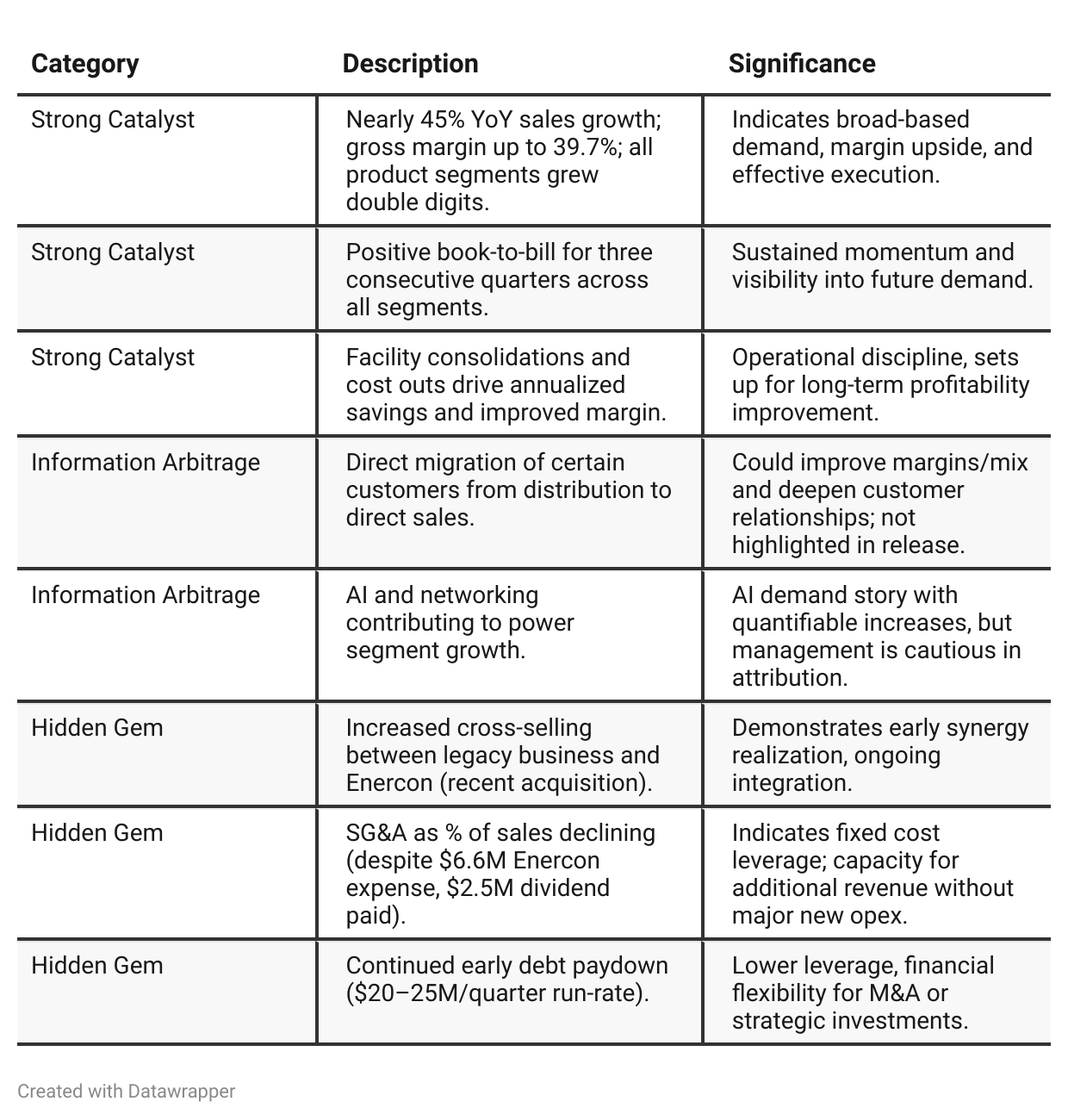

Positive Insights

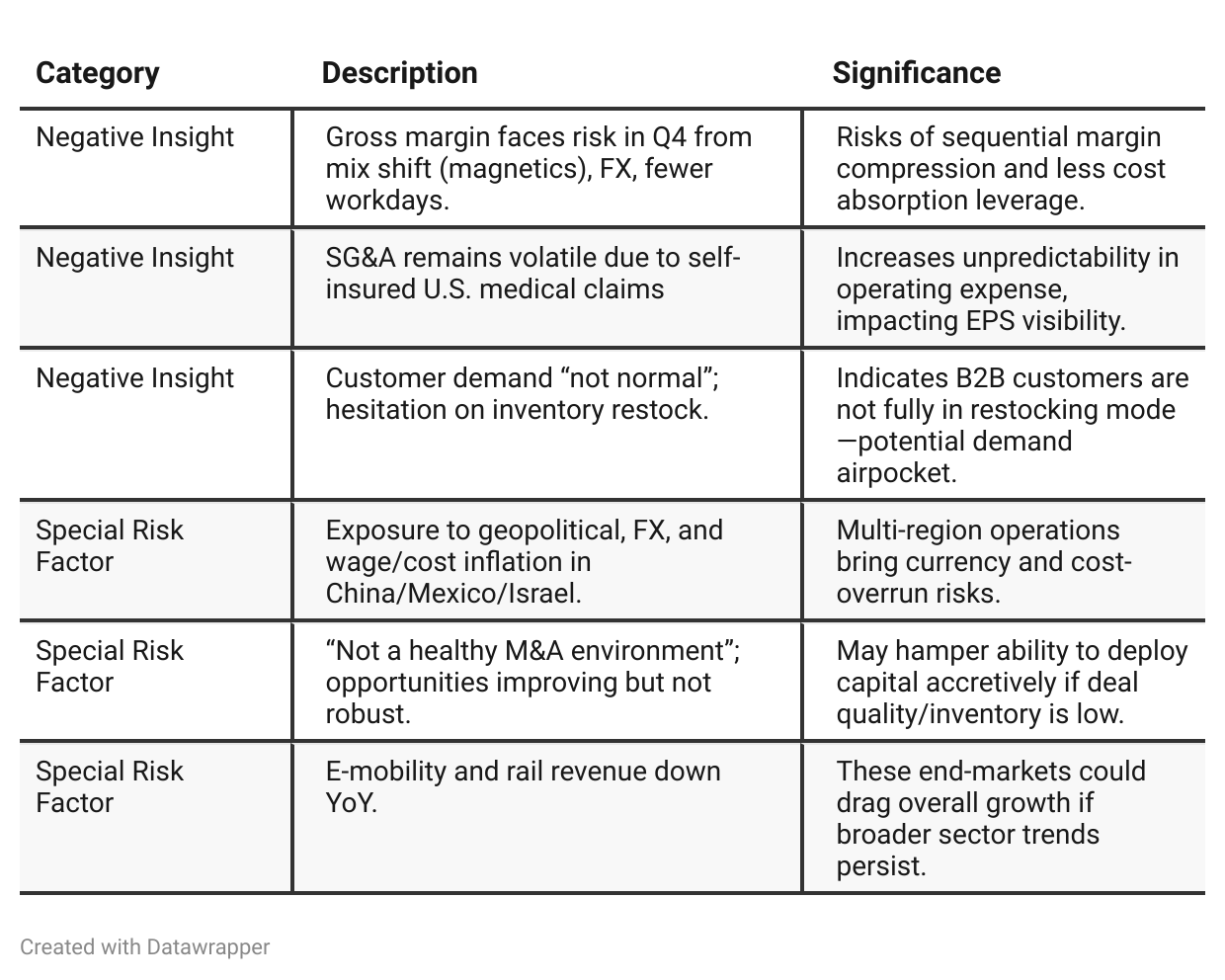

Negative Insights

Tariff Risk

Mentions/Analysis:

The transcript does not contain detailed or explicit discussion of the impact of U.S. tariffs, trade restrictions, or related supply chain disruptions.

Supply Chain and Footprint: The company is actively consolidating manufacturing in China and considering outsourcing for better cost. This could be partially interpreted as a way to mitigate risk exposure to China-specific tariffs or future unpredictable trade policy, but this was not directly referenced.

Forward-Looking Statements: References to macro/geopolitical/unpredictable “externalities” (including some from China, Israel, Mexico) hint at broad sensitivity but are not explicitly tied to tariffs.

No Clear Mitigation: No specific mention of shifting supply chains, renegotiating customer/supplier contracts, or pricing actions due to tariff impacts.

Conclusion: While general geopolitical and supply-chain risks are acknowledged, the company did not address U.S. tariffs/trade policy or mitigation strategies in meaningful detail. Investors should monitor future disclosures and conference call Q&A for more on this evolving risk.

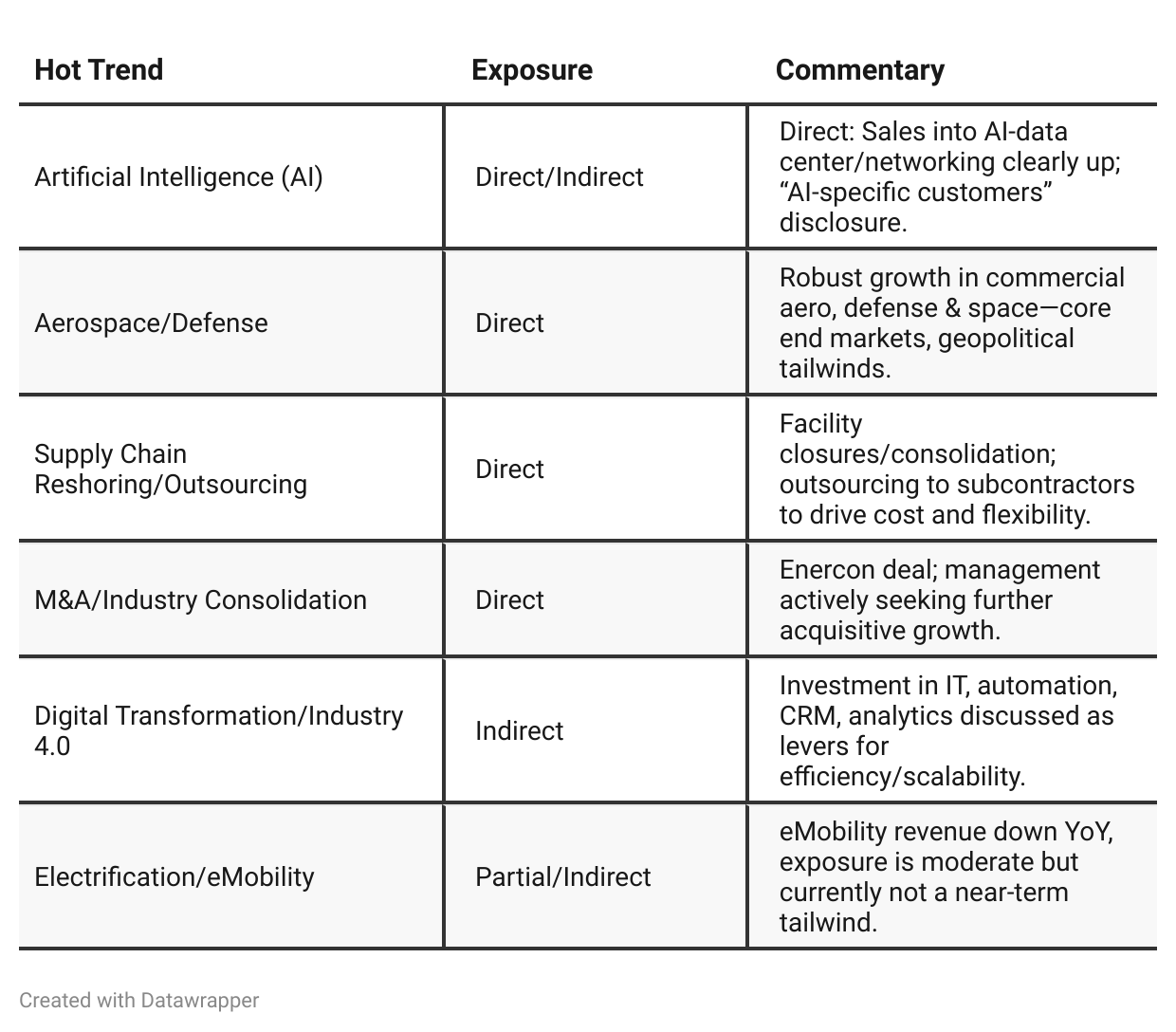

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025: Bel Fuse was in a robust recovery phase, with performance exceeding internal expectations thanks to inventory normalization, strong order flow (especially in networking/power), and operational focus. Management exercised caution around macro risks (tariffs, FX) and highlighted sustainable incremental margin improvements via efficiency, but flagged risks around end-market cyclicality, pricing, and non-recurring margin boosts. Enercon was contributing as expected, with integration on track but no near-term revenue synergies forecast.Q3 2025: The company’s story has become more forward-leaning, transformation-driven, and ambitious. With three consecutive quarters of positive book-to-bill and all core end markets/revenue lines posting double-digit growth, management has pivoted from recovery to scaling for sustained, strategic growth. A new emphasis is placed on transforming go-to-market strategy—shifting from a product to a customer/end-market orientation—along with heavy investment in IT and process standardization to enable scalability and M&A integration. Facility consolidation and selective outsourcing, particularly in China, are now tangible sources of cost leverage. Risks remain (margin mix, FX, customer hesitancy), but the message is one of scaling up for a multi-year growth journey, not just stabilizing post-recovery.

Year-over-year comparison

Q3 2024: Bel Fuse was in a stabilization phase, turning the corner from a year of sales contraction, supplier and inventory challenges, and operational restructuring. Management was committed to cost discipline, careful capital allocation, and fixing the company’s “base” before pursuing new growth. Early “green shoots” in bookings and recovery were emerging, and optimism was beginning to return, but guidance remained prudent. The Enercon acquisition was framed as a coming catalyst, not yet a realized driver.

Q3 2025: Bel Fuse has graduated into a scalable growth and transformation phase. The narrative is now about proactive change: shifting the go-to-market strategy, leaning into automation and digital modernization, and scaling up for growth—both organically and through further acquisitions. Every segment is in growth mode, broad-based margin gains are being realized, and management’s focus is on how to maintain and integrate these gains. Risks are now operational (how to manage growth, how to allocate margin flexibility, how to integrate further M&A) rather than existential. There is a new level of optimism in the company’s strategic intent and delivery, with clear pride in progress and purposeful planning for the future.

Final Takeaway

Bel Fuse Inc. is in a late-stage restructuring and operational leverage phase, pivoting toward a growth-oriented, customer-focused model. The company is capitalizing on secular demand in AI, aerospace/defense, and networking, while actively managing cost structure and facility footprint. Margin performance has been strong, with early returns from M&A and cross-segment synergy. While gross margin and expense headwinds may temper sequential results, the operating backdrop remains highly constructive. Execution on margin guidance, successful integration of Enercon, and demand stability will be critical for sustained outperformance. Verdict: Buy, with a potential re-rating if Q4 trends materialize as management anticipates.