Bel Fuse Inc. (NASDAQ: BELFA) – Q2 2025 Earnings

Bel Fuse Inc. (NASDAQ: BELFA) – Q2 2025 Earnings

Earnings Release Date: Jul. 24, 2025

Stock Price: $34.71

Market Cap: $1224.7 million

Q2 2025 sales of $168.3 million vs $133.2 million in the prior year

Q2 2025 EPS of $1.58 vs $1.46 in the prior year

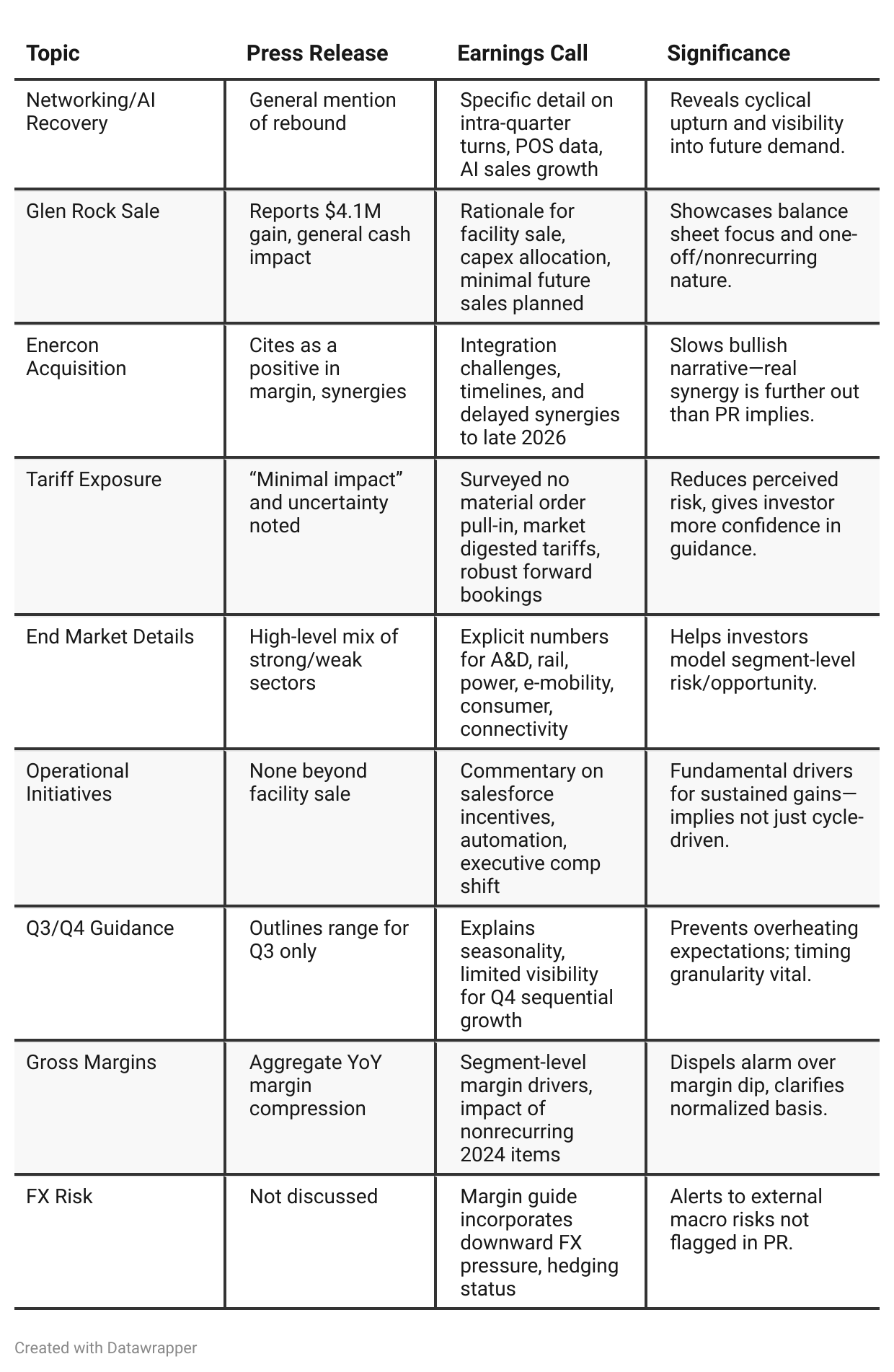

Press Release vs Call Transcript Comparison

Depth on Capital Allocation: The call addressed debt paydown from asset sale and enhanced cash flow, which indicates management’s commitment to financial discipline.

Customer/Supplier Rebuild: Update on Chinese supplier losses and successful alt-sourcing/recovery efforts (detailed in call, not PR) increase confidence in operational adaptability.

Pricing Environment: The call addresses absence of widespread price erosion—which matters for margin modeling in light of inflation and competitor actions.

Segment Margin Structure: The call contextualizes segmental margin declines with specific nonrecurring items in 2024—a vital nuance for accurate forward margin estimates.

Risk Discipline: Management is explicit on their cautious approach to margin expansion and OpEx investments, emphasizing long-term returns over aggressive short-term gains.

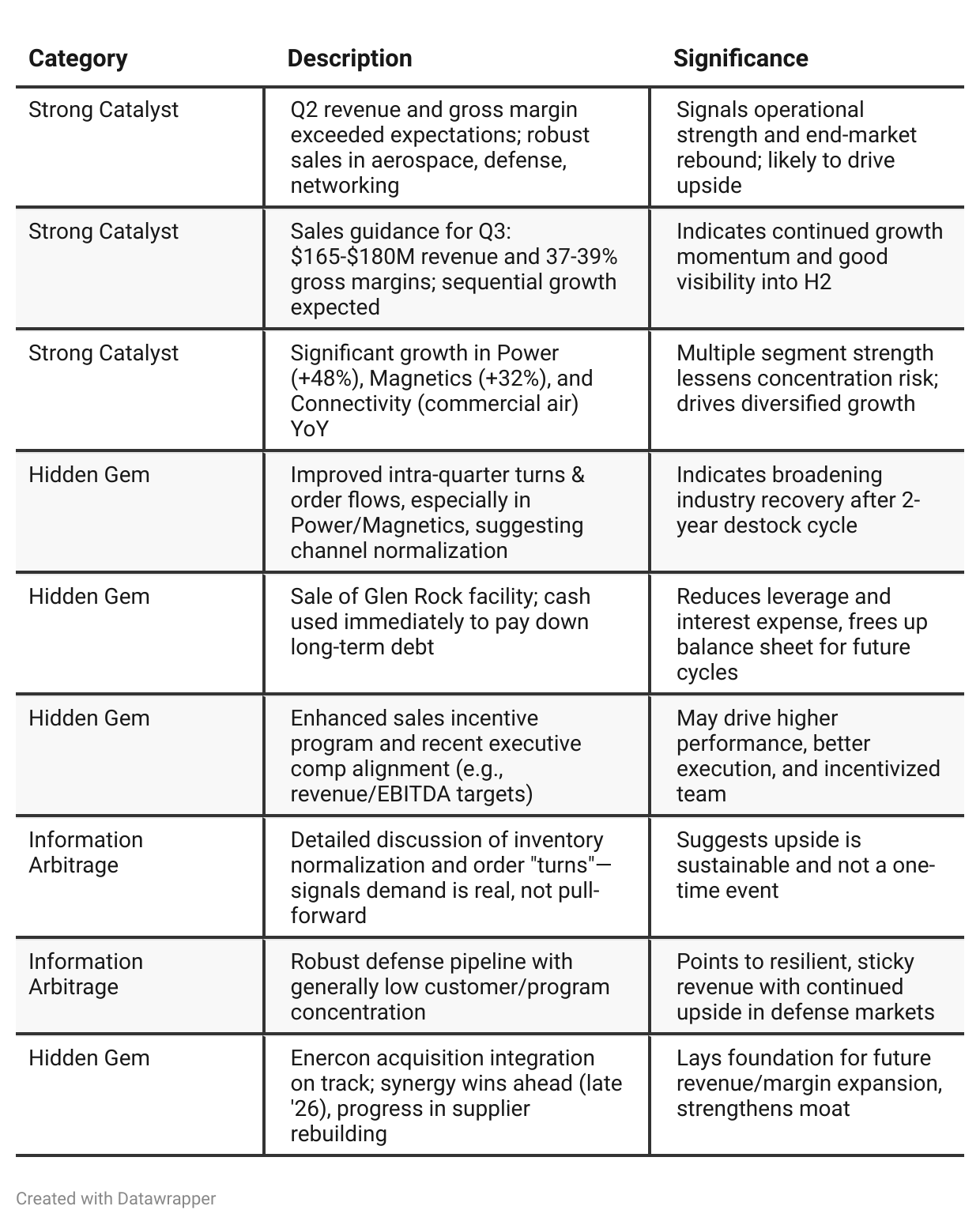

Positive Insights

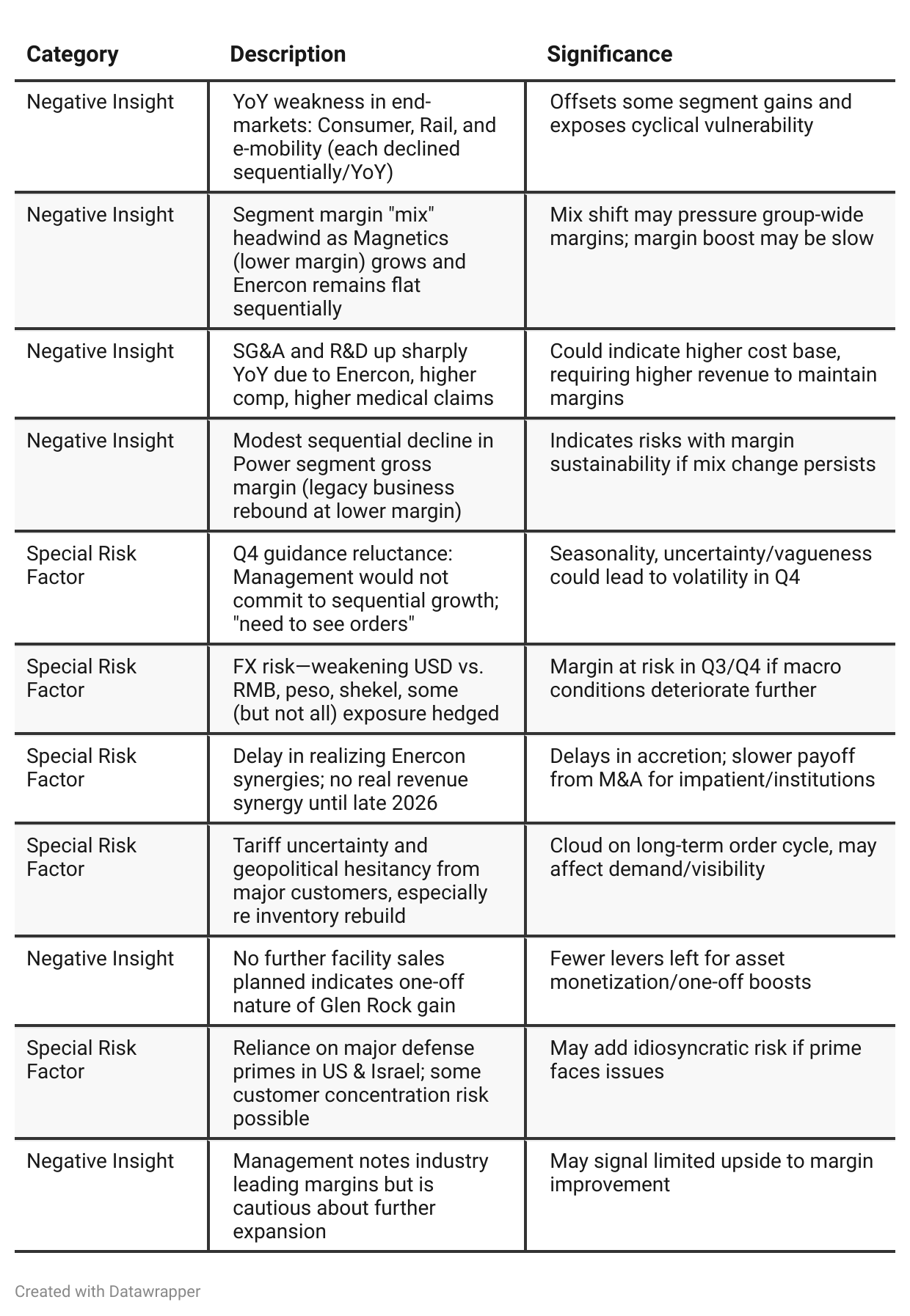

Negative Insights

Tariff Risk

Tariffs were a central topic in the call, with management clarifying that Q2 impact was minimal ($2M of low-margin sales), and there was no evidence of widespread order pull-ins to front-run tariffs; this was confirmed by a global customer service survey. Bookings remain robust into July, indicating continued demand "beyond" any deadline motivation.

Management notes ongoing uncertainty but asserts the market seems to have largely digested the latest tariff structure. Efforts to mitigate risks include:

Ongoing adaptation of supply chains alongside suppliers and customers,

Highlighted customer caution/hesitancy on inventory rebuilds,

Active monitoring and readiness to adjust operationally to future tariff or geopolitical shifts.

No explicit mention of margin repositioning, contract renegotiation, or facility moves in response to tariffs.

Sentiment Analysis

The overall sentiment is bullish. Investors are highlighting Bel Fuse’s strong Q2 results, robust growth in key end markets like defense and aerospace, successful integration of acquisitions, prudent capital management (including debt reduction), competitive advantages, and resilient backlog. Positive forward-looking commentary, mentions of undervaluation, and optimism regarding the company’s supply chain optimization and technological leadership outweigh any neutral or factual mentions, supporting a constructive outlook on the stock's future performance.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

In Q1 2025, Bel Fuse’s story was one of resilience and cautious optimism in the face of elevated external uncertainty—a CEO transition, looming tariff risks, and channels still working through excess inventory. Management addressed these headwinds by emphasizing diversification, nimble operations (especially in supply chain/location), and formative changes in sales and incentive strategy. However, messaging was “wait and see”; the company was positioned defensively and focused on building flexibility and preserving financial strength.By Q2 2025, the story had pivoted to one of renewed confidence and operational momentum. The much-feared tariff shocks emerged as minor, inventory overhangs were finally clearing, and core end-markets (networking, defense, commercial air) were rebounding meaningfully. Management’s tone turned assertive, highlighting tangible sequential growth, robust bookings, and upside visibility. The new CEO and team brought a clear, performance-driven attitude, stating the company is now reaping benefits from groundwork laid over prior quarters in incentive systems, sourcing, and customer pipeline management. While risks persist (FX, mix, some lingering segment softness), the narrative is one of momentum building after a period of prudent preparation, with focus shifting from resilience to execution and growth.

Year-over-year comparison

Q2 2024: Bel Fuse presented a story of coping with adversity: navigating inventory destocking, confronting supplier & trade headwinds, and working through operational restructuring. The mood was cautious, focused on weathering a “reset year,” controlling costs, and laying groundwork for eventual recovery. Investors were told to expect more of the same into Q3, but that the company’s structure was improving and that end-markets such as AI, A&D, and space were seeds for future growth.

Q2 2025: The narrative has shifted decisively. Bel Fuse is now in rebound. Early strategic actions are yielding fruit: destocking is behind, bookings and revenue are growing sequentially, core end-markets are contributing robustly, and operational improvements (from cost management to incentives) are visible in results. What was once caution over tariffs is now replaced with confidence in the company’s ability to manage through external risks. The focus is on broad-based execution, prudent margin/cost discipline, clear communication around mix and synergy timing, and continued opportunistic growth. The tone is energized and forward-looking, stressing momentum and renewed optimism for the second half and beyond.

Final Takeaway

Bel Fuse is in a recovery and operational optimization phase, building momentum in aerospace, defense, and networking as inventory normalization unfolds. While segment growth and cost discipline support upside, risks include FX volatility, delayed synergy realization, and continued weakness in some cyclical markets. Execution on margin mix, tariff navigation, and successful Enercon integration will be key. Verdict: HOLD—with upside potential if growth broadens and risks abate.