Zynex, Inc. (NASDAQ: ZYXI) – Q2 2025 Earnings

Zynex, Inc. (NASDAQ: ZYXI) – Q2 2025 Earnings

Earnings Release Date: Jul. 31, 2025

Stock Price: $2.49

Market Cap: $75.3 million

Q2 2025 sales of $22.3 million vs $49.9 million in the prior year

Q2 2025 EPS of ($0.66) vs $0.04 in the prior year

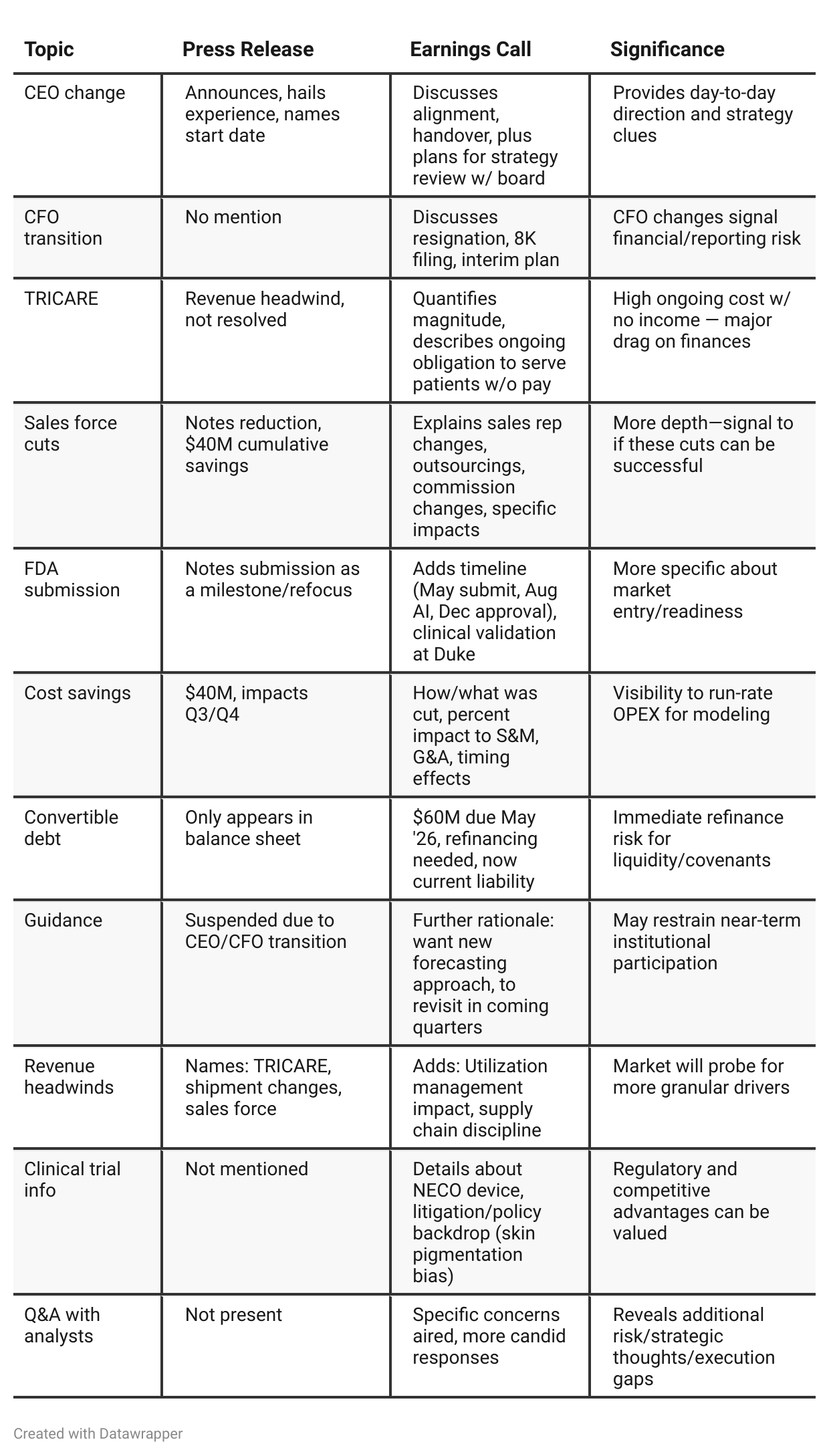

Press Release vs Call Transcript Comparison

Analyst Q&A provides unvarnished risk/opportunity: Only the call transcript surfaces analyst doubts about TRICARE, about the depth of revenue miss (beyond TRICARE), and pressure on resource allocation when not being paid by a significant payer.

FDA process risk discussed with more candor: Management expresses uncertainty about possible FDA second round, reveals confidence but also the regulatory unknowns.

Cash flow commentary more complete on the call: Investors get a sense the cash burn is stabilizing, but not cured—press release only gives hard numbers.

Competitor and market readthrough: Only the call mentions lawsuits and policy changes relating to pulse oximetry, which may mean faster market adoption for NECO if approved.

Sales strategy fine points: The call details performance tiers, the plan to staff all 800 territories, and tweaks to sales comp, whereas the press release lumps all under “efficiency initiatives.”

Guidance rationale explicitness: Calling out that they’re suspending guidance not just due to leadership churn, but because they want to rethink all forecasting, signals possible business model or market volatility ahead.

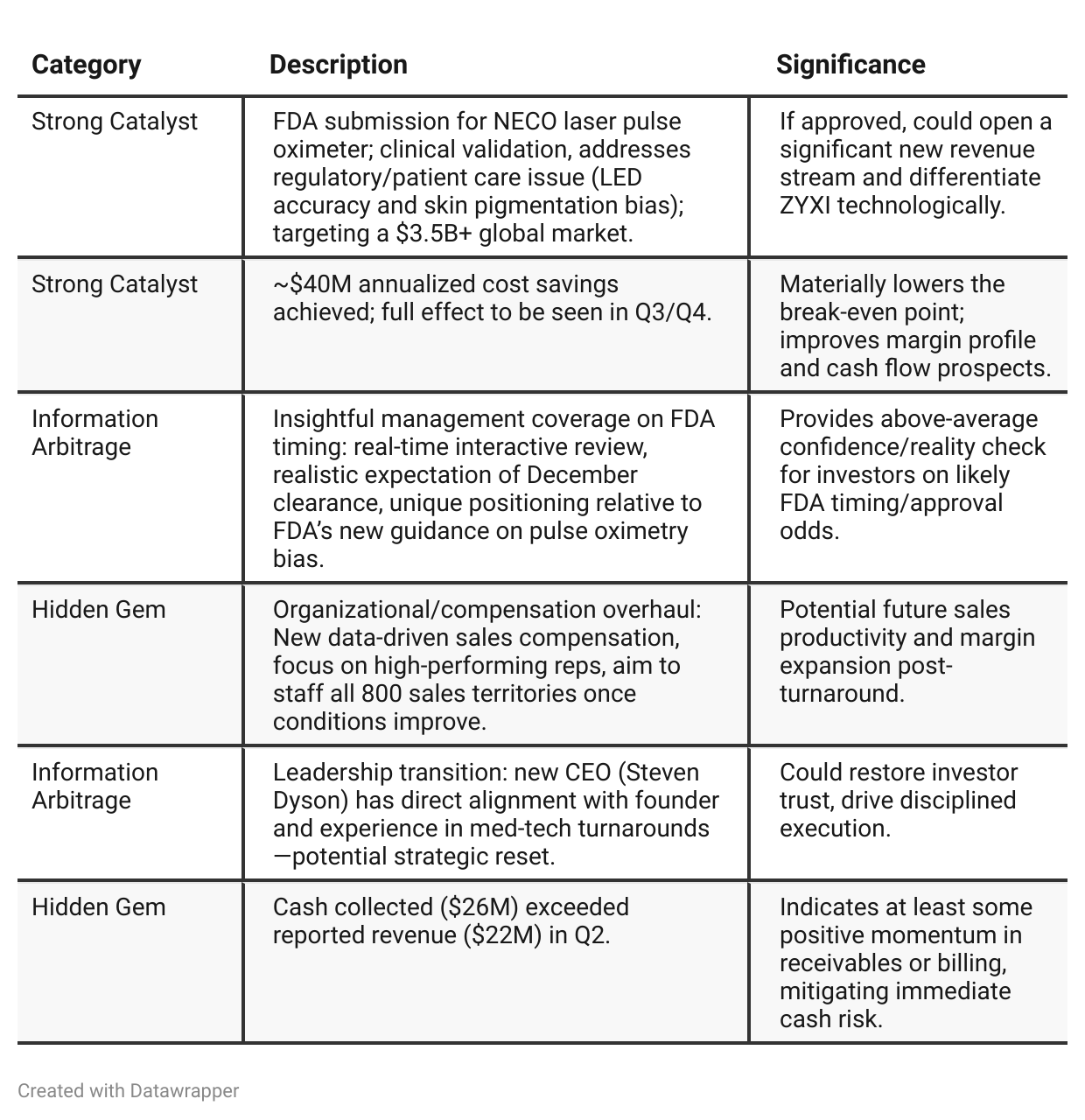

Positive Insights

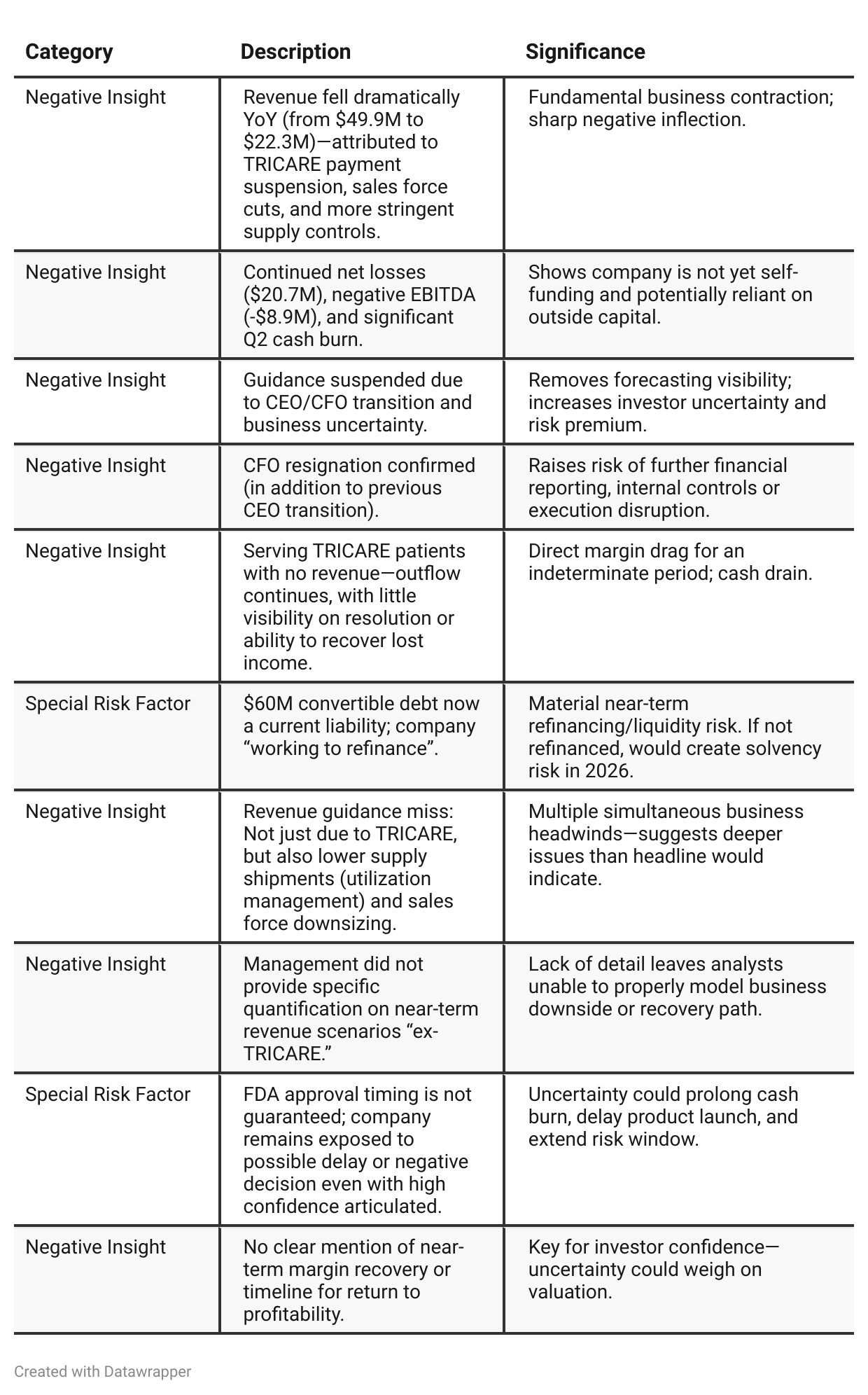

Negative Insights

Tariff Risk

Mentions of U.S. tariffs, trade policies, or related risks:

There are no references to tariffs, U.S. trade policy, or related supply chain/geopolitical risks discussed anywhere in the transcript.

There is no information on import duties, potential impact from tariffs on cost of goods sold, or any mitigation strategies (production shifts, contract renegotiation, etc).

There are also no forward-looking statements regarding the possible effects of tariffs on future earnings or competitive position.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025 Story: “We’ve hit a major reimbursement hiccup with TRICARE, but are working hard for reinstatement while managing costs. Our technology (NECO) is almost ready for FDA submission and, if approved, could fuel the next growth wave. We are right-sizing but optimistic a return to growth is straight ahead.”Q2 2025 Story: “TRICARE risk persists and is now being treated as an indefinite loss. The balance sheet and profit/loss have deteriorated more than hoped. We are aggressively cutting costs, overhauling operations, and reducing reliance on vulnerable payer streams. Hope now lies in cost discipline, a new CEO, restructuring, and the possibility of NECO FDA approval. Guidance is suspended—we need to prove we can stabilize before looking for recovery. Once NECO is approved and new leadership settles, we may have a foundation for renewed growth.”

Year-over-year comparison

Q2 2024: Zynex positions itself as a growth story—profitably expanding its product lines, increasing order volumes, and looking to leverage robust internal resources to drive both current profitability and future innovation. NECO is highlighted as a near-future revenue driver, and management maintains discipline around rep productivity and operational improvement. The mood is balanced with both realism (minor recalibration) and confidence (active share buybacks).

Q2 2025: One year later, the narrative is fundamentally changed. Record growth gives way to crisis management after a payer (TRICARE) suspends payments, leading to a massive revenue collapse and operational rethink. The company is forced to abandon guidance, restructure its workforce, and focus on cash survival. Hope shifts from ongoing business momentum to future catalysts—namely approval and commercialization of NECO and incoming turnaround leadership. Shareholder returns and flexibility are replaced by warnings of caution and an urgent need for execution on all fronts.

Final Takeaway

Zynex (ZYXI) is in a restructuring phase, facing severe revenue headwinds from TRICARE payment suspension, operational resets, and leadership transition. While NECO’s FDA submission and material cost savings are legitimate potential catalysts, high execution risk, cash burn, unclear timelines on critical revenue restoration, and financing risk dominate the near-term outlook. Monitoring FDA progress, debt refinancing, and real revenue/margin stabilization will be essential for any future shift towards a bullish stance. Verdict: Hold, with possible downside if execution and external conditions do not improve.