Zoomd Technologies Ltd. (OTCPK: ZMDTF) – Q2 2025 Earnings

Zoomd Technologies Ltd. (OTCPK: ZMDTF) – Q2 2025 Earnings

Earnings Release Date: Aug. 14, 2025

Stock Price: $1.45

Market Cap: $149.3 million

Q2 2025 sales of $19.6 million vs $14.0 million in the prior year

Q2 2025 EPS of $0.05 vs $0.02 in the prior year

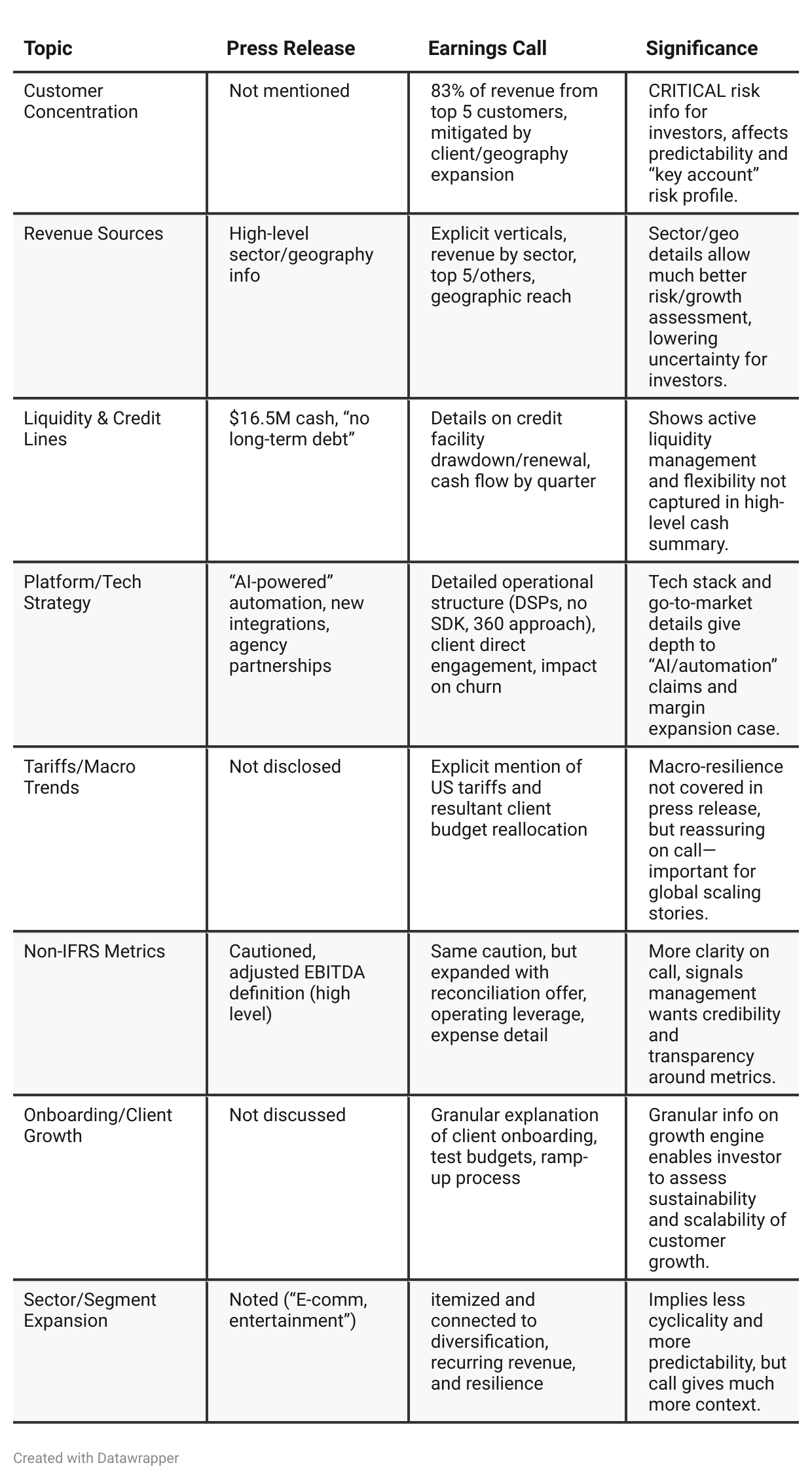

Press Release vs Call Transcript Comparison

Call is far more granular: Operational and customer detail, especially on risk management and sector exposure. Investors get a clearer view of “how” growth is achieved, and its repeatability.

Press release more promotional: Focuses on year-over-year growth, operational “highlights,” and positive messaging, with much less disclosure on customer, segment, or execution risk.

Press release does not discuss customer concentration, macro/trade (tariffs), onboarding/sales pipeline/ramp-up efficiency, or flexible liquidity arrangements (e.g., credit lines)—these are vital for assessment of risk and opportunity, especially in a cyclical sector or with a concentrated client base.

Earnings call addresses questions sent by investors, signaling responsiveness. It also candidly addresses the context behind the numbers, improving transparency.

Disclosure rigor differs: The transcript’s explicit note on recurring revenue, cash flow, and segment deep-dives provides reassurance about business durability that could be missed if relying only on the press release.

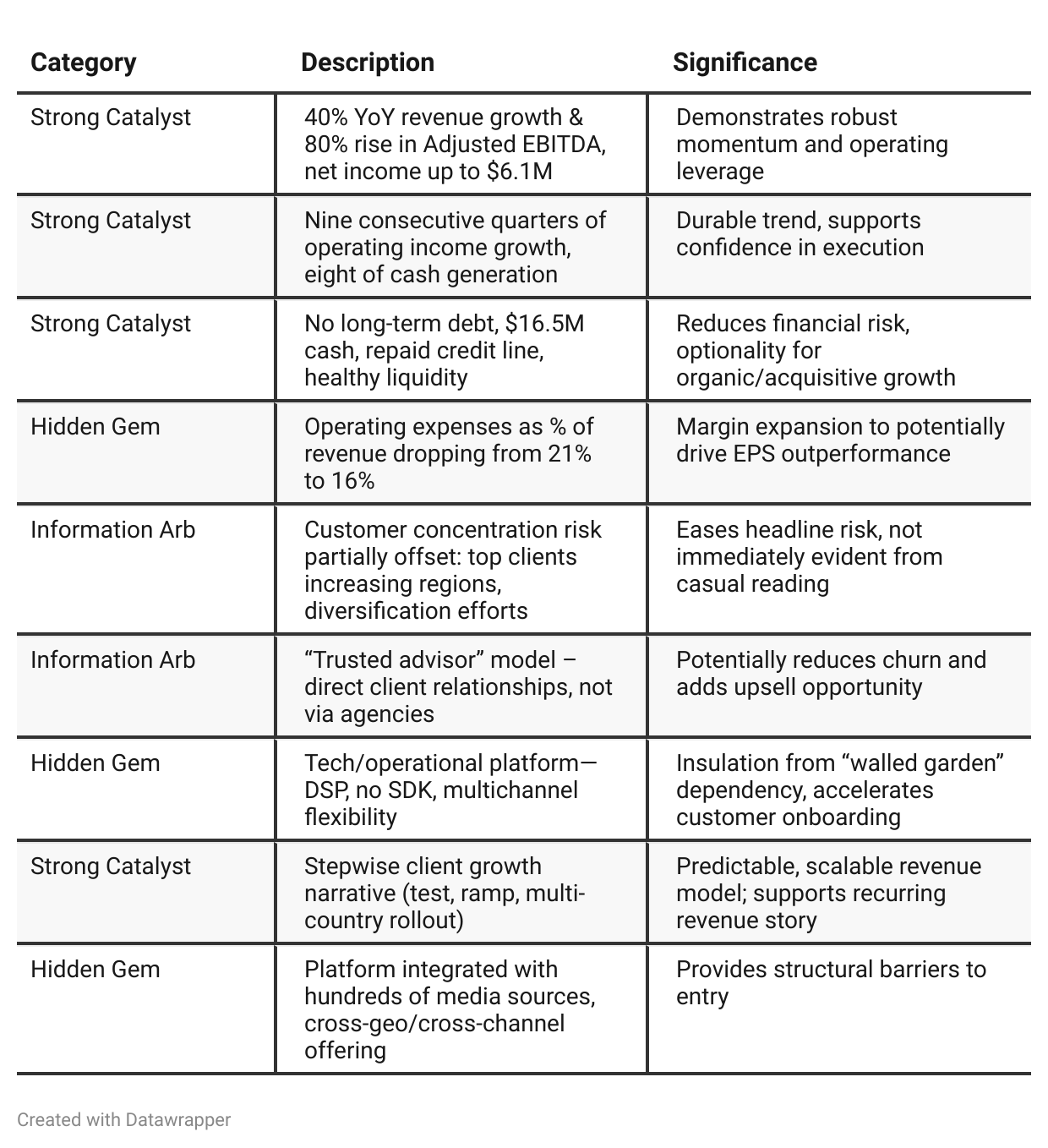

Positive Insights

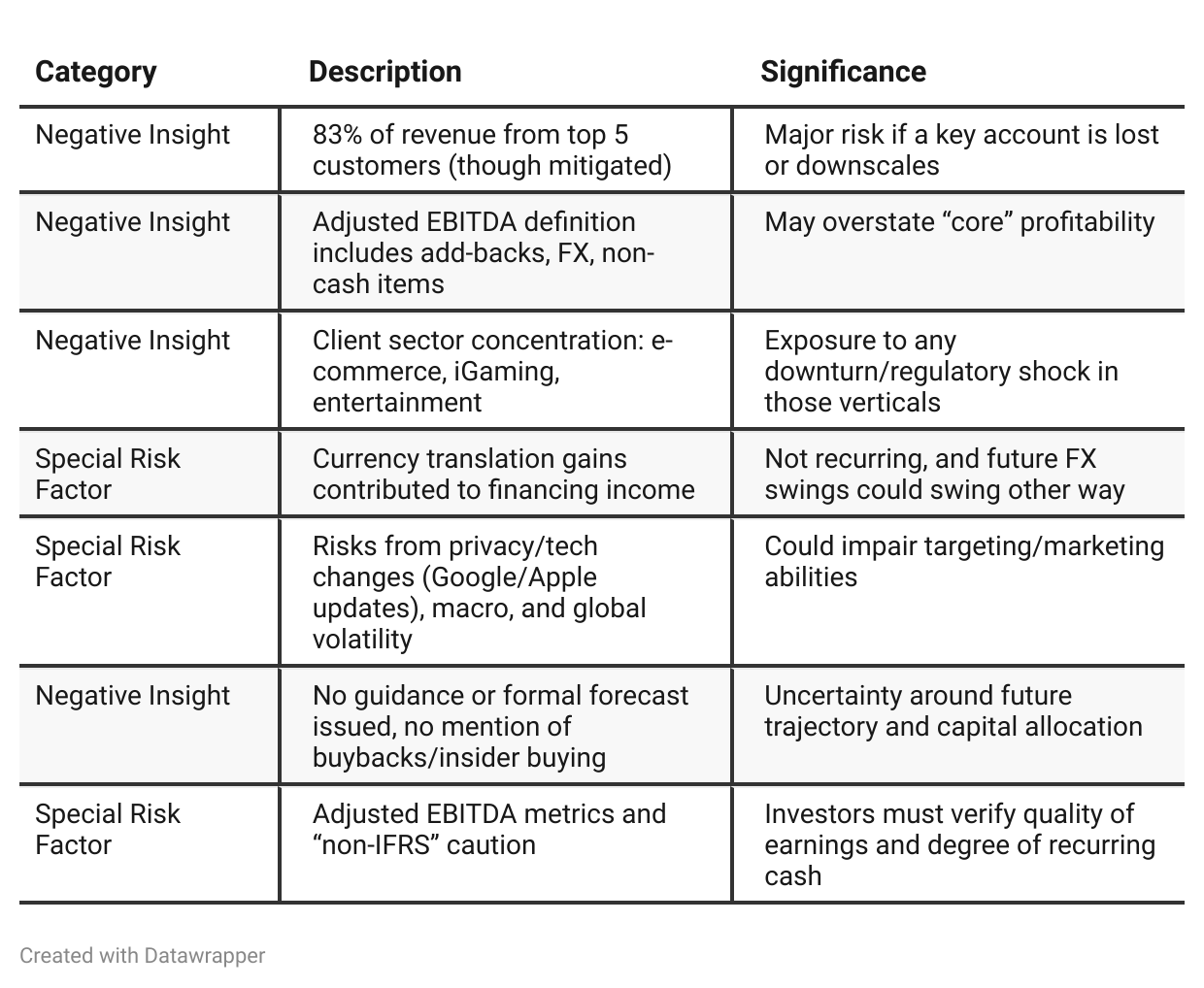

Negative Insights

Tariff Risk

Tariffs Discussion: Management directly addressed US tariff impacts. Instead of a material reduction in overall client spend, there has been a reallocation of marketing budgets away from the US and into other global regions. The geographic diversity of Zoomd’s business lessened adverse effects, resulting in no material negative impacts to date. In some cases, the company captured an even larger share of client budgets due to expansion in other regions.

Mitigation Actions: Zoomd supports clients’ international user-acquisition efforts, proactively adjusting campaign focus across countries. There is no evidence of supply chain disruptions, as the company is asset-light (service/software focus). No need for major renegotiations or changes in pricing strategies was signaled.

Market Share/Innovation Impact: Management stated, indirectly, that the flexibility and global reach of their platform is a competitive advantage during tariff shifts, as they can “capture share” when clients move budgets internationally.

Forward-Looking Projections: No explicit forecast for future tariff effects. Management positioned the company as resilient but acknowledged timing gaps as clients reallocate.

Conclusion on Tariffs: Risk of tariffs appears manageable; if anything, increased geographic diversification and Zoomd’s ability to swiftly redirect client campaigns may even turn macro tariff challenges into an opportunity for incremental market share. Nevertheless, investors should monitor for any prolonged global trade disruptions or shifts in international digital advertising budgets that could eventually impact topline momentum.

Previous Earnings Call

Quarter-over-quarter comparison

From Q1 to Q2 2025, Zoomd Technologies has shifted from a story of rocket-fueled expansion (“over 100% growth!”) and platform scalability towards a more mature, operationally resilient narrative.In Q1, management led with hyper-growth, cost control, and the potential for both organic and inorganic (M&A) expansion, focusing on their platform’s scale and light asset base.

By Q2, the company sought to demonstrate that the exceptional Q1 was sustainable, anchoring the story in consistent, predictable growth. Messaging now highlights recurring revenue, margin gains, and prudent financial stewardship (cash management, credit facility flexibility). Client concentration and sector risk are more transparently discussed, with added attention to external macro risks (tariffs, FX), and the company’s ability to adapt and capture share.

The tone and substance have evolved: from exuberant growth to sustainable, diversified, margin-rich expansion—with a willingness to address latent risks and a focus on maintaining strong internal alignment and a durable financial base.

Year-over-year comparison

From Q2 2024 to Q2 2025, Zoomd Technologies’ story has evolved from a turnaround success—focused on cost-cutting and financial survival in a tough macro climate—to a self-confident growth and scalability narrative. The company, having rebuilt itself post-restructuring, now presents as a margin-rich, cash-generative enterprise with expanding global reach, improving client “stickiness,” and operational sophistication. Management’s tone and priorities have shifted from defense to offense: cost control gave way to strategic investment, crisis management to seizing market opportunities (including those created by macro volatility), with investor communications now more transparent about risks, especially client concentration. The strategic story is now “how high can we scale,” not “can we survive.”

Final Takeaway

Zoomd Technologies is in a growth and margin expansion phase, leveraging a focused strategy in digital marketing across high-growth sectors and diverse geographies. Strong cash flow, improving profitability, and an innovative tech platform are positives. However, a high degree of customer and sector concentration and reliance on adjusted earnings metrics warrant caution. Continued progress on diversification and recurring revenue, and transparent reporting on cash quality and sectoral exposure, will be critical. Verdict: Hold, with upside as diversification efforts and sustained growth are proven; mindful of concentration risks.